Here’s a preview of what we’ll cover this week:

Macro: Scott Bessent on Bloomberg Surveillance, Point72’s Cohen Gets Bearish

Market: Share-Based Compensation, Markets Misprice Risk

AI: GROK vs OpenAI

Lumida in Spotlight

Ever wondered where the biggest hedge funds are deploying capital?

We break it down for you in the latest episode of the Lumida 13F Podcast.

In this episode:

- Hedge Fund Positioning – A deep dive into Q4 2024 13F filings.

- Who’s Buying, Who’s Selling? – Insights on Bridgewater, Coatue, Altimeter & more.

- Market Signals – What these trades reveal about future trends.

Watch it on YouTube: Hedge Fund Positioning: 13F Review

Prefer audio? Listen here: Spotify | Apple Podcasts

Download Tracker – Whale Watch: 13F Q4 '24 Full Report

First Things First

What a Week!

I feel like we should rename the newsletter to ‘What a Week’.

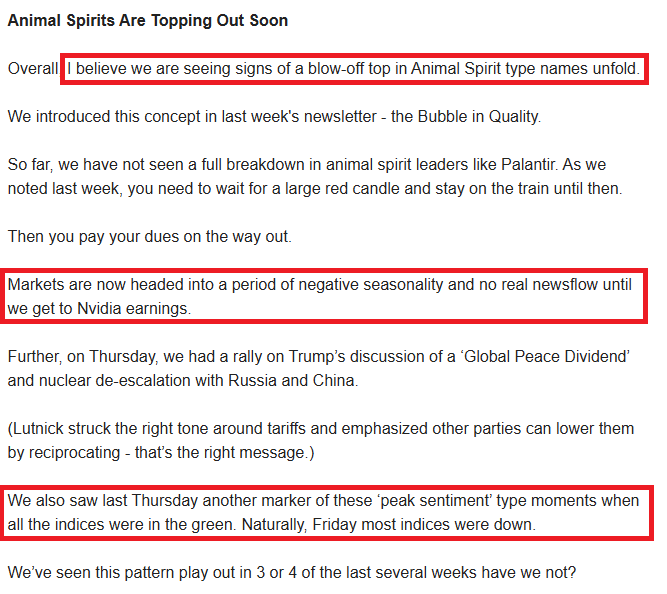

The last two weeks we shared our thesis there are twin bubbles - a bubble in quality and its twin opposite - a bubble in Animal Spirits.

We also noted in a section titled ‘Animal Spirits Are Topping Soon’ that Animal Spirits Are Topping Soon.

Both of these bubbles burst this past week.

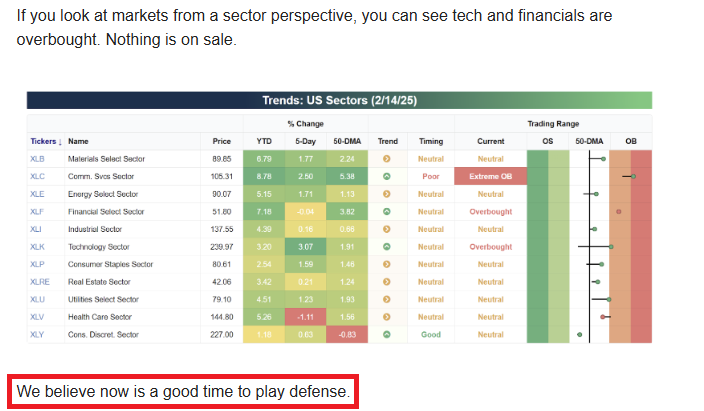

We also noted ‘Now is the time to play Defense’

Hopes of a global peace dividend came unwound as Trump and Zelensky had a very visible public dispute, and Russia appears poised to declare a ‘Victory’ on its third year anniversary of invading Ukraine.

The Munich Summit also poured cold water on the vibes.

However, it’s worth noting that markets were especially vulnerable. If it wasn’t that news, it would have been something else.

