Here’s a preview of what we’ll cover this week:

Macro: Two-Year Bull Market Surge

Markets: QXO, Shelter Inflation

Company Earnings: Microsoft vs. Nvidia, Utilities, Tesla

AI: AI Nobel Prize, AGI Timing

Digital Assets: Bitcoin Turbulence

Last week, Ram took the stage at the Permissionless III conference as a featured speaker and also was interviewed on the Forward Guidance podcast.

Lumida had a small short position in Tesla going into their Robo Taxi event.

Tesla’s share price dropped 8%. Click here to hear Ram’s informal thoughts on the banks, Tesla, the insurance sector, and the state of Venture Capital.

This week, we had Jeff Park from Bitwise with us in our latest episode of Non-Consensus Investing.

Jeff is an ex-Morgan Stanley equity derivatives trader who also was a trader at Harvard Management Company before joining BitWise.

We discuss “What Harvard Got Wrong?” and plenty more in this episode on Youtube, Apple | and Spotify. Be sure to subscribe.

02:06 Harvard Management Company

10:18 Multi-Manager Models and Alpha

14:44 China and Global Liquidity

20:09 Memes and Market Movements

22:56 Market Dynamics and Indicators

25:30 Volatility and System Stability

30:02 Liquidity Challenges and Economic Indicators

32:33 Investment Strategies for Bitcoin

35:07 Hedge Fund Skill Disparity

38:24 Momentum Trading

42:07 Trend Following Techniques

44:12 Impact of Elections on Digital Assets

49:26 Institutional Adoption and Market Behavior

51:02 Trading Psychology and Best Practices

Also, later this week, Ram was invited to appear on the Wealthion podcast, where they discussed AI, the Fed, and the Economy. Click here to watch the full episode.

01:54 Economic Outlook and Labor Market

03:43 Implications of Interest Rate Cuts

06:37 FED's Decisions and Market Adjustments

09:49 Housing Market and Retiree Investment Behavior

14:25 Bond Market and Investment Strategies

20:10 AI Investing Strategies

23:10 Energy Transition & Semiconductor Investments

26:33 AI Demand and Strategic Importance

28:44 Nuclear Energy Revival

31:14 China Market Dynamics

35:18 Investment Liquidity Trends

36:53 Long-term Investment Strategies in a Transformative Era

41:32 Stock Picking and Active Management

Here is a shorter highlights reel if of interest.

Macro

The S&P hit all time highs again this week on strong bank earnings.

JPM and Wells Fargo noted the consumer is fine.

Last year, we noted during the banking crisis that the move to make was to buy the highest quality dislocated asset: JP Morgan.

The stock is now at $222 now - or an 85% gain in 1.5 years.

(We also bought UBS and Morgan Stanley during the crisis as well.)

We love buying high quality dislocated assets when they go on sale. The key is analysis so you have the conviction to step in and pluck the gem, and ensure you are not stepping into the freight train.

Our most recent high quality dislocated asset play was CVS.

CVS is now up 20% since our first buy in May - exceeding the S&P with much less capital at risk.

CVS Chart:

We call these ideas ‘Mean Reversion’ plays.

I believe as we get into Q4, we’re going to see a plethora of ‘left for dead’ stock rally sharply as rate cuts and the prospect of Goldilocks come into view.

The vibecession is ending soon.

Back to the Banks

I enjoyed this write-up by Telis Demos at the WSJ on bank earnings.

Excerpts:

JPMorgan’s card-services sales volume, which excludes commercial cards, rose just under 7% from a year prior, versus closer to 8% growth in the second quarter, and over 9% in the first.

On the face of it, that appears to be a sign that activity might be slowing, albeit perhaps only softly. But JPMorgan Chief Financial Officer Jeremy Barnum said the spending numbers still need to be considered with the pandemic, and its aftermath, as context.

Coming out of that difficult period, there was a “heavy rotation” into travel and entertainment spending, “as people did a lot of traveling and they booked cruises that they hadn’t done before, and everyone was going out to dinner a lot, whatever,” Barnum said. “That’s now normalized.”

