Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we’ll cover this week:

Macro: Non-Farm Payrolls, Productivity

Markets: Growth to Value, Eli Lilly

Company Earnings: Tech & Consumer - Strong Earnings, Revenue growth

AI: Hollywood Taps AI, Broadcom and Datacenter Spend

This week, we had a great conversation with Mark Mahaney.

Mark Mahaney is a senior managing director and heads Evercore ISI’s Internet research team.

Mark has covered internet stocks for over 25 years.

He has been ranked as the #1 Tech analyst 5 years in a row by Institutional Investor and is the author of Nothing But Net: 10 Timeless Stock-Picking Lessons from One of Wall Street’s Top Tech Analysts.

We discussed Mark’s investing framework and how he hunts for the next 10Xers in this space.

Subscribe to watch the full episode below on your favorite platform.

It airs at 2 PM ET.

Remember to like and subscribe. Apple and Spotify links get updated after the show airs. You can subscribe to our podcast page below to be notified.

It helps us grow and interview experts like Mark.

A September to Remember

What a week. Last week we noted:

Each Sunday we do a review of our chartbook to look for good entries and exits.

That led to this post shared last Sunday evening where we reiterated this message:

We are now about 3 weeks since the Aug 7 lows where we noted ‘equities should be higher in 1 to 3 months’.

We were bullish then on risk/reward, and now I don’t see attractive risk/reward… Tactically reducing net long exposure seems like a good idea until earnings season starts in October.”

Overall, we believe we are in a correction (again) and we will get an all-clear somewhere around earnings season in October.

Something I want to comment on is this ‘hot ball of liquidity’ we observe in markets. We continue to see market moves that ordinarily would play out over longer-time frames take place in shorter timeframes.

That’s adding to volatility.

It’s not healthy for markets, and we saw that behavior in the 2020 and 2021 timeframe - the era of massive Covid stimulus and the rise of Robinhood.

Take a look at Robinhood stock. It’s a classic tell for ‘Animal Spirits’, which we believe is linked to investors’ willingness to pay for high multiples.

These animal spirits topped on July 16th along and never fully recovered after the August 7th Yenmageddon flash.

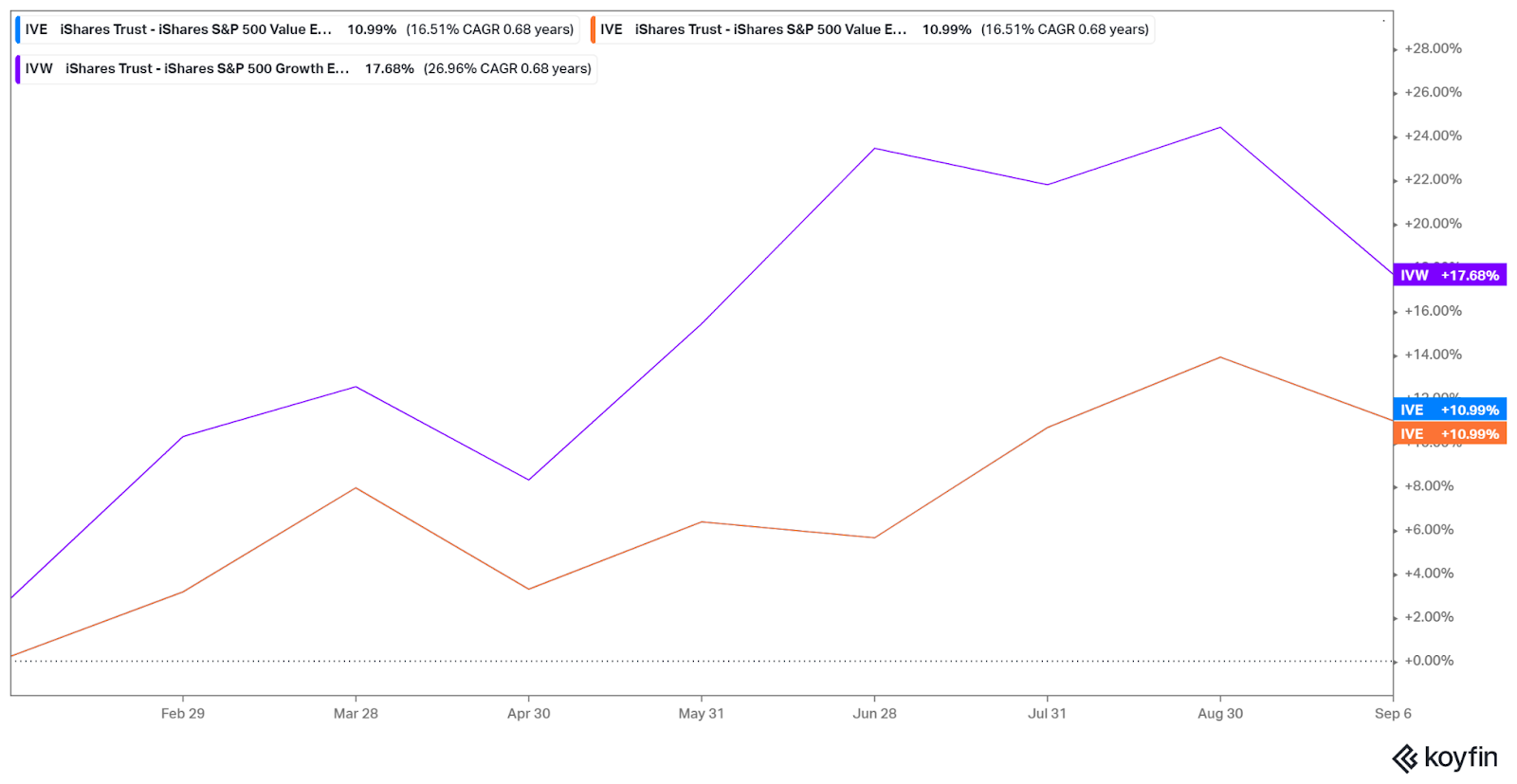

What has recovered is Value stocks.

