Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Macro: Goldman & Rate Cuts, Lumida Telegram

Markets: NVDA, Uranium, AI Investing, Lumida’s Call

Company Earnings: Resilient Enterprise Demand, Consumer Brands Face Inflationary Headwinds

AI: ASML Kill Switch, MSFT CoPilot, Defense AI

Digital Assets: Grayscale ETH Trade - End of an Era

This was a big week for Ethereum ETFs.

We met with crypto-native fund managers and advisors to discuss the impact.

Here are some themes we discussed on the live stream with YouTube timestamp links (don’t forget to like, share & subscribe - it helps us build social proof and attract luminaries for new episodes)

00:35 Ethereum's Market Dynamics and ETF Speculation

01:34 Expert Opinions: Analyzing Ethereum's Position

03:44 Macro Perspectives and Crypto's Regulatory Environment

07:52 Political Dynamics and Crypto's Role in Elections

19:22 Market Movements and Investment Strategies

27:35 Future Outlook: Crypto Bill Approvals and Market Predictions

31:39 Exploring the Crypto Landscape: Public Markets and Institutional Interest

33:07 Decentralized Technology and Transparency

34:17 The Future of Crypto: Solana, Stablecoins, and Public Offerings

37:03 Regulatory Environment and Banking Challenges

45:36 Digital Asset Custody and Investment Strategies

48:09 Ethereum Ecosystem and DeFi Opportunities

55:48 Speculating on ETF Approvals and Crypto's Future

For those interested in the audio format.

This week, we had a lively conversation with Amit Kukreja (X: Amitisinvesting)

We talked about SOFI, TSLA, PLTR, and secular investment themes in the current market.

Here are the best bits, link to the full conversation in the thread.

Don’t forget to give us a follow!

Macro

Goldman Sachs on the Fed:

‘Comments by Fed Governor Christopher Waller in a speech today raise the risk

that the first cut could come later than our forecast of July’

Only now they are thinking that might not happen.

Look at how many names are in this report.

GS should take the approach in the Three Body Problem…

Here’s their July Prediction

Lumida Telegram Group

We have launched our telegram group where we curate all our insights, market commentary, earnings calls and more with special takes from Ram.

Click here to check it out and join in on the conversation. We will continue to iterate on this and add content streams over time.

Markets

NVIDIA Earnings

How did we do on our Nvidia call?

We wrote this the day before Nvidia reported:

‘We are long. I expect Nvidia delivers a beat / beat / raise’

Today:

Revenue: up 242% y/y and 18% q/q, (BEAT by $1.5B)

EPS: $5.98, up 629% y/y (BEAT)

Practically, I’m kind of disappointed as we don’t get a good buying opportunity like we had with META and GOOGL.

If you are deploying new capital every month, you want good entry prices.

It makes it harder for us to get good prices for new accounts.

‘You make your money on the ‘buy.’

What about existing accounts?

Exit prices matter when it is time to sell.

This is classic Buffett & Munger logic…

Investors want lower prices to accumulate great assets.

That’s exactly right.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Our Nvidia Thesis

Here was our reasoning going into earnings.

– Nvidia is 2% from its all-time high

– We know that Google, Meta, Amazon, Oracle, and CoreWeave are spending billions of dollars to buy GPUs

- The return on CapEx spend is higher than the market thinks so ‘hyperscalars’ will continue to spend (look at Cloud revenue growth)

- Countries like Saudi Arabia are starting to FOMO into data center spend

- The new meme is “intelligence cannot be outsourced’. On-prem is back: that helps Nvidia and hurts Microsoft and IT Consultants

- Read thru: Taiwan semiconductors revenues show 60% YOY growth

- TSMC’s largest customers are AAPL and then NVDA

- We know Apple isn’t selling many vision pros. (They have that hospice-type music on their earnings calls now…)

- The inference is that Nvidia is selling every GPU that comes off the belt

- If Jensen touches a CEO, that CEO drops a couple of billion. He is a master salesman selling to an easily identifiable customer set

- Jensen has a posse that includes DELL

- The stakes for winning the AI ‘space race’ are so high, that the demand for GPU compute remains insatiable

- I have no idea what the stock price will do

- If stock price drops like META, which has largely closed that gap (did you get in there anon?), we are a buyer

- If the price gaps up, we stand pat

- Growth stocks that report have seen stock price declines

- Nvidia is the ‘pace setter’ and is therefore an exception to the rule. Meaning, comps to Nvidia are causing these dips.

