Here’s a preview of what we’ll cover this week:

Macro: Trump’s decision, Tax Bill Tensions, Fed’s growth reset, Dollar short positioning

Market: HOOD vs X, ETH’s Stablecoin Edge

AI: AI Defense Spending

Lumida in the Spotlight

This week, Lumida’s CIO Ram joined Real Vision to break down the under-the-radar rotation happening in digital assets.

The basic idea is that stablecoins are surging. This will disproportionately benefit some chain vs others - we believe ETH is a natural beneficiary.

ETH has also been the funding leg as it has been a popular crowded short. ETH also has significant momentum from the April lows out-running all other major digital assets.

That combination may lead to continued outperformance.

Watch the featured clip here.

Catch the full Real Vision episode here.

Macro

Trump made his decision.

On Saturday, while markets were close — and allowing a full day of messaging on Sunday shows — Trump confirmed what we previewed four days earlier:

No hesitation. No ground troops. No second guessing.

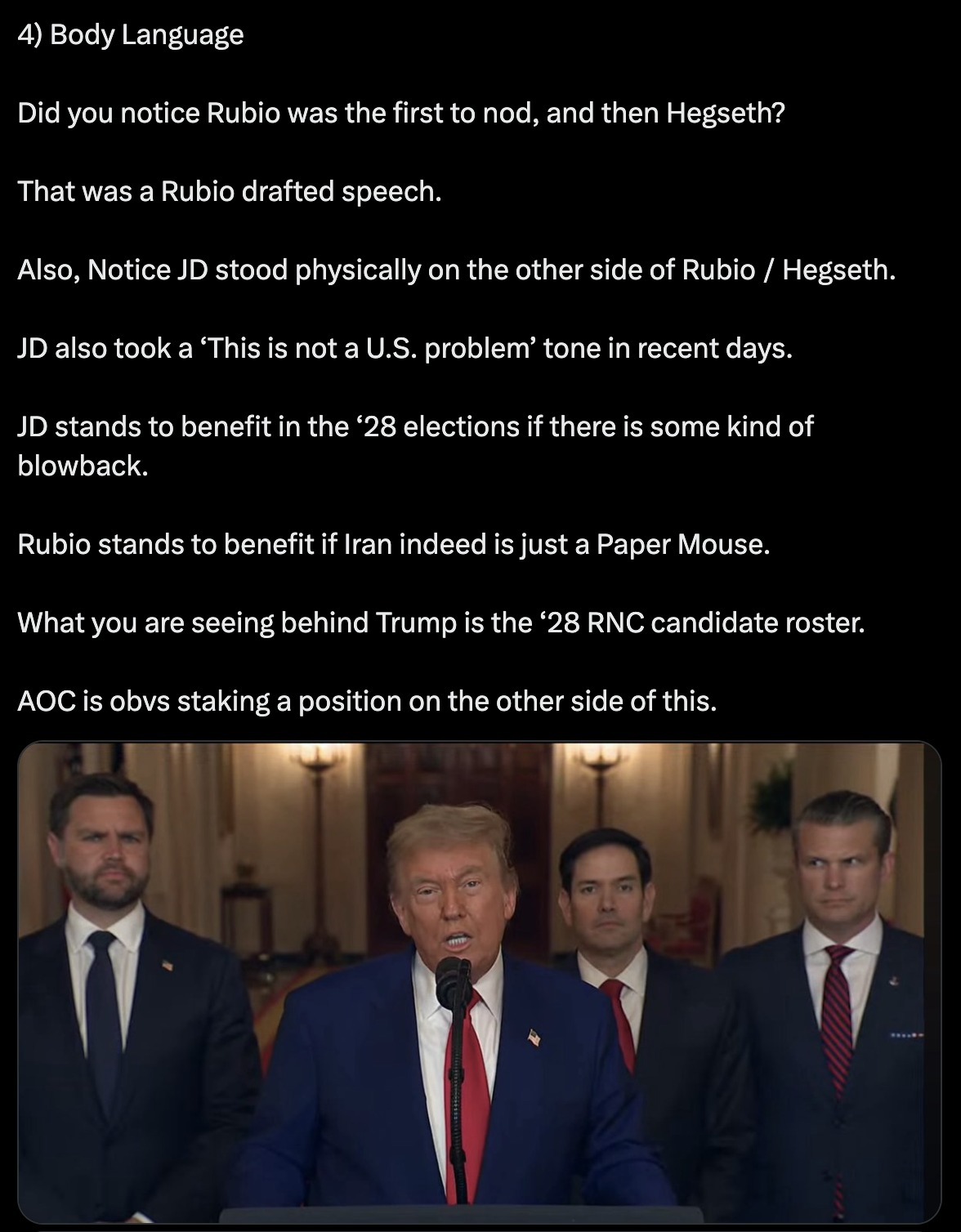

Trump’s inner circle - Rubio, Hegseth, and Netanyahu - all played their part.

And if you looked closely, the signs were everywhere:

Rubio nodding before Trump spoke

Hegseth already boosting USAF budgets

Even Fox News running glide-path simulations of bunker busters

This wasn’t impulsive. It was the Rubio doctrine delivered with Trump’s branding.

What Was Hit?

Fordow, Natanz, Esfahan.

