Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Macro: Strong Dollar Wrecking Ball; Time For Brazil, LNG?

Markets: NVDA Correction; Energy Rotation; Tech Overvalued?

Company Earnings: Cloud & Semiconductors’ Continued Growth

AI: End of Analysts - AI beats Wall Street?

Digital Assets: BTC vs NVDA Momentum; Tokenize Celebrities

This week, we were at the Coinbase State of the Crypto Event.

A lot of suits: Pensions, Endowments, Brokerages, Asset Managers, Banks, etc were in attendance.

Brian Armstrong (CEO) made an excellent case for using digital assets to eliminate intermediaries.

This post from our friend Yano at BlockWorks is an excellent summary.

Macro

The CPI came in a bit cooler than expected.

Recall the first quarter, there was a string of hot CPI prints. Each time, markets sold off.

Then, in May, there was a weaker CPI print. Markets have been rallying strong since then.

At the same time, central banks globally are starting to ease - Canada and Europe.

That combination makes for a strong dollar. Take a look at DXY:

Note: The red lines in the chart are “risk off” regimes. The green lines are “risk on.”

Trends in the USD have been an incredible explanatory variable for risk.

If you squint more recently, you can see the USD is breaking out.

We believe the strength in the USD is having a “wrecking ball” effect on commodities, commodity producers, and emerging markets.

Take a look at Brazil (EWZ). Brazil is a major oil commodity exporter - we used to own their leading company, Petrobras (PBR), which was a great investment:

Brazil is back to October 2023 lows.

It’s getting close to a capitulatory stage. We still think it’s a bit too early to venture into Brazil. But we could be weeks away.

There are stocks in Brazil that increasingly are attractively priced. (No, not Mercado Libre—a fantastic business—the Amazon of Brazil—but, remarkably, almost as expensive as Nvidia.)

We have identified the stock to own in Brazil. We'll write about our buy decision if we see a capitulation in the coming days or weeks.

Here is the stock we are tracking:

The entry is looking pretty good. We might be early or right on time. We suggest a partial position. Then, wait for more data. We’ll keep you posted on Brazil.

Brazil is one of the few countries in the world with a strong demographic story. It also has the best capital market in Latin America, and credible banks like BTG Pactual are there.

And there are multiple success stories such as Nu Bank, Mercado Libre, Stone, and a few others.

Mexico is another country that is on sale. This is due to both the strong dollar and recent elections, which give the leader, a leftist, strong control over the economy.

We have yet to see policies that look anti-market. There is a lot of anti-capitalist talk.

On Mexico, India & Uranium:

Mexico and India were the two strongest stock markets globally after the United States.

We take notice of Mexico because the country does have strong secular trends behind it - not least of which is the ‘near shoring’ phenomenon.

Mexico, sadly, has been marred with terrible gang violence, which has led to the assassination of dozens of political candidates. The market was largely sideways during the political season.

The main question for investors is: will earnings and multiples go up?

We believe the answer to earnings is Yes.

We don’t currently have positions in these markets, but we did want to call out the effect of a strong US dollar on international equities.

The strong US dollar also pressures commodities.

A strong US dollar means everything you can buy for dollars is cheaper - including commodities.

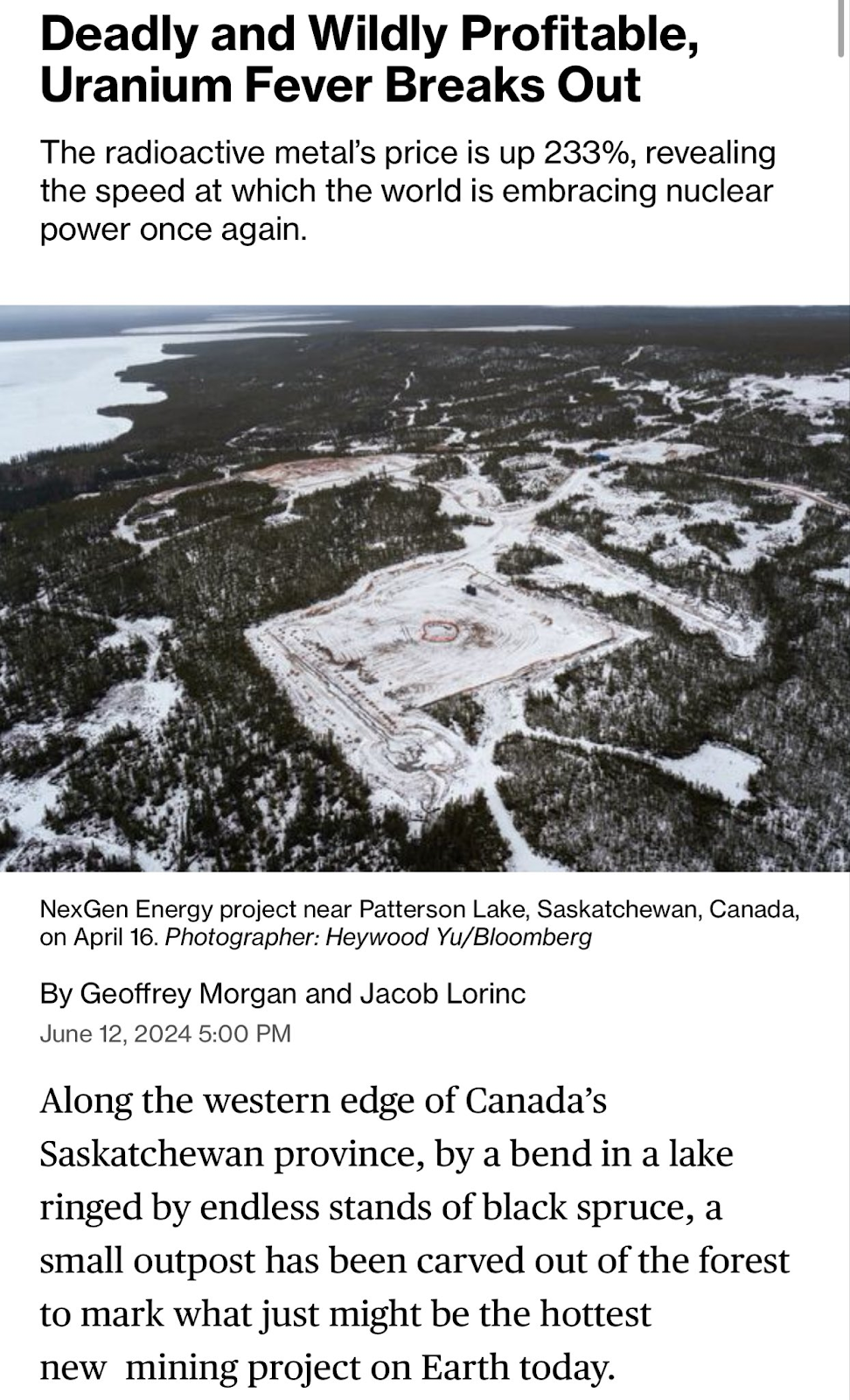

Take a look at Uranium:

Despite this article in Bloomberg about nuclear renaissance and uranium, which is one of our investment themes, we don't think the Uranium selling is done yet.

Take a look at this excerpt.

Notably, since the beginning of this year, Goldman has started talking about Uranium and also slapped buy ratings on Canadian miner CCJ.

