Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Macro: Non-Consensus Investing, China & Trade Wars

Markets: Buffett’s Latest Bet, Youtube beats Netflix, 44% returns in 1 month?

Company Earnings: SaaS Resilient, Retail Uneven

AI: Arms Race, GPT 4o, Apple & OpenAI?

Digital Assets: Blackrock, BTC ETFs

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

This week, we had a fascinating conversation with Michael Parekh.

Michael is an intellectual tour de force. He was a luminary tech analyst who later became a Partner at Goldman Sachs.

He was the GS analyst during the internet era that took many great tech firms public.

We discussed Humanoids, Small AI, Nuclear, Meta Llama 3 + Groq, Nvidia, Saudi Arabia and Geopolitics.

He advises several leading firms in the AI space today.

We unpacked some amazing topics on the livestream! Jump right in with YouTube timestamps to key themes below. Like, share, and subscribe to help us grow and attract industry leaders for future episodes.

02:02 OpenAI's Latest Innovations

04:11 Exploring the Quest for AGI and AI Reasoning

07:27 OpenAI's Competitive Edge in the AI Race

10:26 Meta's Strategic Moves in AI and Social Media

24:29 The Future of AI in Personal and Professional Life

32:13 Humanoids and Robots: Hype or Future Reality?

38:03 Exploring the Future of Humanoid Robots and AI

39:11 The Evolution of Boston Dynamics and AI in Robotics

40:19 The Rise of Home Robots: From Roomba to AI Integration

44:18 AI's Impact on Chip Technology and Data Centers

46:50 The Shift Towards Edge AI and Local Processing

50:19 Qualcomm's Role in the AI Chip Market

55:15 Rethinking Operating Systems for an AI-First World

01:00:00 The Reality of Full Self-Driving Technology

01:09:55 AI and the Future of Work: Optimism Amid Disruption

01:15:23 Exploring the Gig and Creator Economies

01:17:13 Debating Google's Dominance in AI-Driven Search

01:20:11 The Potential of Meta and NVIDIA in AI Development

01:25:03 Nuclear Energy's Role in Supporting AI and Technology

01:31:07 Unpacking the Complexities of Energy for AI's Future

01:32:49 Geopolitical Dynamics in Tech: AI, Energy, and Innovation

01:43:11 The Business Cycle of Bundling and Unbundling

Links to the audio podcast:

All the hedge funds reported their 13Fs this week, and we at Lumida were ready for the Whale Watch with our binoculars.

e are some highlights for those who can’t squint 🙂

Note: We include the handful of hedge funds we admire and several we think are terrible. You need to look at both. The point is a ‘tally’ of popular positions. (And that’s not non-consensus).

1. META is the most favored position among all hedge funds

We agree. Meta is a top 5 position. The last big buy was when they tanked on earnings 15%. It’s now largely closed that gap. What a gift.

2. HF favorites in order are META, MSFT, Amazon, Nvidia, Apple, and Google

We believe Google has the highest risk-adjusted return. (At the beginning of the year, that was Nvidia.)

3. TSLA, not a top 5 holding for any fund

No kidding. Tesla is facing an onslaught of competition and weakening consumer demand. And accounting issues potentially.

4. GLPs are notably underweight except for LLY

Makes sense. We rotated out of Novo Nordisk about 2 months ago. Looks like hedge funds did the same.

5. Outside Quant funds, Apple is the least favored Mag 7 name

It’s essential not to over-read quant hedge fund positions. They turnover their book quickly.

Apple, as least favorite, also agrees with what we’ve said.

Check out the full excel sheet and previous editions of Whale Watch here:

ow Did Lumida Stocking Stuffer Do?

As a regular reader of Lumida you may remember our Stocking stuffers list from Dec 2023. Here’s where it is 5 months later (on an equally weighted hypothetical $3M portfolio).

We’re up 20% on these names. That’s beating the QQQ by 2x and the S&P 500.