This is a comparison of the S&P Value vs. S&P Growth index. Value is substantially out-performing growth.

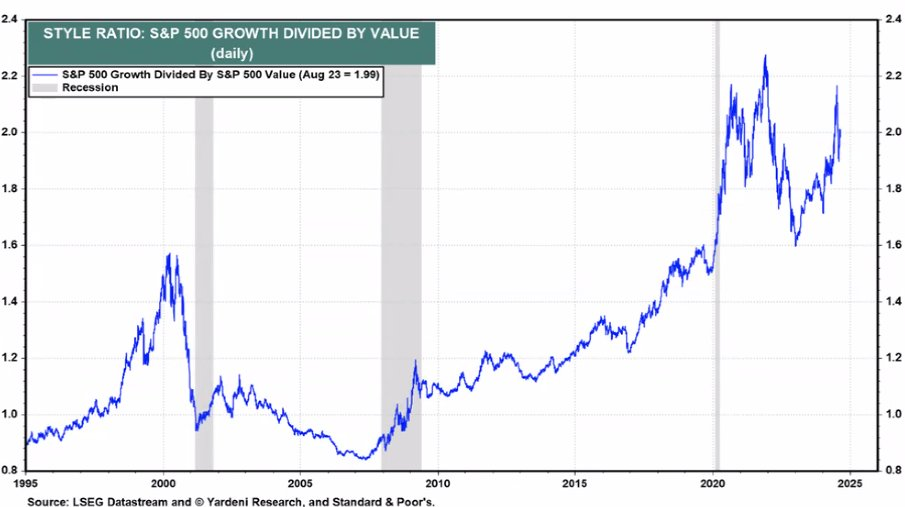

Recall that, at the top of the year, we noted that tech stocks are in the top decile of historical valuation.

Valuations are terrible for timing, but they do exert these positioning effects as investors make millions of decisions on the margin.

That’s the reason why Microsoft is lagging the S&P – it’s over-priced and due to its Consensus AI status.

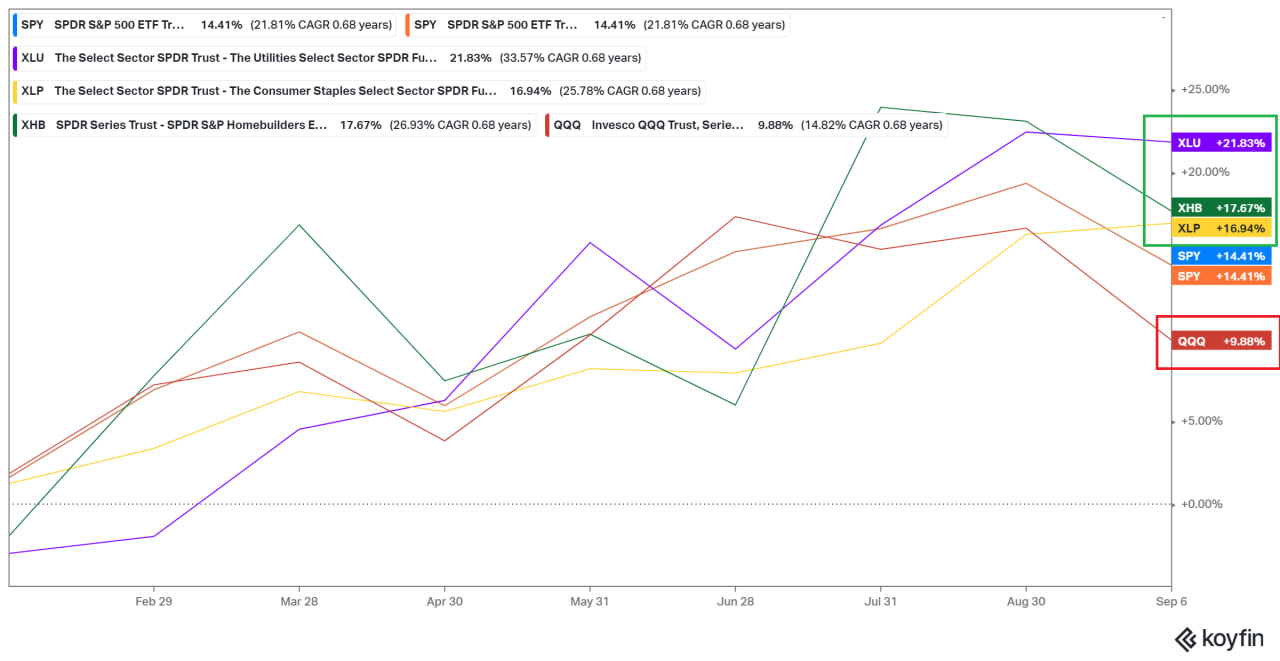

Notably, what we have seen work are rate-sensitive categories: Utilities, financials, homebuilders, and Defensive categories such as consumer staples.

Until this Friday, these categories exhibited the strongest short-term and YTD momentum.