So, our thesis on uranium is broadening. We cut our exposure to Uranium spot commodity when we saw the technical breakdowns taking place a few weeks ago. We didn’t expect it to reach these levels, but here we are.

We like commodities because they are a natural inflation hedge. And the ratio of commodities to equities is near multi-decade lows.

Governments have a tremendous amount of sovereign debt. That debt will not be paid back in 2024 dollars. The debt will be paid back in 2048 dollars (just making up a year). And those dollars will be worth less than they are today.

This is why we like real assets - equities, (distressed) real estate, and commodities. If inflation is higher for longer in the 3%-ish range for a while - your purchasing power is not at risk.

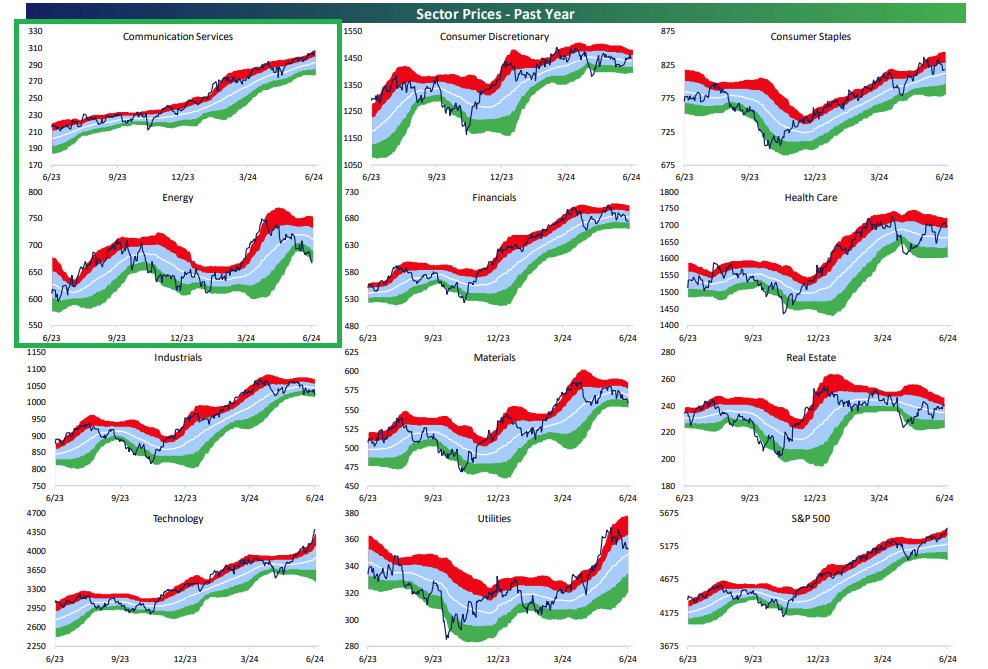

Take a look at Energy. This is the ETF XLE - the two largest holdings are Exxon and Chevron.

We believe now and the coming weeks are a good time to own energy ideas.

Note: The seasonality for energy will be negative for the next several weeks. You want to have exposure before September.

If stocks are weak, energy stocks act as a nice, negatively correlated, positive expectation asset. During the equity sell-off last year, energy stocks rallied.

The inverse is happening now. Indices are hitting ATH, and energy is selling off.

It’s a good idea to ‘rotate’ and acquire energy assets when they are finally now ‘on sale’.

Indeed, Energy is the only sector that is now extremely oversold.

Consumer Discretionary and software are oversold, but the multiples are not that cheap.

Lululemon, which continues to correct, has a forward PE of 21x. That’s not exactly a bargain.

There’s a difference between a great business and a great stock.

We highlight Communication Services above. That category includes Google and Meta. We still recommend an overweight on those names as we expect greater earnings revisions.

