Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we’ll cover this week:

Macro: Initial Claims, GDP, Inflations

Markets: Due for a breather? Staples overbought

Company Earnings: Tech - Strong, Consumer Mixed Performance

AI: Nvidia roundtrip trade with OpenAI?

This week was eventful; we discussed the impact of Jackson Hole on the markets.

We expanded our thesis on the Growth vs. Value rotation, AI & Nvidia, and the state of US Consumers.

Click here to watch & don’t forget to subscribe to Lumida Non-Consensus Investing.

WOYM: Jackson Hole, Growth vs. Value, AI & Nvidia, US Consumer

Timestamps:

02:21 Employment and Retail Outlook

03:03 Historical Rate Cuts and Market Dynamics

05:29 Value vs. Growth Investment Dynamics

07:47 Real Estate and Financial Sector Observations

10:31 Small Caps and Debt Dynamics

11:57 Technological Growth and Market Trends

13:19 AI and Productivity Growth

17:29 Banking Sector Insights

20:16 US Consumer Trends and Retail Shifts

22:31 Housing Market Dynamics

25:16 Auto and Retail Insights

29:50 Lumida AI Test Drive

31:00 Google and AI Integration

33:02 Market Seasonality and Rate Expectations

WOYM: Macro, Nvidia Earnings, Lululemon vs. Abercrombie, SMCI vs. DELL

In our latest What’s On Your Mind, we discussed NVIDIA earnings, macroeconomic data, recession fears, and a market shift from growth to value stocks.

We analyzed retail sector performance featuring companies like Abercrombie & Fitch, Ulta, Lululemon, and showcase LumidaGPT, which aids our investment research.

Click here to watch & don’t forget to subscribe to Lumida Non-Consensus Investing.

Timestamps:

00:34 Recession fears, GDP components & consumer strength

05:06 Growth to Value Rotation in Stock Market, S&P500, Berkshire Hathaway

08:11 Strategic investment opportunities

12:08 Tactics for Superior Market Returns

15:49 Nvidia Earnings and Market Projections

22:31 Nvidia Revenue Projections and Risks

29:18 Custom Silicon and Competitive Pressures

33:00 Semiconductor Market Dynamics & Industry Monopolies

37:17 Dell and Semiconductor Supply Chain Strategies

41:00 Retailer Performance: Lululemon, Abercrombie & Fitch, & Ulta

49:09 Lumida AI Test Drive on Hasbro

Macro

We’re now nearly a month from the August 7th Monday mini-crash.

We noted on the Sunday before that we should expect higher equity prices one month and three months higher.

That’s certainly the case!

And we had further macro data supporting our thesis that there is no recession.

On Thursday, we saw jobless claims beat expectations and recede.

We saw GDP beat expectations.

We saw inflation numbers continue to improve.

On the back of strong GDP, we saw continued breadth expansion – tech is lagging after a sharp off-the-lows bounce and the rest of the market is catching.

We discussed this in a special video this Friday.