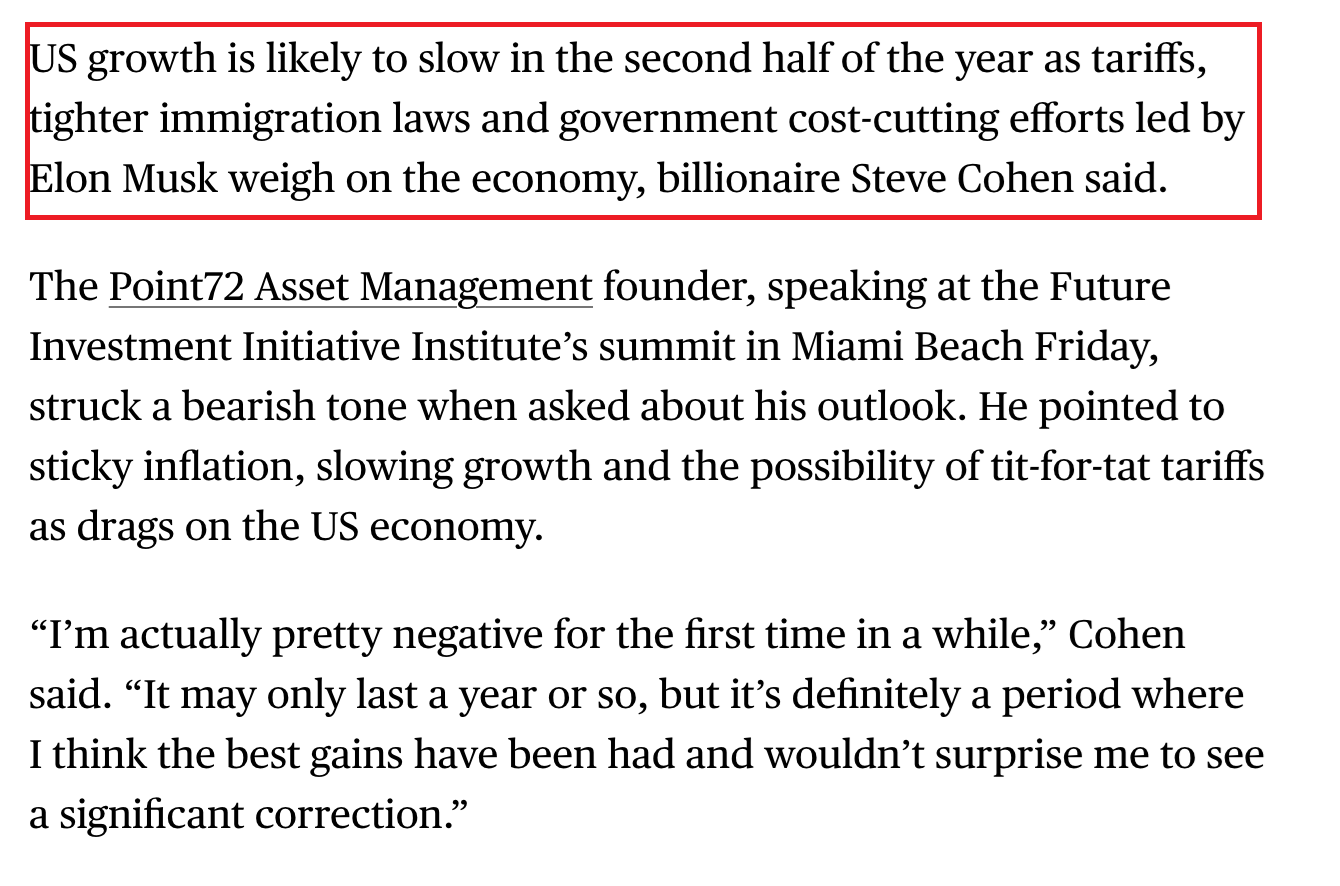

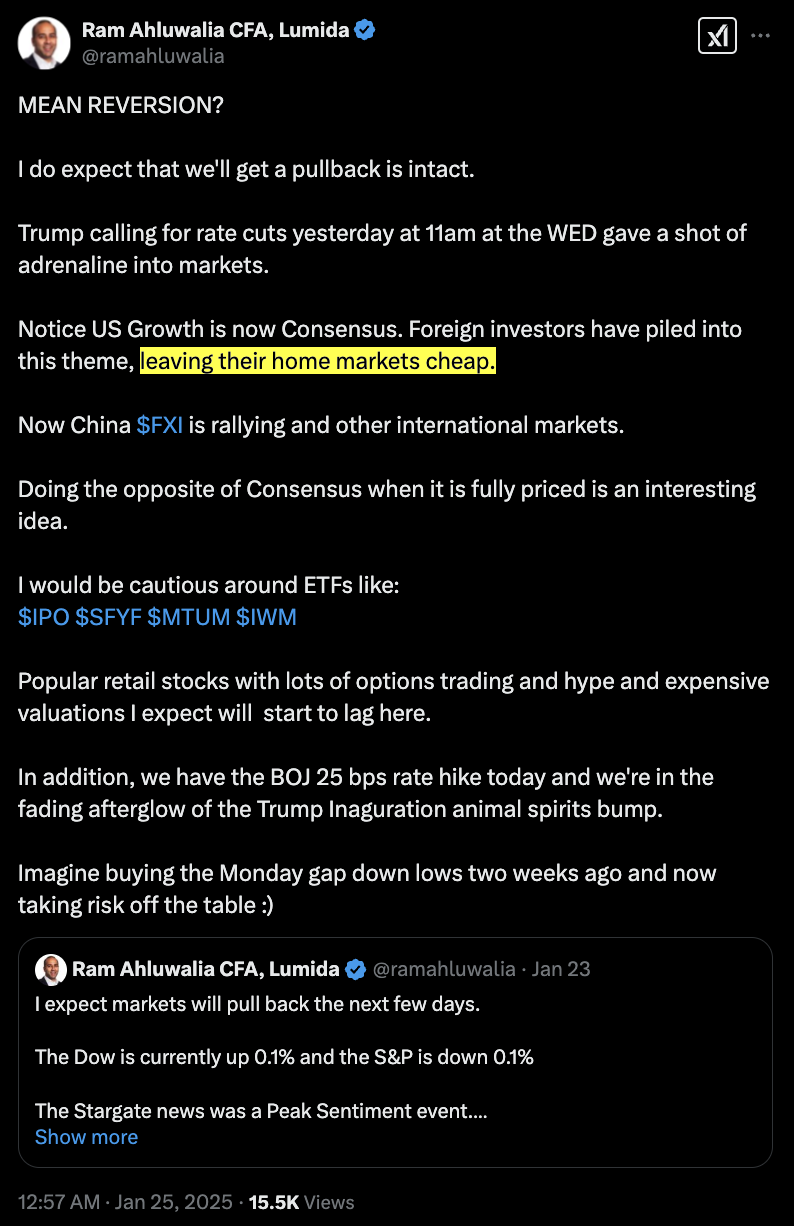

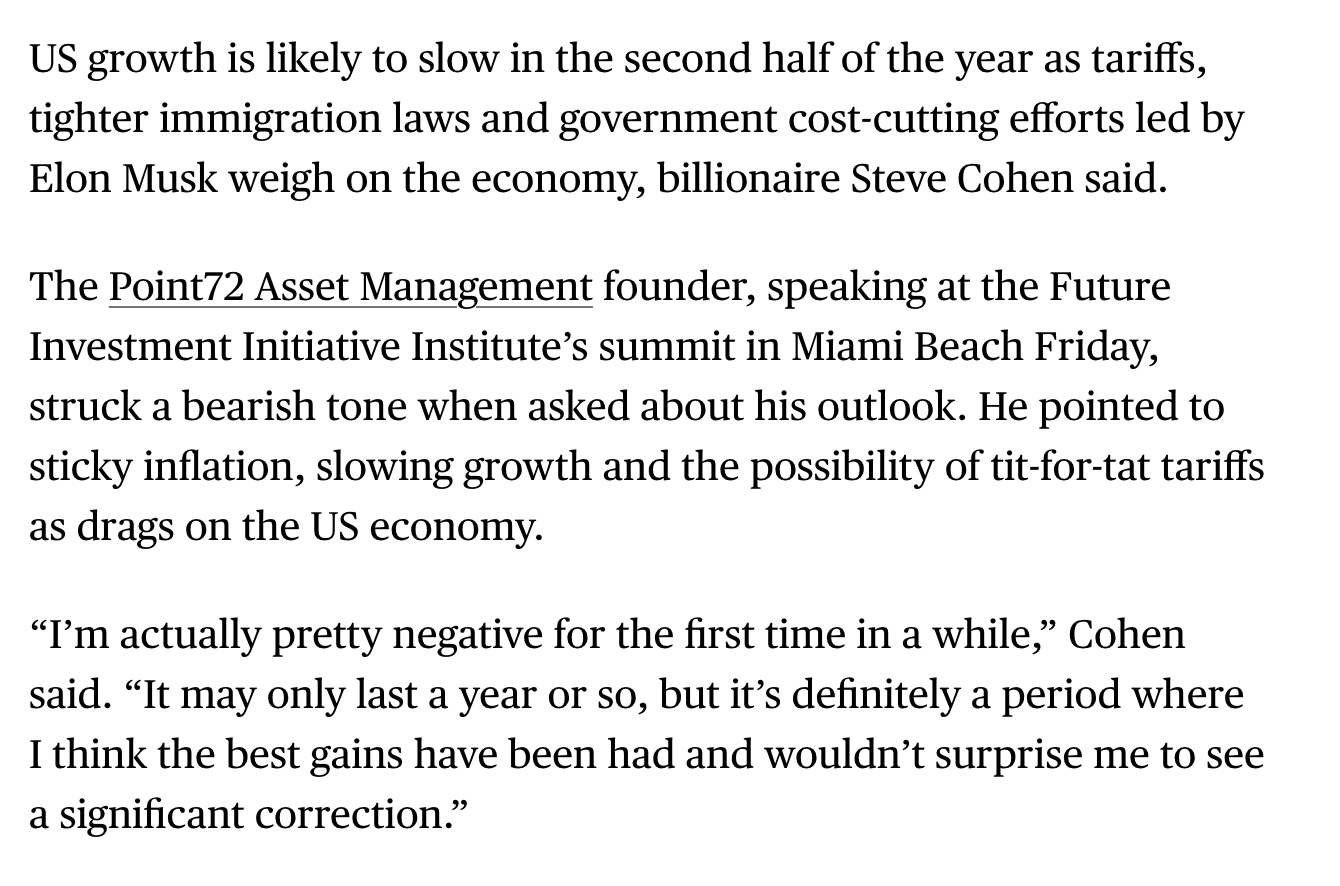

Point 72’s founder, Steve Cohen, had this to say on Friday which certainly accelerated the decline.

We don’t share Cohen’s view here. We believe animal spirits in the real economy combined with an extension of tax cuts (and the difficulty in cutting spending) mean that the economy will do just fine.

