Here’s a preview of what we’ll cover this week:

Macro: SaaS is dead

Markets: China’s rate cuts boost momentum

Company Earnings:

AI: OpenAI; Capex

Next week, Ram Ahluwalia will be speaking at the Mainnet 2024 Summit, hosted by Messari from September 30 to October 2, 2024.

As the CEO and CIO of Lumida Wealth, Ram has been actively sharing his insights on digital assets.

Our biggest performing trade was buying ETHE in 2023 at a 40% discount to NAV, and then starting to exit that position in May of this past year.

The value of ETHE increased from $7 to $30 over that period.

META

Meta is at an all-time high after a successful demo for its roadmap on AI.

Long-time readers will know that within Mag 7, our top holdings of Nvidia, Meta and Google. (We also have warmed up to Amazon after its 200 DMA).

I recommend folks listen to my interview with Institutional All Star analyst, Mark Mahaney, where we discuss for more.

There’s a lot to say about Meta - distribution, embedded real options, Founder leadership, cheap valuation relative to peer group.

The single most important is this: Meta is not priced in for AI. AI leader have much higher multiples than Meta.

And Meta has a credible shot on goal for taking attention away from Apple and Microsoft.

We believe AI is real - and that conventional operating systems and hardware experience are at risk of disruption over the next few years.

Meta is up 56% YTD. Hope you are enjoying the ride.

We get it. Mark gets it. Now, markets are starting to get it.

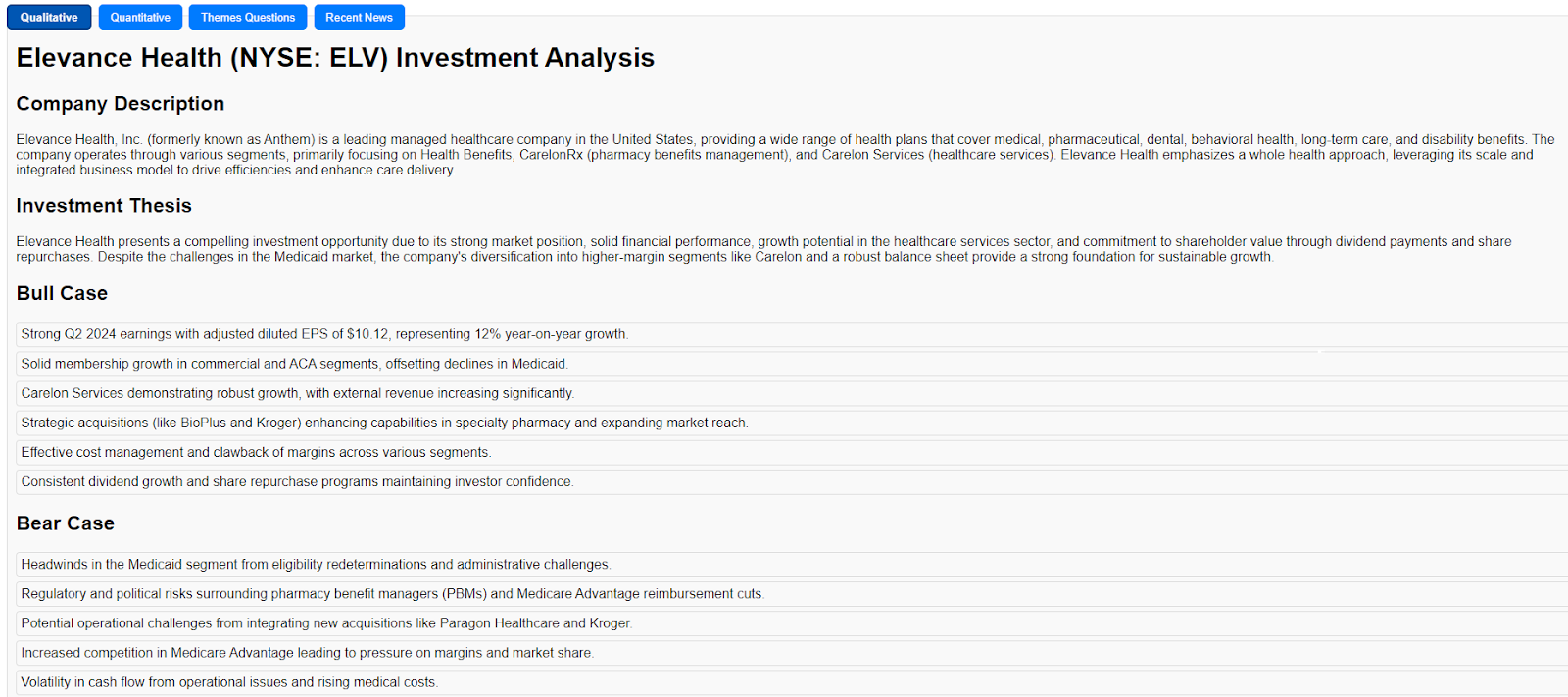

Elevance Health

This week we picked up Elevance Health (ticker: ELV).