All three struck.

No casualties. No escalation. Just dominance.

And now?

Iran filed a complaint… at the U.N.

That’s it. That’s the retaliation.

This isn’t Iraq 2.0. There will be no World War 3.

You can’t have WW3 when the matchup is this lopsided.

The historical parallel isn’t Fallujah. It’s Slobodan Milosevic in the ’90s — a quick, clinical U.S. Air Force operation that ended with no long-term drag.

Strait of Hormuz?

Also a nothing burger.

Iran can’t block it, China won’t let them, and Putin is quietly cheering Israel from the sidelines.

Even if Iran wanted to escalate, the narrowness of the strait works against them — U.S. naval power dominates that chessboard.

So What Now?

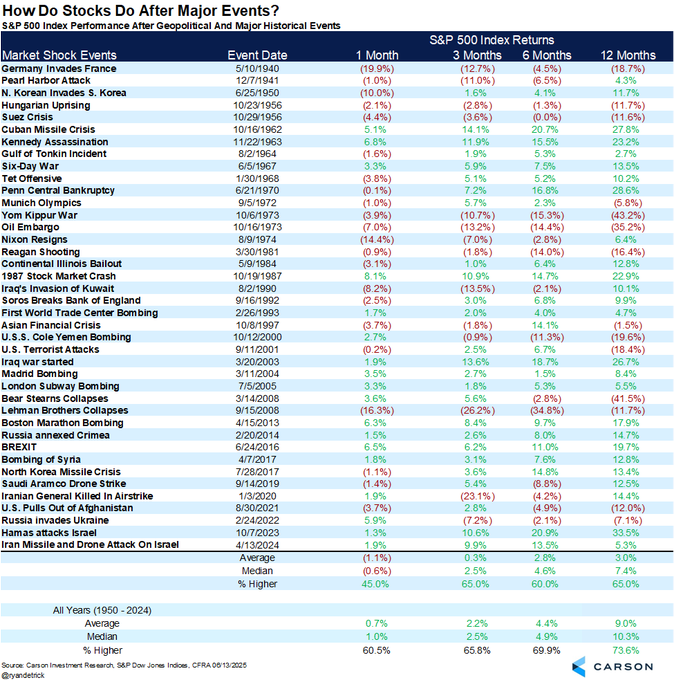

The retaliation has no teeth. The market won’t flinch, simply because there is no impact on earnings growth or inflation.

This was a carefully engineered geopolitical moment — and a campaign set-piece.

Trump can now claim:

He prevented a nuclear breakout

He acted decisively without boots on the ground

He picked up where Soleimani left off

He opened the door for Act II of the Abraham Accords

He even gave JD Vance a clear lane to run anti-war in 2028, while Rubio and Hegseth cement hawk credentials.

This is the most Trumpian maneuver yet — act hard, message harder, and leave the world guessing whether it was improvisation or orchestration.

It wasn’t a reaction.

It was a script.

And now, the headline writes itself:

Trump Ends It.

