Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Macro: Inflation, Immigration & Rate Cuts

Markets: Mag 7, Gold miners & VIX

AI: AI Disillusionment

Digital Assets: Memecoins, Lumida Crypto Service

This week, we had a fascinating conversation with Dr. Adel Elmessiry.

Dr. Adel has a Ph.D. in AI/ML/Blockchain and is a serial entrepreneur with three successful exits.

We discussed non-consensus opportunities in the AI ecosystem, AGI & AI personhood, applications in blockchain and cybersecurity.

Tune in to watch the full episode.

Macro & Markets

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Let’s take stock of where we are.

We went into the New Year with the following observations:

One - tech is at record valuations for major indices.

Two - there is no recession, and the market has recognized that there is no recession.

We wrote last December a newsletter titled ‘There is no recession in sight’

The fundamental backdrop is strong:

It’s an election year

Wartime deficits, spend increases in defense, CHIPS ACT, IRA ACT

There is a surge in illegal immigration

We’re all for a rational policy and there are long-term costs. But these are bullish.

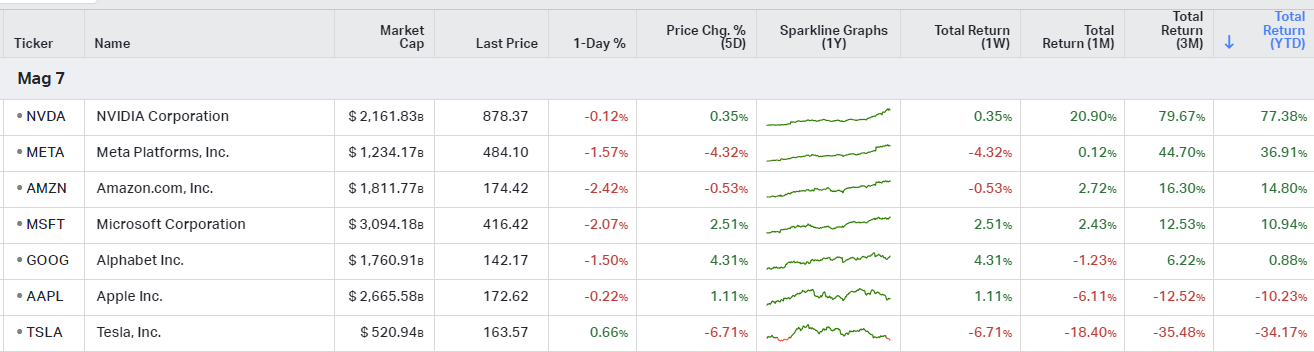

Since our January over-valuation point, we’ve seen a stealth bear market that has taken down the valuations of major leaders in the S&P.

Apple is in a bear market. Tesla is in a bear market.

Our Mag 7 positioning to overweight Nvidia, Meta, and Google - and avoid (or short) Apple and Tesla has worked out very well.

We’ve also seen hype exit the EV space. We had a newsletter focused on the disinflaton of the EV bubble due to increased competition. That’s underway.

The point is - a good chunk of the excess we saw in last July and in January has been worked out.

Mr. Market is exercising greater discipline. Not everything is up and to the right.

What Mr. Market is bidding up are the prices and valuations of the very best businesses in the world.

The heightened valuations are causing new capital to flow into quality small caps with earnings growth. Biotech is also benefitting from a nice rally this year.

Another sector that is benefitting - midcaps.

Midcap Growth stocks are out-performing technology and other sectors that comprise the S&P 500.

It makes sense.

Midcaps are less sensitive to inflation and interest rate gyrations because, unlike small caps, they can access public markets, and there are many quality midcap businesses.

Also, unlike mega tech, they have better valuations; they’ve been overlooked. It’s easier to put more money to work here.

Midcaps include names like Hershey’s, Dick’s Sporting Goods, Toll Brothers and others.

There’s been a stealth rally in mid-quality, small caps, and biotech at the same time as a stealth bear market in other hype categories.