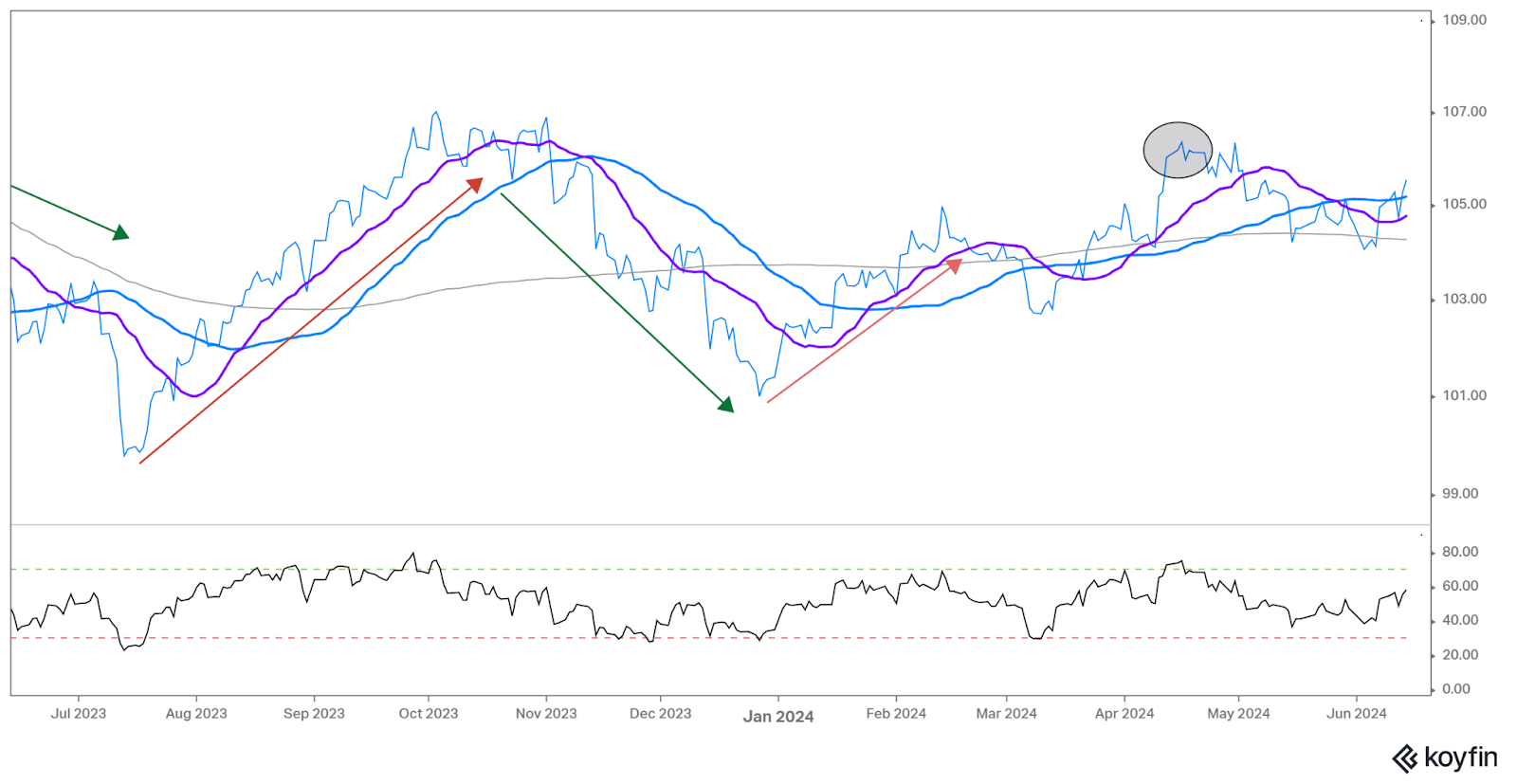

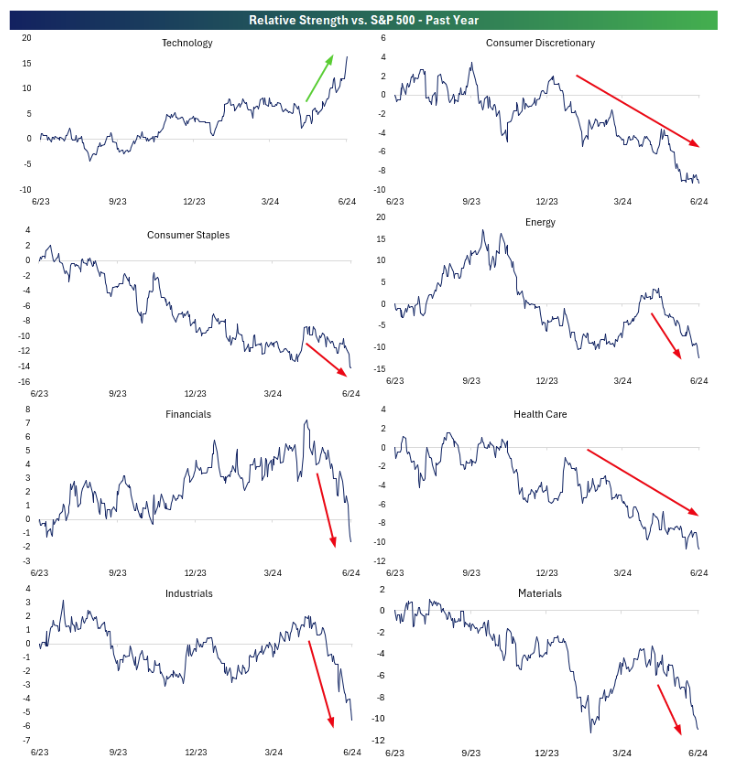

Here’s another look at what’s happening in the markets:

Simply put, this is the Nvidia Correction hypothesis in Action.

We wrote on May 28th, around Nvidia’s earnings, that investors are waking up and deciding to sell what they own and buy Nvidia.

Nvidia is sucking the oxygen out of the room.

Notice again, how nearly every sector in the S&P is hurting... except Tech.

That's the Nvidia correction hypothesis in action.

Your LULU stock is down because the owner decided to buy NVDA.

Your SNOW stock is down because the owner decided to buy NVDA.

Take a look at the attached chart.

I thought this phenomenon would be primarily limited to Tech...

But it's not. Every sector is impacted.

Even internationally, European indices are flat.

I believe the "AI story," with NVDA as the leader, is causing the weak breadth stats.

When does it end?

When NVDA re-rating is done.

Then, paradoxically, we'll see breadth expand.

This was a good Lumida Wealth call, and it's a phenomenon people still need to connect the dots about.

That said, I am surprised by how powerful this effect is.

If you told me every sector would be down red and Nvidia and AI friends are sucking the oxygen out of the room at this level, I wouldn't have believed it.

The tendency for markets to overshoot, despite our knowledge and lived experience of that, still never ceases to amaze me.

What’s Next?

We’ve seen any sector adjacent to AI have a strong rally.

Datacenters have lit up liquid cooling and utilities. Remember our stock call Talen Energy (TLNE) from February? It’s up 50% in three months.

We sold it because we think it is fully valued. However, it could very well continue to run from here, especially with the stock buybacks they have now.

Here’s the next theme in our view…

Utilities like Constellation Energy, VRT, and Talen have run-up due to the massive energy needs of data centers.

But, utilities themselves need energy as an input.

Those inputs range from oil, coal, natural gas and wind / renewables.

Wind and renewables are coming online too slow, and are unreliable (e.g., cloud cover, etc.). The next 3 to 5 years require a transitional energy source.

We believe that will be Liquid Natural Gas.

Natural gas is a cleaner energy source than oil and coal. Also, China and India are ramping up natural gas imports and re-fabbing factories to consume this form of energy.

Europeans also import liquid natural gas from the United States since they can no longer rely on Russia.

Liquid Natural Gas had a strong run-up after the Russian invasion of Ukraine. It’s pulled back.

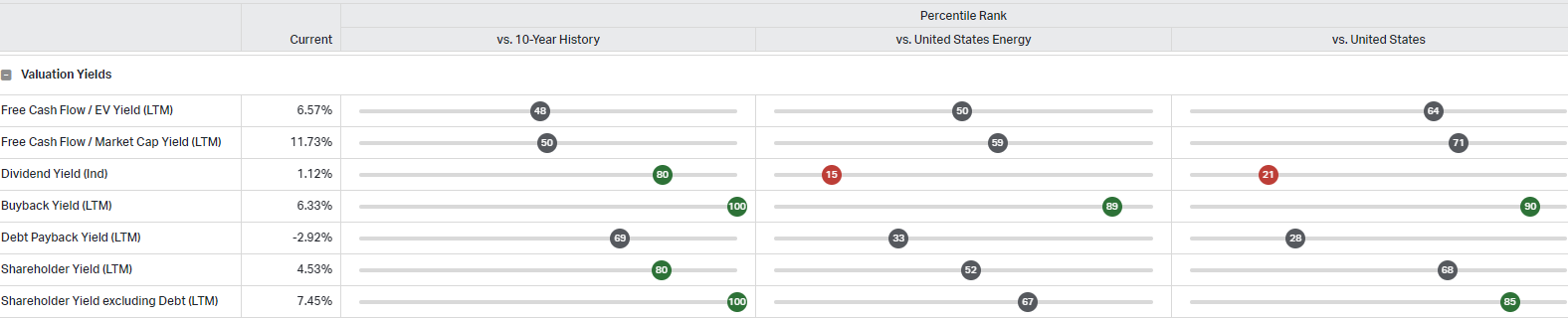

We believe the way to bet on it is through the market leader, which goes by Chenerie Energy (Ticker: LNG).

Chenerie (LNG) is the only large cap pure play bet on natural gas exports. LNG also has a strong moat. They are the largest LNG producer in the United States.

They reported $1.8 Bn in Q1 ‘24 with free cash flow of $1.2 Bn.

They reaffirmed full-year guidance for FY 2024 and expect distributable free cash flow to exceed $2.9 billion. The stock has a market cap of $35 billion.

The stock has a strong buyback yield relative to itself and its peer group.

We believe in 3 to 5 years, this name will do well.

It also will come with a lot of volatility, as the market doesn’t understand the hedging of their contracts.

The downside is if competitors produce an oversupply of natural gas or demand is softer due to strong Solar.

We like quite a few names in energy. This is just one. To put position sizing in perspective, we will initially allocate a sub-5% weight to this across accounts.

Chenerie Energy meets the definition of a classic internal compounder.

If markets realize Datacenters can benefit from liquid natural gas, then in the same way boring utilities rallied on the AI theme, so can LNG.