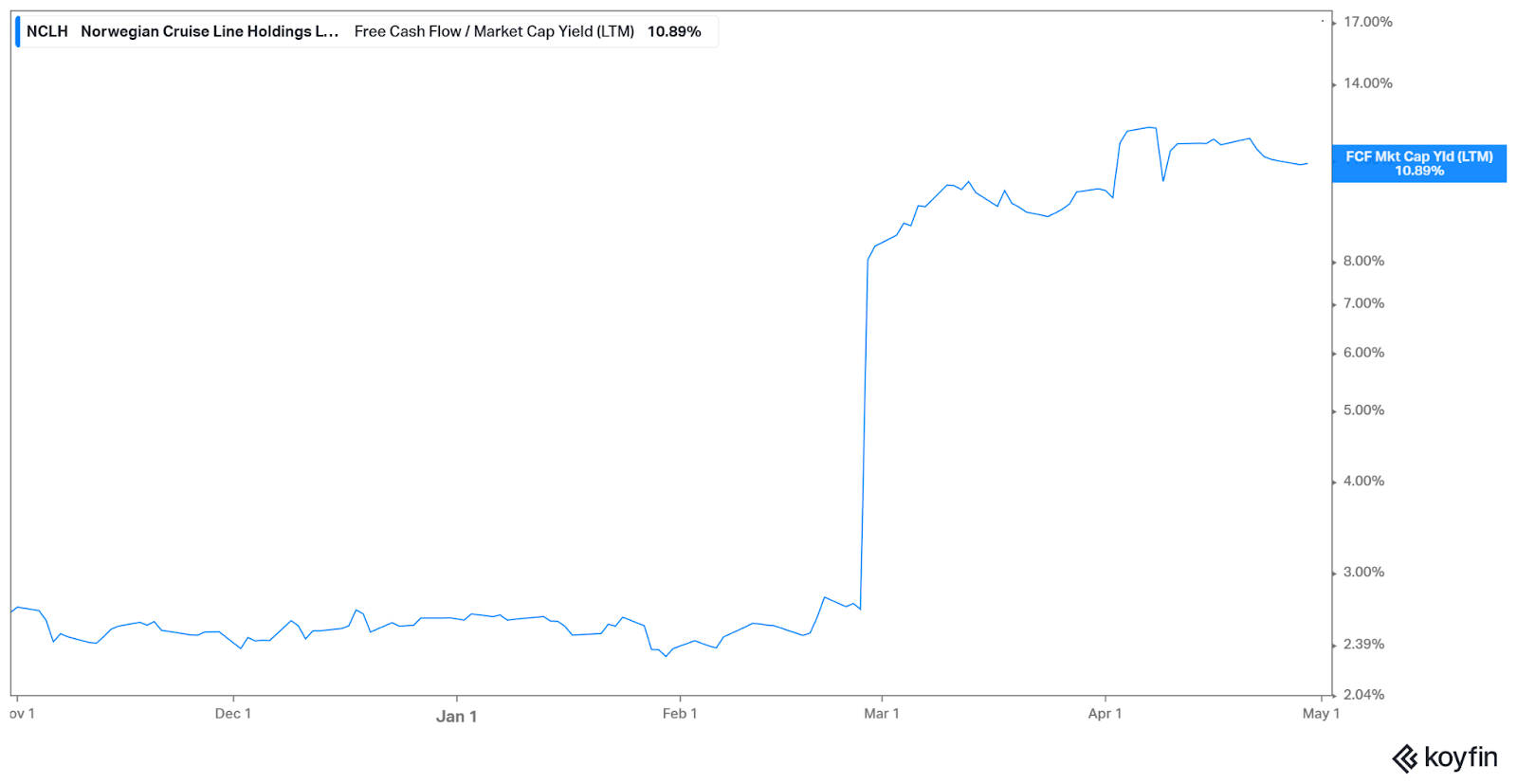

Norwegian Cruise Lines

There are a number of stocks where we see significant mispricings.

We wrote about NCLH a few weeks ago and continue to believe this is quite compelling. We’ll share other ideas in the coming weeks.

I will do a webinar walking through how we analyze NCLH in great detail.

It can take a lot of time to look at all the angles around a business.

The high-level story and metrics are as follows:

Boomers are spending on Travel & Leisure.

Cruise lines are showing strong revenue growth.

NCLH has lagged peers as others have shown higher revenue growth, and NCLH has been ‘caught in the middle’ with an offering that is neither high end (like Royal Carribean) or mass market (like Carnival).