Notice that value-oriented sectors are out-performing tech-heavy categories such as QQQ substantially.

We believe this is the effect of anticipated rate cuts (maybe all priced in now?) and over-valuation in the tech-heavy Nasdaq.

The inability of tech-names like Z Scalar and Nvidia to rally on strong earnings suggests that expectations are too high.

Although tactically (e.g, 1 to 2 week timeframe) we believe Growth is oversold, the higher level concept of rotating from Growth to Value is an enduring trend.

This is a thesis we started writing about in the Spring after we saw this chart and the inherent mean-reversion:

Major macro events - such as changes in the stance of monetary policy or the onset of a new technology (such as GPT) can spark these shifts.

Whatever the cause, it is here and investors should overweight quality value.

That doesn’t mean do not own growth. We believe several of the Mag 7 names deliver extraordinary business models combined with predictable earnings growth.

We still like Nvidia, Meta, and Google, and we shudder at the thought of owning cloud stocks that are priced in the stratosphere.

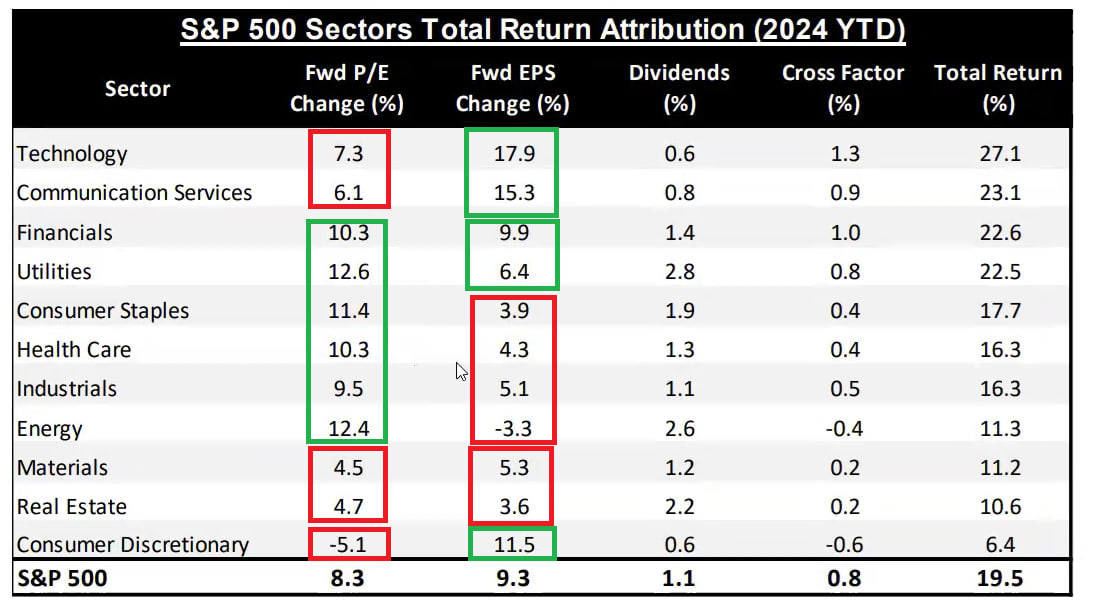

This chart shows the synthesis crisply.

Notice that the top two categories - Technology and communication services - have the highest earnings growth.

We love earnings growth. (Recall Communication Services includes our favorite monopolies, Google and Meta).

But we don’t get multiple expansions out of those categories. They are already priced expensively.

Multiple expansion explains about 50% of stock price returns and earnings growth of about 33% over long-run statistical studies. Ideally, we want both.

Tech names can and should continue to grow earnings – but don’t bet on multiple expansions.

Then you have Goldilocks categories such as Financials and Utilities, which have benefitted mostly from multiple expansions and earnings growth.

The second-best industry group YTD is Insurance. We believe Insurance will continue to perform extraordinarily well.

We did an exercise a few months ago to find the best insurance names. We bought names like Jackson Financial and CoreBridge, which both sell annuities to retirees. (We also like Property & Casualty).

We looked back at the initial basket – the whole basket re-rated higher…

Insurance is overbought, but we like that category very much. Few people are talking about it (other than Buffett who bought Chubb).

Insurance companies also have the green light from state regulators to pass on price increases to their customers.

And the insurance companies' balance sheets are ‘levered’ to a steepening yield curve.