- Mr Market will buy dips on Nvidia. 2026 analyst estimates look low to me

- We have iterated down our exposure to several semiconductors…except Nvidia and a few other dominant players

- The relative value of Nvidia was the strongest in Mag 7 on Jan 1.

- Nvidia had gone largely flat the 2H of ‘23, and was a smoking buy on New Years

- It looks to us that Nvidia’s constraint is not demand; they are a price setter.

- We remain long Nvidia into earnings

- I expect Nvidia delivers a beat / beat / raise

Highlights from Nvidia Earnings Call

I believe Nvidia will be the most valuable company in the world - within a year or two.

I recommend listening to my interview with Fabricated Knowledge author Doug O’Lauhlin if you want to learn more about how Nvidia is playing the game at a different level. Here’s a clip.

The reason is we’re 5% thru the upgrade cycle of transitioning old CPU-based datacenters to GPU datacenters.

Saudi Arabia is building 60 data centers. The earnings call revealed that Japan and Singapore are also getting involved.

Wait until we see the bid from the Department of Defense.

The funny thing about Nvidia is most of its peers are more expensive. And Nvidia is cheaper relative to itself and it’s 10-year history.

Take a look:

Earnings Breakdown

Here are some highlights:

Guidance/Outlook:

Expected Q2 revenue: $28 billion (±2%)

GAAP and non-GAAP gross margins: 74.8% and 75.5%, respectively (±50 basis points)

Full-year OpEx growth: Low 40% range

Data Center:

Record revenue of $22.6 billion, up 23% sequentially and 427% YOY

Demand-driven by NVIDIA Hopper GPU platform, cloud providers, and enterprises

Growth in AI training and inference

New Product Announcements:

H200 GPU sampling started in Q1, full production in Q2

Blackwell GPU architecture in full production, delivering up to 4x faster training and 30x faster inference than H100

Customer Behavior:

Strong demand from cloud providers and enterprises

Meta’s Llama 3 and Tesla’s AI cluster expansion to 35,000 H100 GPUs

Increasing AI adoption in automotive and consumer Internet applications

Market Commentary:

Geographic diversification in data center revenue

Sovereign AI investments by countries like Japan, France, Italy, and Singapore

Here are some quotes from Jensen on the earnings the conference call.

The main points are:

(i) A platform shift is underway

(ii) VC / startup spend is at full throttle

(iii) Government spending is ramping up and Nvidia is at the center of it.

(iv) Demand is not constrained.

Transcript Excerpts:

The next industrial revolution has begun.

Companies and countries are partnering with NVIDIA to shift the trillion-dollar installed base of traditional data centers to accelerated computing and build a new type of data center, AI factories, to produce a new commodity, artificial intelligence.

Token generation will drive a multiyear build-out of AI factories. Beyond cloud service providers, generative AI has expanded to consumer Internet companies and enterprise, Sovereign AI, automotive, and healthcare customers, creating multiple multibillion-dollar vertical markets.

The demand for GPUs in all the data centers is incredible. We're racing every single day. And the reason for that is because applications like ChatGPT and GPT-4o, and now it's going to be multi-modality, and Gemini and its ramp and Anthropic and all of the work that's being done at all the CSPs are consuming every GPU that's out there.

There's also a long line of generative AI startups, some 15,000, 20,000 startups that in all different fields from multimedia to digital characters, of course, all kinds of design tool applications -- productivity applications, digital biology, the moving of the AV industry to video, so that they can train end-to-end models, to expand the operating domain of self-driving cars.

The list is just quite extraordinary. We're racing, actually. Customers are putting a lot of pressure on us to deliver the systems and stand it up as quickly as possible.

And of course, I haven't even mentioned all of the Sovereign AIs who would like to train all of their regional natural resource of their country, which is their data to train their regional models. And there's a lot of pressure to stand those systems up.

So anyhow, the demand, I think, is really, really high and it outstrips our supply. Longer term, that's what -- that's the reason why I jumped in to make a few comments. Longer term, we're completely redesigning how computers work. And this is a platform shift.

Of course, it's been compared to other platform shifts in the past. But time will clearly tell that this is much, much more profound than previous platform shifts. And the reason for that is because the computer is no longer an instruction-driven only computer.

