Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we’ll cover this week:

● Macro: Inflation Tamed, Fed Cuts, Small Caps, ‘97 Repeat?

● Markets: Our Small cap rotation, Mag7 Gamma Squeeze

● Company Earnings: Strong on Banks, Mixed on Consumer & Industrials

● AI: Lumida Curations - AI Bubbles, AI Tech Value Stacks

This week I had a chat with Nic Carter, Founding partner at Castle Island VC.

Nic is a Philosopher turned Investor who is constantly challenging himself.

His work has been published in Coindesk, The Block, Harvard Business Review, New York Magazine, and Bankless.

Nick shares his personal journey into combat sports, including boxing and Karate Combat, and how these disciplines influence his investment strategies and daily routines.

Nic lays out this thesis on CoreWeave - he was a seed round investor in one of the best investments of the last 10 years. (Lumida is an investor as of November, Nic beat us to the punch 🙂)

- Coreweave, AI Investments, & Data Centers

- Digital Asset ETFs, & market cycle

- Nic's Investment process and successes

Check out the full video here. Don’t forget to subscribe.

Spotify | Apple

Time Stamps:

00:33 Nic Carter's Personal Transformation

02:52 Boxing and Investing: A Parallel Journey

11:28 From Philosophy to Bitcoin

15:12 The Birth of Castle Island Ventures

16:47 Navigating the Bitcoin Community

21:00 The CoreWeave Investment

31:47 The Future of Compute as a Commodity

38:52 Investing in AI: Strategies and Concerns

39:35 The Future of AI Models and Regulation

43:46 AI's Role in the Post-Truth Era

47:14 The Intersection of AI and Blockchain

01:10:50 Crypto Market Trends and Challenges

Macro

Here’s a video we recorded last week making the case that Small Caps are set to rally as soon as Fed Rate cuts are in sight.

I've been writing about how small caps are poised to ramp as Fed rate cuts come in sight.

This week, we saw a benign CPI print that shows all three pillars—including stubborn shelter inflation—are at levels that allow the Fed to make ‘insurance cuts’.

Not a full easing cycle, but an insurance cut to help psychology and the housing sector.

Last month, Mr. Market gave us a clue as to what would rally when inflation is beat. We saw small caps ramp dramatically after the June CPI report.

Mr. Market was previewing his intentions.

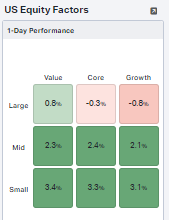

The chart below shows the performance of small caps this past Thursday.

The main question is: Is this a new trend, or is it a head-fake?

Small caps, after all, haven’t gone anywhere at the index level in three years.

And after the benign CPI print last month, we saw a one-day wonder small-cap rally that gave back most of the gains.

Our answer: This is a trend.

The breadth and the magnitude of the rally this time is significant.

Each day, our CIO team reviews dozens of charts and data, testing our hypotheses and worldview against incoming data.

The breadth and strength we see in small caps are similar to what we saw in November and December - the last strong small-cap rally.

That rally faded when Mr. Market said the Fed would not cut rates in December (or January, March, April, May, or June - or even July).

However, Lumida is now of the view that we will see September rate cuts.

Those of us following for a while know we have been skeptical of rate cuts and fading Mr. Market’s hopes of a pivot. That has worked quite well.

However, it does now make sense for the Fed to make modest one-off rate cuts rather than start an aggressive easing cycle by being late.