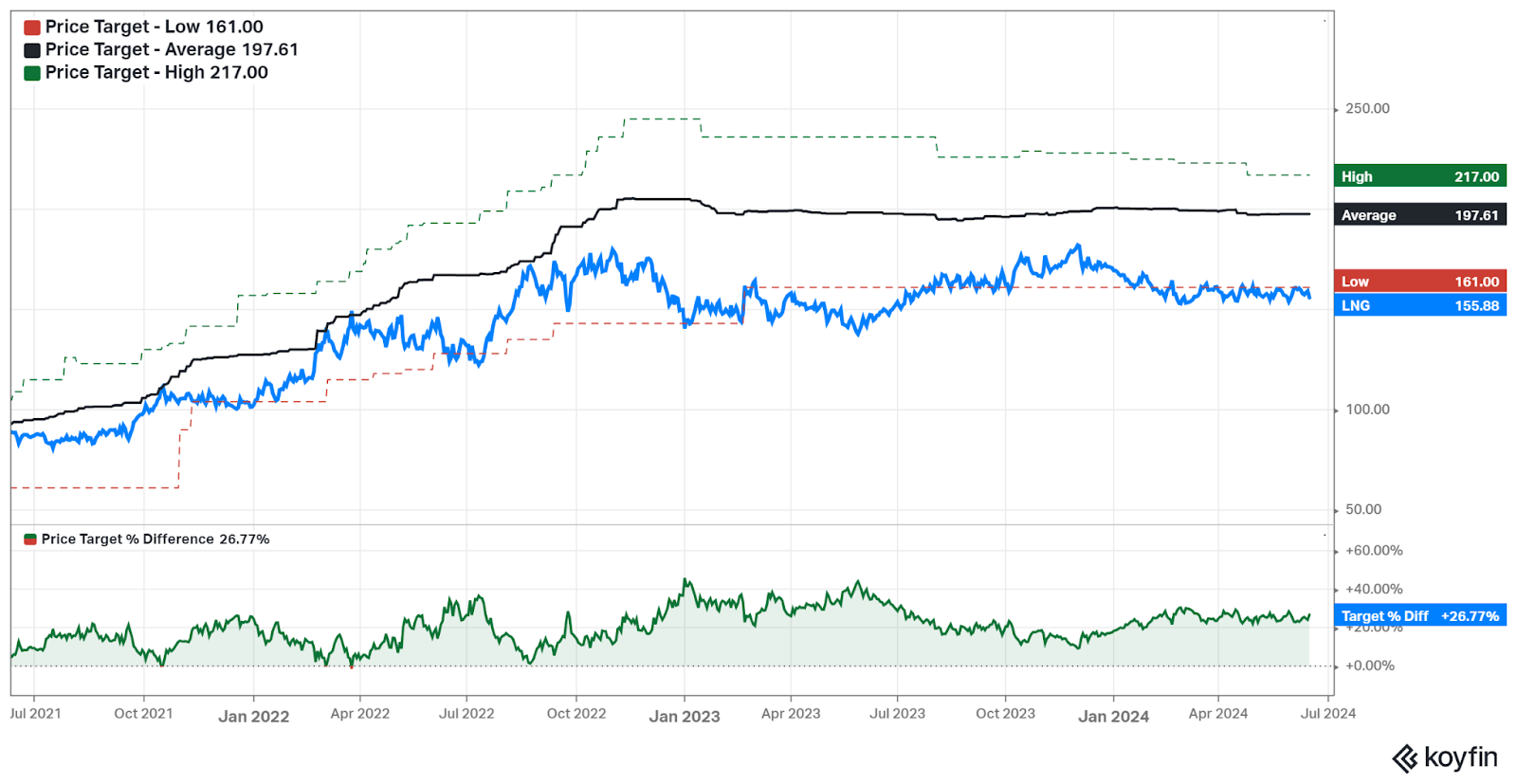

Price targets across the street

The company has contracts that go out for quite a few years for forward revenue.

They have contracts that protect them from natural gas's downside prices, but they can also benefit from the upside.

Crucially, the firm is engaging in strong buybacks and paying down debt on a 1:1 basis.

The median analyst average price target is $197, about a 25% return from here.

We have been teasing this idea on Twitter the last few days. Then BAML came out with a research report on LNG yesterday. So, figure we’ll give up the ghost on this idea.

We think the entry for LNG now is excellent. Here’s the chart:

Explore becoming a Lumida Wealth client: Click here to fill out our form and schedule a call.

Markets

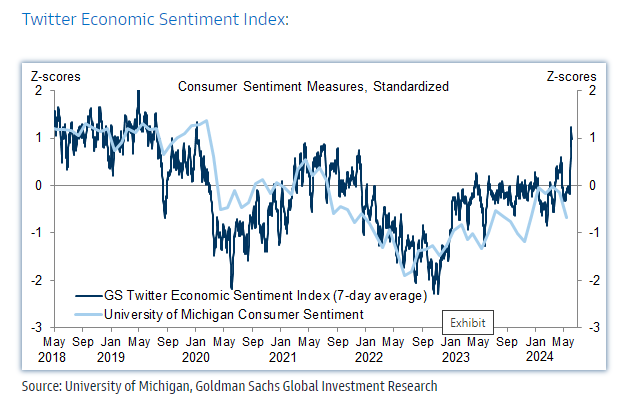

Goldman's Twitter Sentiment Index is right near the highest level since early 2020.

Generally, you want to buy when Twitter sentiment is low. Notice the lows below correspond to ideal buying opportunities. You don’t want to FOMO when Twitter sentiment is high.

Twitter is dumb money, present company excluded :)

This tells us everyone is buying Nvidia.

If you’ve followed along, you know we’ve been long Nvidia, Meta, and Google and enjoyed the ride.

The hard part now is for new accounts. Lumida is growing quickly… We don’t like chasing Nvidia here. We are buying Meta and Google.

If there is a summer correction, we will buy Nvidia there. We are now buying ‘rentals’ or proxies for the AI theme.

If you are looking for a wealth management partner, Lumida is now welcoming a limited number of new clients.We offer a range of services, alternative investments (such as our CoreWeave deal), white-glove crypto management, to public equity management, and high-touch family office services, including trust, tax, and estate planning.

Ready to explore? Click here to fill out our form to start the discovery process.