This is a name we have ‘stalked’ for a while (E.g., waiting for a good pullback). We were waiting for the overall healthcare index (XLV) to pull back.

It finally did, and then we established an initial position this Friday.

Here’s the XLV index. You can see the healthcare sector is under steady institutional accumulation with the regular buying stepping in at the 50-day moving average.

Here’s Elevance which had a ~6% pullback from All Time High.

We like to own high quality businesses that have good trends, factor exposures and then add exposure on pullbacks.

Is this the bottom. No one really knows. Is it a good probability based risk-adjusted return? Yes.

Speaking of healthcare, we also added to CVS earlier this week.

Lucky timing, as CVS was up 4%.

What you see in CVS is several months of consolidation. What’s happening during that process is weak hands that have lost conviction (and bought in at much higher prices) are churning out and selling to stronger hands – like us – that see a dislocated high quality asset.

That ‘dislocated high quality asset’ is a bread and butter strategy for us. It’s why we bought JPM in the banking crisis. Or, semis last year. Or, LPL Financial (LPLA) a couple months ago.

CVS then exhibited a ‘breakout’ on high volume. That’s a classic Mark Mineverni setup for those that know Mark.

In a world where S&P valuations are at their top decile, we take solace in having exposure in a ‘mean reversion’ bucket.

Unlike a momentum name, we have no expectation that CVS will generate performance month in and month out with a higher priced thematic story like Meta.

But, we do expect a 30% to 50% return in 1 to 2 years. It’s hard to know exactly when. So, we pre-position there. And, when markets are overbought, we rotate capital into CVS as the downside as you can see from the chart is limited relative to the upside.

We made the decision to rotate into CVS further because from a Markets perspective, we see the S&P and QQQ indices overbought on bullish sentiment post 50 bps rate cuts.

QQQ Index

We expect we’ll get a modest pull-back here. So, why not add to CVS and reduce exposure to momentum?

Positioning Is What Matters

In the long run, returns are driven my valuation and earnings growth. The correlations are at the 90% level and the theory makes sense.

All stocks are a claim on a long-term stream of discounted cashflows.

In the short-run, we believe positioning interacting with newsflow drives return. Sentiment is bound up with positioning. When people are very optimistic, they are highly positioned long and perhaps on leverage. That means there are fewer buyers and the markets can get exposed to air pockets.

We believe the combination of David Tepper’s China bull case on CNBC, Micron’s Earnings, and favorable initial claims data (once again!) contributed to this weeks rally.

But, underneath the hood we see institutions mostly selling to retail investors that are buying late.

Overall, we are optimistic about year-end S&P levels. A 6,000+ number is quite possible with strong corporate earnings growth and an economy that is going to get super-charged with Fed rate cuts that, in our view, the economy doesn’t need.

Expect to hear the word Goldilocks next year, followed by ‘Should we raise rates?’

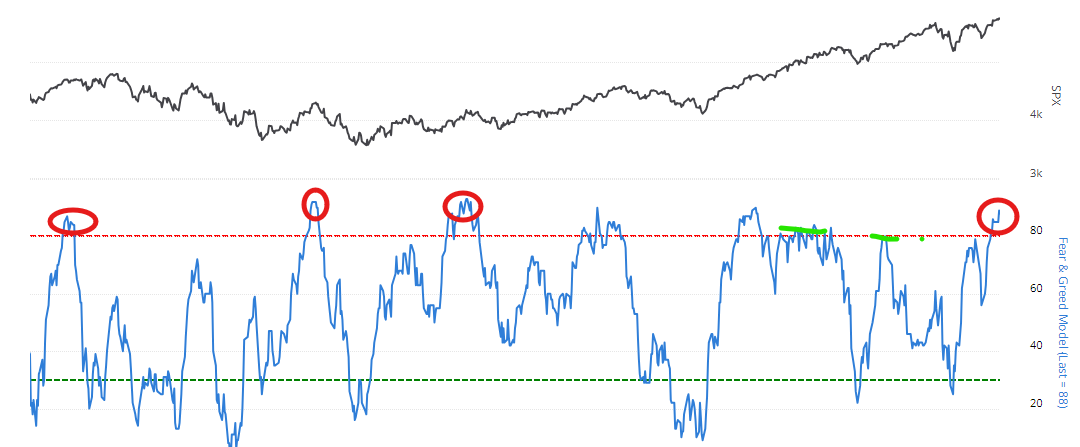

When we look at how investors are positioned, we look at a number of composites. Here’s a fear & greed model that combines sentiment and put/call ratio data.