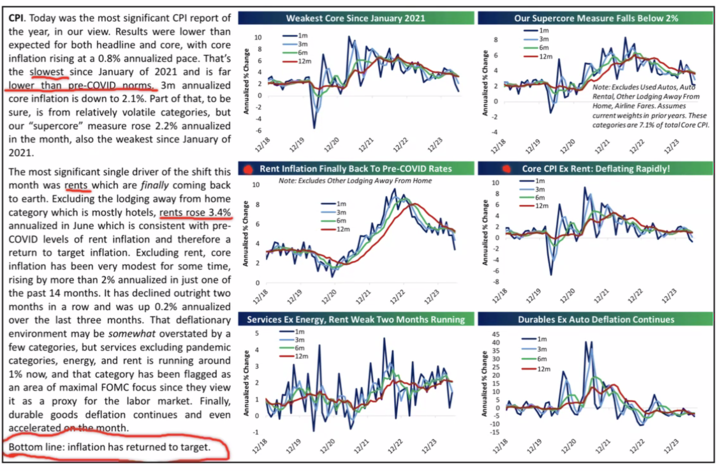

Why We Believe Rate Cuts Are Coming

Simply put, inflation has returned to target.

Take a look at this data and highlights from Bespoke.

What will rate cuts mean for the market?

Looking beyond August and September seasonal weakness - heightened by policy uncertainty - we think it’s quite bullish.

The setup reminds us of 1997.

You have the Fed easing…and there’s no recession.

The rally will broaden to small and mid-caps. That lets the bull market expansion continue.

Even today, there are so many individuals that are offsides hiding in Treasuries…

The top will be when they get back in the market.

Markets

Take a look at Brazil's EWZ.

The red line is when we said in December Brazil is overbought.

The green line is when we bought into the market - via our pick Pag Segeuro (Ticker: PAGS)

We did that by watching the US Dollar and rate cycles.

This was a satisfying entry.

Some of you have asked - why not buy Nu Bank or Mercado Libre.

it's really simple: those names—and they are great businesses (especially Meli)—have limited room for multiple expansion.

Multiple expansion is the primary driver of returns. We can own PAGS for 10 years and let it compound without paying taxes. This is what makes Buffett such a great investor…

If we bought Nu Bank, it would be fully priced within a year or two, say. Then we would need to rotate and pay taxes.

If you can find a great entry in a great business and hold on to it for a long time, you are creating wealth.

People will talk about Pag Seguero in ten years like they talk about Nu Bank or Mercado Libre now.

That said, if we had a major correction and these businesses were trading at 50% off, you can bet we would buy them.