However, the disagreement is not relevant.

What matters is risk aversion is increasing - the pendulum is swinging to Steve Cohen’s view and it is now getting priced in.

Bubbles Bursting

Let’s review some of the bubbles that burst.

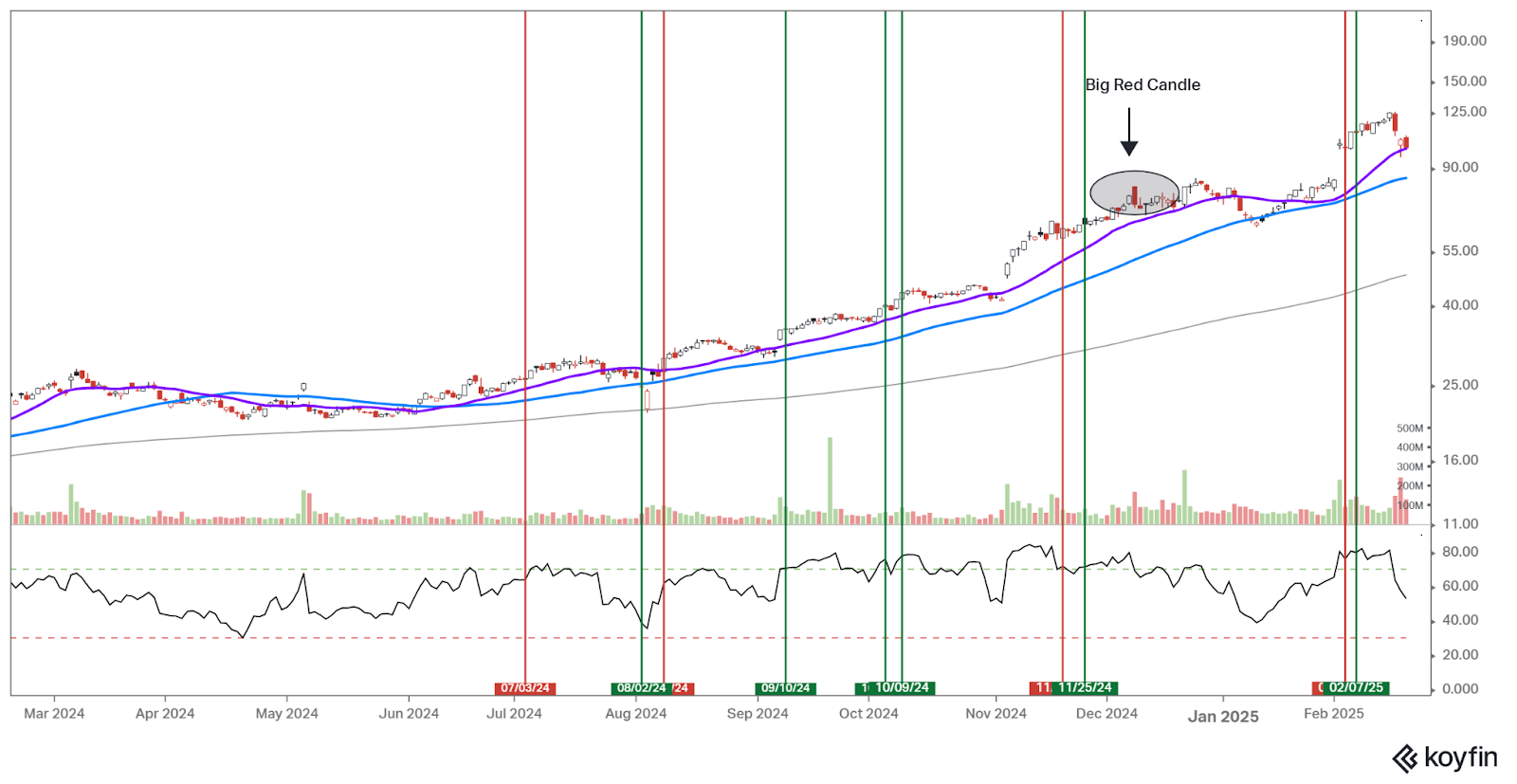

Axon burst. It’s now “only” worth 87x PE. (We had a small short position in this name which was nice.)