Send us other Top 10 lists. We haven’t found anyone do any better - including Barron’s.

st does not include names we were buying for clients at the beginning of the year like Nvidia or Meta, or calls since then.

Our track record speaks for itself, even without disclosing all our holdings (NVDA, META calls, TSLA, SOFI shorts).

If you are looking for a wealth management partner, Lumida is now welcoming a limited number of new clients.

We offer a range of services, alternative investments (such as our CoreWeave deal), white-glove crypto management, to public equity management, and high-touch family office services, including trust, tax, and estate planning.

Ready to explore? Click here to fill out our form.

Interested but not ready to commit? Build a relationship with Lumida and stay informed. MACRO

Non-Consensus Investing & China

If you:

- Banks in March of last year

- Google in Feb after ‘Death of Search’

- sold Apple last summer and bought TSMC

- bought semiconductors in the October dip

- bought Uranium before Goldman’s Buy rating

- and bought Crypto last year, you qualify as a contrarian and should join Lumida Wealth

The common theme here is this…

When (i) a dislocation occurs and (ii) bad news is priced in (e.g., you see evidence of capitulation), you (iii) seek out the highest quality assets.

Then, wait patiently for Mr Market to catch-on.

We have been scooping up energy services for two months now.

Mr Market has been lifting them in the last week.

I could write out a quasi-formula and most people would find a way to rationalize themselves out of taking action.

- ‘This could be another 2008’

- ‘Recession’

- ‘China is un-investable’

- ‘Energy is cyclical’

- ‘But… it’s Apple, safe as a money market’

Temperament in investing is just as important as analytical skills. Millions of analysts, many underperform because their amygdala causes them to make bad decisions when stress is high.

This article about China’s population scrambling to invest in gold bars gave a strong clue that the markets were nearly bottoming.

looiden Adds Tariffs on Chinese Chips, Critical Minerals, and EVs

EV Tariffs on China are set to jump to 102%!

Tariffs are Taxes.

They fall partly on consumers, even if producers pay them.

None of that helps Americans.

If you drive a Toyota, Honda, Nissan, Volkswagen, BMW, Mercedes, Audi, or any number of other brands, you would recognize that product quality has jumped due to global competition.

We are all better off enjoying French wine, Greek olive oil, German cars, Taiwan’s chips, Canada’s uranium, Lenovo’s PCs, South Korea’s LCDs, and Ireland’s butter.

The dollars we pay for those goods and services must be spent, mathematically, on our exports OR on financing the United States' needs (e.g., bonds, foreign direct investment, etc.).

It’s an accounting certainty.

A subsidy from China is a gift to US consumers.

Politicians are pandering to an uninformed electorate.

Get tough on China around IP theft and espionage.

Not on consumer products where Americans are feeling the pinch of inflation.

A $10K EV would boost the real incomes of Consumers.

And how does it make sense to levy tariffs on ‘critical rare earth materials’?

Aren’t they ‘critical’?

Funuying China

Turns out we weren’t the only ones. Take a look at who else bought Ali Baba.

Mar

y ng.

We wrote a post this past Tuesday on X: Lumida Call: Time to Sell Restaurants.

The very next day, Bill Ackman released his 13F filing. The 13F shows what hedge funds are buying or selling. Ackman sold ⅓ of his Chipotle position…

(1) Restaurants are not quite at, but are approaching, 201 valuation levels. And revisions are negative.

Shake Shack, a name we liked at the beginning of this year, has had a tremendous rally and is now sporting a 131 P/E Ratio.

We recommend rotating out of these.

Restaurants as a category are more expensive than Taiwan Semiconductor TSMC, which is the most globally systematic institution on planet Earth.

I believe it, along with Chipotle and, Sweet Green, and others, are overbought.

Shake Shack is near its 2021 peak and has a 131 P/E ratio.

(2) Have a look at my watchlist on Restaurants.

hownds on the Ris36% in 3 months) are crushing Aging Brands (-23%) or Brands in Decline (-6%)

(3) Wall Street organizes restaurants into categories like QSR (Quick Service), Fast Casual, Burger, etc.

