Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.

Here’s a preview of what we cover this week:

Macro: What We Bought in China

Markets: Parabolas are Coming; CRE

Company Earnings: Retail Resilience, $SNOW surprises

AI: AI Disillusionment; Chip Wars

Digital Assets: Ethereum ATHs are coming

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

AI Chip Wars

This week we had a very insightful discussion on all things semiconductors with Daniel Nystedt.

Dan is a former journalist (WSJ) turned financial analyst for a family office focused on Taiwan and Asia.

He has lived in the Greater China region for over 20 years. As investors, it's always exciting to compare notes from someone on the other side of the world. Especially since TSMC and GFS play an important role in the semiconductor value chain.

Tune in, and don’t forget to subscribe.

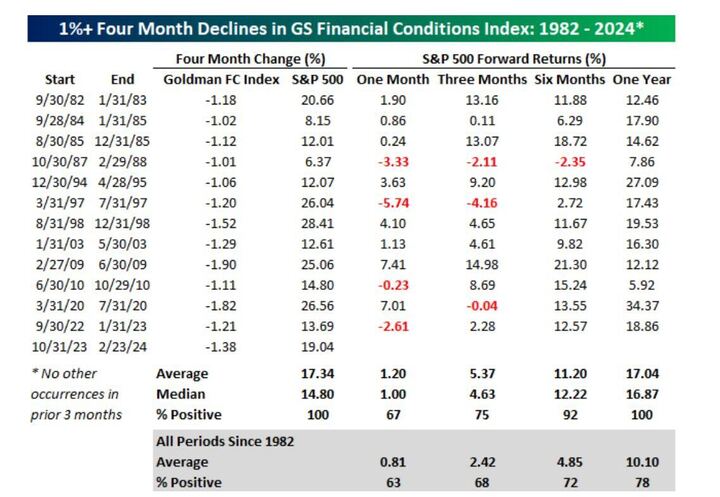

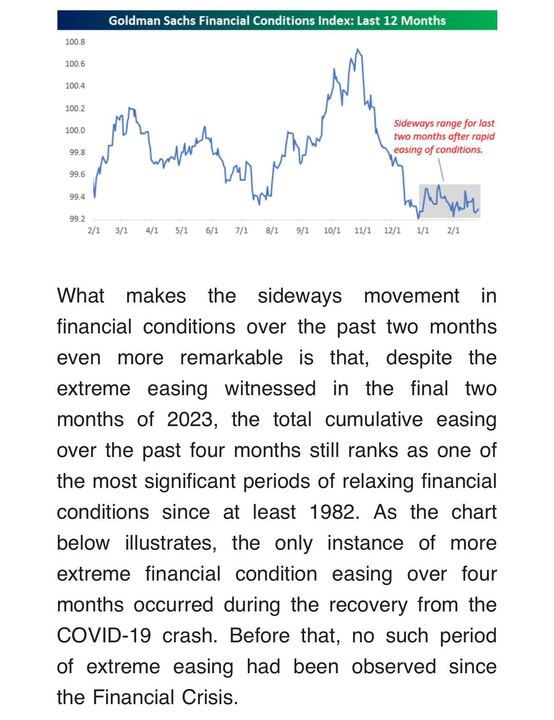

Mother of All Bubbles (Delayed):

In the Dot Com era, we had genuine killer apps:

- Email (Hotmail com)

- E-Commerce (Amazon)

- The Browser (Netscape Navigator)

- Online communities (AOL, Prodigy)

- Direct messaging (ICQ, AIM)

- Digital Music (Win Amp, iPod, Napster)

- Chat (AOL)

- Internet Gaming (Quake)

Take stock of that...

Any 3 of those would be remarkable.

The late 90s was truly an incredible time to be alive.

2024 is not shaping up in the same way.

GPT is great for drafting, summarizing, and researching, but these are not at the 'killer app' level.

I can do fine without GPT.

It's not indispensable. I cannot rely on it for investment advice or decision-making.

So... I don't expect we'll get a super bubble this year.

I do think we'll see a real risk of AI narrative disillusionment soon.

Altimeter is focusing on Google.

That distracts from the limited success of Microsoft Co-Pilot, OpenAI's GPT, Tesla's FSD, or the neck brace called Apple Vision Pro.