It's an intention-understanding computer. And it understands, of course, the way we interact with it, but it also understands our meaning, what we intend that we asked it to do and it has the ability to reason, inference iteratively to process a plan and come back with a solution.

And so every aspect of the computer is changing in such a way that instead of retrieving prerecorded files, it is now generating contextually relevant intelligent answers. And so that's going to change computing stacks all over the world.

How to Invest in AI

Many investors are betting on AI via QQQ or a semiconductor ETF.

That’s a mistake. We believe it’s better to do deep research and identify the mispriced category leaders.

So, we’ve owned Dell (Nvidia’s distribution partner), Nvidia, Taiwan Semiconductor, and players in the Wafer/Memory layer.

You can trace a line from the supply chain to the customer end point - we’ve found the best names there.

Note: We sold Dell last week - it’s up 75% since our purchase price and is more expensive than it’s ever been.

We have no issue locking in gains and rotating to better opportunities.

If you’ve been following us for a while, you know we spotted JPM/UBS in the banking crisis, ETHE, the nuclear renaissance theme last years, and semis in last October.

Mr. Market will create plenty of opportunities for us. We remain disciplined.

Uranium

Christine Todd Whitman, former Governor of New Jersey, came out saying we need ‘small modular reactors’ (SMRs) to power data centers.

Many companies and entrepreneurs worldwide, including Sam Altman, are trying to fund the development of alternative sources of energy.

Wind and solar power are not enough.

The energy demands are extraordinary.

We’ve been long the Uranium thesis since last year and it’s done quite well. There are many ways to play it (e.g., spot physical, miners, etc.)

Lumida Call: ASPI

In the last several months, we have been buying the stock of ASPI - Advanced Isotopes.

Our entry prices range from $2.90 to $5 ish.

Clients that were with us in February all participated at the lower price points and are all up 50% in this name.

We haven’t sold a share and don’t plan to - we expect this has a shot at being a $1 Bn business (3 to 4x). It is a highly volatile microcap ($250 MM ish marketcap), however, so not for the faint of heart.

Executive Summary: ASPI, an advanced materials company, has distinguished itself through its pioneering Aerodynamic Separation Process (ASP) and Quantum Enrichment (QE) technologies, enabling the enrichment of challenging isotopes. With a history spanning 18 years of innovative development, ASPI is well-positioned at the forefront of the nuclear and semiconductor industries. The recent legislative shifts and increasing market demands in these sectors make ASPI an exceptionally compelling investment opportunity.

Company Overview: ASPI specializes in the enrichment of isotopes that traditional technologies find challenging. This capability is critical for materials required in small modular reactors (SMRs) and advanced semiconductors, positioning ASPI as a key supplier in these rapidly evolving markets.

Technological Leadership and Operational Excellence: ASPI’s proprietary ASP and QE technologies offer substantial improvements over traditional enrichment methods, achieving efficiencies approximately 600 times greater than those of current centrifuge techniques. In 2023, ASPI completed its first enrichment facility, with revenue generation projected to begin in 2024, signaling robust operational capabilities and market readiness.

Strategic Market Opportunities:

Nuclear Sector: The U.S. has recently banned the import of High-Assay Low-Enriched Uranium (HALEU) from Russia, highlighting a significant opportunity for ASPI to supply critical materials for SMRs, essential for achieving zero-carbon energy production.

Semiconductor Industry: ASPI is set to impact the semiconductor industry significantly by producing Silicon-28, vital for high-performance semiconductors used in quantum computing. With significant backing from industry partners financing new production facilities, ASPI is strategically positioned to meet growing demands in this sector.

Financial Projections and Valuation: The upcoming IPO of its subsidiary, Quantum Leap Energy (QLE), with projected proceeds of $50-100 million, suggests a post-IPO valuation ranging between $200-500 million, potentially exceeding ASPI’s current market cap. This indicates strong financial health and growth potential, making ASPI an attractive investment proposition.

Competitive Landscape and Market Comparison: Despite Silex’s $1 billion valuation with minimal revenue generation, ASPI stands out with its proven technological superiority and operational effectiveness, led by a management team with deep experience from Highbridge and Soros. This competitive edge, combined with imminent revenue streams, underscores ASPI’s potential for a higher valuation relative to its peers.

Investment Rationale:

Technological Superiority: ASPI’s enrichment technologies provide a competitive edge in efficiency and application versatility.