Normally a reduction in this kind of spending might signal a rotation out of discretionary spending and into nondiscretionary items—the things you need every day, such as gasoline or groceries. That in turn is usually a sign that consumers are preparing for a worse economic environment.

But that isn’t what JPMorgan has been seeing across its consumer data. For example, it hasn’t seen a weakening in retail spending.

“So overall, we see the spending patterns as being sort of solid and consistent with the narrative that the consumer is on solid footing, and consistent with the strong labor market and the current central case of a kind of no-landing scenario economically,” Barnum said.

Vibecession is Ending; Welcome Goldilocks

It’s amazing how gloomy people continue to feel.

We had GDP beat expectations - again. We had a blistering jobs report that exceeded expectations by 100K jobs.

We have a Fed cutting rates into all time highs and high productivity rates.

This is a Goldilocks setup folks. There’s an anxiety in the air…

If I were ever get a tattoo, it would read:

"Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria"

This is Non-Consensus courtesy of investment legend John Templeton.

Consider this:

The S&P is near All Time Highs...

and the VIX 'fear gauge' index is elevated.

This is not what euphoria looks like.

We might see euphoria towards year end though as the Fed is cutting rates at record valuations.

Need to turn the cards over one day at a time.

Tax Season Is Here

I write about markets often. However, tax alpha is the best!

Tax is a lever in your control.

If you are expecting to have a large capital gains bill in tax year 2024 due to the sale of appreciated assets - reach out to us.

There are various tax loss harvesting strategies that can help substantially mitigate tax. We work with Founders and holders of appreciated stock to help them get liquidity without a big tax bill.

Email [email protected] for more.

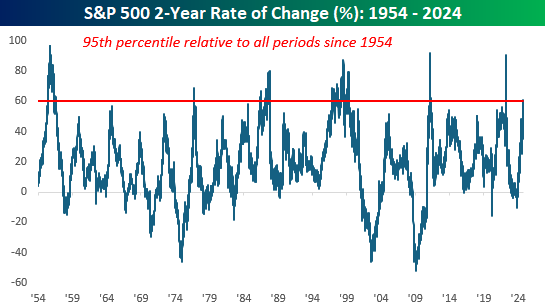

Two-Year Bull Market Surge

As the bull market tunns two, the S&P 500's current 2-year rate of change of 60% ranks in the 95th percentile relative to all other periods.

You can see here the momentum usually continues until we get a parabola where sidelined capital gets into the market. The word ‘Goldilocks’ will help them get psychologically comfortable to do so.

(Also, I can’t tell you how many people are still offsides in bonds.)

This data suggests we are entering Phase 3 of the bull market.

Phase 1: Assets are hated and ignored; deep revulsion.

Stocks are basing

Phase 2: Wall of Worry Rally (We are Here)

Stocks go up on Multiple expansion – the bulk of the move is here

Phase 3: Momentum Rally - there is a common recognition that we have Goldilocks

Stocks go up based on earnings growth

Phase 4: Euphoria

This is where you see Parabolas and you want to rotate out gradually

An ebullient IPO market is one of the cues to look for

A 60% rate of change is a rarity.

The index has never been lower 9 and 12 months later when the uptrend has been this strong.