Google is a scapegoat for Silicon Valley's failure to deliver real AI impact thus far.

No one has hit it out of the park.

The Emperor has no Clothes.

If you live in Omaha or a small town in New Jersey, this is easy to see.

Is there success? Yes.

There are exceptional niche AI apps focused on narrow use cases - midjourney.

But, until the 65+ crowd embraces AI, we have a long way to go.

Mom and Dad were using AOL. They aren't using GPT.

This has a few implications for Mr. Market.

One is that Mr. Market will not build enough internal momentum to get the escape velocity we saw in the late 90s.

Finally, after Apple breaks below its moving averages, Goldman Sachs removes Apple from its Conviction Buy list.

I can rest in peace now.

To my knowledge, Lumida Wealth was the first to call out Apple starting last summer, just after Apple announced plans for the Apple Vision Pro.

And we also said no March Rate Cuts.

Goldman Sachs was wrong on both of these accounts.

Take a look at the capitulation in Apple shares yesterday.

Morgan Stanley - we have not forgotten your $400 price target on Tesla.

And, JP Morgan, how did you miss the extraordinary rally in Digital Assets?

Apple ends Apple Car.

Tesla breathes a sigh of relief.

Both stocks continue to lag Mag 7.

Meanwhile, Google owns Waymo and is actually doing FSD while Tesla talks about it.

Google has a wide variety of ‘embedded real options’. Driverless cars, YouTube, and Personal Assistant AI are a few of them.

Apple probably kept the car project alive for so long so as not to disappoint investors.

This is shaping up to be a ‘reset’ quarter — throw all the bad news in and take a bath.

Apple’s self-inflicted wounds continue to grow.

Macro

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

On China

What did I buy when China was on Sale?

Ping An - an insurance holding company most people never heard of.

Ping An is a leading player in China, and they did not get caught up in the issues surrounding Evergrande.

The Forward P/E ratio was 4.5x at the time of purchase. Dirt cheap.

When the capitulation was done, we had the research ready, so we simply had to execute.

The slide below was a post of me trying to translate and interpret their quarterly update using AI.

Here's a chart of Ping An on a short time frame and a long time frame.

The entry was right off of a 10-year trend line!

With a cheap entry like that, we can hold this position for several years now. This should double in a few years.

And if the company can execute its strategy of growing the consumer insurance market in China, hopefully, a lot more.

China's insurance market is underdeveloped, and Ping An is going after that opportunity.

It's a lot like investing in mobile phone carriers delivering services to Lat Am 10 years ago...

You know the products will come to market - just need to find the best positioned leader.

I had a chance to meet Ping An management and visit the company several years ago, which comforted me.

Before you judge someone for investing in China - note Berkshire does as well - look at their electric car company BYD.

This is a stock you tuck away for 3 to 5 years.

Nuclear Energy and AI go hand-in-hand.

Cheap energy (e.g., nuclear) goes hand-in-hand with the rise of AI.

Last week we said we were buying a utility. Utilities were oversold. We did not name the utility until earlier this week on Twitter.

The stock - Talen Energy.

This utility has a nuclear facility and appears likely to win a contract to win a large data center.

The energy needs of a large data center rival a small city.

Talen is up 4%+ on the week.

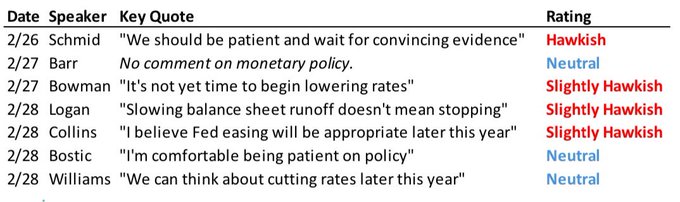

Fed Watch:

What they are saying is no rate cuts anytime soon.

Not March, and it looks like not May either.

We need to assess June as we get closer.

Markets

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Snowflake Drama

Altimeter has a whopping 40% position in Snowflake ($SNOW), according to its SEC 13F filing.

That’s way too high a position - it violates basic tenets of risk management (including the Kelly Betting rule).

Read the ‘Missing Billionaires’. It’s a great book studying why ultra-wealth fails to pass on wealth to subsequent generations. The primary mistake? Position sizing.

