Here’s a preview of what we’ll cover this week:

Macro: Mega Cap Valuations

Market: Tesla vs. Nvidia, Semiconductor CapEx Spend

AI: Open AI new o3 model at $1K per task!

Merry Christmas and Hanukkah!

We're excited to share a special surprise with our loyal followers: a PDF guide, "15 Stocks for 2025”. At the time of writing, we own these names across most client accounts.

This guide is our way of saying thank you and helping you prepare for a successful 2025 in the stock market.

Feel free to check out our video walkthrough of these ideas

Animal Spirits

RETAIL TRADERS VS HEDGE FUNDS

A funny thing happened in October 2023.

Here's a chart showing the returns on a dollar-neutral basket.

The basket is long the stocks with the most turnover, and short a basket with the least turnover.

Think of the basket as long 'Trading Stocks'.

Those would include $PLTR, $HOOD, $COIN, Bitcoin and others.

What happened in Oct '23...

retail traders got back in the market.

In Nov & Dec '23, as concerns of 'credit event' faded, the market re-rated higher.

Recession fears were priced out.

Also... hedge funds were short these stocks in the August thru October '23 correction. Names like $UPST for example.

They were forced to cover at the same time as retail traders started buying stocks in Q4.

You will notice this factor did well when Trump was ascending in the polls.

And it took off on the day after the election.

Does this match your own behavior?

In short, hedge funds are 'midcurve' this cycle.

Left curve (retail traders) trounced mid curve.

What should right curve do?

Stick with the winning team until the trend is broken.

This is why you see this funny meme online sometimes… hedge funds underperformed.

Since Gamestop, Twitter and Reddit have transformed investing.

Investing was always a social phenomenon.

We can see it in the performance of our 'Twitter Momentum' basket.

You need new analytics in the social age.

Hedge funds and Institutions are adapting.

I have shared several anecdotes in recent months.

One was a 5 decades long money manager. 70% of his holdings are in 'Quality'.

30% are in Back from the Dead trades. Like Peloton.

So, some HFs - and smart quants - are in on it

If I think about some of our biggest wins this year...

Harrow: HROW

Dave: DAVE

AppLovin: APP

Bitcoin / ETHE

Chenerie: LNG

They all had a social buy-in.

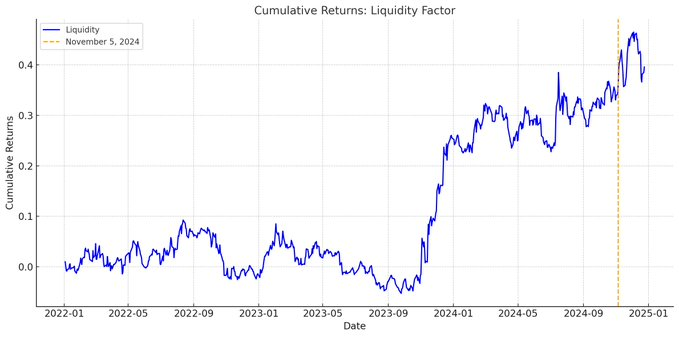

While we're at it, here's the Value Factor

Notice - it did very well in 2022. It made money during the bear market due to Energy stocks.

In 2023, the traded down as Growth stocks took off.

They are doing fine this year too - that's the Growth to Value Rotation

And, here is the Growth Factor.

Notice it did great in 2023 -- when all the retail traders came back and bought their favorite stocks they jettisoned in 2022.

It's been flat 2H '24 -- up until Trump election.

We had a melt-up after Trump with Value AND Growth cranking

Some of you are wondering 'But, my growth stock did well.'

No, that's the Trading Liquidity factor. The herd is buying your stock.

Look at SaaS stocks. They are below their February highs. SNOW, TEAM, WDAY, MDB.

Those growth stocks have no love from the crowd.

Some of you are wondering 'But, my growth stock did well.'

No, that's the Trading Liquidity factor. The herd is buying your stock.

Those growth stocks have no love from the crowd.

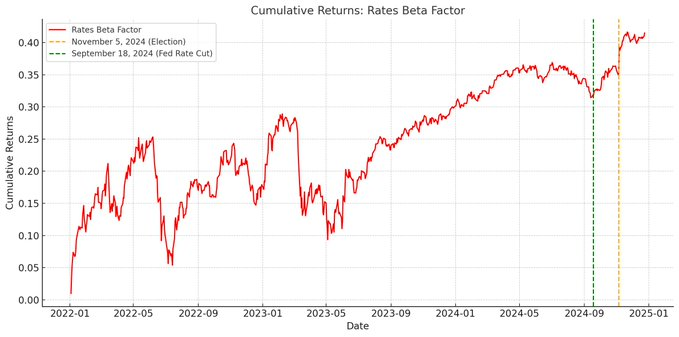

What about Rate Sensitive names?