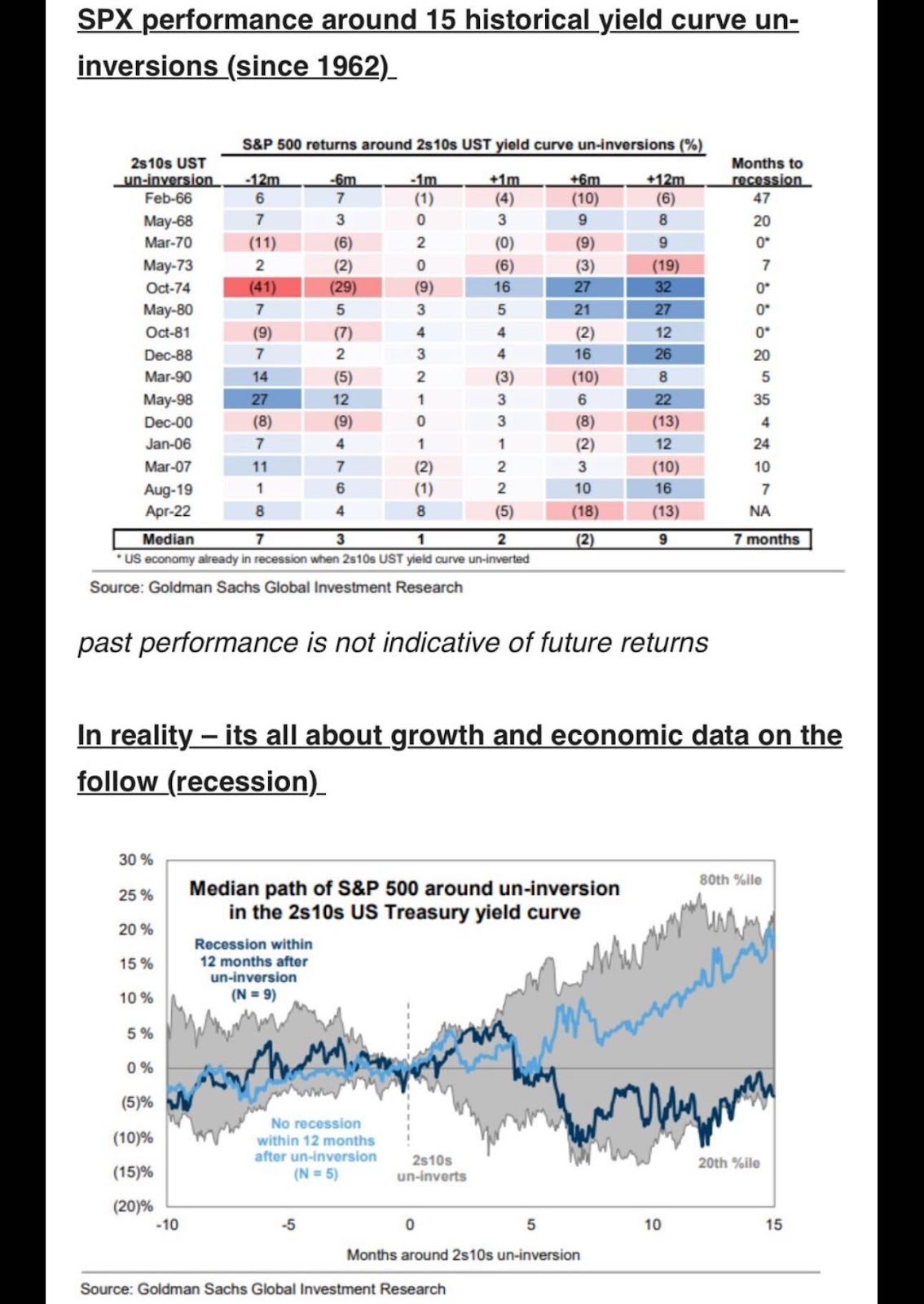

Speaking of yield curve uninversions - we are having one now.

There is a lot of scary data showing that yield curve uninversions are associated with bear markets and recessions.

The key question is the prospect for economic growth.

We believe the economic growth story is intact.

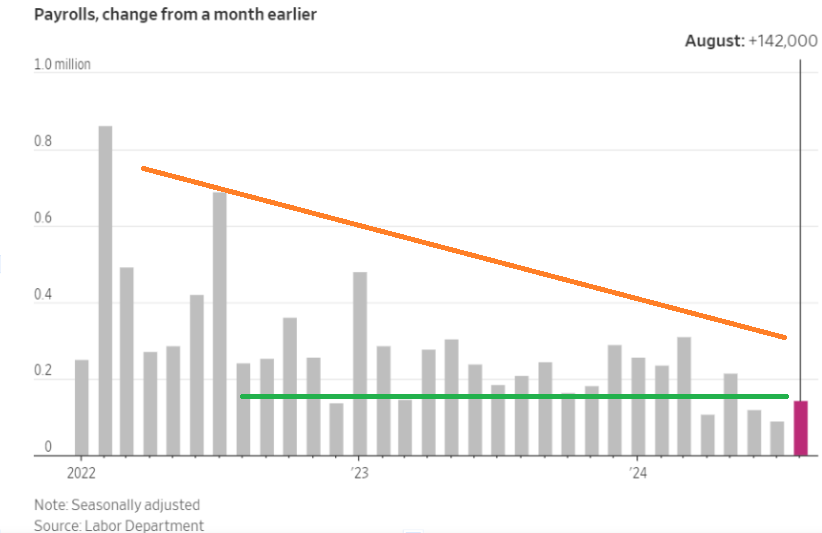

This past Friday, the Non-Farm Payrolls report (aka Monthly Superbowl) clocked in at 140K for the month of August, below the whisper of 150K and Consensus of 160K.

The unemployment rate clocked in at 4.2%, meeting the Consensus.

The report came in somewhat softer than expectations. Now, this is also a survey with statistical adjustments.

Markets tanked on the news, most likely due to the orange trendline here:

We are of the camp that the green line is more relevant - this is the normalization story.

The NFP doesn’t give enough ammo to the Fed to cut 50 bps either - those odds dropped to 30%.

Mr. Market today has shifted concerns from inflation to growth.