Palantir gave us the Big Red Candle

CrowdStrike is now worth only 100x PE

MongoDB is worth 88x Forward Earnings

We also saw breakdowns in other Quality names such as Walmart.

(Note: Walmart has a chance to bounce here even though it has a forward PE of 35x now and is pricier than Microsoft and Nvidia and is exposed to tariffs on China. Importers pay tariffs - even if you call it the External Revenue Service.)

In a prior newsletter, we showed a list of stocks with a higher Forward PE ratio than Nvidia. Take a look at the worst offenders on that list:

We owned App Lovin and took our lumps here. Recall this stock shot up 30% after earnings. The difficult part - taxes. If you wait for long-term capital gains (and re-assess at that point), you can save 30% of your gains.

If you pull the trigger and sell, you leave a lot of money on the table. All of that changes with an ETF where you can do an ‘in kind’ transaction, like a 1031 Exchange in Real Estate, and not pay taxes at all.

Very few active managers in ETFs seem to take advantage of this. It shows you how backwards modern investing is.

(This is another reason why we are assessing demand for a Lumida ETF at www.lumidaetf.com. An ETF can do an ‘in-kind’ transaction and not incur capital gains tax, very similar to how real estate investors can do a 1031 exchange and avoid capital gains.)

Incidentally, our team specializes in a range of strategies to mitigate capital gains, income, and passive income taxes.

Be sure to reach out to our Senior Advisor [email protected] for more.

Markets: Where Do We Go From Here?

The good news is a decent amount of excess was wrung out of markets.

We saw, finally, a spike in fear with the VIX fear gauge moving up 18%.

But, a stronger resolution would be a Monday gap down open. Then a VIX spike above 20.

However, these bubbles that have burst are not coming back. It is quite common to have a reflex rally or a partial recovery.

But these recoveries should be sold.

Software stocks are a good example of this pattern. Take a look at IGV, the Software ETF. (We were and remain short this ETF into the tail end of the week.)

Visit our website to learn about our ETF or talk to our team about wealth management strategies tailored for this market cycle.

That partial recovery after the breakdown is the phenomenon we are discussing.

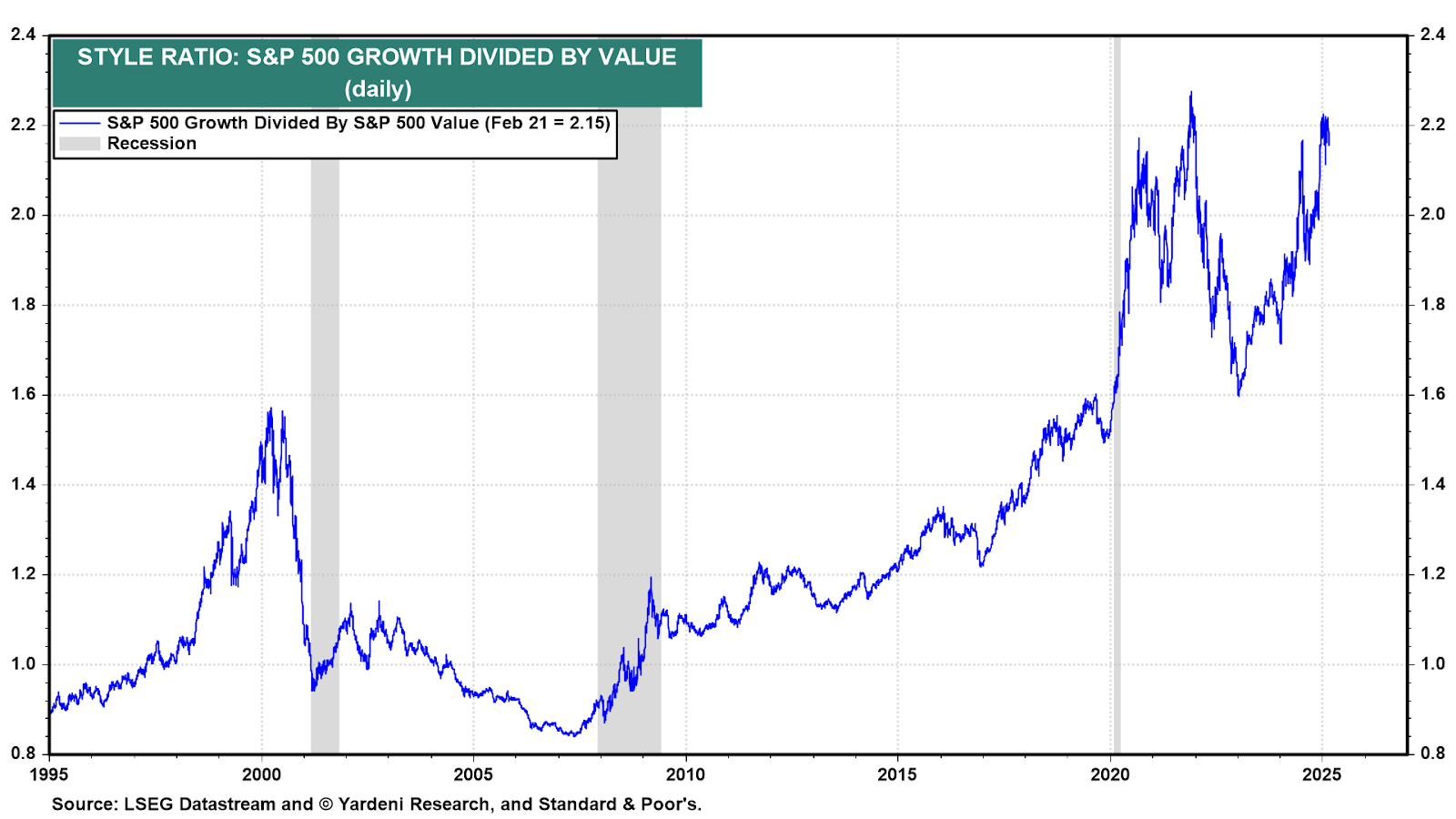

The Great Rotation

It’s extremely difficult to find mispricings in the market.