We expect that rotation to continue.

On Inflation

The inflation print came in hot once again, as it has for quite a few of the last CPI prints.

Mr. Market really doesn’t like FOMC meeting and CPI prints, have a look:

Our long-standing view is that inflation remains higher for longer.

It’s going to take time to get from the 3% range to 2% when you have an economy running on all cylinders.

Consequently, we expect the Federal Reserve to hold rates higher for longer.

Recall at the end of December, Lumida made a non-consensus call predicting that the Fed would not raise rates in March back then.

The odds of a rate cut were around 80% and we looked out on a limb. Now the market has come around to our view. We’ll see what happens this Wednesday.

At this point, we do not expect any rate cut in May either.

The probability of a rate cut in June is diminishing. Like the Fed, we want to look at the data each month and re-assess.

It’s hard to imagine a need for rate cuts when the economy is strong.

On Immigration

One of the confounding variables in all of this has been the surge in illegal immigration.

We have yet to see a clear study on what sectors benefit and are hurt by illegal immigration.

On the one hand, a surge in illegal immigrants relieves pressures in the labor market.

We have discussed how immigration is improving the outlook for several businesses ranging from DoorDash to Instacart. It also helps businesses.

There are costs - especially to cities like New York that are paying hundreds of dollars a day to house migrants. And there are costs from the lack of an assimilation framework. And other risks as well (e.g., fentanyl, human trafficking concerns, etc.)

It’s complicated. But, overall, the surge in labor relieves the labor shortage.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Productivity Rate

The productivity rate is increasing faster than we’ve seen since the late 1990s.

This is a very big story, and no one is really talking about it.

Is that productivity boom driven by AI?

No, it’s too soon for that. AI can’t even process my email.

Productivity is defined as the output you can get for a fixed set of inputs. Simply put, we are getting more output for less inputs.

We believe the surging illegal immigration is improving productivity.

It’s easier now for small businesses to fill roles for staff; anecdotally.

Here’s a quote from a restaurant owner for the first time in four years: “I have no positions to fill. We have staffing for the bus boy, the waiters, and the kitchen filled.”

GDP can be expressed as the product of labor and labor income.

If you have 5 MM migrants earning $25 to $50 K per year, that’s hundreds of billions in stimulus.

Big picture - The constellation of factors means it’s difficult to envision economic weakness.

Market Sentiment

Market enthusiasm is starting to soften. That’s healthy.

This past week we saw a few days of softness around the inflation report.

The risk factors to market internals are:

The 10-year is breaking above the 4.3% level. We haven’t seen that in a long time

The US Dollar is also threatening to gain strength

Should both of these break out that would indicate a transition to a risk-off environment.

We also see tremendous call option buying activity (call skew is near records). Quarterly expirations for options contracts took place this Friday.

Options cause market makers to delta hedge which adds a type of support for markets. The expiry of those options could cause more volatility.

Our read of the situation is that Mr. Market is waiting to hear from the FOMC this next Wednesday.

If the FOMC does a copy paste of the last update to Congress, then we’re OK. If the FOMC says the recent inflation print is too hot, then markets could very well correct.

If that happens, we don’t expect anything more than a 3 to 10%. It’s a buy the dip. The fundamental backdrop is strong.

Buy the Dips

We wrote a piece a few weeks ago, making the case for a correction; so far, we have not seen that expression of that thesis.

Fortunately, it has been through names like Apple and Tesla that have experienced double digit declines in value. We are maintaining a net 85% long posture.

April is a historically bullish month; it’s the most bullish month of the year. If there is weakness, we should see it now on the heels of the FOMC meeting.

However, should that take place, we would caution against turning bearish. Take advantage of that opportunity to buy the very best names that go on sale - including names that map to our long-term secular trends within the semiconductor, biotech, small and mid-caps, and longevity.

Don’t buy Microsoft. Great business, too expensive (consensus).