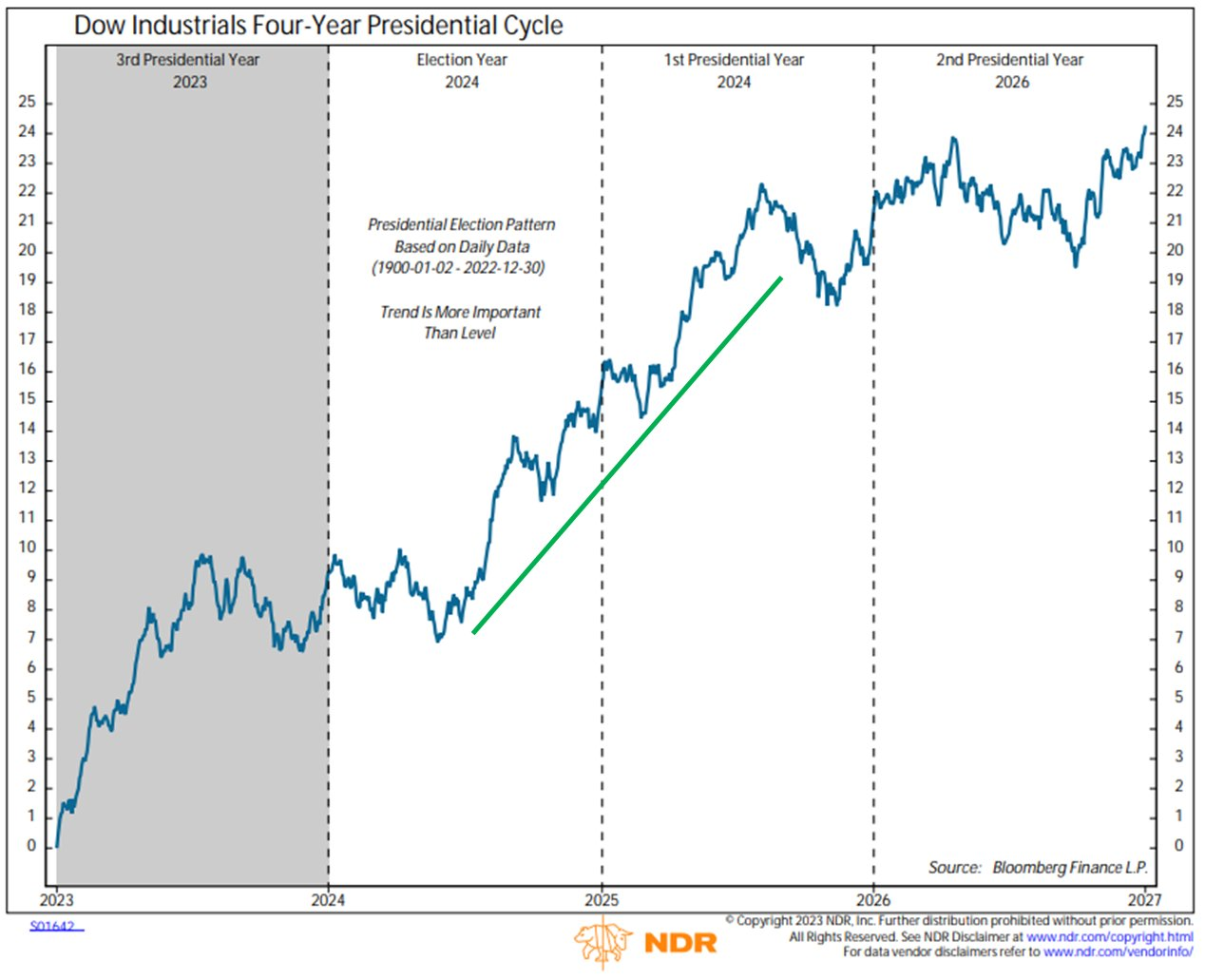

Let’s take a look at the Presidential Cycle. After all, politicians run all sorts of stimulus during election years and they pay for the hangover later.

You can see election years are positive. Perhaps sometime in 2025 or 2026 we’ll see weakness.

I believe a catalyst could be a resurgence of inflation. This is not the focus now - so stay invested.

Also, mortgage rates and the 10-year are tightening on behalf of the Fed.

Nevertheless, if China is stimulating their economy then oil and commodity prices will increase.

The CPI print was hotter than expected this past week. That may be a preview of what we might see next year.

We continue to look to 2019 as a rough guidepost for how markets may evolve.

Q4 was a strong rally on the heels of adjustment cuts, followed by a hangover in 2020 Q1.

We strongly believe tilting to quality value and cyclicals make a lot of sense: regional banks, insurance plays, quality small and mid caps.