Strategic Market Positioning: Positioned as a key supplier in critical and expanding markets, ASPI's capabilities align closely with the global shift towards advanced nuclear technologies and next-generation semiconductors.

Legislative and Market Dynamics: Recent legislative bans on HALEU imports and the urgent need for domestic uranium enrichment position ASPI to capitalize on national security and energy independence needs.

Proven Leadership and Swift Execution: With leadership experienced in managing and scaling complex financial and technological operations, ASPI demonstrates a clear capacity for rapid and effective strategic execution.

Risks

The customer demand is not a risk. As noted, customers including large publicy traded companies are financing the capex needs of ASPI.

The two major risks are (i) technical readiness. Each isotype requires its own plant and adaptions to the process. Management believes their technical readiness for the core business is ‘9 out of 10’, and the newer technology (‘one step laser enrichment’) is ‘7 out of 10’. Delays in delivery are a risk

Financing Risks. ASPI in the past has issued shares to raise capital. Management considers their balance sheet strong, and does not have imminent financing needs. Should ASPI need more capital or time, a secondary offering might be issued.

Licensing Risks. ASPI operates in the highly regulated isotope market. Entering new markets or delivering certain isotypes requires skillful navigation of federal and state licensing - globally. ASPI is aware of this and thoughtful in their market and isotype selection.

Market Liquidity risk. Should US equity markets experience a sharp downturn, ASPI and other small cap securities could be disproportionately punished due to thinner liquidity.

Re-balance consideration. Note: We expect Vanguard and other indices to buy ASPI to so they can include it in the Russell index on June 28th. Historically, as you get closer to the re-balance on June 28th, the price gains from that event are priced in. Also, there’s some evidence that prop desks at banks and other firms have already started accumulating ASPI in anticipation for inclusion into the Russell index. They will likely sell their position to the asset managers that run indices.

ASPI is also highly overbought. It’s thinly traded also. If you execute orders, you want to work orders slowly, and call your broker to chop up buy orders rather than flash a limit order on screen.

Good luck!

If you are looking for a wealth management partner, Lumida is now welcoming a limited number of new clients. We offer a range of services, alternative investments (such as our CoreWeave deal), white-glove crypto management, to public equity management, and high-touch family office services, including trust, tax, and estate planning.

Ready to explore? Click here to fill out our form.

Interested but not ready to commit? Build a relationship with Lumida and stay informed. Click on the poll below if you want our advisors to reach out.Software Slammed

The trend continues.

Software stocks continue to get slammed on their earnings release

This week both SNOW and WDAY released results and are down double digits

Why?

I argue it's the comparison to Nvidia - which is cheaper and growing faster than all of these.

And these software companies are spending on NVDA.

Take a look at Workday's stock. I used to own this in Q1 (along with Cloudflare NET and Atlassian TEAM).

We did a portfolio review and realized it makes no sense to own anything that is more expensive than Nvidia but grows slower.

So we sold these names before the damage.

Nvidia is the 'speed of light' in equities. Nothing can exceed the speed of light.

It's the pace setter.

We took the proceeds of selling software and rotated to energy services. Those are up nicely.

See TNK for instance.

Here is Workday's chart and Snowflake.

Snow has hit peak market cap, it is melting now.

Future Market Outlook

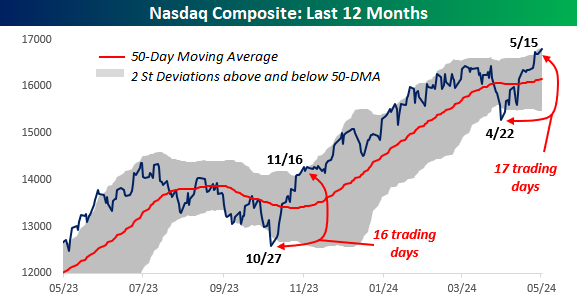

For the second time in six months, the Nasdaq has gone from 'extreme' oversold to 'extreme' overbought in less than four weeks.