Recall at the beginning of the year, we ran market studies on two periods that also exhibited a pattern of overbought market conditions that exhibited a very long duration: 1986 and 2017

Both of these regimes exhibited shallow drawdowns. That pattern is playing out.

The wall of money that missed the rally and is hiding in T-Bills wants to get back into the market.

Dips should be bought.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Risks to the Market

The major risks to markets are the following:

Inflation becomes sticky and entrenched, forcing the Fed to raise rates

No one expects that, and we don’t expect that, but it’s worth acknowledging the factor.

AI stocks failed to deliver revenue or earning growth from the AI hype

We have already seen that in the case of Apple and its Vision Pro.

If you’ve been following it for a long time, you know that we were the first to call out Apple last summer in this newsletter and compare it to Taiwan semiconductor.

PE has gone from 32 to 26 times for earnings, and Taiwan semiconductor has gone from 15 times to 22 times forward earnings over that timeframe.

If Microsoft fails to generate traction with copilot in its earnings, a release that could cause a tech correction. We’ll find out as we get closer to next earnings season.

We are skeptical about Microsoft’s success with Co-Pilot. We’d rather own other names than priced for perfection securities.

Good security selection will help you avoid these risks and focus on opportunities.

Microsoft has lagged Meta and Nvidia considerably.

If you are positioned correctly, you should be OK.

Avoid absurd valuations, and meme stocks that people talk about on Twitter, like Palantir or Snowflake, or Sofi.

Our best read of the situation is that we are experiencing leadership rotation.

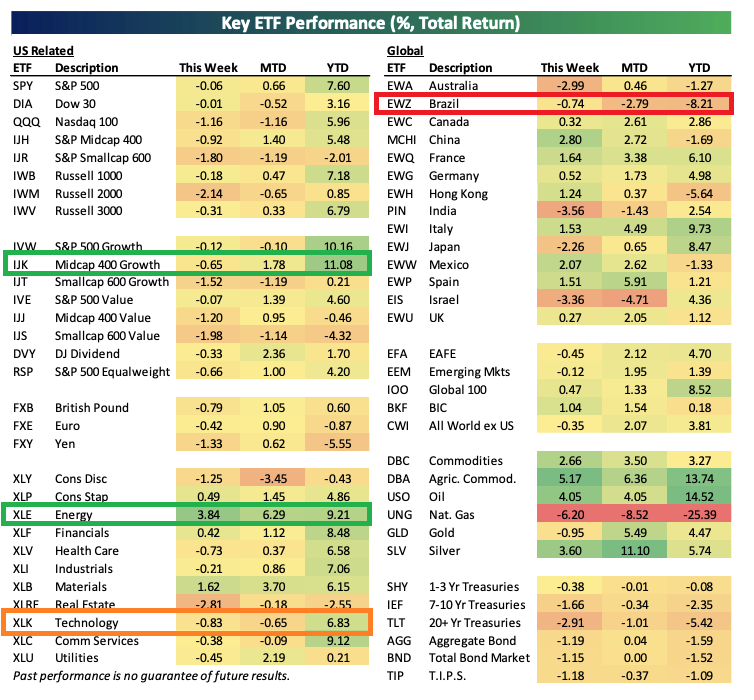

These movements make sense. The global economy, including China, is improving. Oil prices are going up, and that’s benefiting energy firms.

We continue to like energy and overweight energy versus the S&P. Energy remains negatively correlated to technology stocks. We have an 8% weight on energy vs 3% for the S&P 500.

Energy stocks are the new bonds. They throw off cash flow; they are growing earnings, and they have the cheapest valuations across the equity sector.

Elective Health

Perhaps the most interesting thing we are excited about today is elective health, which is part of our aging and longevity theme. People are spending money on health because the oldest of the oldest, the boomers and high earners, want to improve the quality of their life

We have found about 15 companies. They are indexed to trends within elective health that we like.

These companies have attractive revenue, earning growth, and valuations.

So Mr. Market is expensive.