On Growth stocks - stick to growth at a reasonable price. We continue to like Nvidia - which appears to have sold out much of the Blackwell series - due, in part, to their PEG ratio (PE vs Earnings Growth) which is lower than anything in Mag 7.

A number of sell side banks raised their price target on Nvidia to $150. We’ll see that number this quarter.

Our other growth stocks as you may know include: Meta, AppLovin, and Google.

Google is mispriced and has an anti-trust cloud hanging over it.

We’ll soon see a new narrative that allows light to pierce thru the clouds.

We saw Merrill make a comment that much of the anti-trust issues are overblown. That’s a start.

We added to our Google position this week.

Quality Compounders & QXO

Interesting to see hedge funds and RIAs start to build positions in QXO.

If you recall, Lumida bought into QXO at the $9.14 price alongside the Walton Family, 3G Capital, and Duke University in July.

We couldn’t get as much supply as we wanted so we also bought in the secondary market between $10.90 and $12.

The stock is now $15.59 – so the Walton family is sitting on a 70% gain in a couple of months.

We still have a position now but have brought it down from a significant overweight and selling in the $15 to $16 range to bring it to a normal weight.

I remember when I saw this I called our clients and said I hadn’t seen an opportunity this asymmetric in a decade.

Meaning, my downside expectation is we make only 10%. (Why would the Walton’s sell when they just bought?)

If you want to join our list for future deals and are a sophisticated investor be sure to email [email protected].

I personally invest in our private deals to date - QXO and CoreWeave -so there is skin-in-the game.

We can’t announce we are doing a deal because of SEC solicitation regulations - so be sure to establish a relationship.