Carnival engaged in loads of capex - acquiring new modern cruise ships and an island to expand their capacity and increase price points.

They have the highest leverage of their peer group.

Now, all that action is behind them and baked into the price.

What we see now is NCLH has higher revenue growth in the years ahead.

NCLH shows a whopping ROE of 95%.

The book value is compounding aggressively.

As book value compounds like a Gremlin eating donuts after midnight, it’s hard not see a world where NCLH’s stock price doesn’t compound.

The reason for the high ROE is high debt levels.

NCLH management has made the bet that its projects are NPV+ and that the return on those projects are higher than the cost of capital to finance the projects.

Key to this is understanding NCLH’s ability to meet its debt obligations.

About half of NCLH’s short-term debt are customer advances. Those are pre-payments.

NCLH is also paying off its debt each year. Capex is often a drag on a stock - but now that is behind them. The old shareholders paid that price, new shareholders get to benefit.

Additionally, the free cashflow to market cap yield - one of our favorite metrics - is near historical highs. If you compare this to comparable assets in the equity market and the ten-year yield it’s hard not to see how this doesn’t compound nicely.

When you ‘comp’ NCLH to its peer group, it trades at a cheaper valuation and yet has higher long-term earnings growth.

The other names benefitted from ‘momentum’ and NCLH’s capex projects.

What is management saying? How did they perform vs expectations? Here’s an excerpt from Lumida’s AI tool (www.lumidaai.com):

Management exceeded guidance on earnings and operational metrics.

Net Yield is below peer group - primarily due to the wrong product mix which the new capex funded cruise ships will address.

Basically, as NCLH increases the number of cruise lines in operations it grows it revenues and its margins.

The baby boomers continue to “stretch their legs” and get back to pre-Covid familial experiences.

The obvious risks are a major disruption to travel & leisure - such as Covid - when cruise lines and airlines were trading at low prices.

Or, an inability to finance longer-term debt due to a significant recession. Sustained higher interest rates above 5% would also hurt earnings as the company refinances its debt.

Prior to Covid, NCLH traded in the $50s. Today, Covid is in the high-teens and has established a pattern of higher lows.

Fed Dot Plot Drift

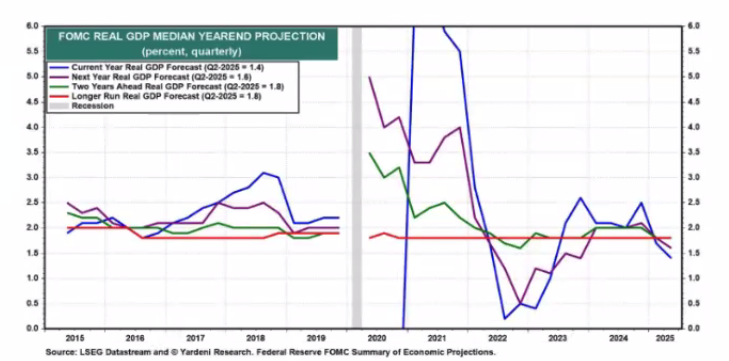

The FOMC in a widely anticipated statement did not lower short-term rates.

Notably, the Fed increased their expectations of both unemployment and inflation due to tariffs.

Real GDP for 2025 is now projected at just 1.4%. That’s down from 1.8% just last quarter.

We believe the Fed is wrong on the long-run trend rate of growth.

In 2022 there was no recession (in part due to massive immigration which acted as a form of stimulus).

2023 was strong. 2024 the US Consumer continued to defy expectations.

We certainly aren’t a fan of tariffs on allies…

but the income tax cuts to sub-$150K, strong earnings growth, and continued productivity growth are bullish. And Trump is hinting he will differentiate ICE policy to limit the negative impact to American farmers.