- The 10-year is at 3.7% down from 4%+ for most of the last 12 months

- Crude oil is testing multi-year lows

- Cyclicals like energy stocks and growth are oversold

- Defensive are overbought (e.g., healthcare and staples)

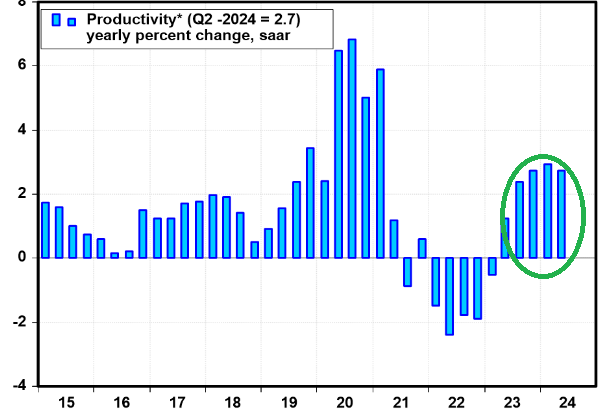

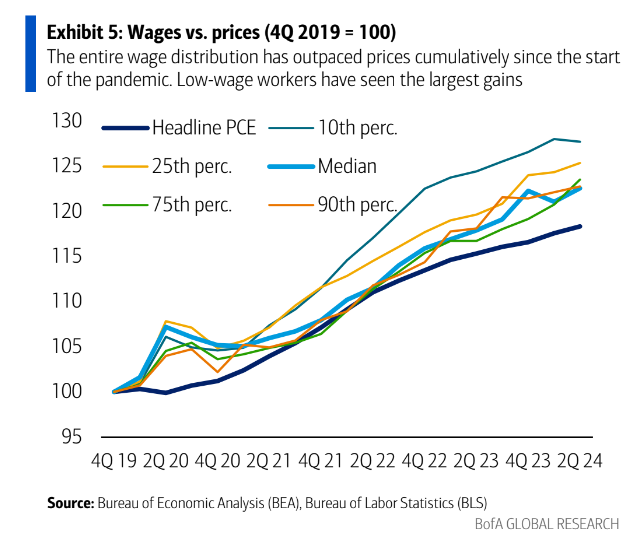

We believe the story that is missing here is the Productivity Boom.

Employment growth is softer due to growth in productivity rates:

Usually, you see a productivity spike after mass layoffs in a recession, such as we saw in Covid.

Productivity growth is the one free lunch in economics – it enables higher wages and corporate profits.

And we are seeing both!

However, there’s less need to hire workers when your existing workers are more productive.

From our vantage point, the economy continues to look good:

Initial claims are declining

Corporate profits are beating expectations

Visa credit card spend YOY is around 4% (2019 levels)

Retail sales beat two months in a row (another release this Tue)

GDP = Labor * Labor Productivity

Both of those numbers are increasing.

Should we be concerned about the Uninversion of the Yield Curve?

Does that mean recession ahead?

Isn’t that indicator infallible?

Correlation is not causation.

A mechanical rules driven approach is comforting.

We can stop thinking and just do what the indicator says. But, that’s a mistake.

At the end of the Dotcom era, we had an inverted yield curve.

There was a massive Y2K capex binge, fiber splurge, and VC binge.

The DotCom recession was caused by the unwinding of excess investment.

We had a recession in the DotCom era driven by reversals in capex spending and an increase in unemployment in tech and telecom.

The 2008 crisis was preceded by an inverted yield curve.

This episode was marked by excess investment — however, this time it was driven by consumer investments in residential real estate

…and fueled by cheap credit and Wall Street’s securitization machine.

The unwind started with a credit crunch.

Where we stand today, we have capex growth around AI/datacenters and infrastructure bills such as CHIPS Act and IRA Act.

These programs are funded by cash flush hyperscalars and governments spending at wartime deficit levels.

That spend is not stopping.

Is there a credit crunch from high rates? Doesn’t something need to break?

Yes, we have a credit crunch and pain in commercial real estate. There are many assets that have upside down capital structures.

We continue to see assets trade at substantial discounts to their last print.

We may have two more years to go to fully digest this and get past the ‘Pretend and Extend’ game that banks are playing perhaps tacitly with regulatory support.

What’s different this time is that the damage is in the private markets - not in DotCom stocks or bank stocks.

So, everyone is conditioned for the shoe to drop and waiting for ‘long and variable lags’ when the shoe already dropped.

Rate cuts help consumers and small businesses.

And the economy is running at a 55 MPH speed.

Don’t confuse correlation with causation.

Maintain perspective.

If you are looking for a wealth management partner, Lumida is now welcoming a limited number of new clients.We offer a range of services, alternative investments (such as our CoreWeave deal), white-glove crypto management, to public equity management, and high-touch family office services, including trust, tax, and estate planning.

Ready to explore? Click here to fill out our form to start the discovery process.

EQUITY

So much doom and gloom on the timeline.

Take a look at Broadcom’s CEO AVGO on datacenter spend in the earnings call:

‘In our fiscal Q3 2024, consolidated net revenue of $13.1 billion was up 47% year on year, and operating profit was up 44% year on year.

These strong results reflected three key factors.

One, AI revenue continues to grow and grow strongly.’

Does Datacenter spend look like it is about to suddenly stop?

Focus on the big trends.

Don’t get distracted by the noise.