Overall, markets have handled the recent overbought condition well - and that bodes well for longer-term.

Shorter-term though, we think there’s some give back on the hotter market themes such as semiconductors.

Indeed, Nvidia dropped 3% this Friday even after news Open AI is likely to close their funding round. (That will benefit Nvidia and Nvidia surrogate CoreWeave - where we are an investor).

Nvidia is tracing out a pattern of lower highs.

We still love the name and continue to have it as one of our top positions. But, we aren’t adding to it here.

That said, overall, one should remain bullish going into year-end.

The Fed is cutting when the econmomy doesn’t need rate cuts. Global central banks are largely easing. Corporate earnings are strong.

Don’t confuse the tactic with the broader trend.

Back to Elevance

At Lumida, we strongly believe AI is set to transform investing.

HEre’s an example.

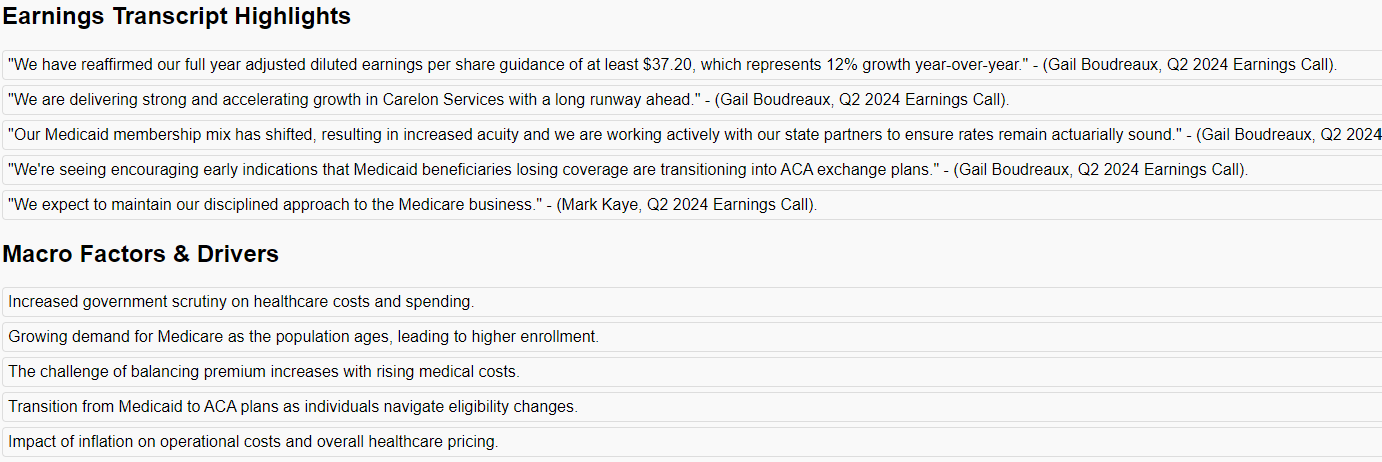

We share below the bull and case for Elevance from our AI system. Note: We had a prior in-going view that Elevance is a quality compounder before – we aren’t relying on the AI here – but it is unquestionably a productivity accelerator.

We have tuned the AI to think how we think and spot risk factors and opportunities that may not be obvious.

Have a look:

Incidentally, if you are an investor that has an interest in learning more about this software, shoot us an email at [email protected].

We think we’ve built something quite special or eating our own cooking right now.

We have also trained the AI to study the entire peer group so it can do Porter’s Five Forces competitive analysis.

Competitive advantage is always in some industry context.

The big long-term questions around Elevance are:

How will they navigate increased utilization of healthcare from insured population?

How will shifts to virtual healthcare models impact Elevan’s business structure and service delivery?

SaaS Is Dead

The SaaS Era is Over ; Software is a Business Tool not a Business Model

Sam Lessin makes the case that SaaS is dead.