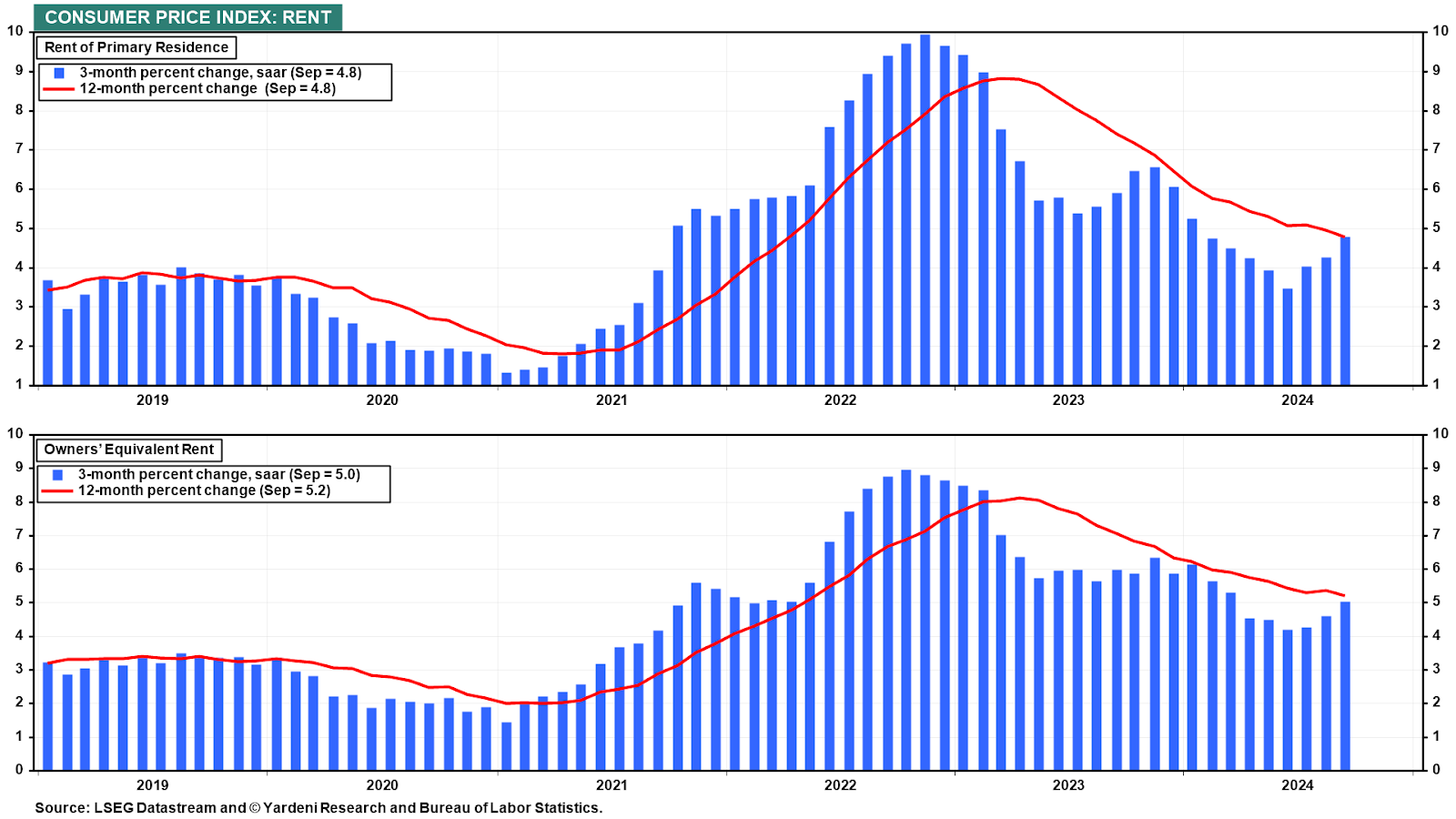

Inflation

This past week we saw inflation come in somewhat hotter than expected.

One cannot take for granted that the dragon of shelter inflation is defeated.

The left-tail risk for the market is a resurgence is shelter inflation. I’m not worried about commodity prices just yet - China’s demand bid for oil still isn’t there.

Microsoft vs. Nvidia

Microsoft is near the 200 day moving average and lagging the S&P.

It’s paying billions of dollars to Nvidia which is approaching its all time high.

This is the ‘bet on picks and shovels’ - or capex receivers thesis - in a nutshell.

Here are 5 data points that came out over the past few days

Foxconn CEO said that demand for Blackwell is "Crazy" - adding a new facility in Mexico to satisfy Blackwell orders

SMCI said it is shipping over 100K GPUs per quarter (didn't cite Blackwell, but not much else out there)

MSFT is announced that Azure is the first cloud service to run the Blackwell system GB200

TSM is moving to production with computational lithography "cuLitho" to push to accelerate manufacturing and push the limits on physics.

NVDA 's CEO, Jensen Huang, stated that production is on-track and demand for Blackwell is strong.

We did add to our position earlier this week. It’s not my style to chase.

The last good entry was in mid-September at the $105 level.

We wrote about that on X here.

Going into Q4, we believe that’s an excellent time to participate in what we expect will be an S&P that hits 6,000.

If you see the value of our research and our invest alongside clients approach, consider shooting an email to [email protected].

I encourage you to ask about our performance, tax strategies, and our focus on wealth creation.

Utilities

INDIANA JONES & THE GREAT ROTATION

We at Lumida Wealth sold VST earlier this week and documented that call in this this tweet.

Is it the top?

I have no idea.

Is the risk / reward as attractive as it once was?

Absolutely not. We saw a parabola and simply waited for the first big red day to suggest a reversal in trend.

We still like Utilities as a bet on datacenter growth over a longer time frame.

It’s a question of tactics and nimbleness vs. long-term view.

Tesla

We’re skeptical on Tesla’s over-valuation, heightened competition, and lackluster earnings.

The stock dropped 9% this Friday on a disappointing announcement.

This stock has gone nowhere in 3 years. People that made money on the way up are churning and missing better opportunities elsewhere.

A common mistake I see: investors that made their money in a certain name or category fall in love with it. They also assume they have an ‘edge’. I call it The Attribution Error – per nobel laureate Daniel Kahneman in his book “Thinking Fast and Slow”

JP Morgan noted an underweight at $130 target vs $217 where it is now: “.. last night’s event .. was notably lacking in detail, including .. the path to regulatory approval, or even the HMI for its network .. or key aspects of the business plan .. All this to us suggests material downside risk ..”