Overall, Mr. Market, like a heat-seeking missile, is discovering and finding those pockets of opportunity.

On Google

Google is showing early signs of becoming a share cannibal.

Share count is decreasing each quarter, and cashflow is increasing.

18 months from now, we’d expect Google to be up 30 to 50%.

We bought last Tuesday (great timing), and it’s now about 10 to 12% of our equity portfolio.

Google is one of the few areas in the market where there is a bargain.

Buy low, sell high. Pretty simple folks.

Build a Bear Shout-Out

One of Lumida’s stocking stuffer picks Build a Bear shot up ~20% on earnings.

The stock has an ~8 PE ratio, throws off cashflow, and is buying back their stock.

No one is talking about it. We like that setup.

You need value stocks in your portfolio as well - multiple expansion is the primary driver of stock price returns (followed by earnings growth).

Take a look at that candle…

We continue to outperform the S&P and QQQ with less market risk and none of the concentration you see at a hedge fund.

We have about 30 to 50 positions.

To perform at that level automatically implies good stock picking skills and thematic selection. That’s what we do in our public equities strategy.

Apple Fans are starting to return their vision pros.

Ouch.

The best calls we've made get the most pushback on X: Apple, Tesla, SoFi, and fading FOMC March Cuts.

The best winners have been names everyone feared to own or ignore: ETHE, Dave, SLQT, Meta...and now Google.

The ones that are more consensus have done fine (e.g., Cloudflare, Haliburton, etc.) -- but not outsized returns.

The best opportunities are Non-Consensus & Right.

Is Apple a Growth Stock?

No. Earnings grew < 1% last quarter.

Is Apple a Value Stock?

No. The PE is 26.

That’s the crux of the issue.

So, what is Apple?

It’s a Quality Consumer Staple.