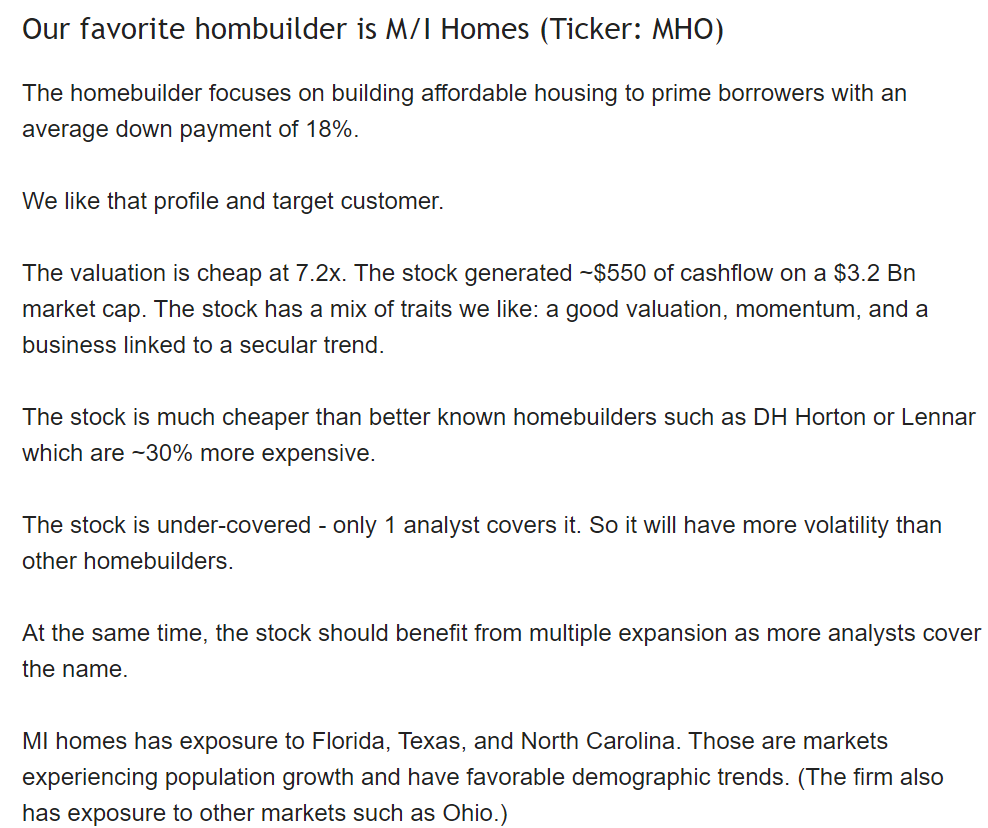

Small Caps: A Check-In on M/I Homes

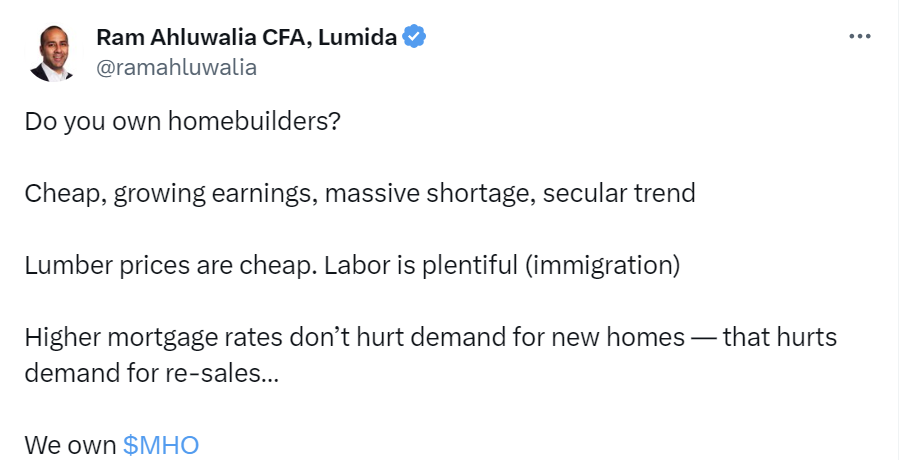

On April 23, we wrote, “Do you own homebuilders?” and shared our pick of M/I homes.

We wrote about M/I Homes in our April 14th newsletter. Here’s an excerpt:

M/I Homes outperformed the other homebuilders we track - KB Homes, Lennar, DreamFinder, etc. - on this small-cap rally. No surprise - it’s cheap, has growing earnings, has buybacks, focuses on starter homes, has financing incentives…

What’s not to like?

Here’s M/I Homes, our April buy call, and where it is now.

That’s a 17% gain in the last 3 months.

This was a difficult hold for us. Internally, we had many debates about the deterioration in multifamily housing.

Multifamily incompletion rates are rising, and starts are slowing.

On the other hand, rate cuts are coming, and it’s a great asset.

We could have done better by waiting for better technical support from the 200-day moving average.

The ideal entry would have been 8 days ago, but you would only have had a 2-day window, and we might have missed it.

In fact, there’s another small cap where we were looking for an ideal entry. We saw it last Thursday, and it gapped up 5% as we spotted the entry. Apparently, others in the market were looking at it at the same time, so we missed that.

The stock is up 21% in two days. It’s quite painful as we saw this and were actively stalking it. We’re reluctant to chase, and we’re quite patient.

So, in one case, our style benefitted us, and in another case, we missed an opportunity.

The only thing we can really do here is reflect on those scenarios and see how we might have improved our decision-making.

Hindsight is always 20/20.

Someone looking at this last week might have also said that the name broke support after all.

Why We Love Small Caps

I love the small cap rotation for quite a few reasons.

Please look at an earlier Lumida Ledger where we make the case that small caps will have a strong 2024. We lay out various technical studies showing small caps are poised to rally.

What those studies miss is that macro backdrop. Now, the Fed Rate cuts are in view.