After the Fed cut rates on Sep 18th, these lifted off.

Hard not to like Financials going into 2025.

Let's wrap up with Momentum Factor.

It's actually been a poor factor, on average.

Example: RobinHood HOOD was terrible in '23. It did great in '24.

Momentum factor says 'what did well last year does well this year' (simplifying a bit).

Investors are confusing Herd Behavior with Momentum factor.

2024 is a Thematic market. Thematic means story telling (e.g., datacenter, online trading, nuclear energy, crypto, etc.)

No surprise then that stories that capture the imagination of the herd are doing well.

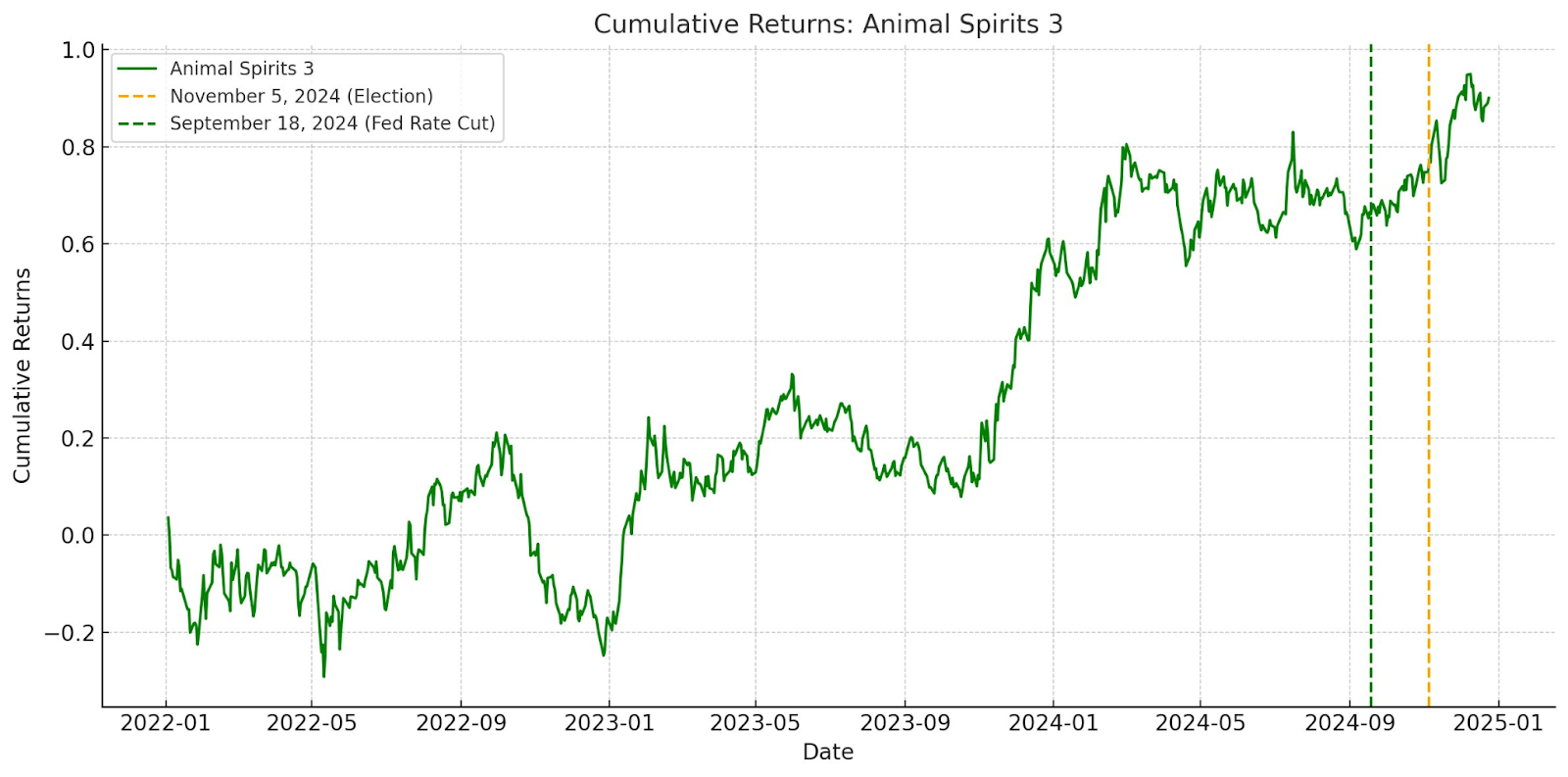

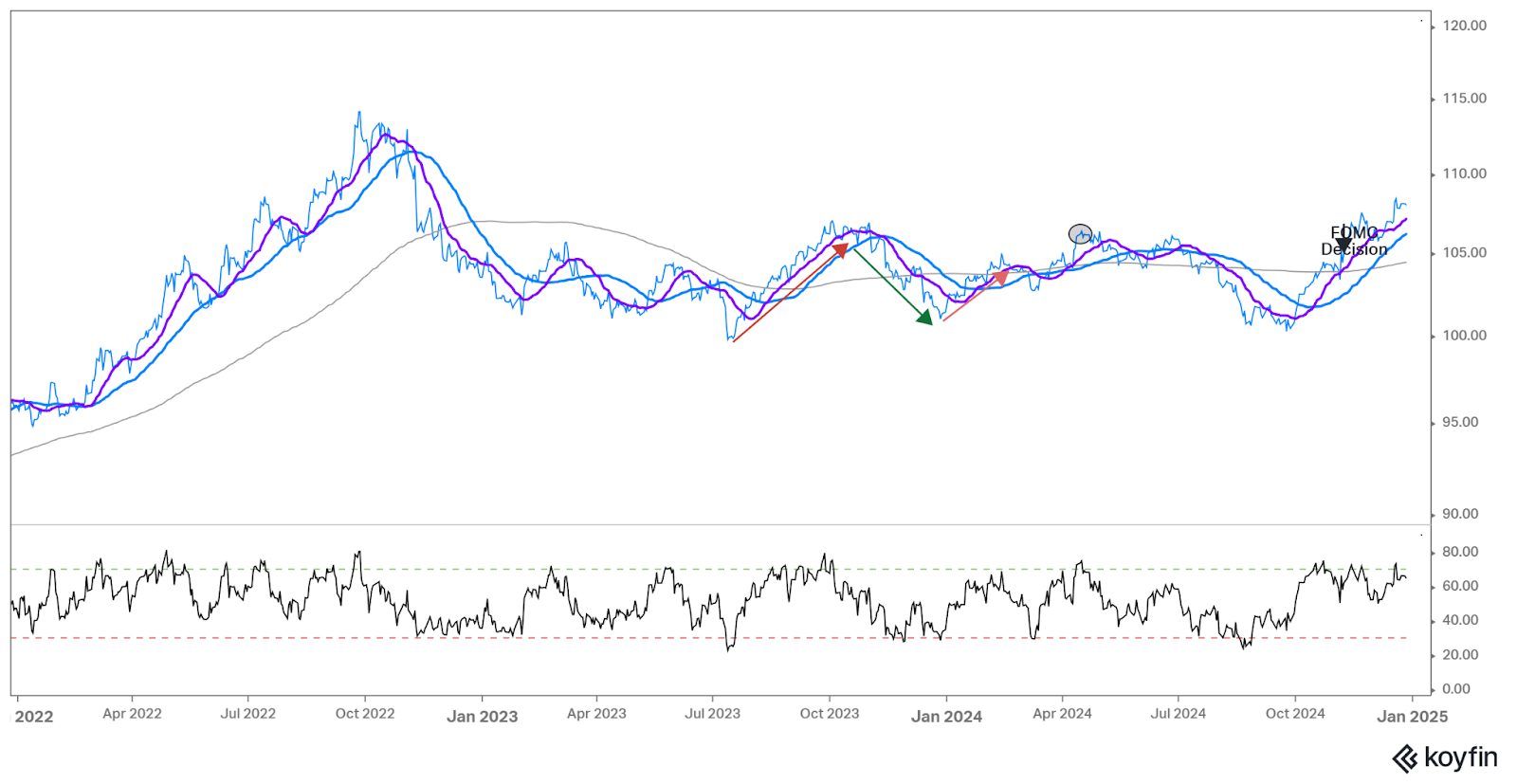

Here is a revised Animal Spirits factor.

This captures the market sentiment perfectly I believe

Look at the Peaks and Valleys.

How does it compare to your P&L?

It looks set to relax somewhat going into the New Year, just like start of 2024 as holiday vibes fade.

Can you apply technical analysis and macro these factors? Yes, these are investable baskets.