Apple is oversold now.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

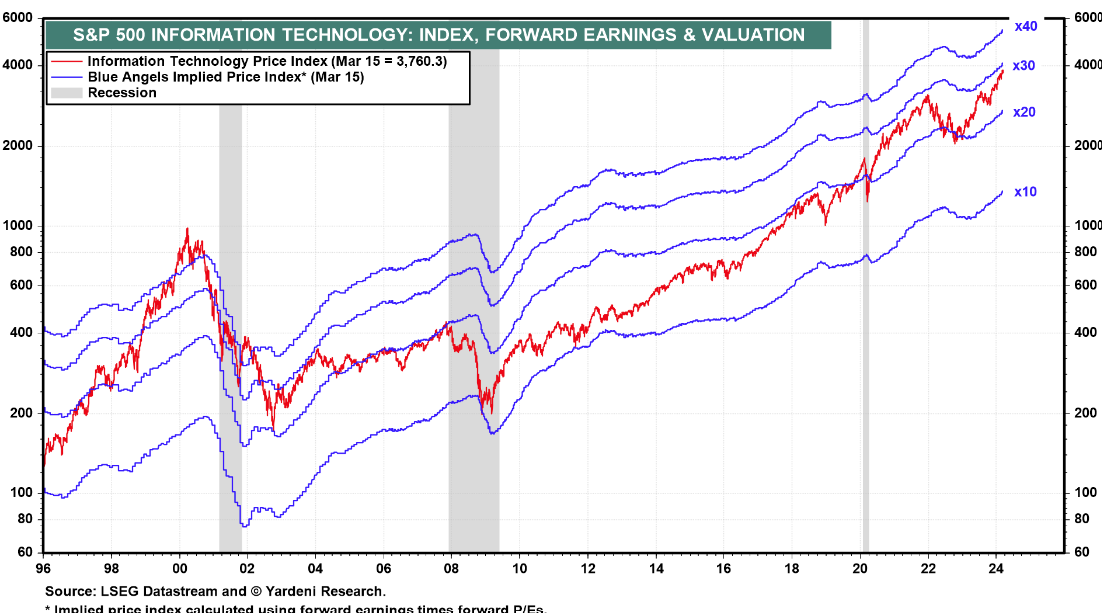

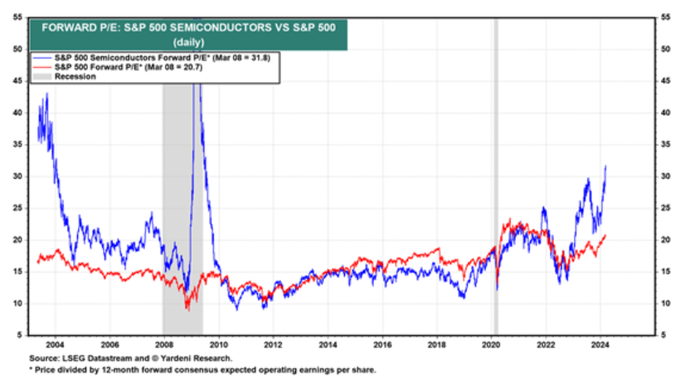

On Semiconductors

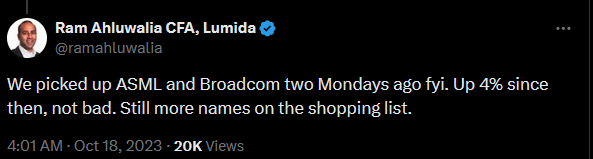

In the last few weeks, we reduced exposure to AI/Semiconductors from 'Overweight' to 'Market Weight.'

We went Overweight in October when they were on sale (receipts).

And names like Broadcom and ASML have gone up 50% +/-. (Nvidia is a different story...much more.)

Look at the Forward PE of Semis vs. the S&P 500 on this chart.

'You make your money on the buy.'

I'm seeing better value in nuclear energy these days—and good old-fashioned value stocks, and small-cap stocks.

Small caps will benefit from lower rates, a stronger economy, and a broader labor pool.

They will also benefit from other investors, like me, who are looking around for value.

BUT I don't want to be underweight semis.

I do believe this is a powerful secular trend that you want to continue to have exposure to.

Note: The CPI hits on Tuesday.

There's usually a 65% chance of rain on those days.

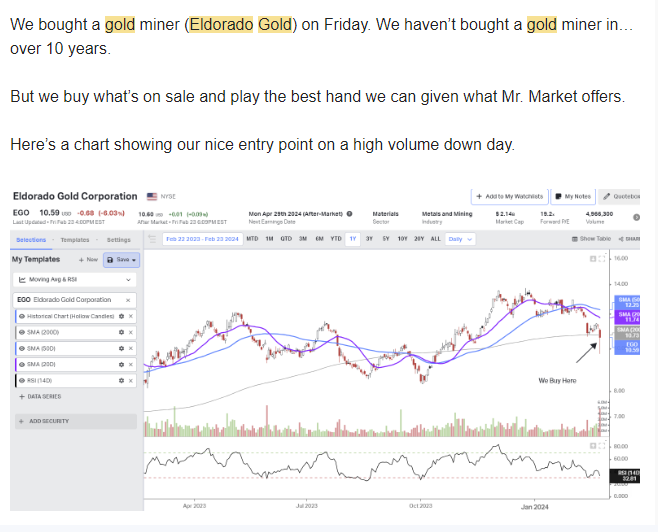

El Dorado Gold ($EGO):

We bought a gold miner a few weeks ago and wrote about it in the Feb 25th @LumidaWealth newsletter.

The darn thing ran up ~20% since then.

It's no longer cheap.

So, we sold it.

The excerpt from our call is below, and you can see the price today.

We don't have a thematic view on Gold Miners, so there is no reason to hold it longer term.

This was the only item on sale from Mr. Market, and now it's expensive.

This started as an investment based on good fundamentals.

But, it happened to become a 'rental', only because the price moved up quickly.

If the price had not run up, we would still be owning it.

We also see some better opportunities where we have thematic views.

Discipline means we sell El Dorado Gold.