I believe that misses the primary dimension - and it shows.

How you organize your information is how you structure and organize your analysis.

Don't get me started on small-cap value vs. large-cap growth...

(4) I would recommend you scrub your portfolio for any stocks more expensive than Nvidia in terms of forward PE (unless it is growing earnings faster than Nvidia, which it isn't)

Those stocks are the most vulnerable.

Chipotle's burgers don't come with a side of GPU chips.

For instance, CMG has a forward PE of 55 vs. Nvidia at 36.

Bill Ackman gave an interview about how valuations don't matter; you just want to find great businesses.

That's what a top signal looks like, folks.

kman Dumpinipotle

Ac is quietly exiting his position… by not talking about this concentrated position.

Notice Buffett had 1 sentence on Apple in his last filing.

I take some satisfaction in tagging both at the exit door :)

Notice Chipotle was down today while indices were up sharply.

Knowing how others are positioned adds a bit of edge.

Retail investors are providing the exit liquidity (chasing momentum) — and that’s a bad idea.

The smart money is out of this name.

On Google

YouTube is the #2 company in total TV time spent—the power of the creator economy is real, and advertisers need to shift to targeted digital spending faster.

We’re all going to spend more time on AI-intermediated content.

Think about how much money is spent on premium content by YouTube's competitors, who generate far less viewership.

Nuclea w Congress ed a bill to limit imports of Russian nuclear fuel (subject to DOE exceptions).

This week, the US is building up a mini- Strategic Petroleum Reserve.

Let’s check in on Talen Energy, a nuclear reactor play we wrote about in this newsletter in February.

We wrote about the stock on the first Sunday in March. TLNE's price was $75. Now, it is $107.96.

That’s a 44% return.

Here’s when we shared our Talen position in the newsletter.

Today, we believe Nuclear Energy names like Constellation are overvalued. That doesn’t mean they will drop now; it just means this theme has run its course.

Talen is not as well known, but it can keep running on a relative basis.

We will wait for long-term capital gains and re-assess at that poi

our otium namas been running, too.

I mentioned we sold Cameco (CCJ) about a week after Goldman gave it a buy rating, which pumped the stock. Our issue with Cameco is that they are actually short uranium and not producing enough to meet the demand. They are also therefore not a pureplay bet on Uranium.

We rotated to UEC - an unhedged American uranium miner.

UEC was up 6% this Friday, and anything touching uranium was up.

Wetited aboumicrocap ura firm. We are still buying it for new clients so we can’t write about it here. We’ll use codeword LASER when we can share more.

Inspire Medical Systems (Ticker: INSP)

It’s worth sharing calls that we either got wrong or not working.

Here is Inspire Medical Systems. This is a name we bought around the green circle on this chart.

The stock dropped after earnings reported. Our lesson here is that one should not own any growth stocks that have a higher multiple than Nvidia. (If you own something more expensive than Nvidia, it better generate more cashflow growth than Nvidia…and nothing does.)

We cleaned out our portfolio 1 or 2 months ago of such names - including Cloudflare.

But, we did keep Inspire. That was a mistake. We took our tax loss harvest.

We still like the company very much. The higher level idea is that Value Stocks are outperforming Growth, and we expect that to continue.

Mr. Market is looking for value - something we have written about extensively over the last several weeks.

If we happen to see Inspire capitulate (along with other growth stocks), we may pick it back up again.

Interestingly, Inspire is cheaper than it’s ever been relative to itself. That was a consideration in our buy decision. But, it’s more expensive that most stocks in the market. And those other stocks are performing - energy services, financials, and leaders like Nvidia. So, that dynamic keeps these ‘growthy names’ in check.

There are other themes competing for capital.

Inspire Relative Valuation Analysis

As a reminder, Inspire is a play on Aging Demographics. They provide sleep apnea solutions to the fastest growing demographic cohort: ‘the oldest of the oldest’.