However, the correction is creating more opportunities for that in the future.

We believe our Growth to Value rotation is intact and you’re seeing that play out violently.

Here is a chart I like to trot out showing Growth vs. Value.

You can see we have a ways to go.

Microsoft, a once pricey Mag 7 stocks, hasn’t gone anywhere in a year.

The biggest culprit in Mag 7 is Tesla - that name is correcting.

Many software stocks are in a bear market.

ARM needs a Stargate deal to give it life.

Where to focus then?

Book a session with Marc, our client advisor & explore focus themes.

We believe focusing on themes that have relative value, earnings growth, and emerging momentum are a good idea.

Healthcare is one of the few sectors that is appealing and performing.

The category sold off Friday on news of DOJ investigating UNH for excess reimbursement - but out-performed other indices.

In semiconductors, Nvidia has substantially recovered the DeepSeek sell-off.

Within semiconductors, we believe Taiwan Semiconductor is once again mispriced. It has an 18x forward PE and 20% YOY revenue growth.

All roads go to TSMC. Hard to imagine Trump inflicting tariffs on TSMC. Recall, importers pay tariffs – that would be a body blow to Tesla, Microsoft, Meta, Google, xAI and the US AI ambition.

TSMC is not a screaming bargain, but it does offer relative value. They are also not blowing their earnings on capex spend - they are the beneficiary of capex.

Tariff linked names are a good opportunity as well.

If you have a strong stomach and can wait one year, names that were whacked by tariffs hold promise.

In the auto sector, we sold GM as tariff news came to the fore. Now we’re back in the name. We think the stock is near its lows – bad news is substantially priced in.

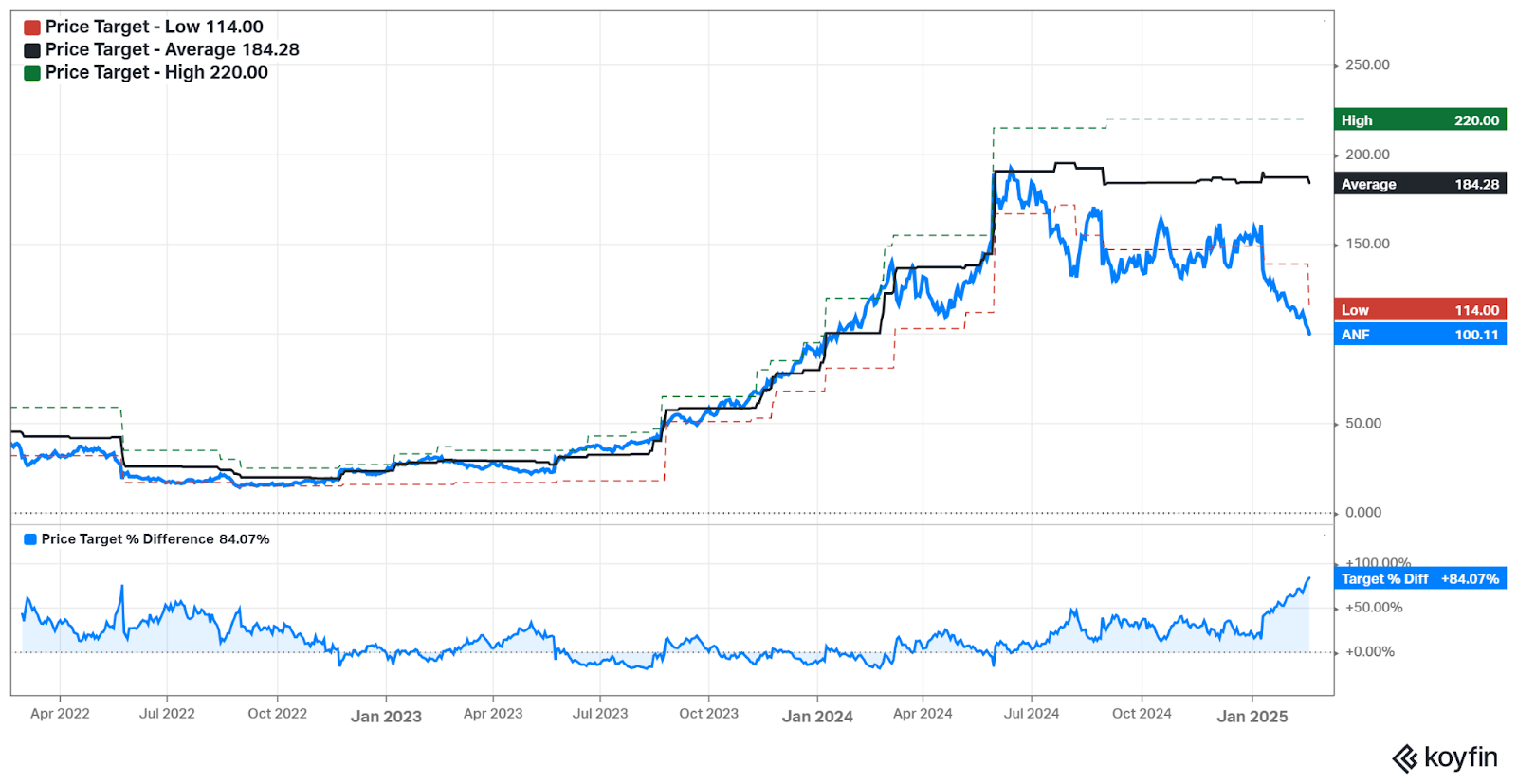

We believe Abercrombie & Fitch is setting up for some near-term downside volatility. But, within a year, it’s hard to see how this doesn’t perform quite well given the double digit earnings growth and forward PE of 9x.