(We have about 40 to 70 positions that we own at a time sampled from a pool of ~100 investments that we deem high quality. We link our entry to favorable valuations and tactical entry points.)

You can diversify across names within a theme and create wealth. This is essential to avoid ‘growth to value’ bombs blowing up your portfolio - like Apple, Tesla…and now Snowflake.

Observations:

1. Snowflake is down 20%.

The revenue growth is now sub-10%. It's massively over-valued and may drop in price further after it returns to its moving average.

2. It's irresponsible to have a 40% position in a single stock.

Silicon VCs fall in love with management because they are too close to them. It's better to be a monk in Omaha and not get too close to charismatic CEOs.

Investors are sometimes intoxicated with narratives and lose perspective.

3. Google now has a Forward PE of 17.5.

There's no bigger critic of Google than Altimeter.

We believe Brad got the trade exactly backward.

4. I wrote before I'd be happy to compare our public market returns at year-end.

I know we are beating QQQ and SPY YTD - and we're not even fully invested.

Brad graciously took us up on the bet over a steak dinner sometime next year.

5. The news yesterday from Snowflake was somewhere between awful and terrible.

Why? Revenue growth is slow. That's why the CEO is out the door.

And the PE ratio is at nosebleed valuations.

Snowflake is the latest business to make the growth-to-value transition.

Here’s a video where I elaborate on these issues and the difficulties of hedging the SNOW position. Jump to minute 13:00.

Biotech and the Search for Alpha:

You have to approach Biotech like a venture capital portfolio.

A handful of outliers will drive the returns: 5X to 10X. So you need many small positions.

And most will lose value - because you can't be sure which biotechs will pass their clinical trials in advance.

One name we own?

Rocket Pharmaceuticals.

RCKT is focused on providing Gene Therapy solutions for rare diseases.

It's up 80% from the October lows. It's grown into our largest biotech position.

The key to biotech is (i) excellent research and (ii) diversifying your idiosyncratic risk across many good ideas.

You want the odds to work in your favor rather than overweight any name.

If you are not diversified in biotech, then you're not harvesting the return from the investment process.

Biotechs are searching for product market fit in the form of FDA approvals, very much like a startup.

They are unprofitable cash guzzlers (generally). When they hit a milestone, they jump in value or get acquired.

After you have your biotech portfolio, the strategy is to let the winners ride.

Tax-loss harvest the inevitable losers.

If there is adverse news on your holding (e.g., a failed milestone), consider selling.

I would wager our biotech strategy will outperform the vast majority of venture capital strategies...while maintaining liquidity.

We also like biotech long/short hedge funds. We are close to decisioning a high-quality biotech fund with the following traits:

5-year track record

No losing years (yes, including the 2022 bear market)

25 to 35% net return

Zero correlation to the market

That’s the definition of alpha folks.

I started investing in biotech back in 2011 via relatively small hedge funds.

Those hedge funds have since grown to $5 Bn+ behemoths.

Smaller, niche biotech funds that are capacity-constrained are the best move here.

Our biotech hedge fund investing history has given us access to a network in the category, including access to specialists and researchers who have databases on virtually every clinical trial and their probability and impact tables under the sun.

That research and the historical tables is where the alpha comes from.

We are still early in the biotech cycle. In Oct '23, biotech valuations were at 10-year lows.

Many firms were trading below net cash assets.

Elective health spending is ramping up.

The fastest growing demographic is the 'oldest of the oldest'.

The demand for treatments and therapeutics is going up and to the right.

The success of the GLP1s is only the first of many new 'modalities' that will come to light in the coming years.

I will be interviewing a portfolio manager in the coming weeks if you want to learn more. We also have a biotech primer deck we’ll be releasing soon.

Stay tuned.

Software vs Pharma:

We sold long-time holding Novo Nordisk (NVO) for Biotech & Software.

Here’s why.

Novo Nordisk is a world-class pharma company benefiting from the GLP1 trend.

Novo has a dominant market position, quality leadership, and taking share.

We love those characteristics.

However, Novo and Eli Lilly have a higher forward PE than Microsoft.

There’s a big difference between the two.

Microsoft is in an ARR business with an installed user base.