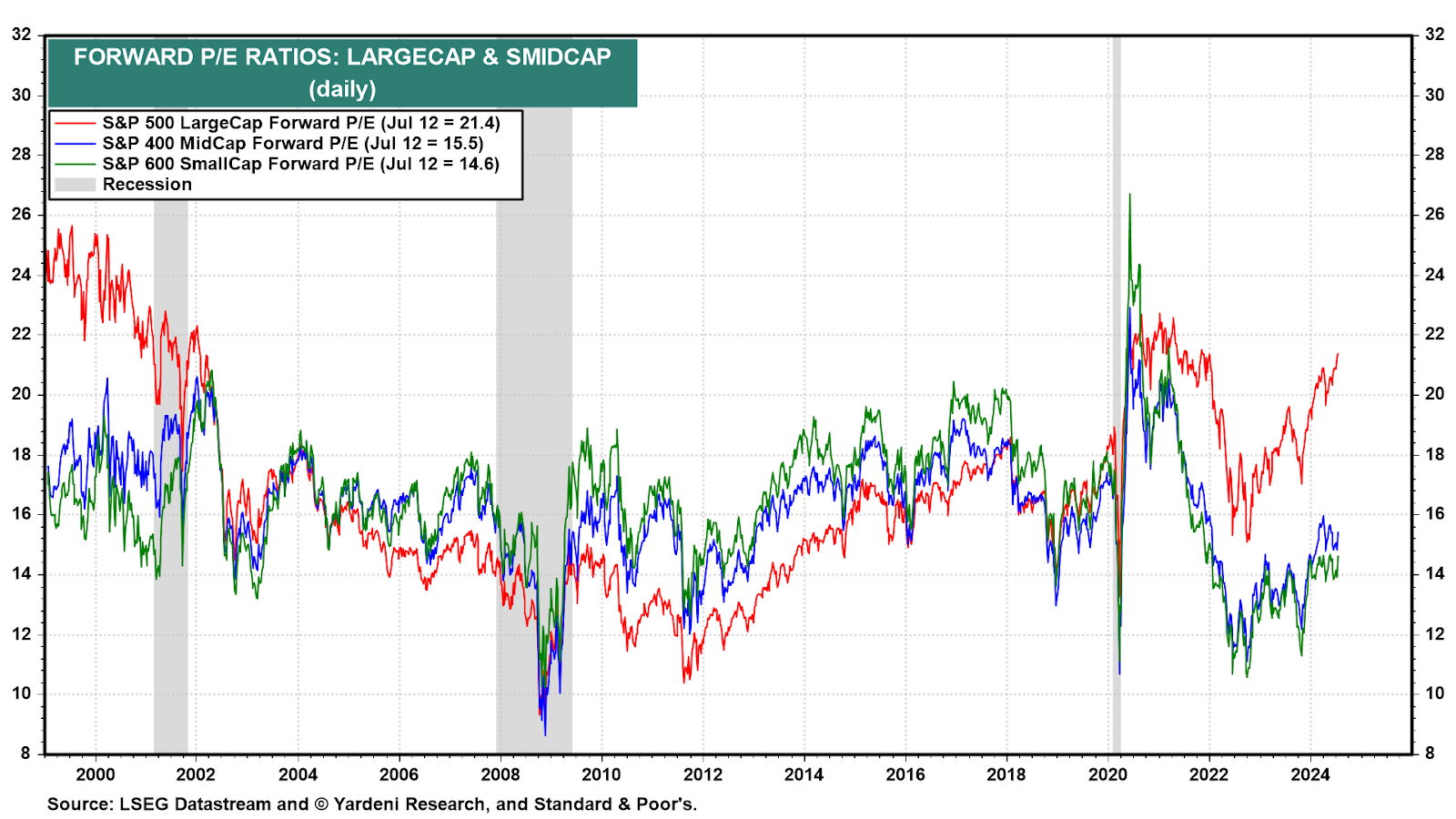

Take a look at the relative valuations of large caps to small and mid-caps:

Valuations are cyclical time series, representing the psychology and animal spirits of investors as well as the business cycle.