We don’t have a washout capitulation here. Should the stock experience that we would want to own quite a bit of it.

Over a 3 year period, it’s hard to see how ANF doesn’t produce a strong return. Every time we re-underwrite this we see strong earnings growth fuelled by new store expansions and same store sales growth.

We see this as a high quality dislocated asset impacted by tariffs. The driver of stock prices however is earnings growth. A one-time increase in cost of good sold (of 10%) is not justified here.

What’s happened is negative psychology combined with stellar gains from 2023 have led to selling.

We’ve been wrong on the name so far. We have a 2% position size give or take.

Earnings are in under 30 days, so hard to tax loss harvest and get back in here.

When we look across various sectors in the market, it is hard to find sectors that are bargains.

Maybe Defense stocks - but you have to bet that Trump will fail in his goal of cutting defense spending 50%. (Probably a good bet, but you still have negative newsflow).

The fact that many markets are over-extended - domestic and international, large cap and small cap, growth and value stocks, quality and animal spirits - is what gave us pause these last two weeks.

We don’t have an “all clear” sign like we had at the end of August 7th.

It is possible that we get a 10% type correction with some bounces along the way to truly setup the next leg of the bull market.

A lot will turn on how Nvidia reports earnings this week.

We expect Nvidia will re-ignite the datacenter theme which also sold hard this week.

There are also good buying opportunities in that segment of the market.

However, if Nvidia’s results don’t inspire market confidence, then you could look at the current pullback evolving into a 10% correction type move.

We expect sometime in the next two weeks for homebuilder stocks to present attractive entries, as well as regional bank stocks.

We will continue to buy healthcare on dips.

There’s stuff to do, but the level of valuation makes it much more challenging to maneuver no doubt.

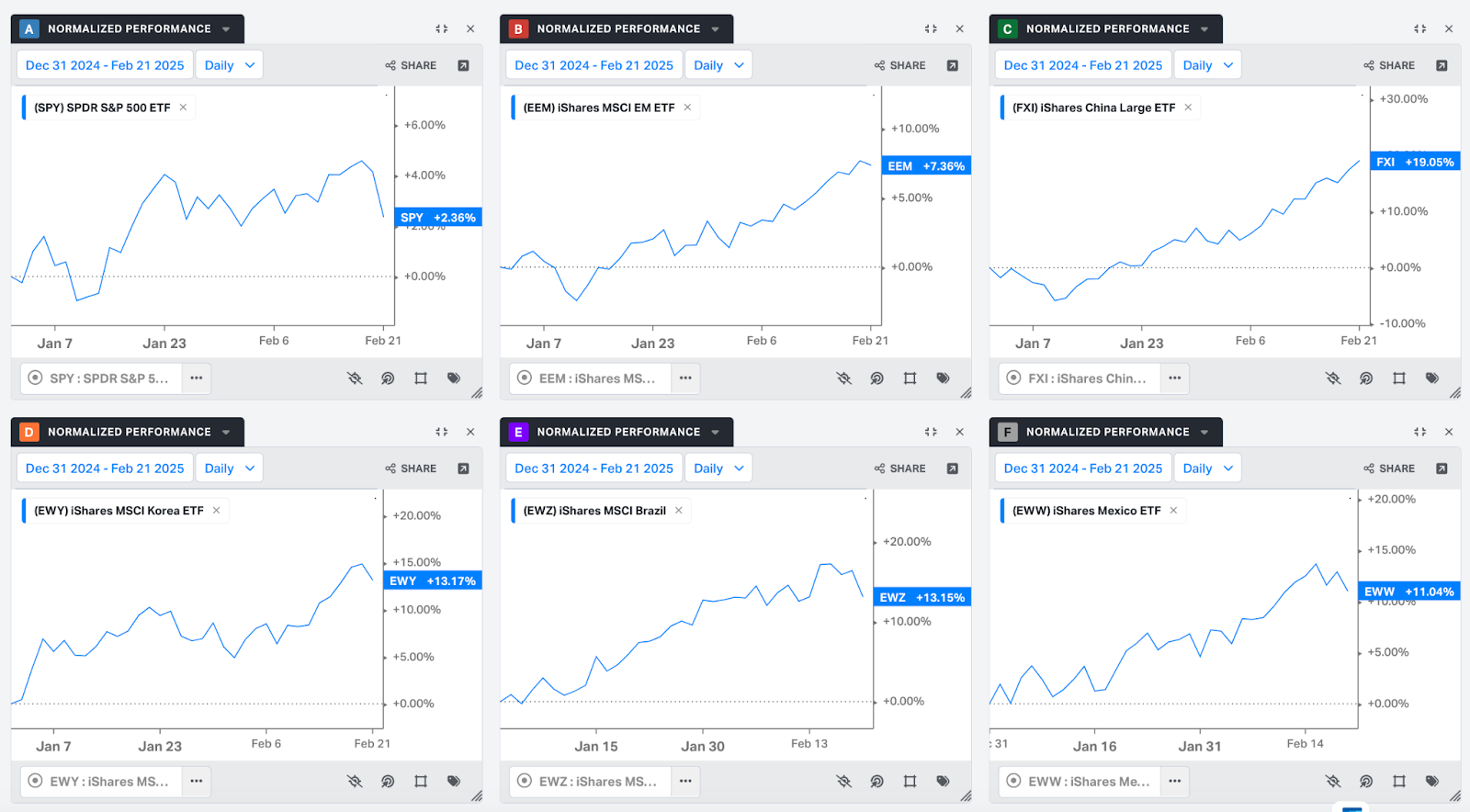

Emerging Markets Are Trouncing U.S. Equities (Europe too)

Sometime in January, we made the point the foreign investors have trampled themselves trying to invest in U.S. markets – and they made their stocks cheap in the process:

Take a look at how much the S&P 500 has lagged international markets. Imagine if you were forced only to invest in the United States.