Novo has its IP go generic in 10 years.

Pharma companies do not generate the same kind of high quality earnings as Software.

We believe Novo and Lilly are fantastic businesses.

They will continue to grow revenues quickly.

We are still early in the adoption curve.

But, Mr. Market will arrive at our conclusion as well one day.

There’s a longer-term stream of cashflows in software and other businesses that can be purchased at a much lower price.

(There are also more affordable peptide substitutes that may take a share. And tail risk should adverse drug symptoms emerge, although by most accounts, these are effective treatments.)

At this valuation, we’d rather own the very companies Novo, Lilly, and Pfizer need to acquire to stay relevant after patents expire.

Or, we can own software businesses that can internally compound for a longer time frame at a cheaper price.

As an investor, all assets are comparable on a risk/reward lens

It does not matter that Microsoft is a software company and Novo is a pharma.

There is an opportunity cost of capital.

Novo is more expensive than Microsoft on a relative value basis.

Both are the best in the world at what they do.

On Microsoft, Microsoft itself is more expensive than other Big Tech, SAAS, and biotech on a risk/reward basis…

That’s where we are focused.

We don’t own Microsoft either… the general point is that Novo and Lilly are more expensive on a relative value basis than alternatives in the market.

Mr. Market is going to figure that out one day.

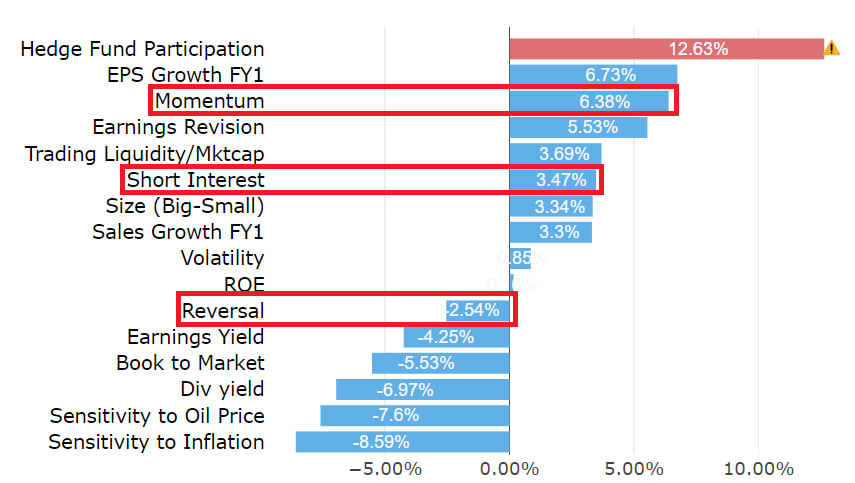

What factors are working?

Have a look. There are some major differences from last year:

We noted before in our ‘Best vs. the Rest’ that Quality Momentum is rallying.

We happen to own a bunch of those names - think MongoDB, CloudFlare, Meta, and others.

Beyond that, stocks with momentum and high short interest are rallying. We don’t own these names.

These are names like Carvana, SoFi, and Bitcoin miners.

These are ‘battleground stocks’. Hedge funds are shorting, and retail investors are making long calls to try to create a ‘gamma squeeze’.

Until the short interest factor stops performing again, it’s better to stay net long.