Small caps can run quite a bit from here and are below historical average.

Another reason is that analysts don’t cover small caps much. Back in the day, the best analysts would cover small caps. The junior analysts would cover large caps.

A lot has changed since then.

If you can spot a good business model, moat, management team, catalysts, and sustainable business – you have an edge in small caps.

Institutions are like whales - they get exposed to small caps via indices over a stock selection

It takes months for institutions to position into small caps. They have to start by purchasing ‘macro products’—indices and futures outright.

So, if you’re not BlackRock, you can front-run them.

Small caps are also a type of growth equity investing Understanding these businesses is a lot of fun.

Over decades of history, small caps have delivered higher returns than large caps. That phenomenon has not been true in the 2010s, the age of mega cap tech.

However, as mega-cap tech approaches the high end of its valuation range, we expect those names will increase share price via earnings growth rather than multiple expansion.

We can get both in small caps!

People underestimate the return potential in small caps.

Take a look at American Public Education.

This stock is one of Lumida’s Stocking Stuffers. It’s up 85% YTD and 285% in 1-year.

Those returns blow Mag 7 out of the water. And the forward PE ratio is still 12x.

You still have to get your picks right, and if the name doesn’t work, sell the stock and don’t look back.

One mistake we made that was also on our Stocking Stuffer list was Zoom Communications (ZM). That was a Covid darling.

It throws off a lot of free cash flow and has a cheap valuation.

But it hasn’t worked. We were wrong on that one. We sold it within a few weeks and moved on.

Cutting losers is crucial.

Here’s another small-cap idea: Jackson Financial (ticker: JXN).

Jackson was a spin-out of Prudential.

They sell annuities and other products to retirees. We like that because we believe this is a Boomer economy. (Look at Cruise lines, restaurants, travel, and healthcare spend…)

Their business model is simple to understand, and they have a strong customer value proposition. Boomers want income and become risk-averse as they age.

Jackson has a free cash flow/enterprise value yield of 50%.

They are buying back 6% of their stock. We like buybacks for the same reason Warren Buffett does. You own more of the company for doing nothing.

The stock is up 50% YTD and 140% in 1 year. It has momentum and a strong trend.

That means institutions are buying this, likely via a VWAP order.

And the Forward PE ratio is 4.4X.

So, this can compound for many years.

Take a look at the chart.

A stock like this has many of the qualities we look for:

- On theme (boomers)

- Good factor exposures: profitable, value, momentum

- Strong customer value proposition

- Free cashflow + buybacks

- Quality customer: boomers

- Demographic tailwind

We are “stacking edges” in quite a few ways here.

We noted in May that there are quite a few opportunities in insurance.

This is one of several bets we have in the insurance space.

Remember how Auto insurers passed on a 24% CPI to consumers? That’s the sign of a strong business model and revenue growth.

No one is talking about Insurance - except for Buffett, who bought Chubb. (Our edge over Buffett is we don’t need to hunt elephants - Buffett could never buy a name like Jackson - it’s too small.)

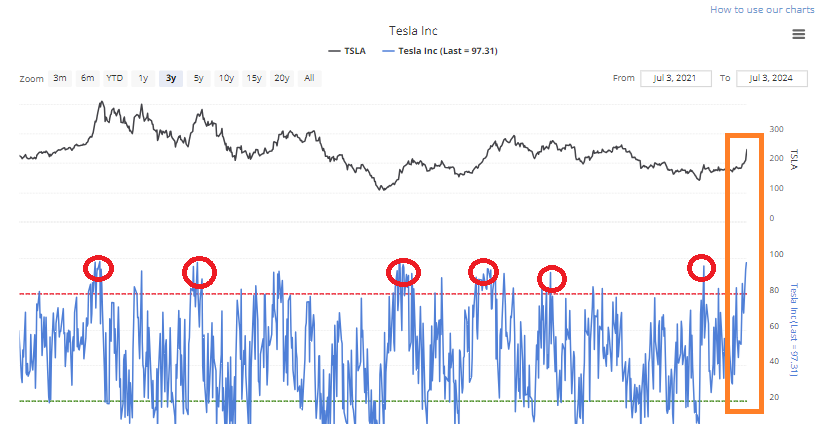

Mag 7 Call Gamma Squeeze

There’s been a tremendous amount of call option buying on every Mag 7 name.