Housing starts fell nearly 10% month over month. But, 30-year mortgage rates ticked back to 6.84%

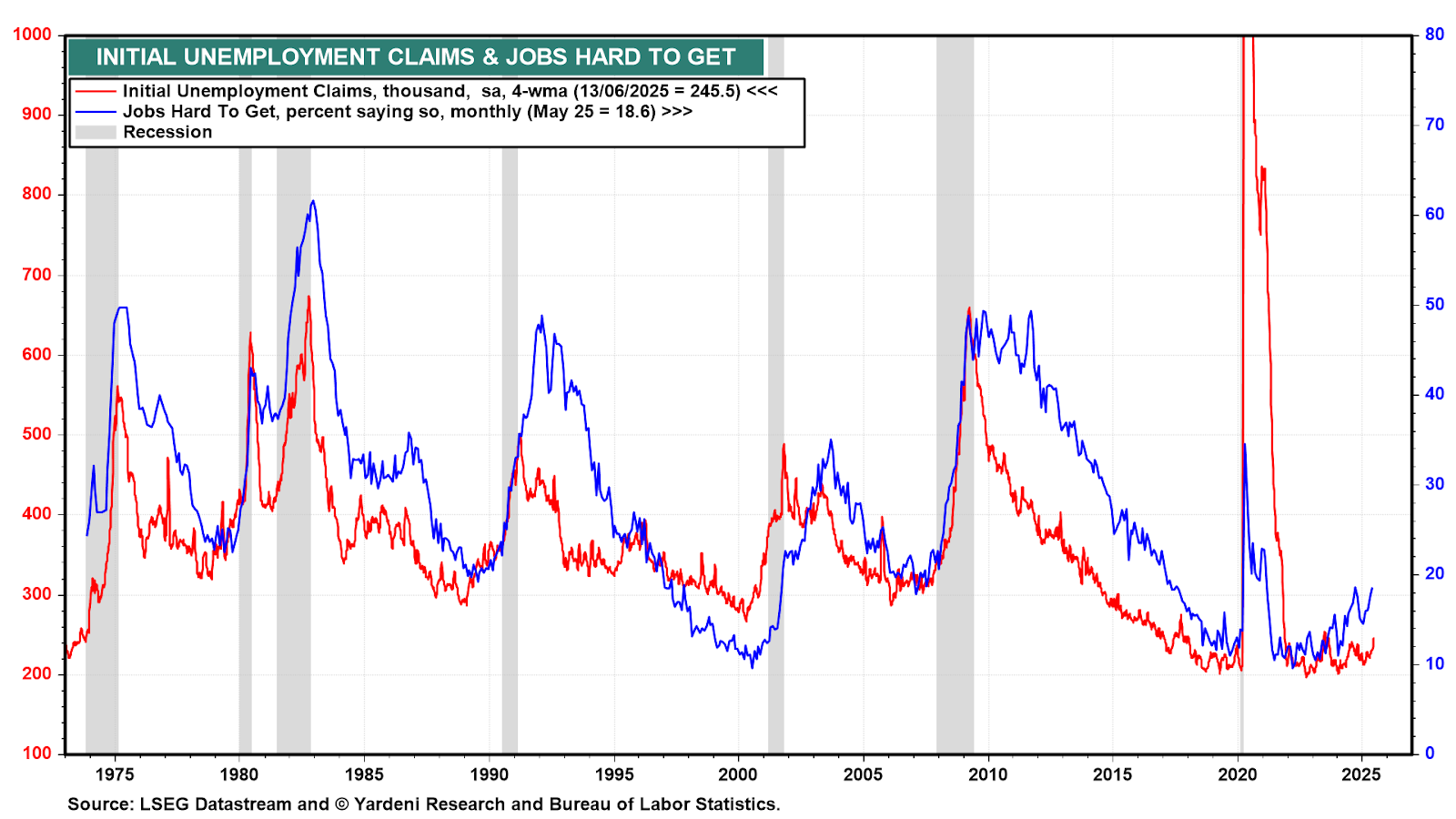

This past Thursday initial jobless claims came in at 245K.