We agree. We wrote a few months ago in the newsletter titled ‘Where are All the Great Tech Investors’ that the big tech firms have significant competitive advantages.

SaaS by and large does not.

And AI is poised to disrupt this model. AI app related revenue is already growing faster than SaaS revenue.

I don’t see how firms like Adobe or Salesforce survive this transition without getting severely mangled from an earnings growth perspective.

Focus on picks and shovels players, or tech firms that have a distribution and data moat.

Zuck gets all of this, and META is at all time high.

The Haves vs. Have Nots Market

Mr Market expects the next ten years earnings for American companies to have even better growth than the last ten.

That’s quite possible with productivity growth on the rise.

However, I expect a significant amount of Shumpterian creative destruction.

Those are lofty expectations will be met by a narrower set of firms that are AI-enabled or AI-proof (e.g., such as real estate, healthcare delivery, etc.)

I’d expect a lot more feast and famine in the next ten years

Destruction of businesses like Walgreens and Intels. We are going to see rapid growth of leaders in new categories

AI, robots, e-comm and mobile is a curve ball hitting different players in the same industry differently

Look at Dollar General vs Walmart for example. Walmart is benefitting not only from the “consumer trade-down” to value brands…but also from GLP1s, curbside delivery, and e-commerce. (I learned that from our AI - how wild is that).

Next ten years will be one of the hardest for investors to navigate also b/c valuations are now top decline

I spoke to a family office that owns world-class businesses: SPGI, FICO, ICE, VISA and others

Those were fantastic buys in Nov 2023 (and Visa just 1 month ago), now you have FICO at 70x forward and 100x trailing PE.

That safe haven and “quality bet” is fully priced. I believe rotating to quality small and midcaps with earnings growth and room for multiple expansion is a better idea here.

Here’s an ETF that is indexed to quality businesses:

I would wager that these quality names which dominate the index are more likely than not to pull back over the next week or two - which also coincides with weak market seasonality.

So, we’ve built some cash up over the last week to take advantage of that opportunity.

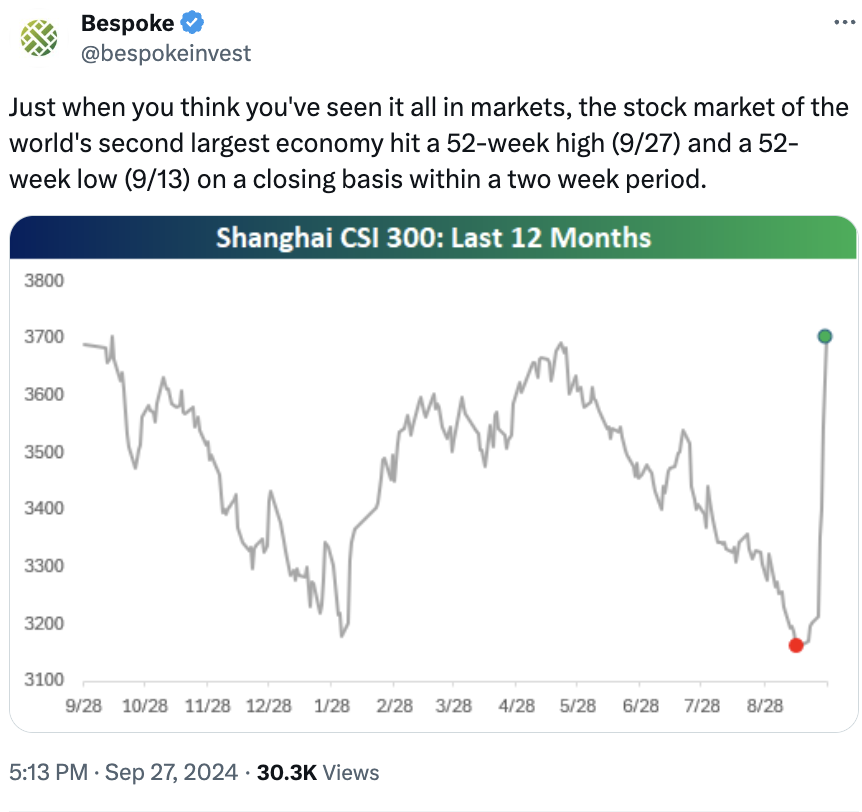

China

China is beating the S&P YTD due to a 1 week move.

This is the ‘hot ball of liquidity’ I have discussed previously in action. Please see my “On the Margin” podcast for more on that here:

Breaking news: China announces multiple rate cuts and banks’s reserve ratio requirements.