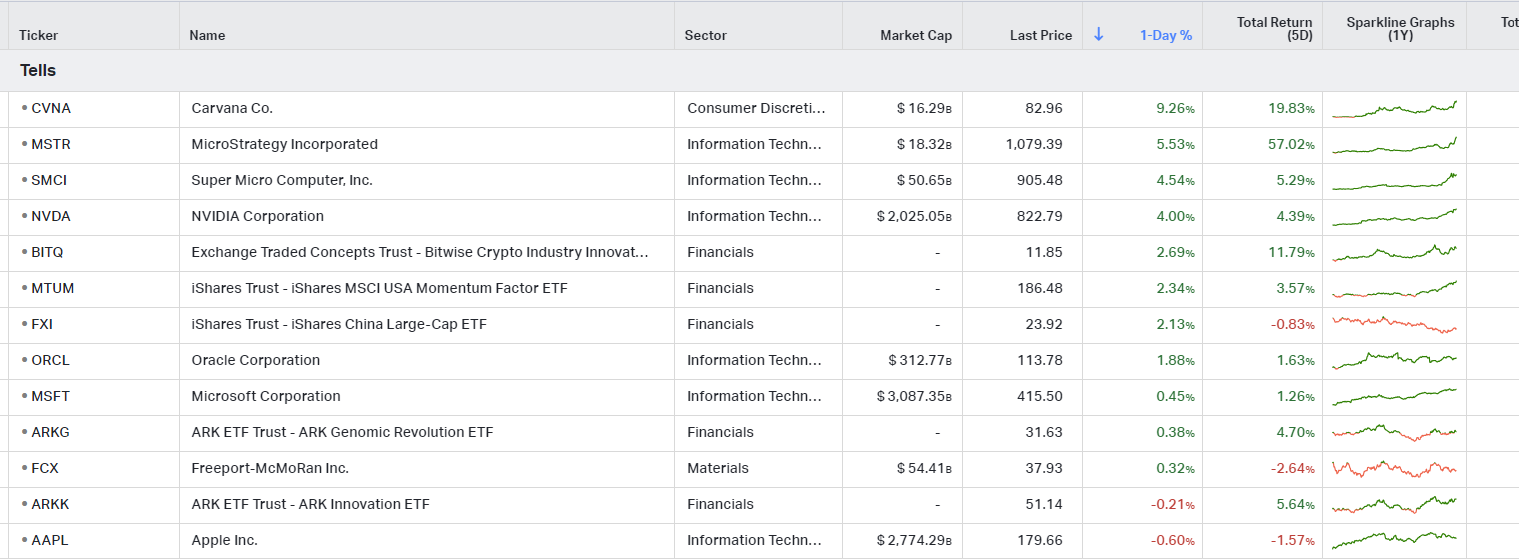

If I had to pick just one stock to look at concretely that captures these abstract factors, it would be Carvana.

Carvana has a 100x PE ratio. It is highly shorted. It has tremendous momentum.

We have no position, never have, and don’t plan on it. We don’t like ‘battleground stocks’ or Consensus names.

Notice the sharp jagged peaks in Carvana. Those are short-covering rallies. You will also notice that local peaks in Carvana coincide with market peaks.

If you want a market tell - this is one to look at. Other ‘Market Tells’ we look at to get a sense of near-term market behavior are the following:

All together, the factors and the performance this past week is indicative of a momentum market.

A momentum market is prone to parabola development. New buyers get sucked in. Shorts want to call a top and get squeezed by new inflows. Prices go higher.

The process repeats until there is exhaustion.

Nvidia’s earnings changed the dynamic of the market and emboldened animal spirits.

Up until earnings, we saw deterioration in market internals and leaders rolling over - including Microsoft, SuperMicro, and others.

So, until we see that behavior again, any correction is deferred.

Mr. Market wants to go up.

Fortunately, we noted before our hedges were in Apple and Oracle. Both of those worked.

Why would you want to hedge with QQQ or SPY when these contain the best businesses in the world?

Our approach is to find the weaker players that stray from the pack and where we have a variant perception.

So far, our public calls track record on shorting SoFi, Apple, and Oracle (and Domino’s Pizza) has worked well.

We don’t recommend you try this at home. And our positions are situated within the context of a net-long portfolio. The hedges are used to ‘sculpt,’ and risk manage more than anything else.

But, if we can make money on the hedges - that’s a treat.

Gold Stock

Last week, we wrote:

“We bought a gold miner (Eldorado Gold) on Friday. We haven’t bought a gold miner in… over 10 years.”

The stock is up. The factor in your control is when you buy. The statistics show you make your money on the buy.

We increasingly focus on less-covered parts of the market to find value.

On Commercial Real Estate:

A Canadian pension fund just sold its 29% stake in this New York office building for $1.

The 26-floor building in Manhattan stands at 360 Park Avenue South and was purchased in 2021 with plans to redevelop it.

The pension fund had already poured $71 million into the property, and the building currently has a $220 million mortgage.

Boston Properties, the acquirer of the pension fund's stake, said the project needs "a change in strategy."

Office building prices are down nearly 50% from their highs.

The way to buy a distressed is NOT to buy the equity.