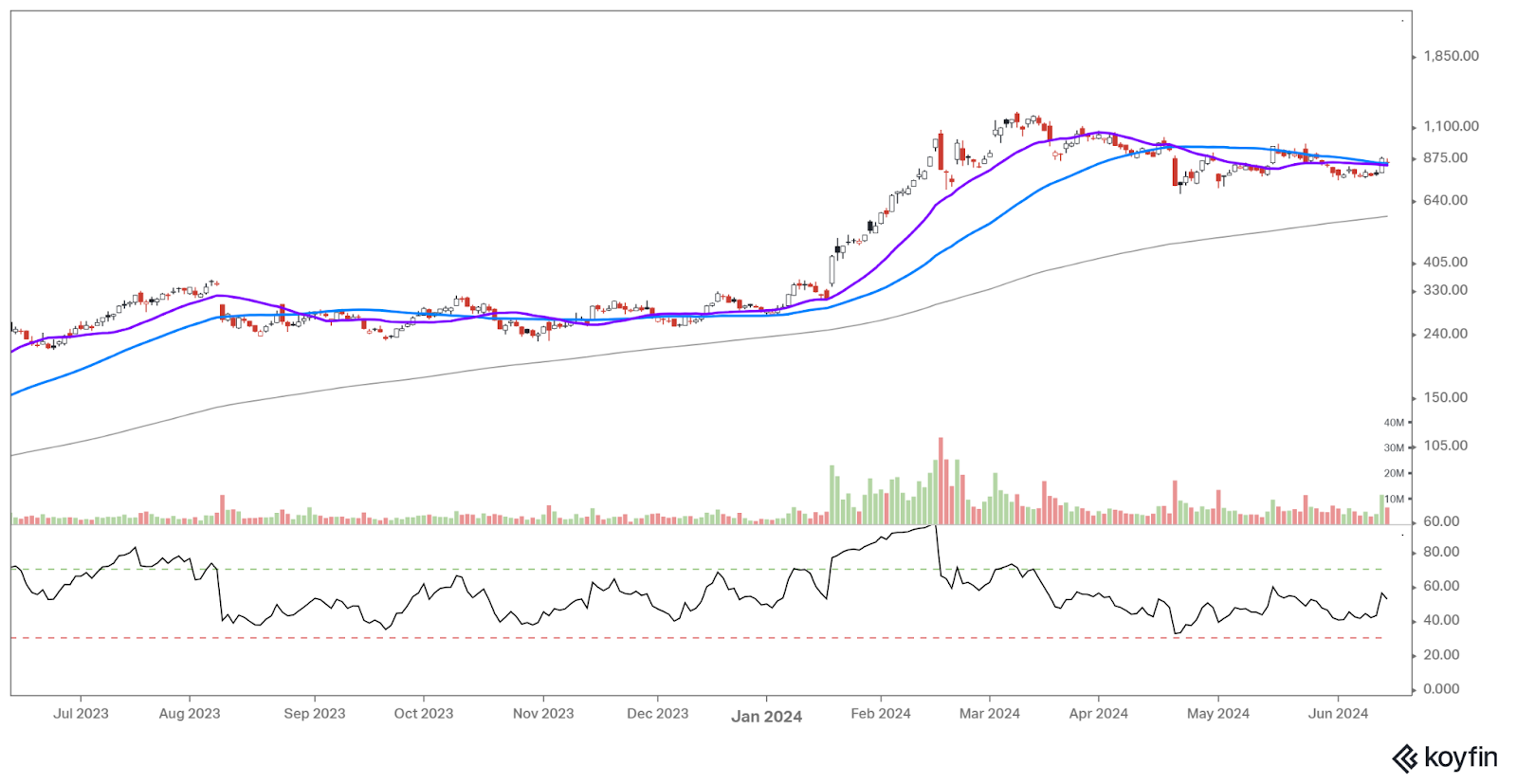

Interested but not ready to commit? Build a relationship with Lumida and stay informed. Click on the poll below if you want our advisors to reach out.Our NVIDA Rental: SMCI

I switched from team DELL to team SMCI.

Why do we prefer SMCI over Dell?

1) Earnings revisions for SMCI are up, and yet the price has been flat for the last few months.

No other major semi is doing the same.

In fact, since the Apr 19th lows, 2/3+ of the semiconductor rally is multiple expansion and 1/3 is earnings revision.

2) Dell has a 0% margin on AI servers.

SMCI makes mid-teens margins.

3) SMCI has liquid cooling and is already configured for the latest NVDA Blackwell platform.

4) SMCI is a smaller, more focused pure play on GPU compute than Dell.

5) Michael Dell is selling $2 Bn+ of his stock for the same reason we did — it’s fully valued.

6) Like Dell, SMCI also has a partnership with NVDA.

(Dell has a longer history with Nvidia and is a core distribution partner for the enterprise.)

SMCI is a ‘catch-up’ trade for those who missed the NVDA, META, GOOG, and TSMC because they were not reading our newsletter.

The day after SMCI rallied 9%. There’s now talk about SMCI joining one of the major indices.

We think our analysis is correct, but the timing was pretty good too.

Here’s a chart of SMCI.

It’s a Boomer Economy

Thought Experiment:

Suppose BlackRock’s CIO Ric Reider is right.

His idea is that Boomers have more free cashflow due to the trillions in Treasuries that are throwing off high coupon - more than ever.

His argument is that higher rates are helping Boomers.

Higher rates might hurt CRE and commodities, but they may support US consumers' (boomer) spending on services.

We believe rates are higher for longer.

Powell said on Wednesday they are kicking out the timing of various rate cuts to next year.

So Boomers keep spending (due to higher treasury yields).

That keeps inflation on a slow glide path.

Now, the Fed believes they are ‘restrictive’.

The Fed does not believe high rates drive spending. (Meanwhile, cruise stocks and restaurants are near ATHs…)

The Fed doesn’t believe Ric’s argument.

Play it out.

Rates are higher for longer.

So Boomers keep spending their Treasury bill coupon.

So inflation stays higher for longer.

So policy stays ‘restrictive’ for longer…

So Boomers keep spending their Treasury bill coupon…

Consider the following.

This cycle is unlike any we have seen.

The leading indicators are down , yield curve inverted, bank credit stalled, loan officers are tight.

All these once reliable predictors of recession failed.

The conventional models may not be helpful.

We have an income led boom rather than a credit boom.

Stay mentally flexible.

We may need new mental models.

Energy

THE ROTATION: ENERGY

The move to make in Jan was semiconductors capex receiver thesis, energy services, staples.

Now is the time to buy Energy more generally…

We recently bought Marathon Petroleum MPC.

Why:

1) China's recovery, and global rate cuts, creates a bid for energy;

2) The SPR is re-filling at these levels;

3) EV demand low, ICE demand high;

4) Oversold and stabilizing, due for a bounce;

5) Strong cashflows and buybacks abound if you know where to look; and

6) Diversifier for tech (negative correlation).

Why MPC?

1) As a refiner, with oil at these levels, I don’t mind exposure to the oil prices;

2) MPC trailing PE is 8.6x;

3) Cashcow - MPC will generate about $7.3 Bn in free cashflow on a $66 Bn market cap.

Do the math!

Ok, here’s the math:

11.6% yield; and

4) BUYBACKS.

MPC has authorized $8 Bn in buybacks.

That’s 10%+ of the float evaporating.

You own more of the stock over time.

There’s a natural bid;

5) Return on Equity of 25%. (Buffett’s rule is 20%)

Can energy do well?

Sure.

MPC has delivered 57% in the last 12 months; and

6) Last but not least… it has a good entry

Note: There are even better names in energy…

Energy services is still working.

We also own a driller based in the Permian Basin.

That basin bas the lowest cost-per-barrel drill costs in United States.

It is gearing up to the change in oil prices.

Will write about that small cap later.

Marathon Petroleum is a solid blue chip refiner - and a true internal compounder.

And it appears to have an excellent entry.

Marathon is a leading American refiner. It does, therefore, have exposure to energy prices. But with energy prices where they are, that’s exposure we don’t mind having.

Marathon has a 17% buyback yield. Their free cashflow as a % of market cap is 15%

Assuming no multiple expansion, that’s a good expected return assumption. We believe the stock will benefit from re-rating as well as energy prices recover. So you get the double benefit.

That’s exactly the kind of opportunities Lumida Wealth looks for. How many times do you hear us talking about multiple expansion.