So what you have is a classic policy trap: housing is soft, but jobs are holding the line

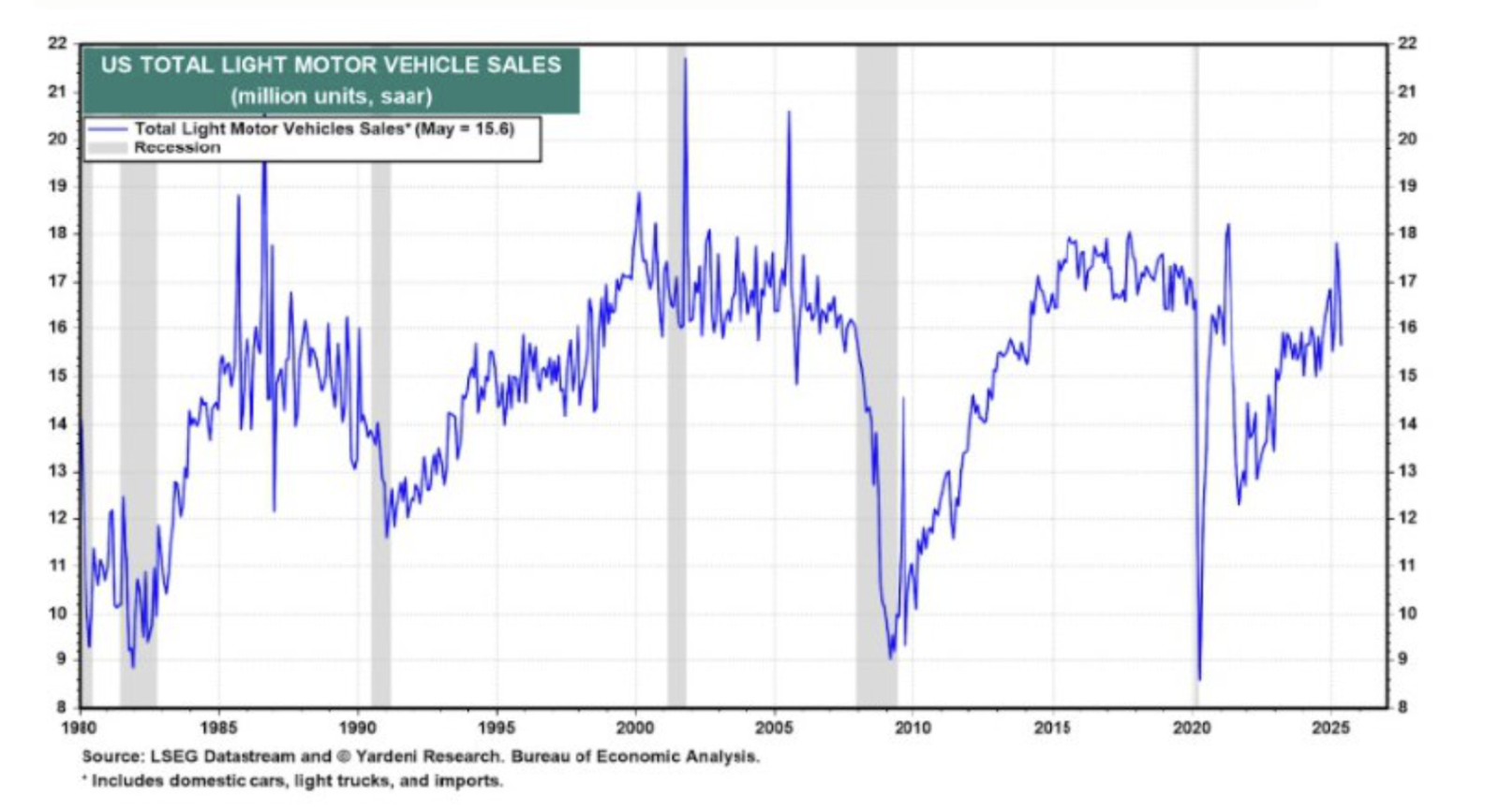

Consumers aren’t cracking — they are shifting their pattern of consumption. Take a look atu auto sales for example.

Consumers accelerated purchases to front-run imports, and now are pulling back on auto spend.

Credit card delinquencies are falling. Take a look at this Master Trust data which measures DQs from credit card receivables.

Payment rates are climbing.

Consumers are still spending — but they have shifted to value rather than conspicuous consumption.

We’re still in the same regime we’ve been in since 2022:

Boomers are spending.

Labor is stable.

Productivity is increasing.

Households are leaner and better capitalized.

Congress continues to spend like Drunken Sailors.

There can be short term technical volatility in markets from digesting this incoming whiff of inflation - but don’t mistake the squiggle for the broader trend.