We need a new Vix

The current Vix is weighted towards big market cap names where the implied volatility rarely spikes.

Even now, the implied volatility for Apple remains cheap near the lows despite a significant re-rating

On the other hand, if you look at smaller-cap securities of bad stocks like SoFi, you can see that the implied volatility is high.

Risk aversion does spike during sell-offs, but you can’t see it in the Vix.

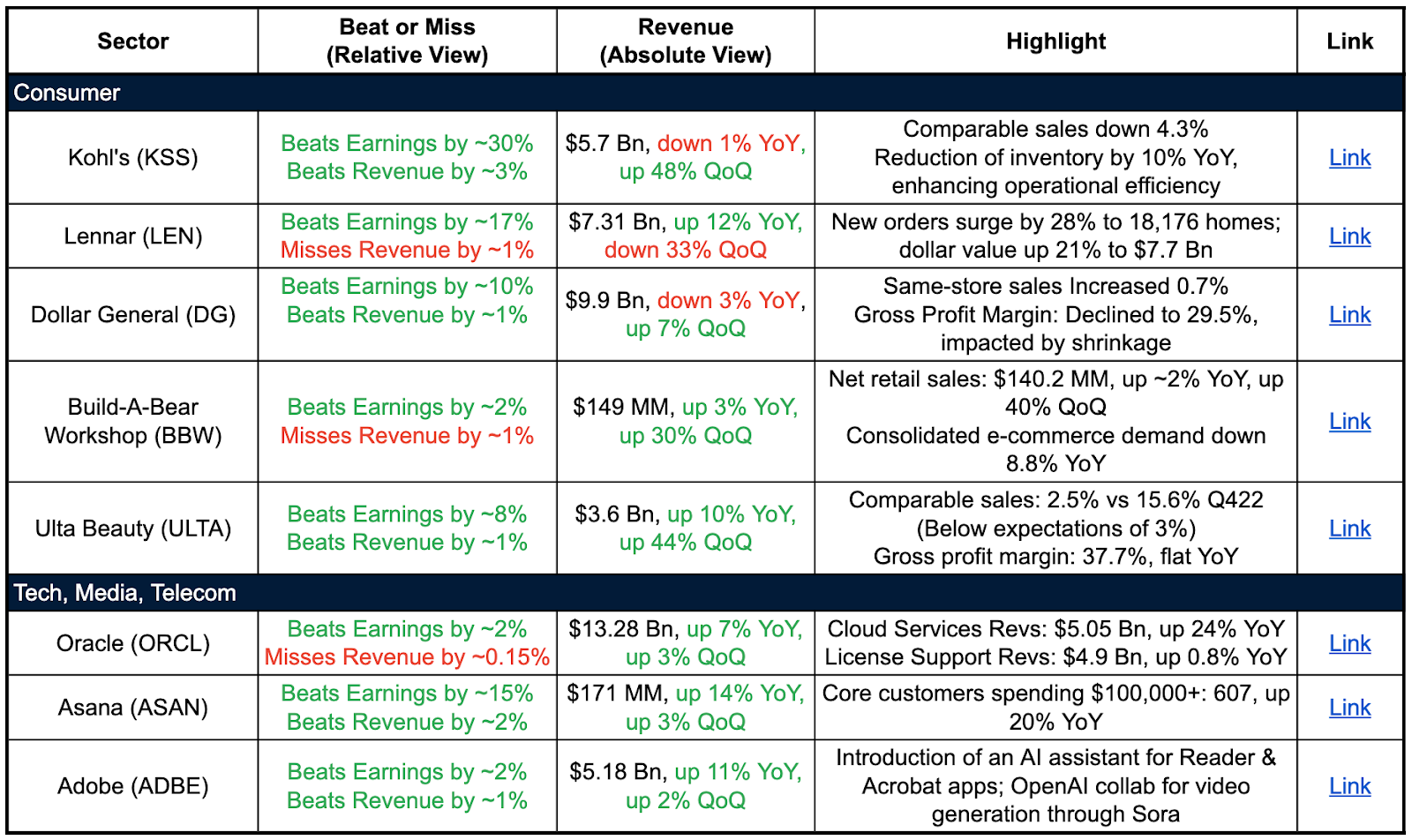

Company Earnings

Overall, a challenging consumer spending backdrop for legacy retailers.