There is a call option gamma squeeze. Speculative traders are front-running earnings.

Put/call ratios were at record lows.

We believe a lot of those recent calls will expire worthless on next Friday’s options expiration.

The technical factor of call option buying - combined with real earnings revisions - played a role in the rally.

And you have strong positive seasonality the first two weeks of July.

You can see that call gamma squeeze in Tesla here:

You can read the original post here.

Company Earnings

Q2 Earnings cycle has started, here’s a quick curated review of the trends and insights from Q1: Lumida Earnings Review Q1 2024

Here’s an analysis of important earnings from this week - you can read more about them on our news website, by clicking on the company name below (bookmark for daily updates).

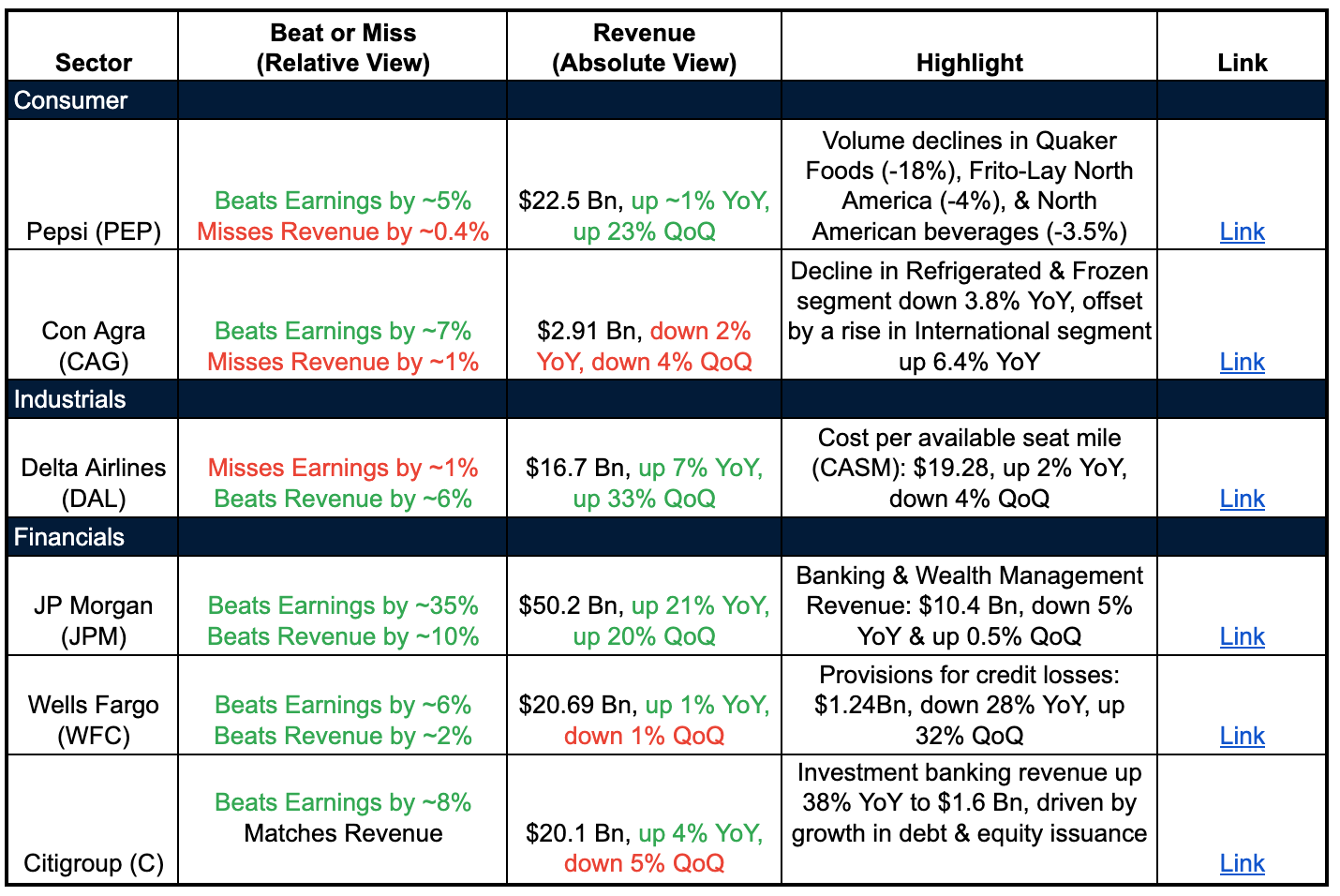

Consumer Staples:

● Pepsi (PEP): Revenue growth might be slowing down due to volume decline in key segments

● ConAgra (CAG): International segment growth is a positive sign but revenue from core business segments down

Industrials:

● Delta Airlines (DAL): Revenue growth is positive but rising costs need attention

Financials:

● JPMorgan Chase (JPM): Strong overall performance but Banking & Wealth Management revenue decline

● Wells Fargo (WFC): Improving credit quality but YoY revenue growth is stagnant

● Citigroup (C): Strong investment banking growth indicates a positive trend