You wait for the debt to stop performing.

Then you contact the bank and buy the debt from the bank at a discount: say, 40%.

Then you reset the equity.

Now you own 100% and no debt.

This strategy is called ‘buy non-performing loans, then foreclose’ or ‘loan to own’.

That’s the strategy of our preferred distressed CRE manager as well.

CRE Bank Failures Are Coming

I was poring through the 10Q of a small bank this weekend.

What else do you do on a Saturday?

I noticed that the loans on their watchlist appear to be well below what they should carry, based on my knowledge of this bank.

I won’t name the bank. I have no interest in causing fear or panic in the financial system.

And there is zero systemic risk from these issues.

However, I am fairly confident we will see other banks - not just NYCB - lose a pound of flesh sometime this year.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Company Earnings

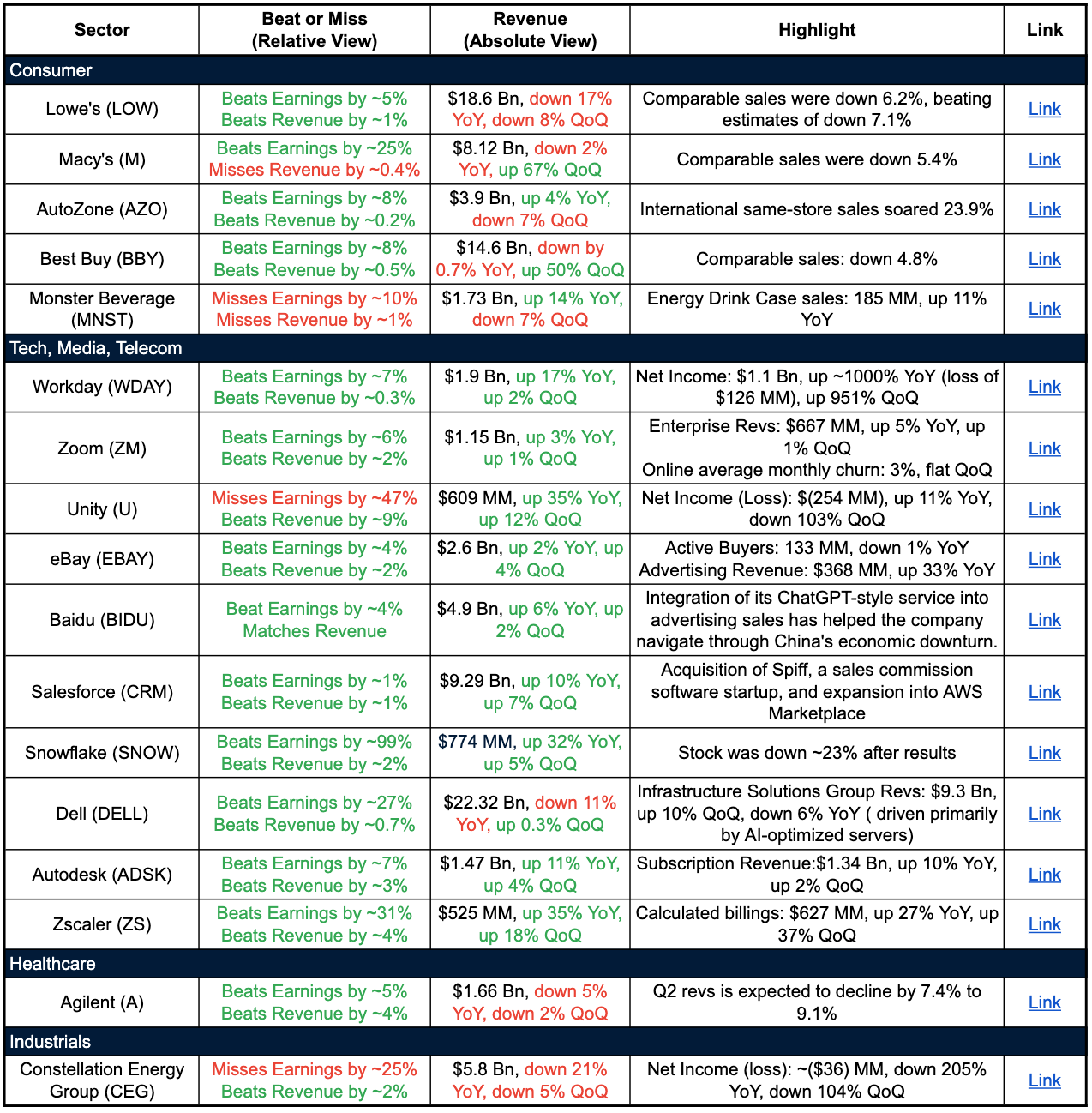

Consumer:

Retailers like Lowe's, and Macy's are seeing modest comparable sales declines but better than expected.