The price to free cashflow ratio is 6.3x.

Consider that Nvidia’s market cap is enough to buy all the energy companies in the world. Maybe the rubber band has gone too far? Maybe not? Energy looks like a good idea to us.

Again, the seasonality is off for a month or so. It’s hard to line it all up perfectly.

Further, I prefer MPC over XLE where you get stuck with big giant oil companies like Exxon or Shell that I have no interest in owning and don’t grow as quickly or have less buyback yield.

GS is also “pumping” the oil story

Fortunately we bought this week and some time last week.

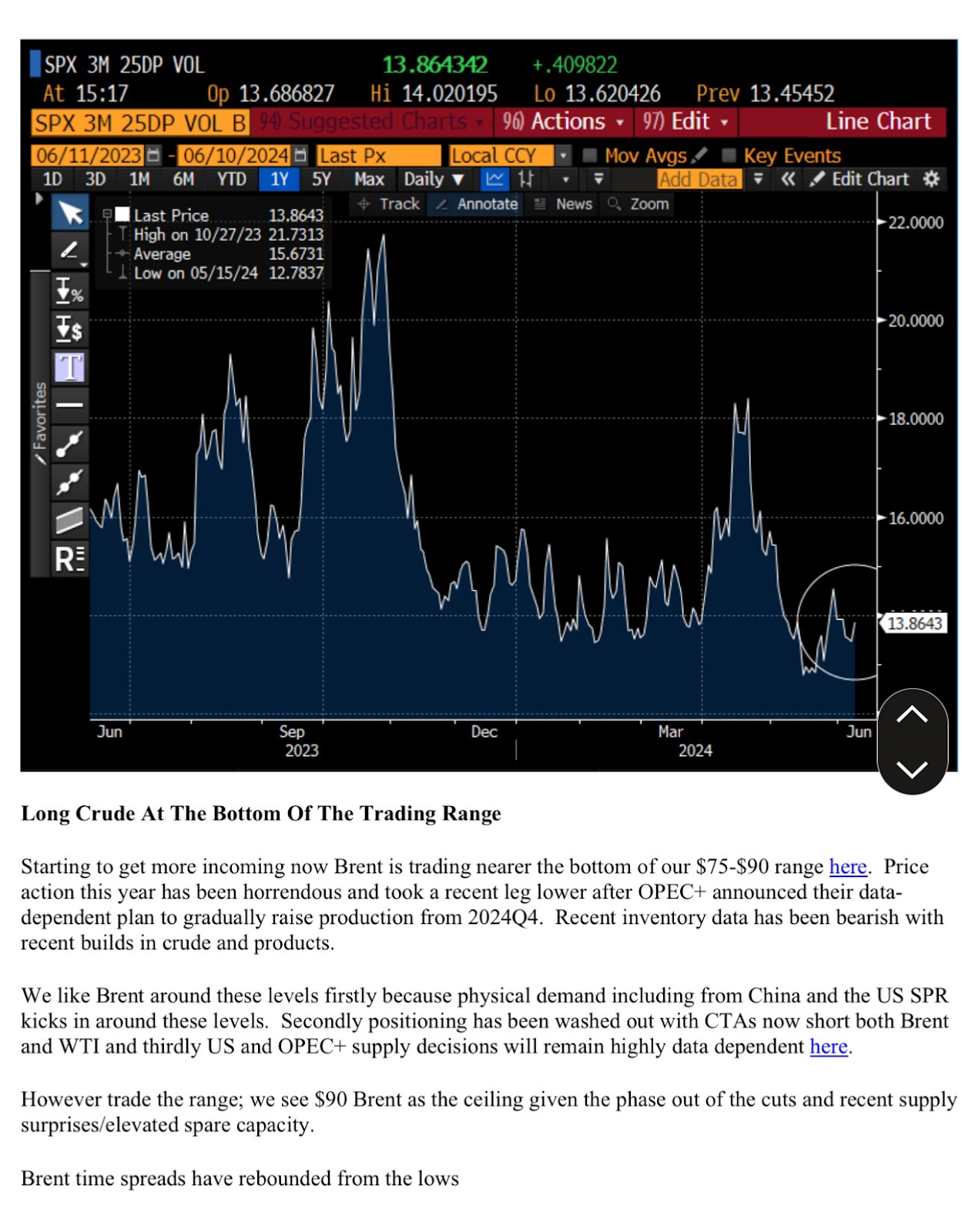

“Long crude at the bottom of the trading range”

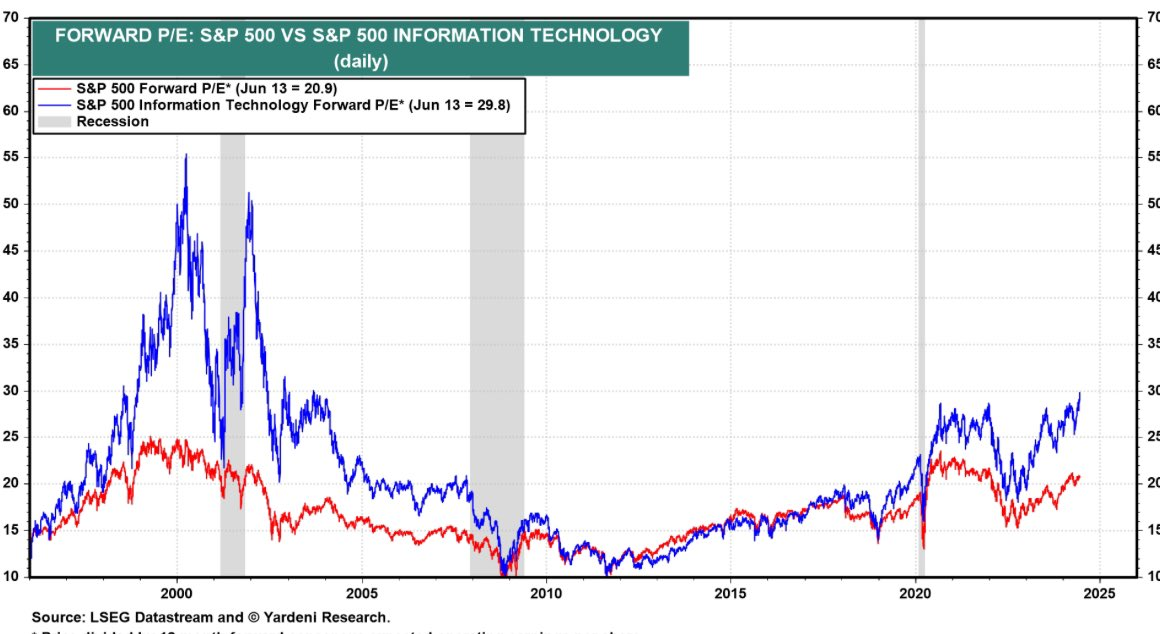

The Forward PE for tech stocks is now higher than 2021.

That’s a yellow light.

Why not a red light?

Earnings growth potential is higher.

In Dec ‘21, the last wave of stimulus checks were sent out.

Today, we have Chips Act, IRA, immigration, etc.

That said, the bar for execution is much higher.

Non-Consensus Investing is powerful but requires a contrarian psychology.

You are counter-cyclical.

You are buying when assets are overlooked and out of favor.