Warren Buffett's 13F Lifted S&P to New Highs

Buffett's investment in insurer Chubb (CB) lifted the stock 7%

Warren is back to his second love (insurance)

In the 2H of last year, Buffett revealed he was scooping up investments in multiple homebuilders.

9 months later his investment in $DHI is up 30%, outpacing the S&P...

Buffett has 'alerted' the market that the next rotation is in Insurance.

Notice quite a few insurance companies rallied in sympathy with Chubb.

Insurance premiums are elevated due to recent hurricanes in FL. YoY premiums have gone up 6%.

And their stocks have lagged. So, the bad news is priced in, and they are making more money.

Buffett has single handedly re-focused Mr. Market, like the eye of Sauron, on the Insurance sector.

And, if we get a 'trend kick-off', we can get returns of 30% much like homebuilders on the second half of last year.

Insurance is also consistent with what Mr. Market is building up: Value.

We have extensive "prepared research" on different categories and an a priori view of the best businesses in the world.

Then we wait for the theme to perform or the asset to go on sale for silly reasons.

That's part of what allows us to stay ahead of Mr. Market or at least anticipate the turn.

We believe Buffett is creating a renewed focus on Insurance names. We have identifide 2 or 3 companies that are at final stage of analysis… They look pretty good.

Company Earnings

Tech, Media, Telecom:

Mixed earnings results, with some companies beating expectations (Baidu, Tencent, Nu, Monday.com, Applied Materials) while others missed (Alibaba).

Revenue growth is slowing down for most companies, with some even experiencing QoQ declines (Alibaba, Baidu, Applied Materials)

E-commerce and cloud computing segments are showing slower growth compared to previous years (Alibaba)

The gaming segment is experiencing mixed results, with declines in China but growth internationally (Tencent)

Fintech companies are showing strong growth in customer base and purchase volume (Nu)

Software-as-a-service (SaaS) companies are maintaining high net dollar retention rates and increasing their high-value customer base (Monday.com)

Semiconductor companies are facing challenges, with declining sales in the US but strong growth in China (Applied Materials)

Consumers:

Retail giants are experiencing mixed results, with Walmart beating earnings expectations while Home Depot missed on revenue

Comparable sales in the US are declining for Home Depot, indicating a slowdown in the home improvement sector

Walmart's e-commerce sales continue to grow strongly, suggesting a shift towards online shopping

Customer transactions are down for Home Depot, which could be a sign of reduced consumer spending on discretionary items

Overall, the tech sector is facing growth challenges, particularly in the e-commerce and cloud computing segments. However, fintech and SaaS companies are showing resilience. Traditional retailers are experiencing mixed results in the consumer sector, with e-commerce continuing to gain traction. Companies may need to adapt strategies to navigate the evolving economic landscape and changing consumer prLi

arlow tion as a BATNA.

Zuck is creating negotiation leverage for AAPL even if he’s not in the chat.

Long: META

BATNA = Best Alternative to a Negotiated Agreement

Tim Cook: ‘But Llama 3…’

That’s all he has to say to get a better price.

OpenAI needs revenue for valuation.

Small Tech Firms Bracing For Consolidation

Last weekend, our Lumida Wealth newsletter was titled: ‘Where are all the great tech investors?’

We sought to answer why fancy tech hedge funds lag the benchmark.

One of the points raised is that the leading tech firms in Mag 7 have extraordinary competitive advantages.

Big Tech can pick off the businesses of smaller tech firms (see Microsoft’s entry into data & analytics, or Google’s entry into cybersecurity, etc.)

That’s hapng in AI now.

Excerpt from Bloomb

problem hat the costtalent and cting for developing AI are high and immediate, while the payoff from feeding all that data into AI models and the path to commercializing the technology is distant or unclear for many smaller firms. That leaves them burning through what funds they have — with little hope of an immediate revenue stream.