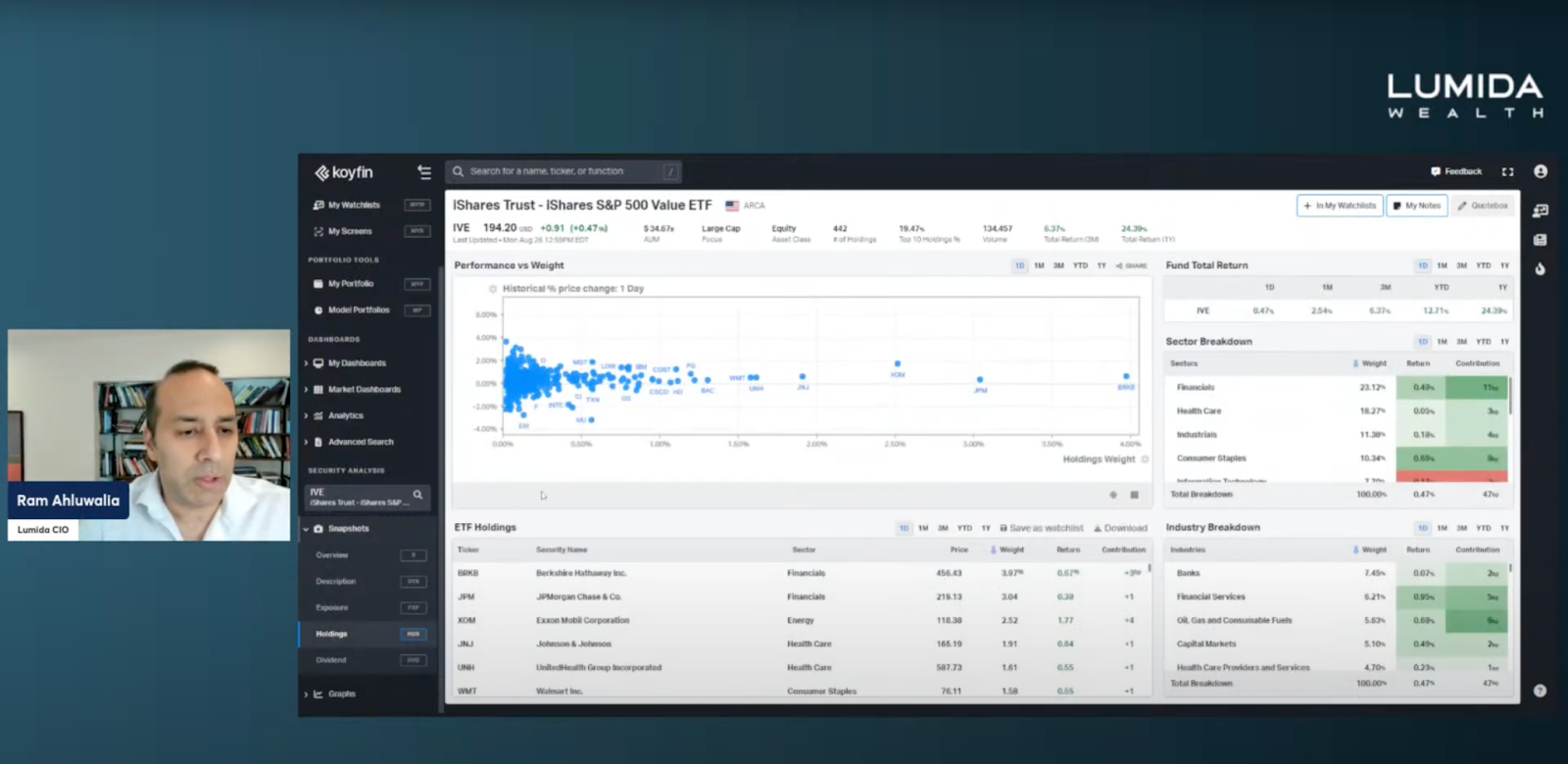

Note that the S&P and Dow Jones are around new highs, whereas Nasdaq QQQ has failed to recover fully.

I expect value to continue to out-perform growth, and continued breadth expansion. This is a core thesis, and we are positioning it by tilting it towards our portfolio.

Fears of recession continue to pervade the market. Look at Defensive sectors such as Staples, Utilities, and Healthcare.

They are all near their 52-week highs at the index levels.

I expect next Friday’s non-farm payrolls report to reverse last Friday’s August surprise and cause investors' tight grip on Defensives to relax.