When everyone is on one side of the boat, go to the other side of the boat.

Take a look at how foreign markets compare to the S&P 500.

We believe emerging markets - including Mexico, Brazil, South Korea, and China - are due for a breather now.

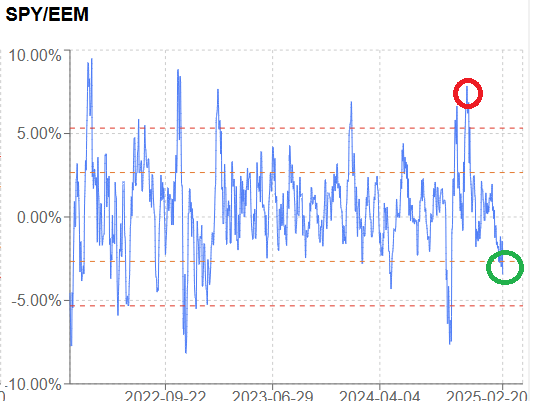

Take a look at this chart comparing the S&P 500 to the Emerging Markets index (EEM) which includes China, South Korean, and Taiwan names.

The red circle indicates relative over-valuation of the S&P 500 vs. Emerging Markets.

That red circle maps to Nov 15th - when the first post-election Trump Bump hit max frenzy.

That was the first best time to buy China and emerging markets.

Another opportunity opened a few months ago.

We are now on the other side of this pendulum – U.S. markets are selling off and China is rallying.

We do believe China is in a bull market. It beat the S&P 500 last year, and we think it will do so again!

But tactically, it’s a good time to re-position within China.

Ali Baba delivered strong results. But, better to rotate to PDD. Compare the PEG ratios and you’ll see what we mean.

Ali Baba is also experiencing a parabola now. You should sell that and rotate.

Here is a chart of PDD.

Psychology is Everything in Markets

I remember the week prior to this week, as markets were hitting all time highs and euphoria was hitting on talk of ‘global peace dividend’ was a random thought that Nvidia may be needed to save the market in a few weeks.

It wasn’t a forecast so much as an idea that was entertained.

The thought sounded completely absurd on the one hand. Here we were hitting all time highs, and now we are talking about the need to ‘save the market’?

Here we are.

It’s so important to temper one’s enthusiasm during big run-ups, and also temper the gloom and doom fear mongering at bottoms.

Trying to cultivate the quiet inner contrarian voice will help.

Buffett was right. It’s not investment analysis - it is the temperament of the investor that drives long-term performance.

Schedule a call with Marc, our advisor, and let’s discuss how we can help optimize your approach.

Macro

Scott Bessent on Bloomberg Surveillance

Lumida Wealth curates the best snippets and content on our X handle @lumidaweatlh.

We also post them in our telegram channel.

What struck me about the Bessent clip was his sensitivity to markets.

We noted that it seems like the Trump admin is A / B testing different forms of policy and seeing how the markets react.

They drop tariff news on Friday, then fix up any spills on Monday.

Bessent said he would “listen to the market”

"Now I'm inside the room trying to figure out what everybody outside the room expects us to do, how the market is going to react, and what the economic and market implications are—short-term, but more importantly, medium-term, and how that is going to affect the underlying economy." (00:41 - 01:07)

Frankly, we like this approach. It’s more humble rather than assuming a technocratic approach is best.

If Mr. Market was stuck with the initial hypothesis - universal tariffs - instead of bilateral and reciprocal - we’d be worse off.

But what about the broader investment landscape? That’s where Steve Cohen’s latest bearish outlook comes into play.

Point72’s Cohen Gets Bearish

Steve Cohen added some Red Wedding splash this Friday sharing bearish comments on the outlook for the economy.

He expects growth to slow in the second half of the year due to tighter labor supply and government cost cuts.

Cohen is making Druck’s point that ‘Trump is inflationary’

We should note Bessent made the case that Trump is disinflationary. And his policy is disinflationary: (i) lower oil and gas prices via greater production and Saudi pumping, (ii) a desire to lower mortgage rates thru lower deficit spending.

This week Trump mentioned they are looking at using Federal Housing to grow the housing supply. Most of the issues around housing have to do with local permitting / zoning.

(Towns want single family homes not big multifamily apartments).

In our reading of Trump, he appears highly respectful and even deferential to Secretary Bessent to develop policies that achieve Trump’s high level objectives.

On February 10th, Trump advisor Hessent made a statement on CNBC a goal to ‘increase the labor supply’ to fight inflation.

Part of that is via having babies - and Trump is pushing for IVF treatment. But… that’s an 18 year gestation period.

Another is via legal immigration. Trump has said he supports H1Bs. Expect more of that.

We believe Trump’s comments around Canada as a 51st state are a type of ‘short cut’ boost to increase labor supply while delivering against his ‘manifest destiny’ shared in his State of the Union Speech.

Wondering what to do next? Book a session with Marc, our client advisor & explore the world of wealth management further.

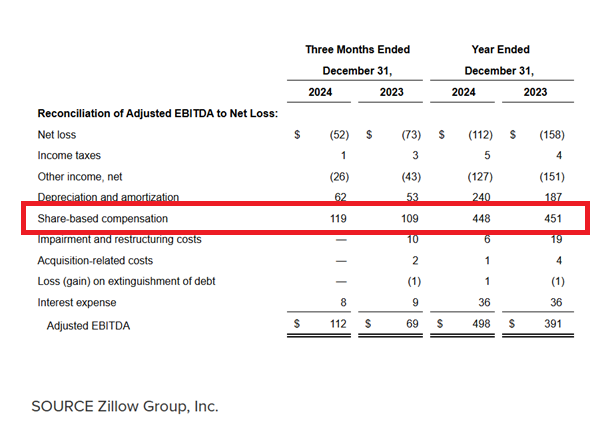

Zillow was a name we saw in various 13F filings including Altimeter and Cathie Wood (!).

I love the top of recall and app economics.

I would be an owner but for the fact that Zillow's share based compensation is absurd.

Zillow issued $1 Bn in shares issued to management in one year on a market cap of $20 Bn.