“Incumbents with scale, data, capital and distribution have a natural advantage,” Sequoia partner Stephanie Zhan, who focuses on early stage investments, told us. Sequoia was one of the first backers of Nvidia Corp., now the top provider of chips that power AI models. The firm also is involved in OpenAI, valued at $86 billion in February, but continues to target new startups that are focusing more on tangible AI products and less on the underlying foundation models that train the tools. “New startups have a shot,” Zhan added.

There was a sentiment expressed that ‘Big Tech’ is playing an oversized role in absorbing the competition. One large-scale example this year is Microsoft Corp.’s hiring of Inflection AI’s founder-CEO Mustafa Suleyman and most of his staff. The company had been in talks to raise more money, prior to the move by Suleyman and other workers to the giant software company, which is also a major investor and partner in OpenAI.

“There's certainly a lot of air being sucked out of the room by Big Tech, but there's still a ton of opportunity for startups,” said May Habib, CEO and co-founder of Writer, which makes an AI writing assistant for businesses. “Even though it feels like we are going to go through a big consolidation phase, I still think there's a ton of opportunity for startups.”

On Open AI:

Quick Take on GPT-4o Demo:

1) We are in a ‘slow take-off’ world for AI

The demo shows potential.

There’s still work to be done (eg, native AI built-in the OS for example, and always on AI)

‘Fast Take Off’ world could be a year away with the intense pace of competition from OpenAI, Google, Meta, Perplexity, and others.

2) Behavior change.

The demo was effective… but is it enough to get behavior change and regular adoption though?

An Apple integration with Open AI would significantly increase my daily usage of AI.

That deal makes sense for Apple and OpenAI.

3) What’s missing is an Operating System that is AI-first

The inability of the AI to ‘see’ the desktop and copy/paste code hinders speed.

If you agree we need an AI-first operating system, then Microsoft has risk in a few years.

4) AI is broadening out its use cases beyond coding.

We often see the AI trying to see or access information contained in a different context window.

That’s the constraint.

5) Multi-modal text, video, and audio is impressive

6) We don’t need Prompt Engineers.

We need workflow engineers to start mapping existing process to AI-driven processes.

AI is the new microservice

If ‘fast AI’ world is one year(ish) from today, then the time to plan and prepare for rapid take-off is now.

Firms that are AI first will have a speed and margin advantage that can compound quickly.

Digital Assets

Crypto: BlackRock will buy and give us a God candle

BlackRock: When crypto is praying to God, we will buy that candle

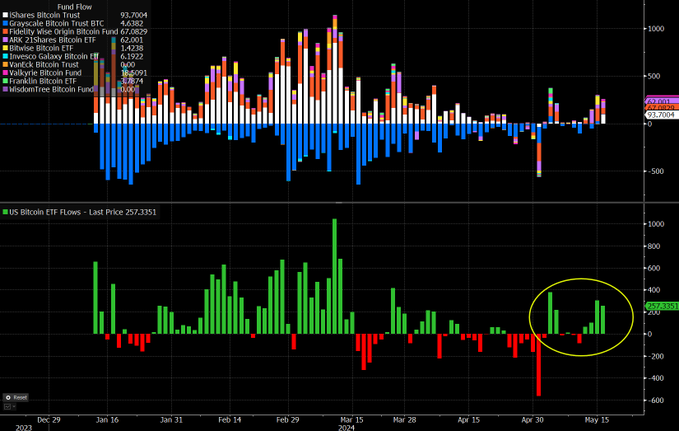

Per Eric hunas (Bloomberg): Titcoin ETaut togethesolid two weeks with $1.n inflows, which offsets the entirety of the negative flows in April- putting them back around the high water mark of +$12.3b net since launch. This key number IMO bc it nets out inflows and outflows (which are normal)

Memethe Week

Q oe Week

fir I heard when I he business, not from my mentor, was bulls make money, bears make money, and pigs get slaughtered. I'm here to tell you I was a pig. And I strongly believe the only way to make superior long-term returns in our business is by being a pig.” - Stanley Druckenmiller

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.