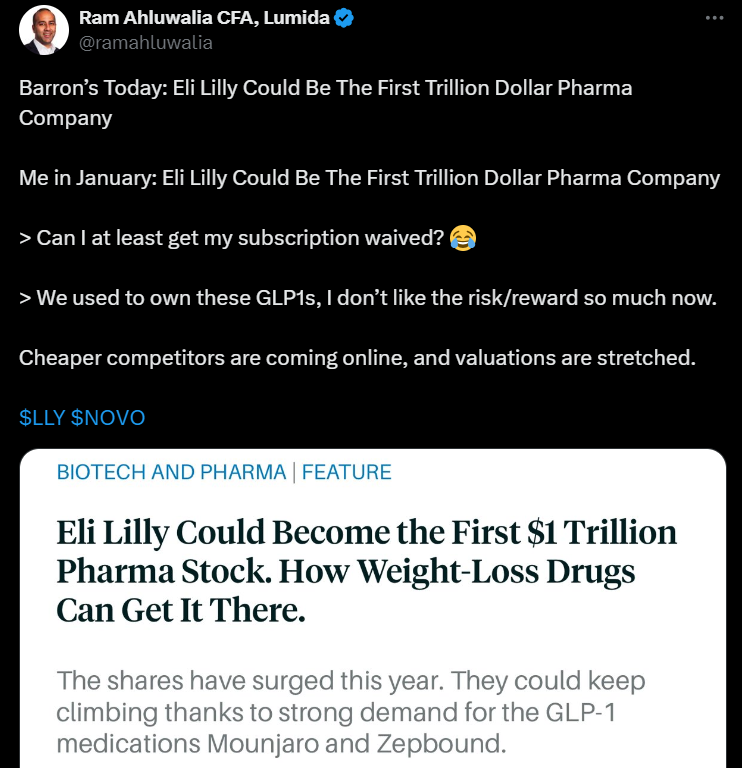

On Eli Lilly:

Barron’s Noted last weekend that Eli Lilly Could Be The First Trillion Dollar Pharma Company

We noted in January: Eli Lilly Could Be The First Trillion Dollar Pharma Company

Our thoughts here:

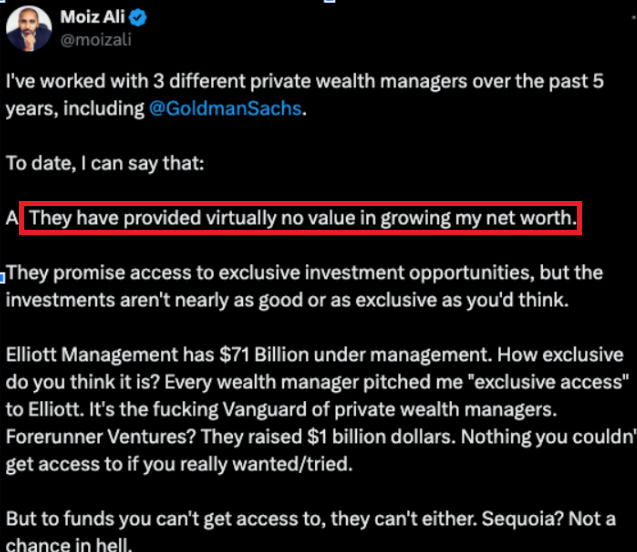

Goldman Sachs Private Wealth Business:

A twitter fellow took this axe to Goldman’s Private Wealth Business.

Their conclusion is that Goldman’s private wealth “has provided virtually no value in growing my net worth.”

How is Goldman on alternatives?

Did they offer CoreWeave? No.

Did they offer Brad Jacobs QXO? No.

These frustrations are why I built Lumida Wealth.

Incidentally, we have a page focused on one-off deals at Lumida Deals

We are assessing our next deal.

Click here if you are interested to know more and are a Qualified Purchasers & Accredited Investors only.

Like our other deals, I will be investing personally in this as well.

This is not an offer to buy or sell a security. See terms and conditions on site.

Company Earnings

Technology, Media, Telecom:

Asana (ASAN): Earnings and revenue beat. Revenue up 10.3% YoY. Record multi-year deals highlight strong customer commitment and future growth potential.

Zscaler (ZS): Earnings and revenue beat. Revenue up 30.3% YoY. Robust full-year fiscal 2025 guidance significantly exceeds market expectations.

Broadcom (AVGO): Earnings and revenue beat. Revenue up 47.2% YoY. Strong Q4 2024 guidance, bolstered by VMware contributions, supports continued growth.

DocuSign (DOCU): Earnings and revenue beat. Revenue up 7% YoY. Q3 guidance slightly above consensus, indicating steady demand for digital solutions.

Consumer Discretionary:

Dick's Sporting Goods (DKS): Earnings and revenue beat. Revenue up 7.8% YoY. Raised full-year guidance reflects confidence in continued sales growth.

Sector | Company ticker | Beat or Miss (Relative View) | Revenue (Absolute View) | Highlight | Links |

Technology, Media, Telecom | Asana (ASAN) | Earnings beat by 37.5%, Revenue beat by 0.87% | $179.21M, up 10.3% YoY | Record multi-year deals were signed, indicating strong customer commitment. | |

Technology, Media, Telecom | Zscaler (ZS) | Earnings beat by 27.5%, Revenue beat by 4.45% | $592.9M, up 30.3% YoY | Full-year fiscal 2025 revenue guidance significantly exceeds consensus. | |

Consumer Discretionary | Dick's Sporting Goods (DKS) | Earnings beat by 13.2%, Revenue beat by 1.17% | $3.47B, up 7.8% YoY | Raised full-year 2024 guidance for comparable sales growth to 2.5% to 3.5%. | |

Technology, Media, Telecom | Broadcom (AVGO) | Earnings beat by 2.5%, Revenue beat by 0.85% | $13.07B, up 47.2% YoY | Q4 2024 revenue guidance is approximately $14.0 billion, including contributions from VMware. | |

Technology, Media, Telecom | DocuSign (DOCU) | Earnings beat by 19.8%, Revenue beat by 1.12% | $736M, up 7.0% YoY | Q3 revenue guidance set between $743M and $747M, slightly above consensus. |

AI

Productivity Growth and AI

Have you seen the Netflix documentary about Andy Warhol?