And when things get expensive, you can take your marbles and go home.

I look around now…

I don’t feel like many games are worth risking my marbles.

That said, when rate cuts come into view, we will see an extraordinary rally…

If the Fed had cut by now, S&P would be at 6,000+ already.

Between now and rate cuts, don’t lose your marbles.

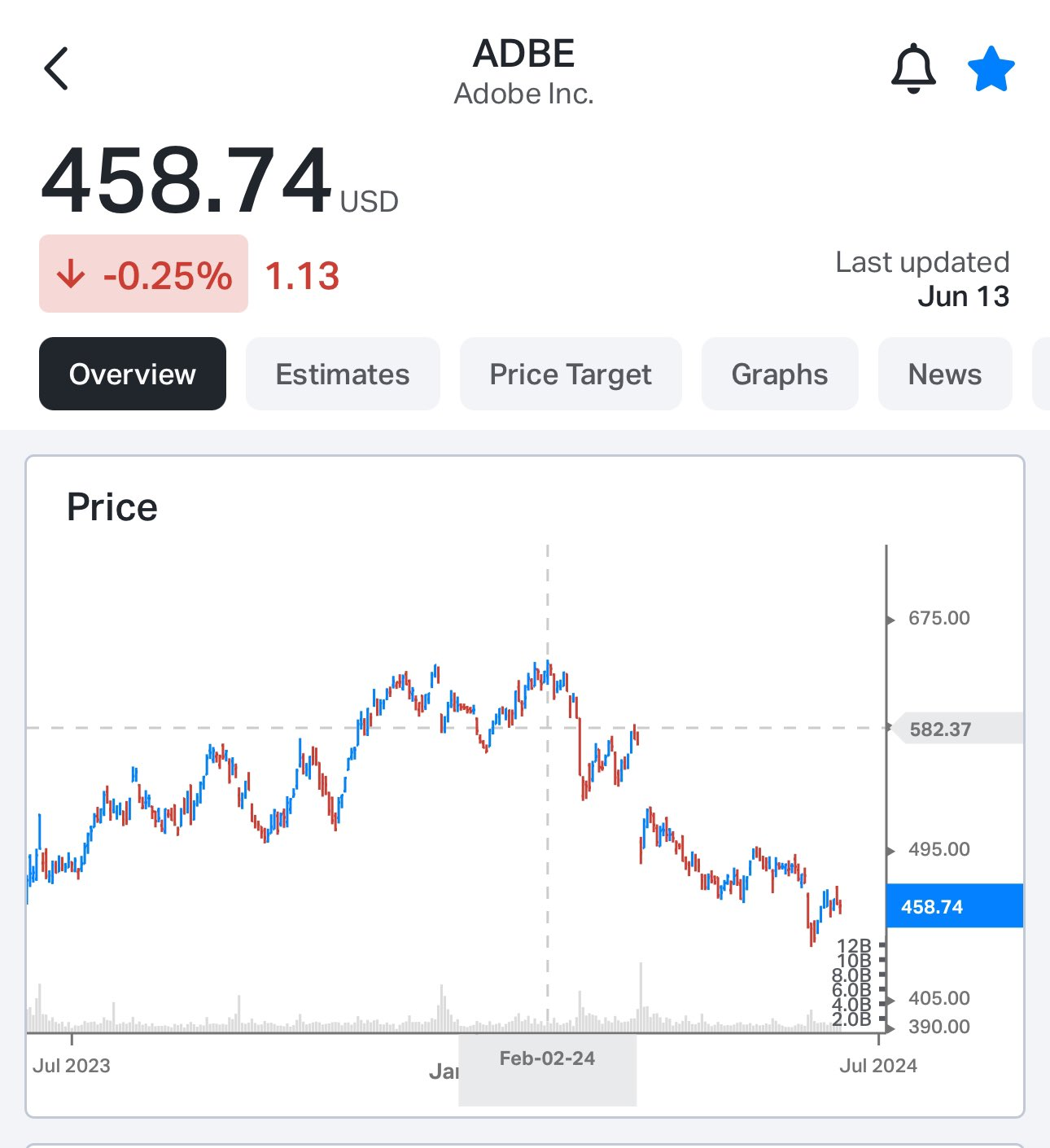

Adobe is down 36% from its high

I wrote this post about the mistakes I made.

Namely I had expected: ADBE, AFRM, and CRM to decline.

It turns out all of them were actually correct in hindsight of this post, they just needed more tim.

Interesting lesson there.

Company Earnings

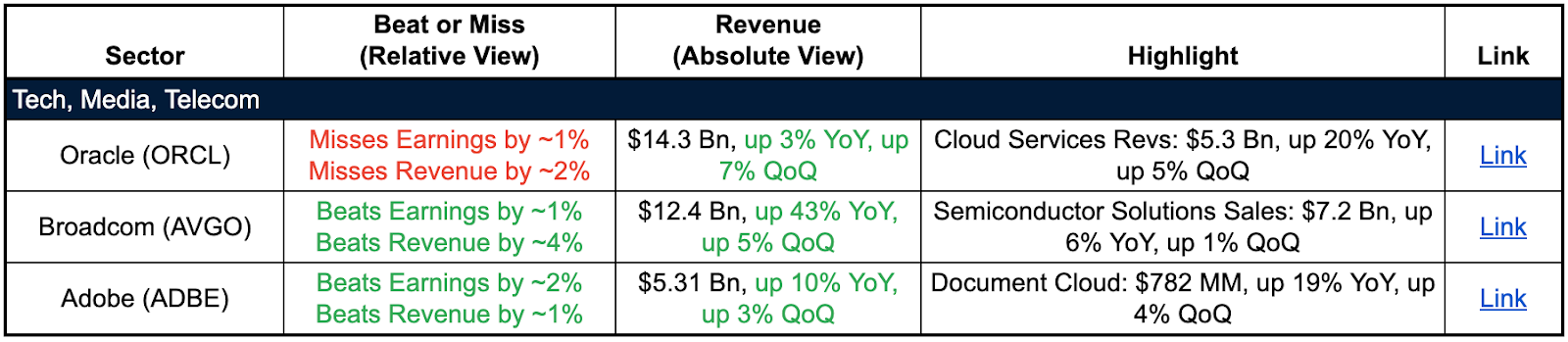

Tech Sector:

Cloud Growth: Oracle missed earnings and revenue targets, but cloud services revenue grew, indicating a potential shift in focus but challenges in meeting overall targets.

Strong Semiconductor Demand: Broadcom's strong revenue growth suggests continued high demand in the semiconductor industry.

Sustained Growth in Document Cloud: Adobe's performance highlights ongoing strength in the document management software market.