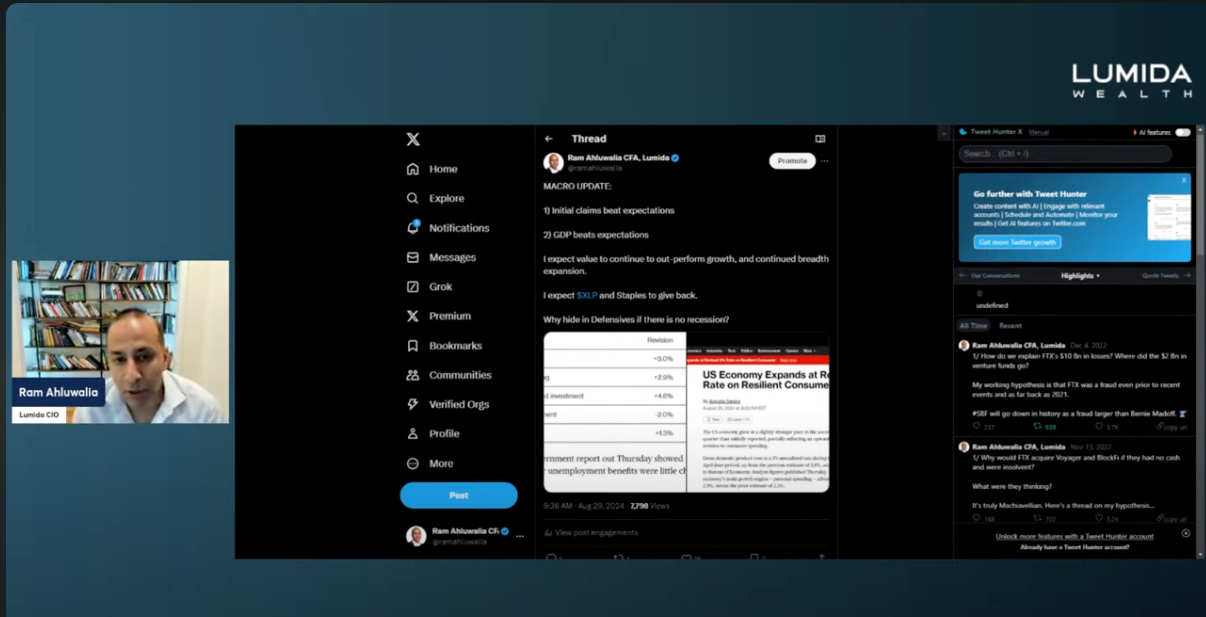

I expect Consumer Staples to give back and cyclicals to come to the fore.

Why hide in Defensives if there is no recession?

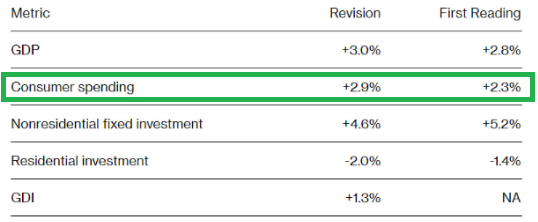

The GDP report shows that Personal Spending grew faster than expectations.

We also saw better than expected results from Lululemon and one of our holdings Abercrombie and Fitch. Listen into the 40 minute mark here for a deepdive.

Latest Thoughts on Nvidia

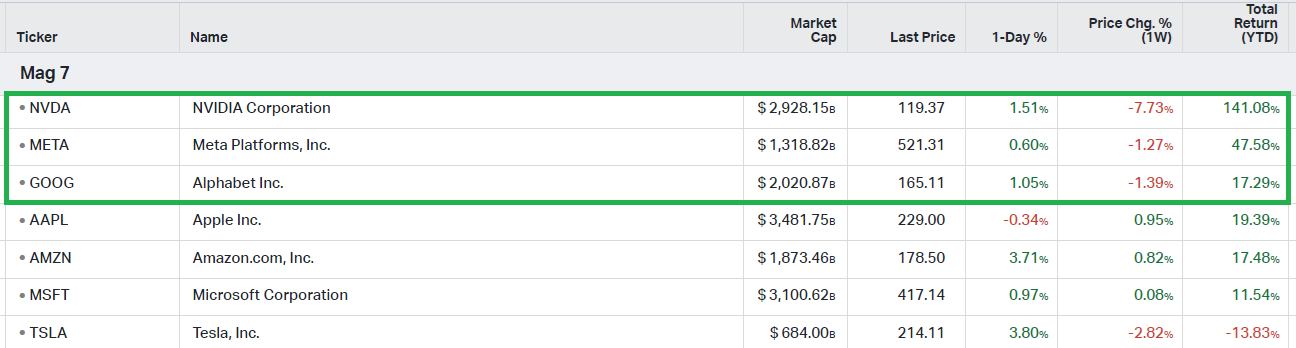

As long-time readers know, our favorite growth stocks and top holdings include Nvidia, Meta, and Google.

Let’s walk you through our thought process and explain why we believe Goldman Sachs is underestimating the upside here. Note: GS has a $135 price target looking 12 months out.

They are sandbagging.

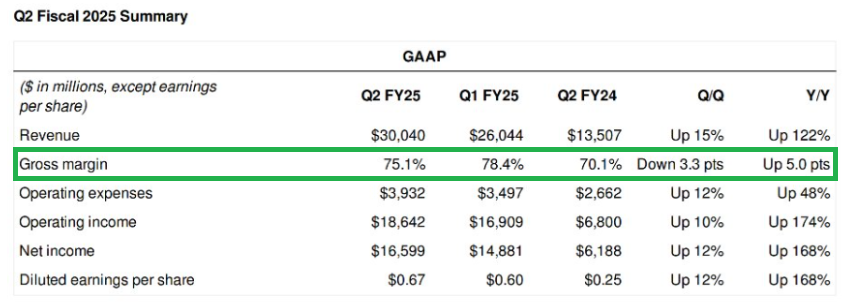

First off, Nvidia delivered a double beat. The results were strong.