That's completely absurd.

It's a misappropriation of capital from shareholders.

From an investor perspective, it means you have the following obstacles.

You need :

1) earnings growth to exceed the SBC

2) and cover the inflation rate

3) and cover cost of capital

... before you can even start talking about excess returns.

Add to that a valuation multiple that is pricier than NVDA

For those reasons, I'm out.

Take a look at how significant SBC is relative to earnings

Shareholders in Zillow include Cathie Wood, Bridgewater, Altimeter, Coatue...

Zillow's business model is essentially creating one billionaire per year, paid for by shareholders

Imagine instead if they did buybacks

Zillow was a Q4 animal spirits pump as well wasn't it?

But Zillow isn't the only case where market participants may be mispricing reality. Broader market conditions continue to reflect inefficiencies in how risk and reward are being evaluated.

Markets Misprice Risk & Reward

AI

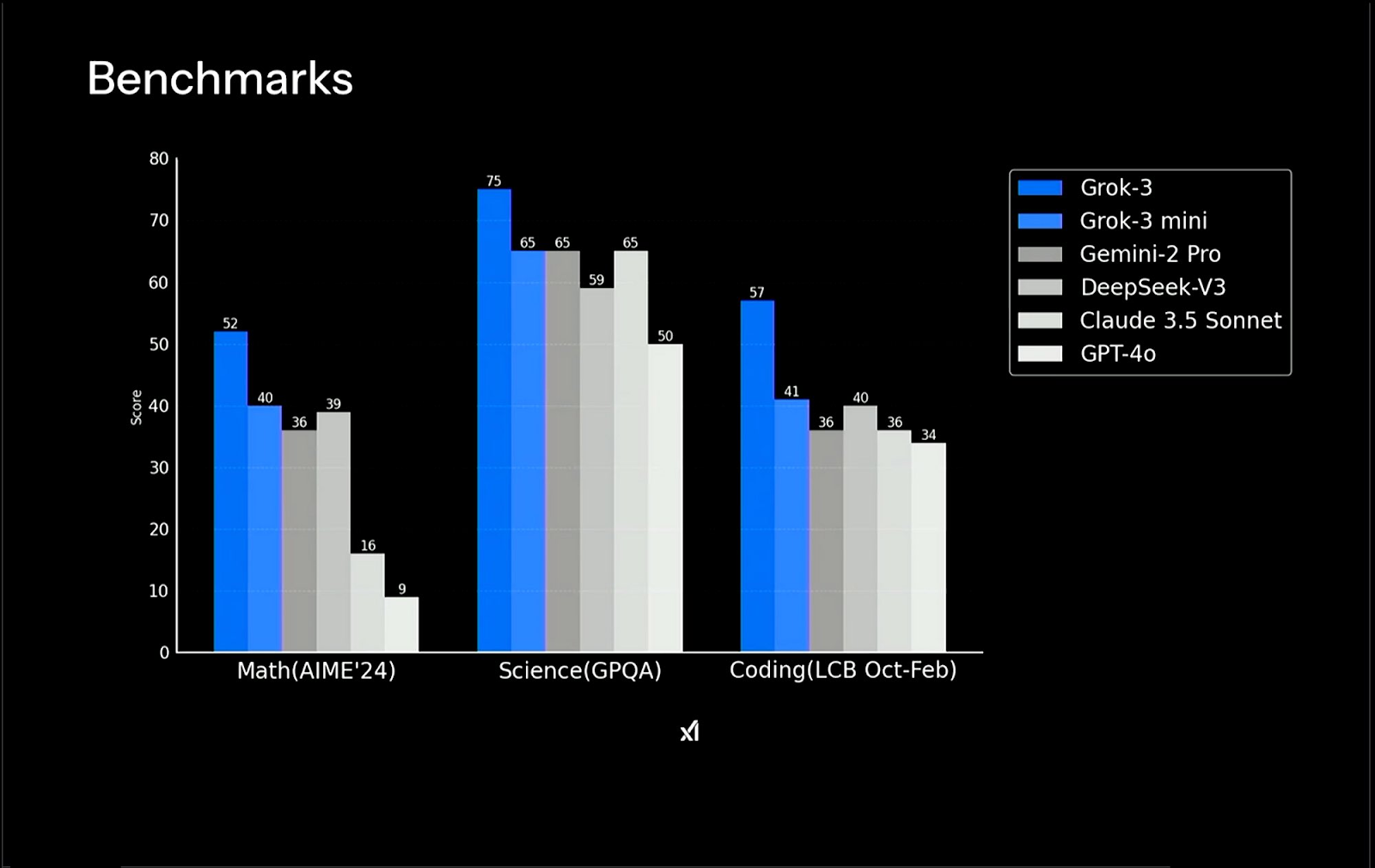

GROK vs OpenAI

I switched to Grok 3.

The model’s Deep Search and Think modes are simply outstanding.

Anyone doing research will need it as a Must Have.

Elon Musk dropped this before OpenAI closed their Softbank $350 Bn round.

If xAI is worth $75 Bn and has more reach, what does that imply about OpenAI’s most and valuation?

Check out the benchmarks.

You know why Elon dropped it before the round closed right?

Same reason Google dropped Quantum news in the middle of OpenAI 10 Days of AI release.

They are all trying to destroy and interrupt each others plans aggressively.

I think about that OpenAI engineer Suchir Balaji.

Was there foul play?

Doge

The average Federal worker makes $150K per year including benefits

The average American makes $60 K.

The median worker makes less.

The average Federal worker has worked from home even after Covid (?!).

The average Federal worker is not managed to goals or deliverables.

Instead, they own processes and activities like microservices in a software stack.

In my first job out of school, I helped companies find ways to save tens of millions of dollars.

These were well run blue chip companies you recognize.

Waste and excess accrues like barnacles on the bottom of a ship.

Are there tens to hundreds of billions of waste in the US government?

No doubt.

Cut, cut and cut more.

High Yield Laughs

Stay tuned, stay informed, and as always, stay ahead.

Not subscribed yet? Don’t miss out on future insights—subscribe to the newsletter now!

As Featured In