They used AI to resurrect Andy's voice and read his own diary in his own voice.

AI is here in many small ways already.

I spoke to a VC who is using AI to process deal data

We use AI to build bull/bear cases and other analysis.

AI is here for leading firms and they will take share and benefit from productivity growth.

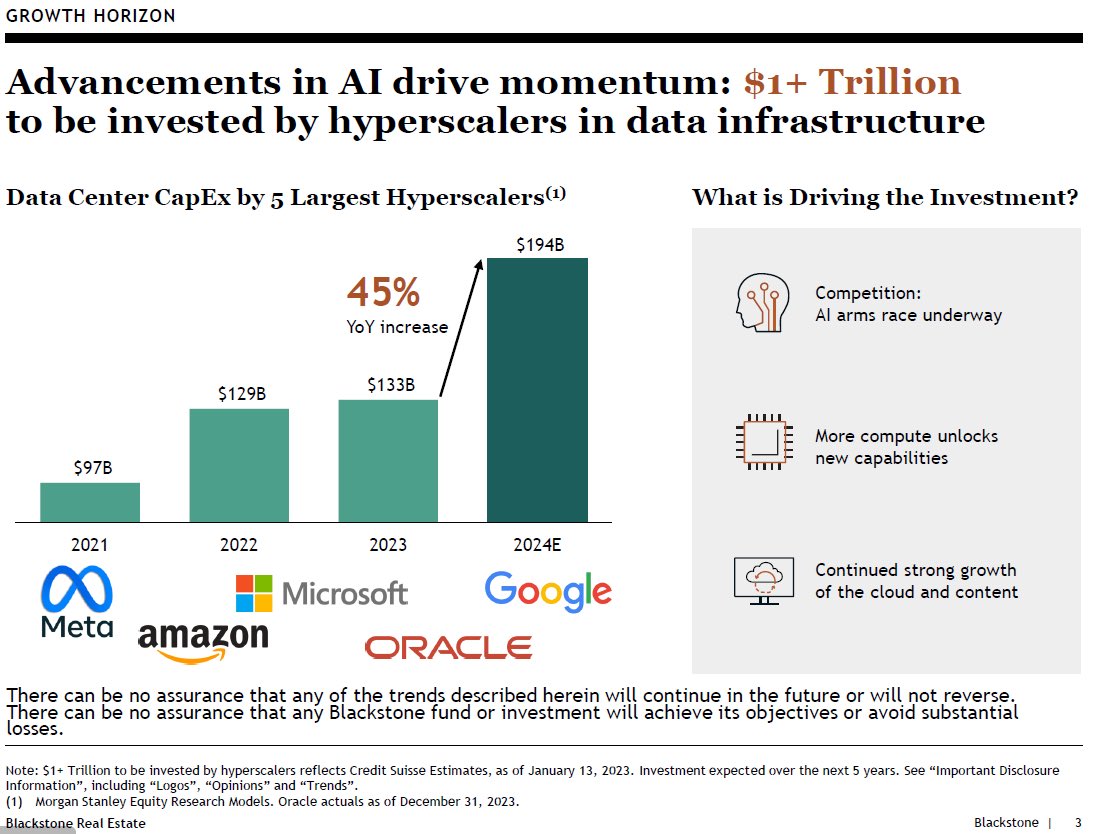

Blackstone did a nice job of summarizing our Semicondcutor CapEx Receiver Thesis in one slide