Our view is that Animal Spirits need some time to pullback and cool off.

What you see in that chart is a major push higher driven by the Fed’s 50 bps in rate cuts, and the Trump election.

(The market did not fully expect 50 bps, and expected a drawn out election.)

Both positive surprises have put Mr. Market into giddy levels.

At the start of 2024, you have to squint, but a similar type of pull-back took place to reset animal spirits and prepare for the next leg higher.

Powell’s hawkish cut adds to that.

The pull-back started two weeks earlier this year.

We view the past two weeks heightened volatility as healthy and a normal part of markets.

Mini-corrections keep the bull market going.

In terms of positioning - notice that the equal-weight index (RSP) out-performed all the major indices: S&P, QQQ, and Dow Jones.

That suggests the selling down of value and breadth contraction is done.

Earnings season starts the second week of January.

We believe owning financials - especially regional banks and insurance related ideas - is a good idea.

We expect the big banks and regional banks will report quite well, and they are on sale.

Citizen’s Financial Group is one such idea. They are poaching advisors from legacy First Republic to grow wealth management. They also seek to enter the NY Metro market.

Contrarian Ideas

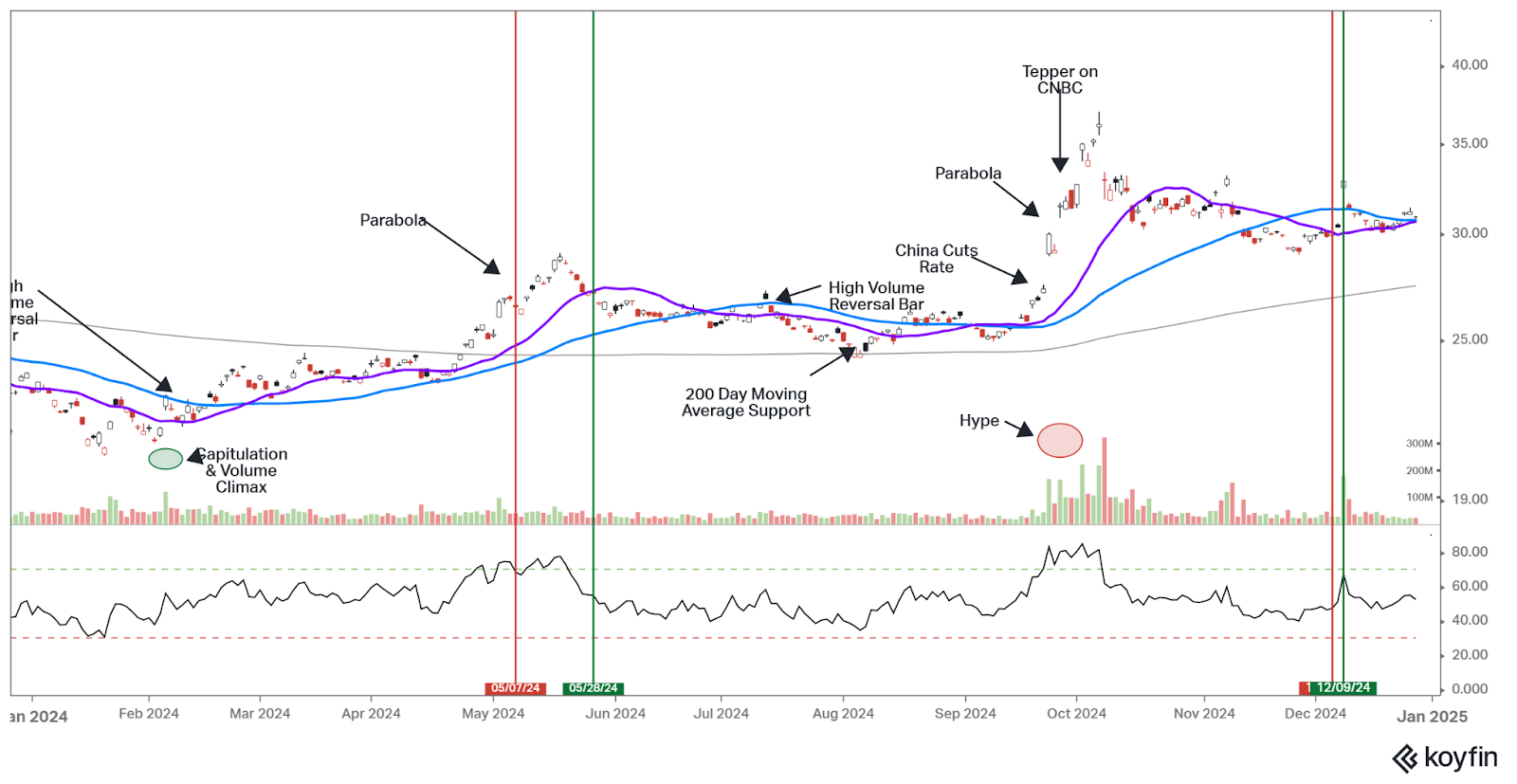

The 2024 year started with China as the most Non-Consensus thematic idea.