However, the stock finished down a few points.

The stock finished inside the option implied volatility bands. That means the house, Citadel, took the money of YOLO traders buying calls and puts again on wild stock price moves.

(That’s the second quarter in a row that’s happened since we started tracking this).

Back to the fundamental story.

The big story with NVDA is that datacenters spend up 122% YOY.

Automotive growth was solid in the #2 position.

We should note this segment represents a real risk for Tesla - Nvidia will become the arms dealer for driverless, enabling legacy ICE players to catch-up.

As they say, you can identify the pioneer because they have all the arrows in their back.

Why was Nvidia down?

Margins compressed from ~80% to 75%.

If you recall, a few months ago, we had noted that their foundry partner, Taiwan Semiconductor, indicated they wanted to raise prices.

Nvidia ate the price increase and was unwilling to pass it on to their customers Microsoft, Meta, and Google.

We should also note that Microsoft’s stock price, a Consensus AI name, is up only 9% this year.

And their margins are compressing as they spend a lot of money on Nvidia chips to power OpenAI.

Nvidia took one for the team. They are trying to find the right balance between value capture and not eye-gouging customers who can build their own custom silicon over time.

Nvidia's Jensen had this to say about demand:

“Hopper demand remains strong, and the anticipation for Blackwell is incredible."

One of the most humble guys on the planet is making statements that are anything but humble.

On Blackwell Platform:

Expected to ramp up production in Q4 FY 2025, with several billion dollars in revenue anticipated from this architecture.

China Market: Data center revenue from China grew sequentially, but the market remains competitive due to export controls.

Jensen is also saying ROI on AI capex spend is here.

We agree!

We saw that in Meta’s last earnings transcript. Zuck is seeing greater ROI due to improved AI targeting of ads.

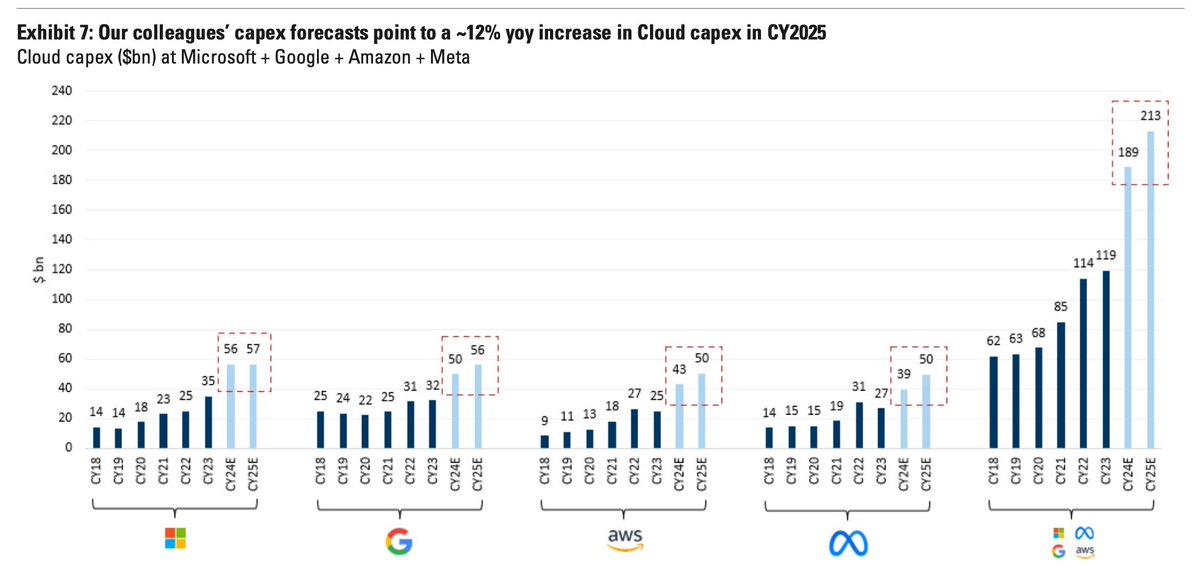

Take a look at Cloud Capex spend forecasts across hyperscalars.