The datacenter spend is not slowing anytime soon

Multiples are compressing though as capital rotates to value

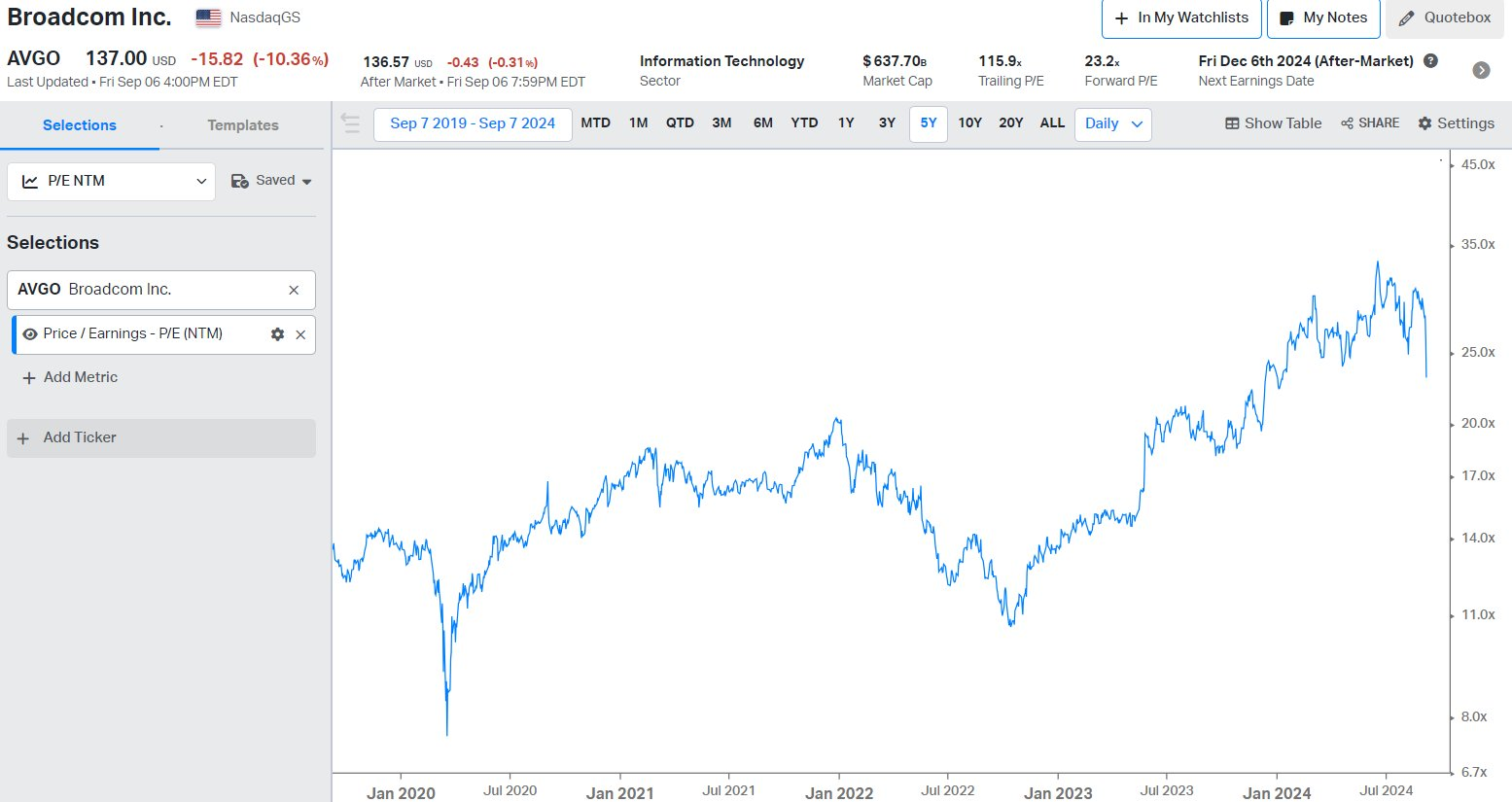

NVIDIA, Broadcom & Custom Silicon

Do you recognize the guy on the left?

He has more hair than I do, but looks kind of familiar...

We noted last week one of the top 3 risks to Nvidia is Custom Silicon.

Broadcom CEO leaned into that heavily on their earnings call.

"I used to think that general-purpose merchant silicon will win at the end of the day... I flipped in my view. And I did that, by the way, last quarter."

Full quote below...

"I used to think that general-purpose merchant silicon will win at the end of the day. Well, based on history of semiconductors mostly so far, general purpose, small merchant silicon tends to win. But like you, I flipped in my view. And I did that, by the way, last quarter, maybe even 6 months ago. But nonetheless, catching up is good.”

Broadcom dropped 10% on earnings and is near its 200 day moving average.

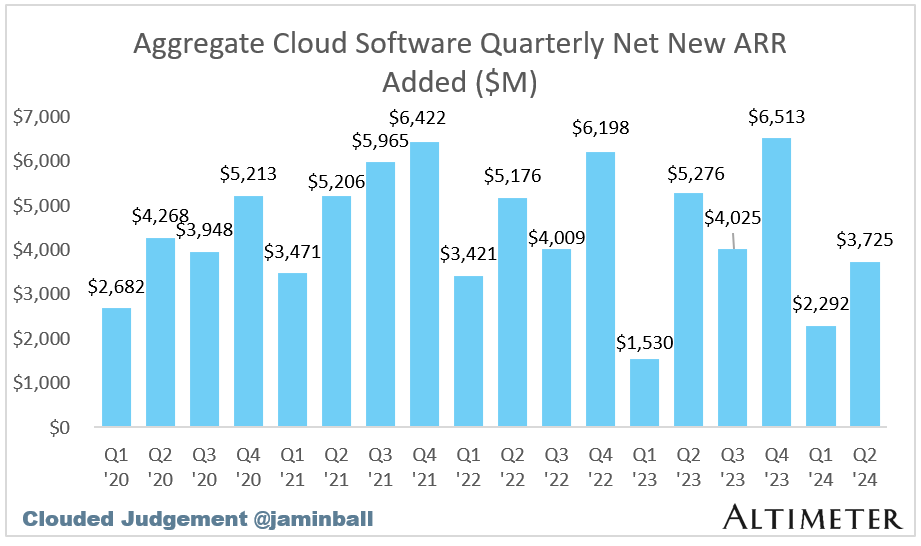

SaaS is Still Dead

As you may know, we’ve been bearish on SaaS.

These supposedly capital light business models need to binge on GPU chips to stay relevant,

Take a look at this chart showing Net New ARR spend topping out.

Now take a look at Cloud stocks in the WCLD ETF.

Lumida Curation

In case you missed it, here are some of the best curations from Lumida Wealth on Twitter.

Be sure to follow Lumida Wealth on Twitter, and on Youtube, where you can get more such curations.

Instead of watching hour-long market podcasts - we distill the key insights in 1 min shorts and serve them in threads.

The goal is to maximize insight per unit of time.

Click below to see the 7 best-threaded insights.

Quote of the Week

“The individual investor should act consistently as an investor and not as a speculator.” – Benjamin Graham.

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.