Lower bank reserve ratios mean banks can lend more by holding less capital.

(As an aside, I love this comment by Joe. His point that China is pressing on the accelerator at this time is right on. That should support commodity and energy prices.)

Long-time readers will know we wrote about the capitulation in February here.

We also discussed David Tepper’s positioning here around minute 9:00 during Lumida’s Quarterly 13F review.

I recommend folks review this thread on how capitulations work for more.

Notice - a full 7 months after the lows there was still skepticism around China.

China is in Phase 2 now. Phase 2 is when a market climbs a wall of worry. There’s a lot of skepticism.

I noted before - we looked deeply into China and we don’t see this as another 2008 crisis.

The main issue is property prices are declining, and that’s hurt consumer psychology. Consumers are saving 30% of their income. (There’s also double digit youth unemployment.)

Is it worth buying into China now? Not really. I’d wait for a pullback. My style is not to invest in parabolas, and that’s what I see here.

There are a lot of momentum monkeys trying to buy into China now.

We are selling into that strength.

That momentum bet has less than a week or two left in the tank and then we’ll pull back.

We’ll see some narrative around how China’s stimulus isn’t enough or must be backed by stronger fiscal supports.

Take a moment to study this chart.

Notice the May parabola was a sell cue. I expect this will be the same. Melt-ups end in melt-downs.

It takes a few months to work off a parabola.

China is still in a bull market, however, and dips should be purchased. The technical skill to navigate this market and get good entries is difficult.

I also suggest sticking with the best. That means buy TenCent on Pullbacks. Think of TenCent as a combination of Meta and LinkedIn - they are the leader in social media.

E-commerce will increasingly flow to Social Media. BABA is a nice value play with buybacks. But it does have pressure from PDD. It’s a reasonable idea… however, between the two, my thought process is, buy the fastest growing businesses without any structural issues while the market is cheap.

What I want to know thematically is this…

Will China’s easing create a bid for commodities - oil and energy?

Energy stocks and oil prices are in the dumps due to softer demand from China.

China, at the same time, is over-producing EVs and Solar that the world isn’t buying.

China will consume that internally. Does China’s renewable investment suppress hydrocarbon demand?

China - The Hot Ball of Liquidity In Action

AI

SOMETHING IS WRONG AT OPENAI

What did Ilya see?

What did Murati know?

What did Sam do?

Last year, the west coast VCs thought OpenAI created AGI and that caused last Fall’s drama.

My view is the opposite.

I believe OpenAI has realized they must spend billions just to stand in place.

Their parent, Microsoft, is lagging the S&P and the bills are too damn high

Capex is so high, it is crimping $MSFT’s margins.

So, OpenAI is pivoting to a for profit.

But… the leadership sees they are boxed in.

Satya Nadella once remarked ‘We are above them, beside them, and below them’.

One could say the same for OpenAI’s competition.

Microsoft is up top competing on Enterprise.

Google on the left going after Personal Assistant AI.

Meta on the right with the ability to attract the best AI engineers under Yann LeCun

Anthropic is beneath.

Altman is throwing a lot at the wall:

Let’s build a phone and compete with Apple

Let’s partner with Apple and then build the phone

Let’s build a foundry and compete with Nvidia

Let’s raise $1 Bn+ from the Kushner’s and then send it to CoreWeave

That’s not empire building.

An empire is built on a foundation of success.

You need a textile mille (Berkshire) or a search engine or an operating system to fund all the grand adventures.

The simultaneous surprise departure of three executives on the eve of closing a financing means something is wrong at OpenAI.

The right move this whole time was to invest in capex receivers

According to McKinsey, generative AI is estimated to add up to $7.9 trillion to the global economy annually.

Overall, McKinsey estimates the AI economy could add $25.6 trillion to global GDP over the next couple of decades.