But, it was also Consensus Non-Consensus. It was too obvious.

The market capitulated in early February creating extraordinary bargains. We wrote about that on X and in our newsletter.

Then the market rallied peaking two weeks after David Tepper summoned the ‘Hot Ball of Liquidity’.

A few weeks ago, we noted, after the recent pull-back it’s better to look for ways to get long China.

We remain of that view today. China has interesting ideas.

Our preference is to stick with the market leader: Tencent.

International value stocks are dirt cheap.

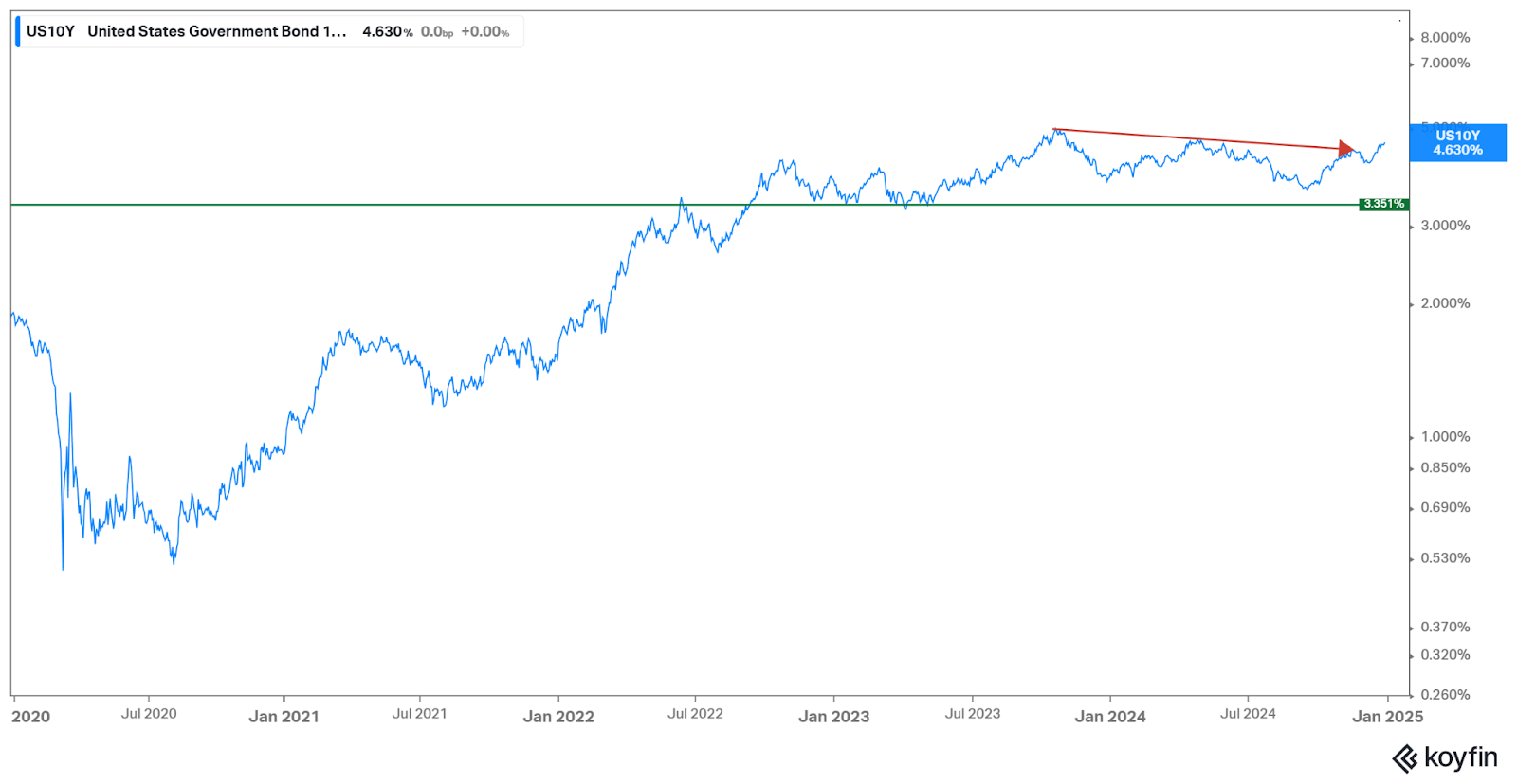

The three horsemen. The US Dollar is up, 10-year is up and energy prices may be going up given Biden’s threat to add sanctions on Russia.