Enterprise software/cloud shift remains a key growth driver for tech companies that can capitalize on AI opportunities.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Consumer:

Legacy Brands in Decline vs. New Brands

Department stores like Kohl's seeing continued sales pressure with declines in comparable sales, though inventory management is helping profitability.

Discount retailers like Dollar General facing headwinds from lower consumer spending and margin compression due to higher shrinkage.

Beauty retailers like Ulta missing expectations on comparable sales growth, though top-line growth remains healthy, aided by new store openings.

Dicks Sporting Goods delivered strong earnings

Homebuilders like Lennar are benefitting from a surge in new orders, though revenues are impacted by lower average selling prices.

TMT:

Adobe’s stock is in a funk. Adobe we believe will face disruption risk from AI.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

AI

On (Short-Term) AI Disillusionment

I used to think the killer product market fit use-case for GPT4 was coding.

That’s not the case either.

‘We can’t really say this in public since everyone … will swear by GPT’s magical coding abilities’

On Crypto

In the crypto market, we’ve seen the beginnings of what might be a mild correction.

This is on the heels of MicroStrategy issuing two back-to-back convertible debts. The last time MSTR issued convertible debt in 2021, there was also a correction.

MSTR is taking advantage of the premium to Nav in their stock. They will issue stock, and buy more bitcoin.

We also see Meme activity on Solana exploring. We counted 2,500 memecoins generated in a single hour. It feels like DeFi summer.

Our read is - this is still a bull market. However, we are likely farther in the cycle than most think.

The crucial indicator is Bitcoin ETF inflows. The ETFs now own 1 to 2% of outstanding Bitcoin. That’s incredible. We don’t expect the bid to stop anytime soon.

Crypto has not had a correction - if it happens, it will lengthen the bull market.

Crypto Memecoin

I bought my first Solana meme coin for my personal account. It had a $7 MM market cap. Either it goes to zero, or it goes up 50x.

You learn by doing and tinkering, and that’s what we are doing.

The token is ‘CFA TradFi Bro.’. The token is down 50% in the last 24 hours, and up 30% in the last 6 hours. Welcome to crypto.

Here’s the public address:

F1n2Tn7Eb9jTbSQiqy2Z7G4VTbkreHGQqcRKKmwZv726‘Yeah but Apple has a great business model.

And SoFi is run by a ex-GS banker’

And crypto has no use case.’

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Crypto is both the easiest and hardest asset class at the same time.

Why Easy:

- The vast majority of projects are BS or have no traction; ‘security selection’ is not that hard

- It’s cyclical. You can see the cycle a dozen different ways.

- You can measure flows, leverage, and liquidations

Why Hard:

- Getting in early is psychologically difficult and you look weird doing it.

- Getting out requires tempering FOMO and greed.

- Large drawdowns must be tolerated (except this cycle?).

If you want Crypto top signals look for these:

Coinbase app ranking (it’s going up again)

Are new listings on coinbase tanking (not yet)

Mvrv chart - still has more to run

Whale behavior - not yet dumping

etf flows - still strong

Sentiment - got hot quickly

Solana has achieved a product-market fit for Memecoins. The token demonstrates relative strength, and we expect it will have more room to run.

Shout out to our investor Mike Dudas and Kyle Samani whom we interviewed in September -for making the correct non-Consensus call to buy Solana.

If you want to learn more about Lumida’s soon-to-be-announced crypto white glove service - click here

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Quote of the Week

“Far more money has been lost by investors trying to anticipate corrections, than lost in the corrections themselves.” - Peter Lynch

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.