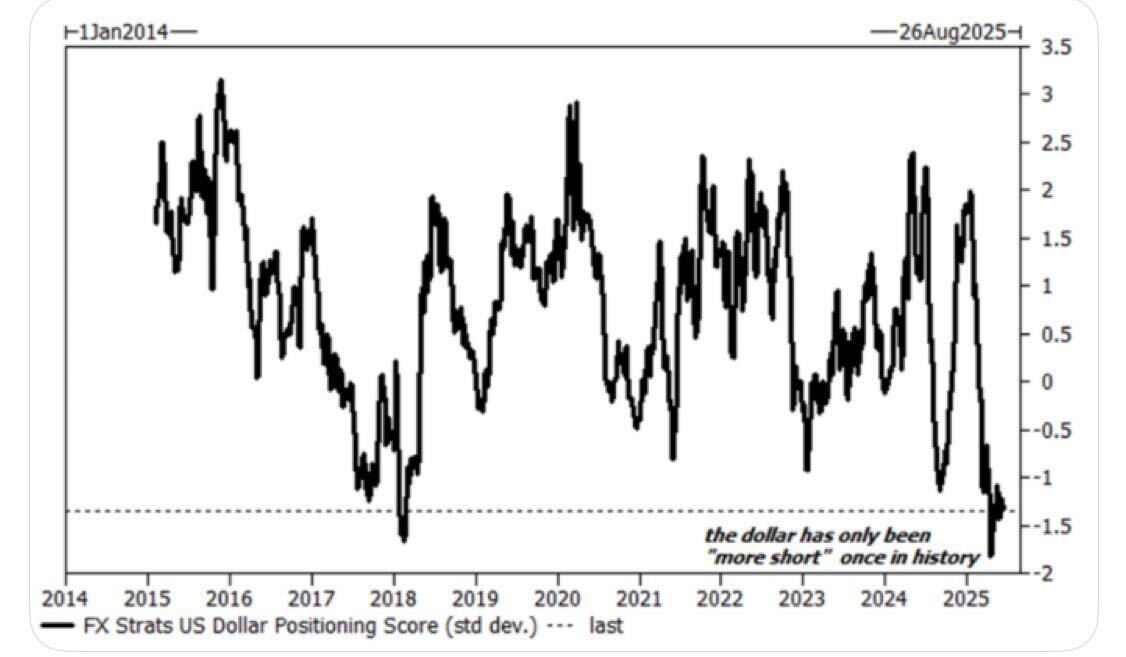

Historic Dollar Short

We’re now in one of the most extreme anti-dollar positions… ever.

The dollar has only been more short once before.

You don’t get many setups like this.

When positioning gets this lopsided, the next move tends to go in the opposite direction.

That suggests we could get a breather in the international small cap value theme which has trounced US equities markets to date.

Markets like Brazil (EWZ) and Mexico (EWW) have sold off somewhat in anticipation of this move.