These are high-quality customers with loads of free cash flow. They compete to own the future in a high-stakes competition with one another.

The cost of losing is $1 Tn to your market cap.

How much will you spend to avoid taking a $1 Tn hit?

A lot.

This is the Operating Income for Big Tech...and it's growing by double digits.

MSFT - $110 billion

META - $60 billion

AAPL - $120 billion

GOOG - $100 billion

AMZN - $50 billion

Nvidia which has about $96 Bn in sales is eating into these firms operating income, and also helping these firms gain an advantage.

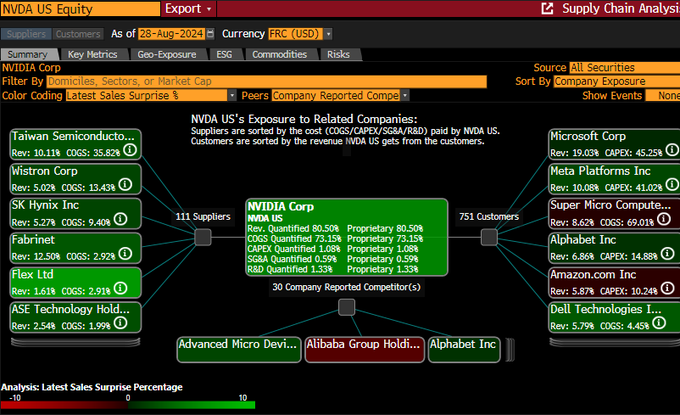

Here's a visual breakdown of Nvidia's suppliers and key customers

(Note this estimate. Surprised to see Micron not here.)

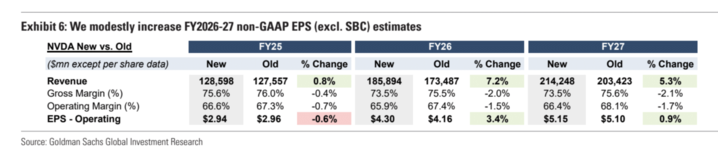

Here is Goldman's EPS forecast for Nvidia.

Goldman sees a decline in revenue growth into the teens in a few years - we think that's a mistake.

We see continued 20% revenue growth for several years to come.

Our fair value model pegs Nvidia at a fairly valued around $120 / share - not too far off from where it is now.

However, in 12 months, we expect a $200 price target. That is much higher than Goldman's price target of $135.

For those keeping scores, Goldman has a 12-month price target of around $1,000 ($100 split-adjusted in April). Prices hit that price target and blew past that well ahead of schedule.

That will happen again due to continued earnings growth. AMD can’t hold a candle, and Intel is trying to sell its foundry business.

The risk to that is a Chinese invasion of Taiwan.

Here are the biggest risks to our thesis:

Custom Silicon

The hyperscalers loathe spending this much money on Nvidia.

And MSFT, Amazon, and Google all know how to make chips.

BUT, today, custom silicon is primarily for internal uses (e.g., serving better ads on Instagram).

CUDA Disruption

There are firms creating a middle-ware in an attempt to displace CUDA by having a translation layer.

CUDA is the moat.

Competition

In a few years, we see certain startups credibly displacing a portion of Nvidia revenues.

We remain bullish on Nvidia, Meta, and Google - although Google today offers the best entry.

Here’s a chart of Google’s Trailing PE.

Remember to read our earnings call analysis of NVIDIA on lumida.com.

We recommend bookmarking, it's like a drudge report for investors.

You don’t have to go through the 50 pages of the earnings call—we curate the most relevant insights on customer behavior, capex, business risks, and more that you require to make quick decisions.

Market Study #1

We don’t expect tech to run away in historically weak month of September. Also, the best election year seasonality is now behind us.

We don’t believe we re-test the August lows, but we believe 5,600 is a cap on the S&P 500 until we get to the next earnings season.

Our view is tactically cautious on risk assets for the next few weeks as the extraordinary gains off the bottom are digested.

Also, we expect Candidate Harris’s policies around taxing unrealized gains and raising corporate taxes will pour some cold water on equity markets.

We believe Candidate Harris is more competitive than market participants think…

None of this really matters in the long-run – but in the short-run these polling swings can impact markets and risk appetite.

Brad Gerstner’s Altimeter and Portfolio Reactions

I wanted to check-in and see how Altcap has positioned itself since the departure of Snowflake's legendary CEO, Slootman.