When those variables move up, it’s a nasty combination for equity markets. This week was no exception.

The good news is that it’s hard for us to see the Ten-Year moving appreciably higher from here. Inflation expectations are coming down along with growth expectations.

That doesn’t mean you don’t get an overshoot in the Ten-Year.

The point is - a dip caused by such concerns should be bought. Recall, the 10-year peaked in October 2023 marking the lows in the US equity markets.

The same pattern occurred in 1982 before the start of one of the best bull markets of all time.

When bonds look attractive, stocks are often the way to go when exiting a high inflation environment.

Here is the US Dollar. Notice it has broken out to new highs.

(A chunk of that is driven by foreign demand for US equities; and a higher USD clearing price required to match imports and exports. It’s really good to be a U.S. national, isn’t it?)

It’s hard to know when the US Dollar tops out, but when it does, that would be a good signal to accumulate international value stocks.

Keep an eye out for the Presidential Inauguration date. That date could mark peak ‘Trump Tariff’ and lead to a reversal thereafter.

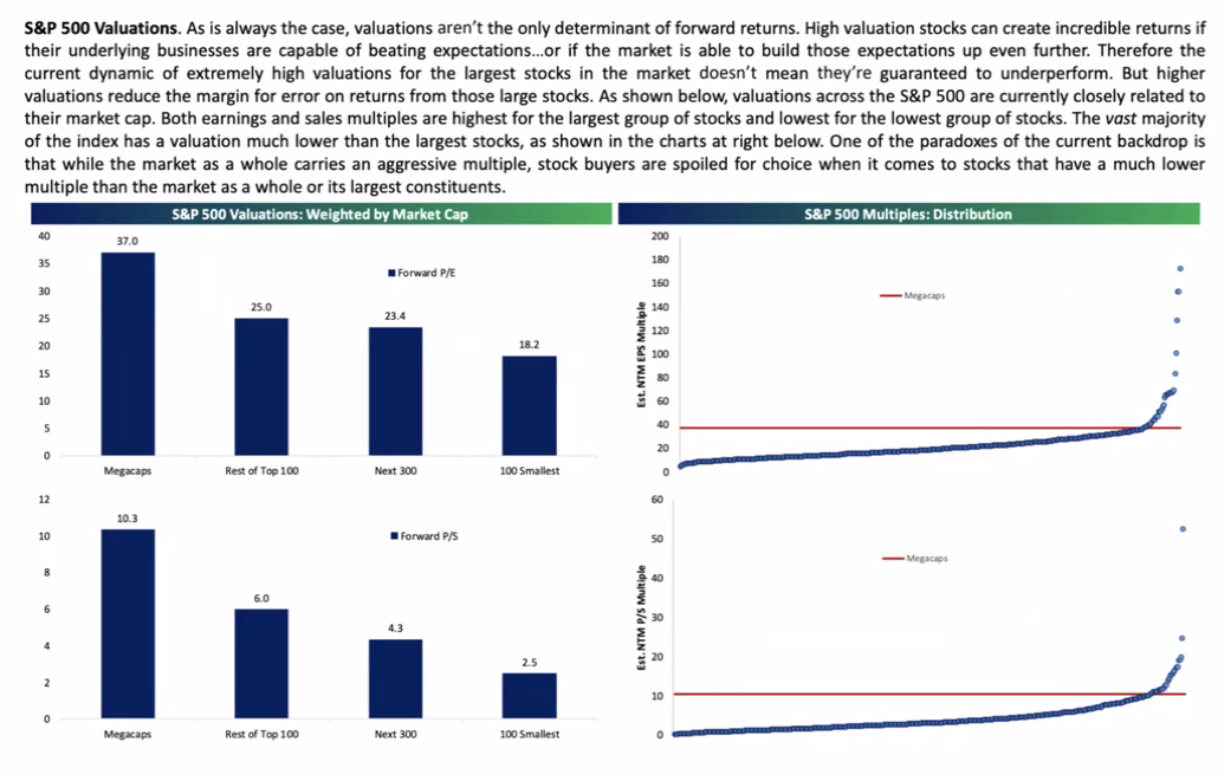

Are the Valuations Too Damn High?