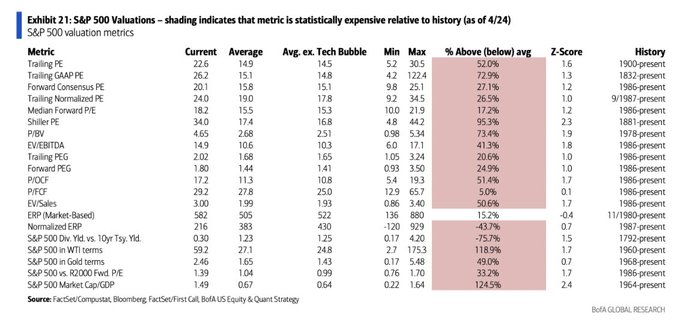

S&P 500 SPX is expensive on 19 of 20 metrics according to Bank of America

We believe that positioning is crucial.

We have a barbell approach.

We are long Meta, Nvidia and Google in Mag 7.

Then the rest of the portfolio is quality value stocks doing buybacks with ample free cashflow.

That strategy is how we found Build a Bear, which is up 30% since January 1.

Value is outperforming growth - we expect that to continue.

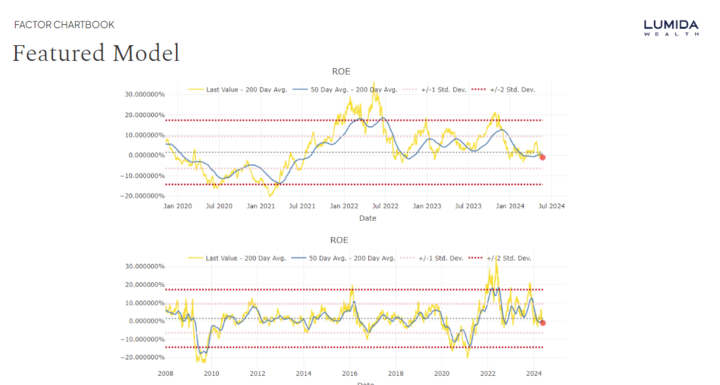

We also want to own stocks that have high ROE and Earnings Yield.

Check out these factor returns from our internal research desk.

ROE is due to bounce back. Earnings Yield (not shown) is also due for a bounce.

Guess which investor best typifies those factors?

Warren Buffett and Charlie Munger.

Now is the time to buy very boring businesses - but avoid value traps.