We have sharp disagreements on Altimeter, and the broader tech hedge fund's positioning.

We refer you to a newsletter from a few months ago called ‘Why There Are No Great Tech Investors’, laying out our thesis on focusing on hyperscalars and avoiding SaaS.

According to Altimeter’s 13F:

1) Snowflake weight is down from 40% to about 19%.

Now, maybe that's hedged, but you are paying a significant cost for hedging.

The cheapest hedge is called 'selling'. That appears to be the case here.

SNOW is down about 36% since 2/29 and is still their largest position.

Is this not a lesson in avoiding concentration risk and getting too close to management?

Mathematically, diversification works. That’s why Citadel and Millennium and Two Sigma print money.

Diversify across the best ideas.

2) A big bet on META

I like the Meta bet. It's one of our bets also - has been for the last 12 months.

A 17% weight however is too much for me... especially when Meta is near its highs.

(We trimmed our Meta exposure in non-taxable accounts.)

This looks like a bet that is made on tilt.

In poker, someone who has lost money and wants to make it back quickly gets aggressive on betting size.

3) UBER has a 15% weight

I believe Uber is a net loser from the rise of driverless cars.

I listened to the CEO dismissing the driverless transition as if it's not a big deal.

Not the case...

Uber peaked on March 4th, it did not rally to new highs on July 16th and is showing relative weakness.

4) Nvidia at a 14% weight.

I like that bet. The name is fairly valued now, but in 12 months, it should do well.

NVDA

5) Microsoft at 11%

No. This, too, is Consensus. Microsoft's margins are compressing due to GPU spend.

The valuations are priced for perfection.

Microsoft is up 9.9% YTD, lagging behind so many other names.

That's what happens when you pay up for perfection folks.

6) Confluent CFLT

I'm not a fan of SaaS. I disagree here.

7) Altimeter was selling down Snow and apparently adding to a mix of other names with smaller weight.

PDD was one. I'm not there on PDD, and their earnings call was a weird form of self-immolation.

Kind of refreshing in a world of hype driven earnings calls actually.

8) Bet on Google. New Position build. I love this idea, great timing at forward PE of 19x.

But... position size is too small - less than 2%?

9) Sold the TSLA position entirely.

I wholeheartedly agree here.

10) Other names I don't know: Rubrik RBRK and Webtoon WBTN

11) CRM new position and Amazon. I get the logic, I'm not there, but I respect the idea.

It's a bet on free cashflow generation meets dominant market position and AI.

If there's a lesson here, it's that most investors at home should stick to QQQ and SPY and tax loss harvest.

Also, own growth AND value.

Value is cranking now... Berkshire is up 30%, smoking Microsoft and many tech names…

Market Study #2

The study above suggests returns will be less than usual market returns over the next few weeks.

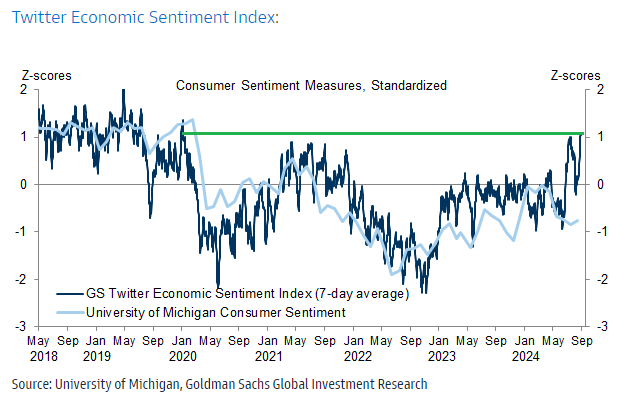

Goldman's Twitter Sentiment Index is back at multi-year highs. That’s also a contrarian indicator.

If you missed the rally, we expect you’ll get another shot to get back in during the month of September.

We also predict the Fed cuts 25 bps not 50 bps.

If you want to get back in the market, we’re taking on clients and have reduced our minimum to $1 MM as we build assets towards a potential ETF launch.

Click here to fill out the interest form for our wealth management services.

If you are interested in learning more about our potential ETF - see www.lumidaetf.com for disclosures, and consider joining our interest list there as well. If we reach 500 people, I expect we’ll pull the trigger!