AI:

Lumida Curations of the Week

In case you missed it, here are some of the best curations from Lumida Wealth on Twitter.

Be sure to follow Lumida Wealth on Twitter, and on Youtube, where you can get more such curations.

Instead of watching hour-long market podcasts - we distill the key insights in 1 min shorts and serve them in threads.

The goal is to maximize insight per unit of time.

Here’s Beth Kindig from I/O Fund on Realvision on AI, Crypto & NVDA

Here’s Wharton Professor Jeremy Siegel & Wisdomtree CIO Jeremy Schwartz on AI bubbles, small caps, and inflation.

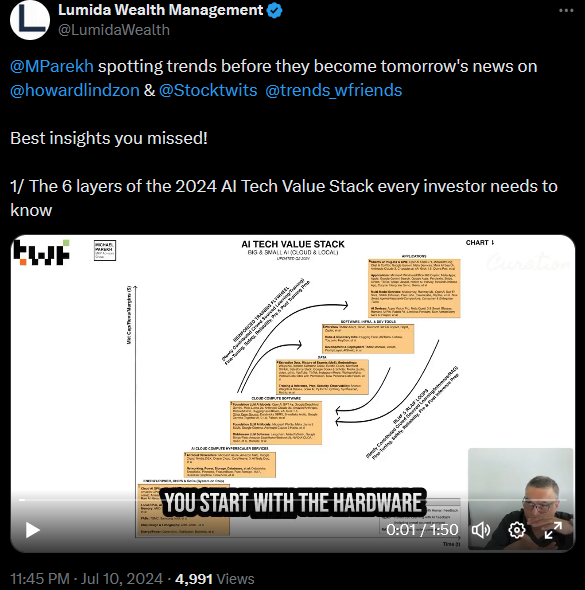

Lastly, here are our friends Michael Parekh & Howard Lindzon on AI Tech Value stacks:

If you are looking for a wealth management partner, Lumida is now welcoming a limited number of new clients.We offer a range of services, alternative investments (such as our CoreWeave deal), white-glove crypto management, to public equity management, and high-touch family office services, including trust, tax, and estate planning.

Ready to explore? Click here to fill out our form to start the discovery process.

Interested but not ready to commit? Build a relationship with Lumida and stay informed. Click on the poll below if you want our advisors to reach out.Quote of the Week

“The stock market is there for you to make money, not to show you how clever you are.” - Peter Lynch

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.