AI

A great read from our friends at Chips Ahoy:

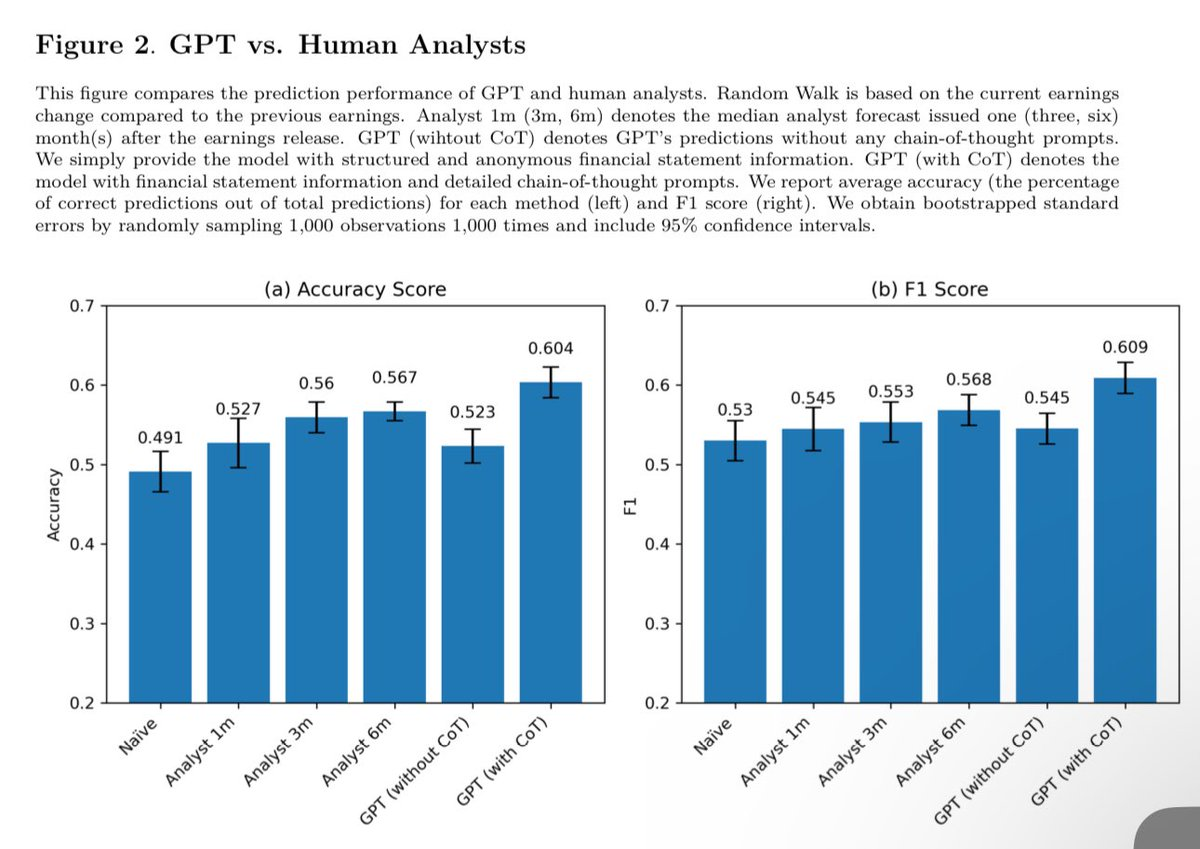

University of Chicago published a paper of a study comparing the accuracy of financial estimates & stock picking performance of Equity Analysts vs Large Language Models (PDF Link in thread)

The conclusion is at first shocking as the study shows LLMs are better than Human Analysts even with no industry background/context (shown in first image). However the paper does show that Human Analysts often have qualitative and broader context that can help inform estimates in a better way, & that GPT needs to have the right prompts to get usable results.

Overall, it’s a very interesting paper that broadly opens the debate of AI's impact on Equity Research and the investment industry.

Key Points :

“We provide standardized and anonymous financial statements to GPT and instruct the model to analyze them to determine the direction of future earnings.”

“Even without any narrative or industry-specific information, the LLM outperforms financial analysts in its ability to predict earnings changes. The LLM exhibits a relative advantage over human analysts in situations when the analysts tend to struggle.”

“We find that the analysts…3 & 6 month ahead forecasts achieve a meaningfully higher accuracy of 56% and 57% respectively, which is intuitive given that they incorporate more timely information.

“A "simple" non-CoT prompt GPT-based forecast achieves a performance of 52%, which is lower compared to the analyst benchmarks, which is in line with our prior. However, when we use the chain of thought prompt to emulate human reasoning, we find that GPT achieves an accuracy of 60%, which is remarkably higher than that achieved by the analysts.”

“Furthermore, we find that the prediction accuracy of the LLM is on par with the performance of a narrowly trained state-of-the-art ML model. LLM prediction does not stem from its training memory. Instead, the LLM generates useful narrative insights about a company's future performance.”

“Lastly, our trading strategies based on GPT's predictions yield a higher Sharpe ratio and alphas than strategies based on other models. Our results suggest that LLMs may take a central role in decision-making.”

Digital Assets

WHY THIS CRYPTO CYCLE IS DIFFERENT

Nvidia.

Come again?

Here’s why:

1) Crypto is a momentum asset.

Like any other commodity, the parabolas get going with a dynamic fueled by new inflows and scarcity perception.

2) Enter Nvidia

Nvidia is the strongest momentum asset.

Nvidia occupies Attention.

Momentum assets feed off of Attention.

In 2021, Bitcoin had Attention.

You had Elon Musk accepting Bitcoin on Tesla.

Cathie Wood was having a good year.

Coinbase just went public.

DeFi narrative was a powerful narrative (and it still should be but for the SEC…)

Nvidia and the AI theme owns the dominant zeitgeist.

In Q4 ‘23, Nvidia prices were relatively muted.

The Bitcoin ETF occupied Attention.

3) The Cause and Effect

Fast money capital that would ordinarily flow into crypto is going into Nvidia.

Remember Gamestop in Feb 2021?

That was the GME retail rally…

Bitcoin was down that month.

Why?

The attention was on GME.

4) What’s the Fix?

The prize is Cultural Relevance.

How? Fix policy.

Update Reg CF and securities laws to permit Tokenization.

That means permitting property rights and royalty streams in creator content.

This expands reach to new circles of capital.

Tokenize Celebrity.

Tokenize the next Taylor Swift that can’t break through the studios.

Let fans earn royalty streams for betting on artists.

Tap into the ‘Rich men from Richmond’ vibe.

The starting point is creators on apps like TikTok, YT, or Instagram who have no property rights in their creative works and earn a small fraction of their value creation.

It’s a big chicken and egg problem.

Overcoming the cold start problem starts with a 1) creator with a large non-crypto following, 2) wants to shake the status quo, 3) in Music, Hollywood, or…Politics

5) Other factors:

Need a commodity rally.

Notice oil, uranium, and gold are weak.

Bitcoin is the leading crypto asset, and it acts like a commodity.

Commodities are soft on a weak CPI print.

The Fed keeps kicking out rate cuts, disappointing the inflation story that drives commodity prices.

If inflation springs back in a few months or if banks / CRE are in the headlines, the mojo will be back.

Wild Card: Does crypto enter as a Presidential Debate topic?

How will Trump respond if asked, ‘Do you own Bitcoin and why?’.

How does Biden respond?

Politics is another way of achieving Cultural Relevance.

Lumida is hiring

To that end, we are hiring a Business Operations leader / Chief of Staff who would work directly with Ram.

Check out the role, and please help us get the word out!

Curation of the Week

Check out this thread on why KKR, Apollo & Blackstone are calling this once-in-a-generation buying opportunity.

Quote of the Week

“Don't be afraid of the boom. Fear the bust. When the music stops, you don't want to be left holding the empty chair." - Charlie Munger

If you enjoy the Lumida Ledger, please forward, share it with a friend, and subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.