If you take out TSLA and AAPL, the mega cap valuations aren't that bad actually.

Apple is now, once again, more expensive than Nvidia. Apple is almost tied for being most expensive vs itself.

The last time that happened, Apple had a rough 1H in 2024.

Tesla and Apple are playing out quite similarly to Q4 ‘23 when retail investors loaded up on these names along with their stocking stuffers.

Take a look at the multiple distributions on the chart above.

A handful of names on the right hand side are bringing up the average valuation.

You know what names those are by now.

Those names should lag into next year.

Rotating from Tesla back into Nvidia makes a lot of sense.

What expectations are not priced into Tesla at this point?

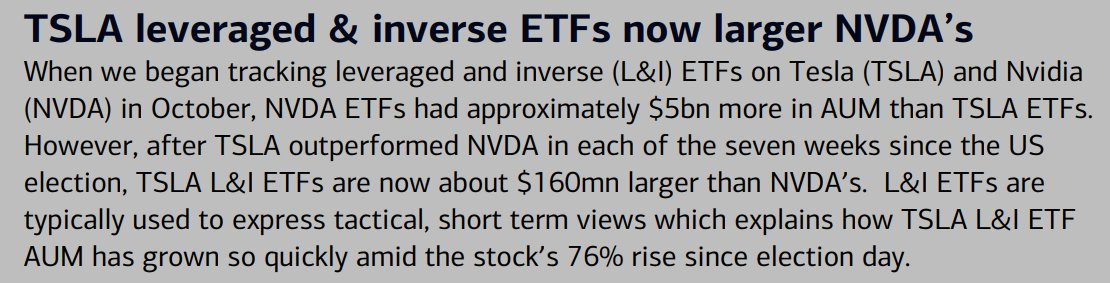

Tesla ETFs Overtake Nvidia

SELL TESLA, AND BUY NVIDIA?

Here is the Contrarian trade you're supposed to do, but you won't do. :)

In October, NVDA levered ETFs had more AUM than TSLA.

That flipped.

Now, TSLA ETFs have more AUM than NVDA.

Sell Tesla and Buy Nvidia

Here's the data from BAML.

Toyota, Ford, and GM Pledge $1M Each to Trump

Strategic Donations or Tariff Insurance?

The Future Doesn’t Wait

The United States is leading the world into the future.

It’s not even close.

Steve Jobs was the son of a Syrian immigrant.

Elon Musk is a South African that entered via a student Visa.

Nvidia’s Jensen was born in Taiwan and grew up in Kentucky.

Einstein was a patent clerk from Germany.

Skills and talents are distributed globally.

Do you stand for maximizing human progress and meritocracy?

If you want continued economic dominance and rising standard - you bring in talent.

You want to create $5 Tn in market value (Nvidia, Tesla, Google, etc)?

You bring in talent.

You want autonomy, driverless cars, and higher living standards?

You bring in talent.

Concern: You are worried about your engineering talent feeling competition?

Sorry to break the news.

OpenAI o4 model is coming for that coding job.

GPT is to coding jobs as EZ Pass is to tollbooth collectors

Autonomy is coming for trucking jobs.

AI is coming for Radiology.

Humanoids are coming for manufacturing.

Nudge your kids into healthcare.

Embrace the fire.

Better yet, if they are capable as you say they are, tell them to build a startup.

The future doesn’t wait, and neither should we.

Hollywood Meets Investing

Every now and then I get a bout of insomnia. The output from the most recent instance is below for your entertainment.

If you had to map an actor to an investment type in the public markets, here’s what they might look like.

Benicio Del Toro: Eccentric, misunderstood, and undervalued. Tanker stocks.

Margot Robbie: Sky-high valuations post-Barbie and WoWS. A Tesla-like trajectory, sustainability is a Q

Timothée Chalamet: The WeWork of Hollywood. Flashy, trendy, and heavily hyped.

Johnny Depp: The Dogecoin of Hollywood. Immensely volatile. Fan loyalty defies all logic, fond moments.

Dennis Villeneuve: A mispriced visionary (Dune), poised for long-term value creation as his assets grow in cultural significance.

Michael Bay: Pure speculation. Loud, flashy, and largely devoid of substance.

Leonardo DiCaprio: Like Mag 7, delivers and delivers — no price too high - appeals to everyone including the haters.

Scar Jo. AAPL. Blue chip with mass appeal.