Mexico

Brazil

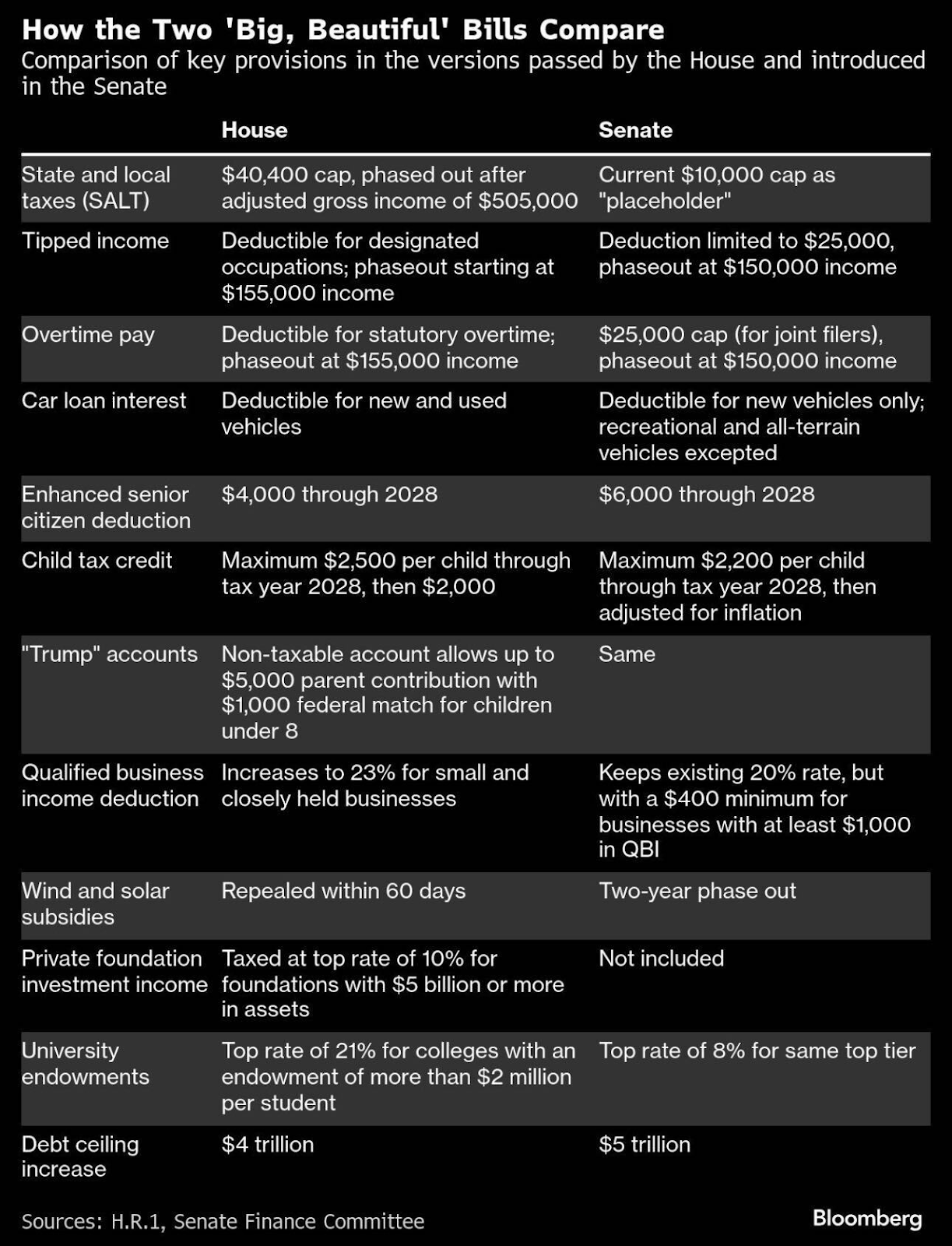

Tax Bill Showdown

Two big, beautiful bills — and the details matter.

House and Senate versions diverge on SALT caps, overtime pay, car loans, and child credits.

The Senate’s playing placeholder on deductions.

The House is throwing sharper elbows on wind, solar, and endowments.

This is less about one bill passing — and more about the tug-of-war shaping what survives reconciliation.

The takeaway?

This is a fiscal reflation moment in disguise. Both parties are spending — they’re just negotiating the flavor.

And keep an eye on that $5T debt ceiling hike — it tells you everything about where policy is headed.

Market

Stablecoin Dollar Leverage

Bessent on 6/19: “Stablecoins could reinforce dollar supremacy.”

Same thesis. Two weeks apart.

So — who benefits?

Which ecosystem is levered to stablecoin growth on-chain?

Where we stand today, it’s clear:

Ethereum.

HOOD vs X

Superapp Wars Are Just Beginning

Elon’s not wrong — turning X into a superapp is the right play.

We’ve seen the blueprint in China with WeChat.

Now he’s gunning for Robinhood, PayPal, and Square.

$HOOD should be paying attention.

AI

AI Defense Spending

Back in ’23, I said the top is near when AI capex becomes a real line item in U.S. defense spending.

OpenAI just signed a $200M deal with the DoD.

That’s a rounding error.

The Datacenter theme?

Still alive. Still running. Nothing shows us any signs of slowing, although TSMC shows demand acceleration due to hyperscalars seeking to avoid tariffs.

Meme of the Week

Stay tuned, stay informed, and as always, stay ahead.

Not subscribed yet? Don’t miss out on future insights—subscribe to the newsletter now!

For real-time updates, follow us on:

As Featured In