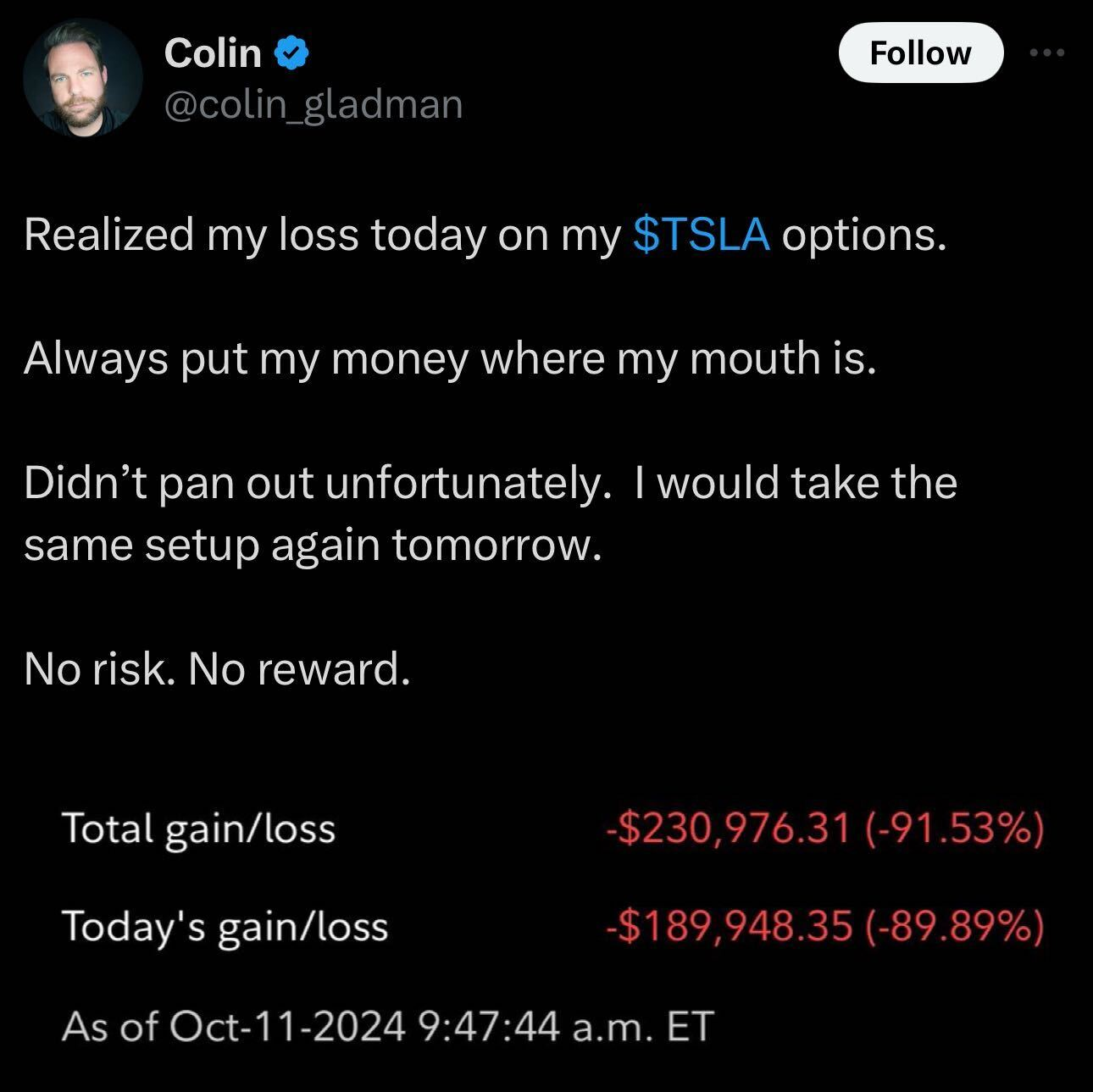

This guy lost a fortune betting on Tesla call options.