Auto parts retailers like AutoZone are benefiting from resilient demand and international expansion.

Consumer electronics firm Best Buy facing sales pressure.

Tech/Telecom:

Software firms like Workday, Zoom, and Autodesk are seeing steady revenue growth driven by subscription transition. Margin expansion

Gaming/metaverse platforms like Unity have strong revenue growth, but profits are still elusive

Search engines like Baidu are getting a boost from AI integration and new offerings

Cloud software vendors like Snowflake and Salesforce are accelerating growth, driven by firm-wide deals and new products. But stock volatility remains high. Snowflake’s sudden change of CEO signaled internal problems and lower sales guidance

PC makers like Dell are being impacted by supply chain issues but server/infrastructure revenues are more resilient. Shift to AI-optimized offerings

Cybersecurity providers like Zscaler benefited from a strong enterprise demand environment and calculated billing growth

Healthcare:

Life sciences/diagnostics vendors like Agilent are facing near-term revenue headwinds

Industrials:

Energy infrastructure players like Constellation Energy have growing revenues but facing cost/margin pressures

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Digital Assets

We recommend folks read our friend Alex Thorne's (Galaxy Digital Research) view on Bitcoin.

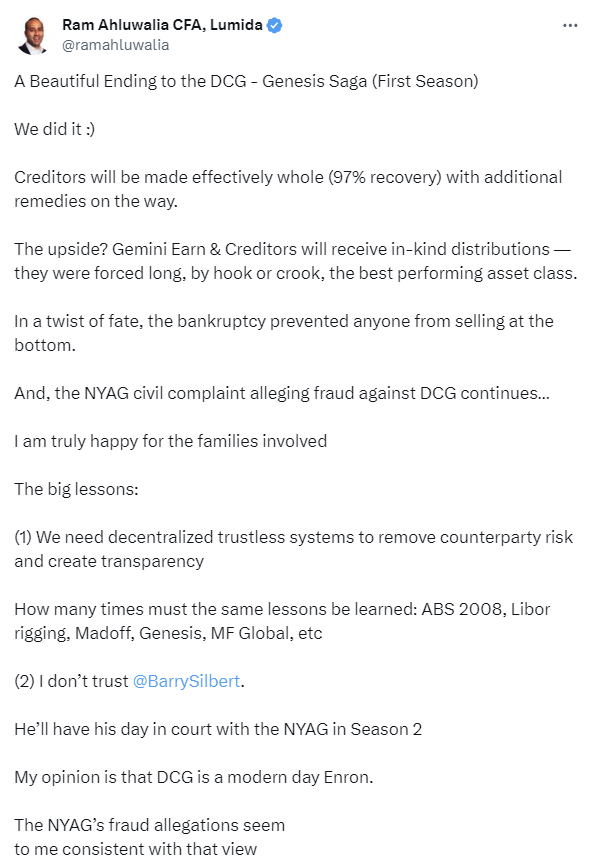

We are pleased that Gemini Earn clients have a path to full recovery.

This is the most satisfying call we have made, as it means hundreds of thousands of small investors and families can return to their lives.

Our Ethereum Rotation Thesis Continues to work.

Here’s a write-up on our thesis below.

We wrote this when Ethereum was in the $2,000 to $2,200 range. Now it’s in the $3,500 range.

For all the hard work we put into managing our public equities strategies and sourcing great managers, it is really quite something to see a passive crypto investment strategy (with good cycle rotation) outperform handily.

ETHE is up 100 to 300% depending on when you might have bought in - even as late as September of last year.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Quote of the Week

“Time in the market, beats timing the market.” – Ken Fisher.

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.