Find businesses growing free cashflow that ideally can buy back shares…

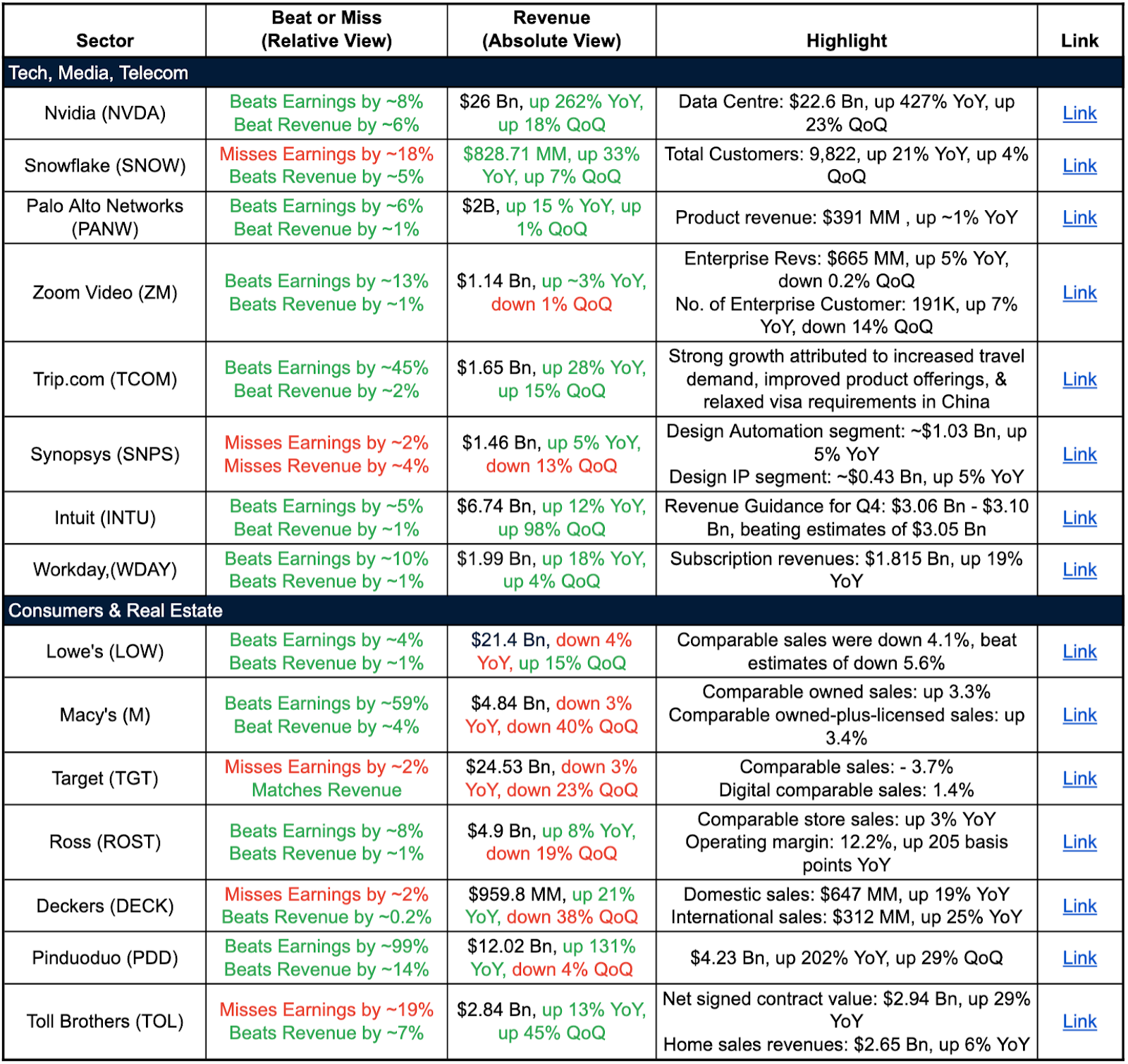

Company Earnings

Tech/Media/Telecom:

Nvidia delivers blowout results driven by staggering data center growth from AI/ML deployments

Cloud data platform Snowflake posting robust revenue gains

Cybersecurity leader Palo Alto Networks benefiting from strong demand for next-gen security offerings amid elevated threat landscape.

Videoconferencing player Zoom stabilized its enterprise business though overall growth has decelerated post-pandemic

Travel booking platform Trip.com riding recovery in Chinese travel demand

Productivity software giants like Intuit and Workday are driving double-digit revenue growth led by cloud transitions.

Consumers & Real Estate:

Lowe's and Macy's beat earnings but experienced lower comparable sales. This suggests resilience in consumer spending but also a shift towards value and promotional pricing

Big box retailer Target facing pressure on store and digital comps underscoring consumption volatility.

Off-price retailer Ross benefitting from value consciousness though discretionary sales remain uneven

Footwear brands like Deckers gaining from higher pricing in the face of elevated promotions elsewhere.

E-commerce player Pinduoduo seeing explosive revenue growth in mainland China.

Toll Brothers beat revenue but missed earnings. While home sales revenue grew, profitability might be impacted by rising costs. The strong growth in net signed contract value suggests a positive outlook for future sales

The overall picture reflects ongoing bifurcation - resilient enterprise demand enabling healthy growth for software/cloud vendors, while B2C names face a push-pull between inflated costs and moderating consumer spend. Pricing power remains key for consumer brands.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

AI

ASML has a Remotely Activated Kill Switch

Imagine this conversation.

ASML: ‘Hey there TSMC. We have a new feature.

We can remotely disable your brand new $300 MM lithography machine upon request of OUR government

This is in YOUR interest.

It’s like the Roman Siege of Masada or the Scythians…

defenders destroyed their property rather than hand over to invaders…’

If you are Taiwan, or fabricator, what is the optimal response?

Both ‘declined to comment’

Will we see AI Operating Systems with a kill switch?

Or, a backdoor?

We live in interesting times.

Excerpts Attached

Meta AI Chief Says AI Will Never Reach Human Level Intelligence

Meta’s artificial intelligence chief said the large language models that power generative AI products such as ChatGPT would never achieve the ability to reason and plan like humans, as he focused instead on a radical alternative approach to create “superintelligence” in machines.

Yann LeCun, chief AI scientist at the social media giant that owns Facebook and Instagram, said LLMs had “very limited understanding of logic . . . do not understand the physical world, do not have persistent memory, cannot reason in any reasonable definition of the term and cannot plan . . . hierarchically”.