Steve Buscemi: A quirky REIT. Strange but consistent, delivering solid returns in niche markets.

Christopher Nolan: Sequoia. Consistently delivers S curves and gets in the best deals.

Christian Bale: Bitcoin. Misunderstood, intense, high octane.

Brad Pitt: MSFT. The guy seems incapable of aging. Best at M&A.

Ashton Kutcher: SoFi. Mostly about presentation and packaging rather than raw talent. Has 1 hit every 4 quarters.

M Night Shalyman: Softbank. Had an incredible debut, trying to re-chase the initial high.

Jake Gyllenhaal: The SaaS stock that has potential, and you check in on it from time to time, but never breaks out

Jessica Chastain: APP. Went from Value to Growth star after Interstellar.

Tom Cruise: The Coca-Cola of Hollywood. Steady, reliable, and delivers big even after decades.

James Franco. FTX. Meteoric rise and fall from grace.

Keanu Reeves: PLTR. Hard to justify the valuation, but has a cult following and the vibes are good.

Mel Gibson: Like Michael Saylor, delivers a performance with religious fervor

Jared Leto: Cathie Wood. ARK Invest has extreme highs and lows. Will leave you euphoric and then depressed.

Nicole Kidman. LVMH. Classic growth to value transition.

Tom Hanks: Warren Buffett. Timeless appeal, humility and warmth.

Adam Driver. Like NVDA, Started with under-the-radar potential, potential for rapid growth despite skeptics.

The hard question… who is IBM? ‘No one was ever for fired for buying IBM’.

Who is IBM? Let us know. We must know.

Goldman Sachs

How do you think Goldman Sachs ‘Conviction List’ did this year?

You can see their picks below.

They lagged the S&P 4% … before fees.

To get on the Conviction List, you need to go thru a Committee.

That kills the alpha right there.

Meanwhile, our Top 10 Basket for 2024 did 38%.

I figure that is 98 or 99 percentile performance.

We’ll see a week or two after the year ends when the studies showing active manager performance comes out.

Check our Stock Picks here: https://docsend.com/view/s/wqvgi685pmcr3uji?utm_source=ledger.lumidawealth.com&utm_medium=referral&utm_campaign=15-stocks-for-2025-holiday-stocking-stuffers-from-lumida-wealth

Link to the broadcast: https://x.com/ramahluwalia/status/1871605264086147452

CapEx Receiver Thesis

In November of last year, we published our ‘Semiconductor CapEx Receiver’ Thesis.

We remain of the view that Nvidia’s forward analyst estimates for sales are way too low.

Have a listen to our curation of Dylan Patel on the BG2 podcast to learn more about the semiconductor industry.

My main takeaways from the show are that Nvidia and Broadcom are well positioned. (Broadcom is focused on the Custom Silicon angle - enabling three hyperscalars build their own chipsets.)

There is so much datacenter space coming online in the coming years, unless they put something other than GPU in those facilities, we’ll see plenty of spend on Nvidia.

We also hosted Dylan on the Lumida Non-Consensus Investing podcast last year. Stay one step ahead of the crowd and subscribe to the pod here: Youtube, Apple Podcast, Spotify

AI Impact: Tweet of the Week

The future is accelerating. The gap between AI forward and AI backward will only widen.

Open AI Rolls out O3 model - PHD Level Intelligence

Are there tasks worth spending $1K per task on OpenAI o3?

That’s the cost of the latest model from Open AI - available for testing only.

OpenAI o3 is providing high-IQ PHD level insights.

It is solving intimidating Math Olympiad problems - fast.

Would I pay for that?

Absolutely.

I would pay for a weekly positioning report (eg, synthesis).

How to position best across asset classes and within assets?

What % to allocate to each asset given our inputs and views?

What views should we reject or keep?

Which views are priced in or mispriced?

Running o3 weekly is $50k a year. That’s cheaper than a $500K PM.

It’s completely worth it.

The key is feeding the AI the correct inputs so it has a coherent framework (and we would provide that framework also).

The edge in the age of AI is having a sound framework. You are paying the AI for discipline and no human cognitive biases

The hard part is it might take 30 or 50 trial runs to experiment before getting the OpenAI o3 model to produce accurate results.

But once you have that, you can beat Bridgewater.

Well, we’re already doing that, but you get my point.

The @LumidaWealth tech investment is all oriented making the CIO team redundant.

A master AI model that we can debate and challenge the CIO team, like a co-pilot, is the intermediate goal.

Link to the tweet: https://x.com/MParekh/status/1870885754244624602

As Featured In