Don’t be that guy.

Learn from the mistakes of others.

At the markets current valuation, there are opportunities, however it’s not like last year.

We’ve had a stong rally that roughly matches in price gains and time what we saw in 2021.

The market is hyper accelerated. It’s not the time for complacency or doing yolo call option trades on a stock with an 80x forward PE ratio.

The market is hyper accelerated. It’s not the time for complacency or doing yolo call option trades on a stock with an 80x forward PE ratio.

Our strong view: The top for Tesla is in for the year.

Healthcare

We noted a few weeks ago healthcare was on sale.

We bought Elevance. We subsequently tax loss harvested the name.

We still love the name - but if the stock is not behaving like we expect after purchase and it hits a stop - better to get out.

Maybe there is some institution selling. Who knows.

You can get back to even on an 8% loss with a 9% gain. If you lose 20%, you need a 25% gain.

Tax loss harvesting is great risk management.

We still like the healthcare thesis. We believe people should overweight this sector.

This week we bought sleep apnea leader ResMed and Regeneron and Amgen.

Resmed is the dominant market leader. The stock was pressured on concerns that GLP1s would diminish demand for Sleep Apnea treatment.

That’s simply not the case in our interviews with various doctors.

I even signed up for an APAP machine (automatic pressure pump) from ResMed to try it out. In the infinite wisdom of our healthcare system, I was able to get the device despite not qualifying for Sleep Apnea.

I gotta say, it does help though and it’s part of our sleep practice.

We also bought Regeneron and Amgen.

Both firms are embroiled in a legal dispute with one another over certain IP.

We like them both due to their earnings growth and can diversify the idiosyncratic risk from their legal dispute - one will go up, one will go down - and we own the overall trend.

Here’s Regeneron.

The company is delivering double digit earnings growth. And the technical entry is beautiful vs. the other healthcare names.

Now, we could get a washout slightly below the 200 DMA. Reward vs. Risk is quite favorable.

Here’s a quick look at Amgen.

In the interest of time, we’re unable to do a deep dive on each of these.

The risk is that healthcare hasn’t quite bottomed. That’s possible. As recession fears wane, the bid for defensives could subside.

Mr. Market has a decision to make whether to lift these from here, or churn a bit more.

I’d suggest 65% odds we move higher. We don’t have a sizeable dislocation here with a clear bottoming process so this is a harder call.

AI

Deepmind Founder Wins a Nobel Prize

Video Link: https://www.youtube.com/watch?v=SdxOouXsaxc

AI analyst Dario Amodei says hen AGI arrives it will be smarter than Nobel Prize winners, will run millions of instances of itself at 10-100x human speed (possible on the clusters of 2027) and can be summarized as a "country of geniuses in a data center".

Dario Amodei says AGI - what he calls powerful AI - could come as early as 2026 and it is possible that 1000 years of progress could happen in the 5-10 years following.

Digital Assets

Bitcoin Turbulence

Per Jason Goephert, Bitcoin tends to lull traders to sleep and then frighten them into extreme action.

Its 6-month trend strength has been this low 4 times in its history.

Get ready for some fireworks.

Our expectation is that if Trump wins, the ETH / BTC ratio will rally dramatically. We might get a blow-off top at the end of Q4.

If Candidate Harris wins, there could be a flush followed by a rally. We are hearing from our network that one of the SEC Chair candidates is a former operator of a digital asset company.

That news is not priced in.

The move might be two have two laptops - one with a buy button, one with a sell button.

Reminder: There are powerful strategies to mitigate capital gains taxes. They give you liquidity, control, and transparency.

But, these strategies require ‘activating’ before year-end so you can get as much benefit as possible. They need time to work.

One strategy - if you put in $1 MM on Day 1, then on Day 365 - on average - one ca

Reach out to [email protected] for more.

As Featured In