In an interview with the Financial Times, he argued against relying on advancing LLMs in the quest to make human-level intelligence, as these models can only answer prompts accurately if they have been fed the right training data and are, therefore, “intrinsically unsafe”.

Instead, he is working to develop an entirely new generation of AI systems that he hopes will power machines with human-level intelligence, although he said this vision could take 10 years to achieve.

LeCun runs a team of about 500 staff at Meta’s Fundamental AI Research (Fair) lab. They are working towards creating AI that can develop common sense and learn how the world works in similar ways to humans, in an approach known as “world modeling”.

“We are at the point where we think we are on the cusp of maybe the next generation AI systems,” LeCun said.

‘’Achieving AGI] not a product design problem, it’s not even a technology development problem, it’s very much a scientific problem,” he added.

Check out this curation where Jensen Huang and Michael Dell discuss AI factories.

A wonderful reason to never run Windows again

MSFT Copilot PCs with Recall - End of Privacy?

Apart from AI-PCs here were the top 3 announcements from MSFT Build

Michael Dell: ‘No country can afford to outsource its intelligence’

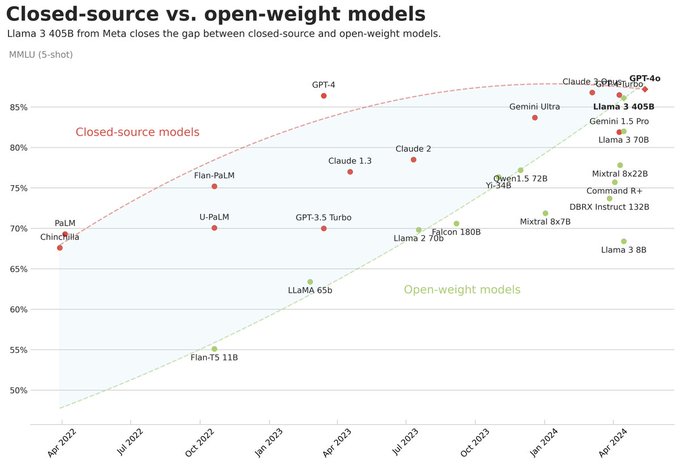

From Bindu Reddy & Beth Kindig:

We’ve been positioning around this since last summer.

The only better customers than Big Tech are governments flush with cash running war-time deficits.

LLMs are plateauing, and the gap between closed vs. open is almost closed!!

If you look at MMLU, open-source is caught up to closed source, and we are seeing the LLMs plateau.

It's time to move on to different benchmarks that measure LLM capabilities on hard problems.

The key point, however, is for simple consumer questions or web searches open-source models do as well as closed source ones. The gap is closed on simple use-cases, and this is a HUGE VICTORY for open-source.

We only need smarter LLMs for AI agents and other complex automation tasks.

All in all, we are continuing to see a trend where they will eventually become a commodity.

Digital Assets

The Grayscale ETHE Trade is Over : End of an Era.

The outcome of the DCG-Genesis mess was the creation of one of the best investment opportunities in years. The big long.

The 'Discount to NAV trades': GBTC and ETHE Last year, we were saying 'we are going to miss these discounts when they've closed'.

Guess what? They're gone. The ETHE discount has closed to a paltry discount of 1.28%. ETHE as recently as 11 months ago had a 50%+ discount to NAV.

There is no longer sufficient compensation for giving up staking yield on-chain. In one year, this investment has gone from $8 to $34: a 425% return. There were also gains along the way...

You could have bought in October of this past year and made 300% The ETHE investment was easily the most successful investment call Lumida Wealth made last year - overall and within crypto.

Congrats to all those that participated.

What we do from here? For clients that are close to hitting long-term capital gains, we're waiting a few more months to sell. For clients that got in the last 6 months, we've already sold.

Here’s the receipt of our call which was written in our July 2023 newsletter. We first shared the GBTC and ETHE ideas at the Bitcoin Miami conference.

Kudos to DavidFBailey for his leadership on the Redeem GBTC issue. That played an important role in organizing investors and ultimately changing investor psychology on this names.

What's the next big idea? Well, coming off a bear market low, you see these kinds of opportunities. We're on the hunt.

Ready to explore opportunities with us? Click here to fill out our form.

Quote of the Week

"I don't look to jump over seven-foot bars; I look around for one-foot bars that I can step over." — Warren Buffett

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.