AI

OpenAI vs. CoreWeave

Bloomberg Excerpt:

Apple Inc. and Microsoft Corp. also have been in talks about participating in the financing, said the people, who asked not to be identified because the deliberations are private. The round would be led by Thrive Capital, which is investing about $1 billion, Bloomberg reported earlier this week.

If the discussions move forward, it would mean the three most valuable tech companies are all backing OpenAI, maker of the groundbreaking ChatGPT chatbot. Microsoft was already OpenAI’s biggest funder, having invested roughly $13 billion.

In her memo to employees, Friar said that OpenAI would use the financing to acquire more computing power and fund other operating expenses, the people said.

My thoughts:

1) So, the valuation will go from $86 Bn to $100 Bn ish?

Is that adequate compensation in that time frame? (No.)

2) You could have bought Nvidia instead and done a 2x or 3x or CoreWeave.

Stick to the capex receivers.

GPU cash guzzlers are fine if you have massive free cash flow generation like GOOGL or META.

Coreweave was one of our private deal offerings for our clients last year - If you are interested in exploring private deals, fill out the interest form on Lumidadeals.com

Company Earnings

Consumer Discretionary

Pinduoduo (PDD): Earnings beat, revenue miss. Revenue up 86% YoY. Slowed revenue growth and premarket stock decline of 15.88% highlight market concerns.

Trip.com (TCOM): EPS beat, revenue miss. Revenue up 14% YoY. Strong cash reserves bolster financial stability despite revenue shortfall.

Chewy (CHWY): Earnings beat, revenue in-line. Revenue up 2.6% YoY. Active customer base growth to 20 million supports steady performance.

Kohl's (KSS): Earnings beat, revenue miss. Revenue down 4.1% YoY. Declining comparable sales offset by planned Sephora partnership expansion.

Lululemon (LULU): Earnings beat, revenue miss. Revenue up 7.2% YoY. Modest share increase post-results despite missing sales projections.

Ulta Beauty (ULTA): Earnings and revenue miss. Revenue up 4% YoY. Stock down 7% after-hours due to declining comparable sales.

The Gap (GAP): Earnings and revenue beat. Revenue up 4.8% YoY. Online sales growth of 7% boosts stock by 2.5% post-results.

Build-A-Bear Workshop (BBW): Earnings miss, revenue beat. Revenue up 2.4% YoY. Stock surged 25% to a near 20-year high, driven by strong market performance.

Technology, Media, Telecom

nCino (NCNO): Earnings and revenue beat. Revenue up 13% YoY. Positive Q3 guidance supports continued growth trajectory.

Nvidia (NVDA): Earnings and revenue beat. Revenue up 122.4% YoY. Record Data Center revenue underscores robust demand and growth.

Salesforce (CRM): Earnings and revenue beat. Revenue up 8.5% YoY. Subscription & Support Revenue growth drives shares up 2.6%.

CrowdStrike (CRWD): Earnings and revenue beat. Revenue up 31.7% YoY. Strong subscription revenue growth lifts shares by 2.73%.

Pure Storage (PSTG): Earnings and revenue beat. Revenue up 10.9% YoY. Strong performance with both EPS and revenue exceeding expectations.

Dell Technologies (DELL): Earnings and revenue beat. Revenue up 9.2% YoY. Record Infrastructure Solutions Group revenue highlights growth.

Marvell Technology (MRVL): Earnings and revenue beat. Revenue down 5.2% YoY. Positive Q3 FY2025 guidance above consensus supports outlook.

MongoDB (MDB): Earnings and revenue beat. Revenue up 12.8% YoY. Stock up 14.56% after-hours, driven by strong subscription revenue growth.

Consumer Staples

Campbell Soup (CPB): Earnings beat, revenue miss. Revenue up 11.1% YoY. Sovos Brands acquisition significantly impacts Q4 results.

Sector | Company ticker | Beat or Miss (Relative View) | Revenue (Absolute View) | Highlight | Earnings Call Analysis |

Consumer Discretionary | Pinduoduo (PDD) | Earnigns beat by 16.8%, Revenue missed by 4.4% | $13.36B, up 86% YoY | Revenue growth rate slowed sequentially; stock down 15.88% in premarket trading. | |

Consumer Discretionary | Trip.com (TCOM) | EPS beat by 9.9%, Revenue missed by 17.4% | $1.8B, up 14.0% YoY | Strong cash position with $13.6 billion in cash and equivalents. | |