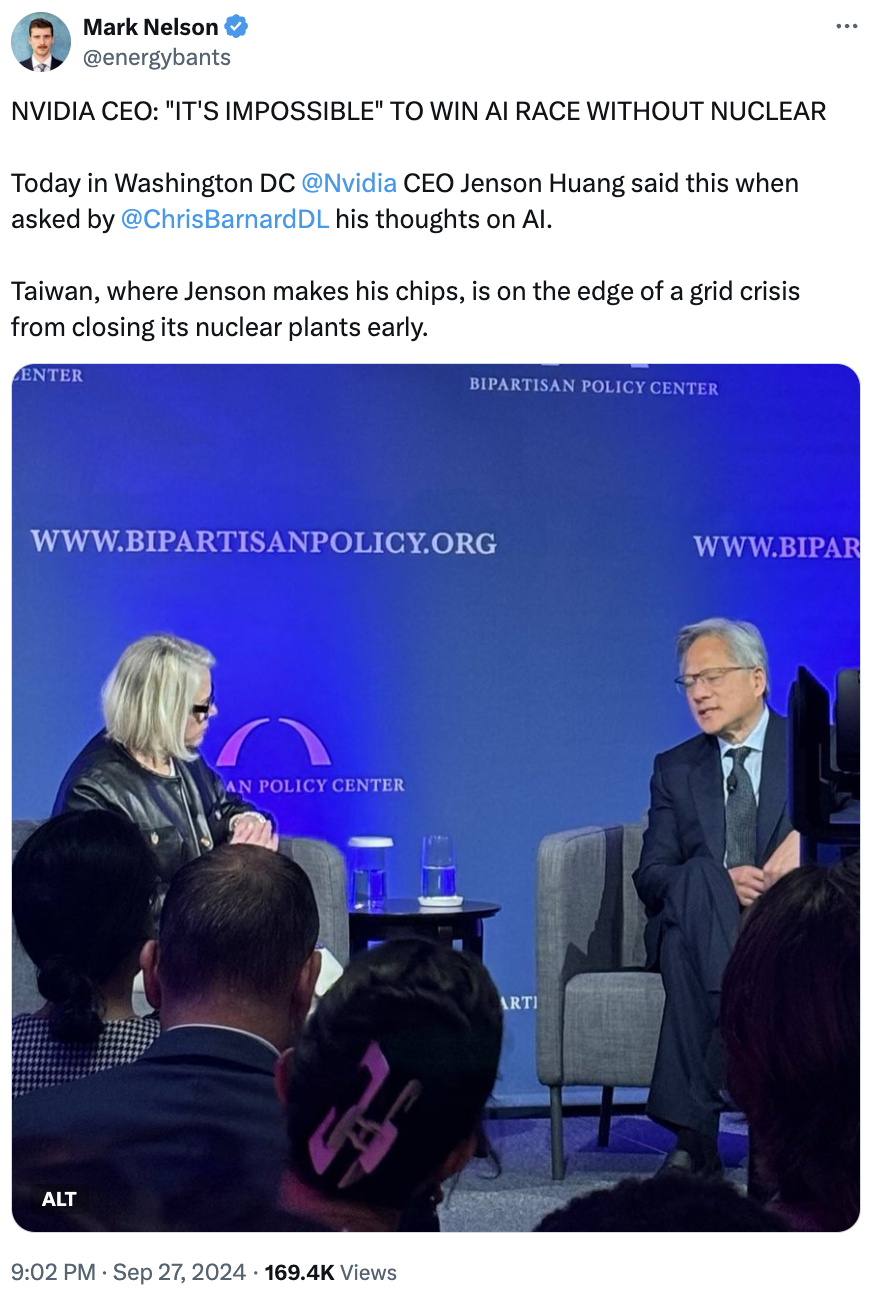

NVIDIA CEO: "IT'S IMPOSSIBLE" TO WIN AI RACE WITHOUT NUCLEAR

Today in Washington DC Nvidia CEO Jenson Huang said this when asked by Chris Barnard his thoughts on AI.

Taiwan, where Jenson makes his chips, is on the edge of a grid crisis from closing its nuclear plants early.

Digital Assets

I'm looking forward to speaking at MainNet next week along with Matt Hougan from Bitwise!

Looking through my notes from last year, my main message was to buy these 'discount to NAV' ETFs such as ETHE and GBTC.

Since then those assets have gone up 2x to 3x depending on your entry point.

We started rotating out of that in May of this past year as we started to hit long-term capital gains.

A big lesson from all of this:

Dislocations create opportunities

Just like the banking crisis put JP Morgan on sale last year.

Or, just like the Nvidia Anti-Trust meme put Nvidia on sale a few weeks ago.

Or, buying China after the capitulation.

Focus on the highest quality asset in the dislocation.

Go for quality rather than junk when there is a broad-based mark down in asset values.

If you wait for these names to hit all-time highs, then guys like me are selling these to you into the hype.

If you are making an investment that is 'easy and comfortable' you are probably paying for a fully or over-valued asset.

The best returning investments are always uncomfortable at the moment.

Shoot me a DM if you will be at MainNet and want to chat.

Preview: Alt season is coming back.