Technology, Media, Telecom | nCino (NCNO) | Earnings beat by 7.7%, Revenue beat by 1% | $132.4M, up 13.0% YoY | Q3 guidance: Total revenues between $136.0M and $138.0M. | |

Technology, Media, Telecom | Nvidia (NVDA) | Earnings beat by 6.25%, Revenue beat by 4.56% | $30.04B, up 122.4% YoY | Record quarterly Data Center revenue of $26.3B, up 16% QoQ and 154% YoY. | |

Technology, Media, Telecom | Salesforce (CRM) | Earnings beat by 8.5%, Revenue beat by 1.1% | $9.33B, up 8.5% YoY | Shares up 2.6% after results; Subscription & Support Revenue reached $8.76B, up 9% YoY. | |

Technology, Media, Telecom | CrowdStrike (CRWD) | Earnings beat by 7.2%, Revenue beat by 0.58% | $963.87M, up 31.7% YoY | Shares up 2.73% after results; Subscription revenue grew 33% YoY to $918.3 million. | |

Technology, Media, Telecom | Pure Storage (PSTG) | Earnings beat by 18.9%, Revenue beat by 1.0% | $763.8M, up 10.9% YoY | Strong performance with both EPS and revenue beating expectations. | |

Consumer Discretionary | Chewy (CHWY) | Earnings beat by 14.3%, Revenue in-line | $2.86B, up 2.6% YoY | Active customers grew to 20 million, with sequential growth in Q2. | |

Consumer Discretionary | Kohl's (KSS) | Earnings beat by 34.1%, Revenue missed by 3.3% | $3.53B, down 4.1% YoY | Comparable sales declined 5.1%; Expansion of Sephora partnership planned. | |

Technology, Media, Telecom | Dell Technologies (DELL) | Earnings beat by 9.5%, Revenue beat by 3.8% | $25.03B, up 9.2% YoY | Record Infrastructure Solutions Group revenue of $11.6B, up 38% YoY. | |

Technology, Media, Telecom | Marvell Technology (MRVL) | Earnings beat by 3.33%, Revenue beat by 1.6% | $1.27B, down 5.2% YoY | Q3 FY2025 revenue guidance of $1.450B +/- 5%, above consensus of $1.41B. | |

Consumer Discretionary | Lululemon (LULU) | Earnings beat by 7.9%, Revenue missed by 1.7% | $2.37B, up 7.2% YoY | Shares up 0.55% after hours; Comparable sales up 2%, missing projections of 4.52%. | |

Technology, Media, Telecom | MongoDB (MDB) | Earnings beat by 45.8%, Revenue beat by 2.9% | $478.1M, up 12.8% YoY | Stock up 14.56% in after-hours trading; Subscription revenue rose 13% to $463.8M. | |

Consumer Discretionary | Ulta Beauty (ULTA) | Earnings missed by 2.75%, Revenue missed by 0.38% | $2.6B, up 4.0% YoY | Stock down 7% in after-hours trading; Comparable sales decreased 1.2%. | |

Consumer Staples | Campbell Soup (CPB) | Earnings beat by 1.59%, Revenue missed by 0.43% | $2.3B, up 11.1% YoY | Sovos Brands acquisition significantly impacted Q4 results. | |

Consumer Discretionary | The Gap (GAP) | Earnings beat by 31.7%, Revenue beat by 2.5% | $3.72B, up 4.8% YoY | Stock up 2.5% after results; Online sales rose 7%, representing 33% of total sales. | |

Consumer Discretionary | Build-A-Bear Workshop (BBW) | Earnings missed by 1.5%, Revenue beat by 3.0% | $111.8M, up 2.4% YoY | Stock surged up to 25% to $34.80, reaching a near 20-year high. |

Lumida Curations

In case you missed it, here are some of the best curations from Lumida Wealth on Twitter.

Be sure to follow Lumida Wealth on Twitter, and on Youtube, where you can get more such curations.

Instead of watching hour-long market podcasts - we distill the key insights in 1 min shorts and serve them in threads.

The goal is to maximize insight per unit of time.

Nvidia CEO Jensen Huang sat down with Bloomberg right before the earnings to provide his views on how NVIDIA is shaping future trends. Don’t forget to check these out.

Check out the curation on the future of humanoids from the company challenging Tesla with Peter Diamandis & Figure’s CEO Brett Adcock.

Quote of the Week

“Experience is what you got when you didn’t get what you wanted.” – Howard Marks

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.