Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we’ll cover this week:

● AI: Microsoft, Google, Databricks

● Macro: The Economy

● Markets: Leadership Rotation

● Company Earnings: Travel & Leisure, Gaming, EVs

● Digital Assets: SBF, ETF Flows

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

This week we had a great conversation with Alex Kruger on Crypto, Macro and trading psychology.

Alex aka @KrugerMacro on twitter (150K+ followers) is an economist from Argentina turned crypto investor.

We talk about his non-consensus approach to analyzing global macro and crypto markets that helps him generate significant alpha.

We dive deep into macro and BTC, ETH, SOL, & meme coins.

Click to Tune in below:

Don’t forget to like, share and subscribe - your support helps us keep growing and booking amazing guests each episode.

Ram joined the Trends with Friends Podcast (Howard Lindzon, Phil Pearlman and J.C. Parets) for a lively discussion on hot topics and investment ideas. He even dives into the surprising growth potential of the "oldest of the oldest" demographic.

In case you missed our last episode on Non-Consensus VC with Dave Lambert here are the links below:

Dave’s typical fund has 600 deals. And their performance is top-decile. Better than what you would see at the ‘name brand’ VC funds.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

AI

Microsoft and OpenAI are working on plans for a data center project that could cost as much as $100 billion and include an artificial intelligence supercomputer called "Stargate" set to launch in 2028.

Stargate may be a reference to a TV series where there is a wormhole that opens up new worlds.

That’s also the same concept behind the ‘Singularity’. The metaphor of Stargate suggests that Microsoft and OpenAI want to build an AGI and we’ll see it in 4 to 5 years.

That lines up with our forecast last week after the Nvidia conference that we’ll see AGI capabilities in 5 years.

Stargate is also the kind of buzzword you want to gin up a good valuation and story for OpenAI which is increasingly beset with competition from Perplexity, Google Gemini, and new LLMs on the rise.

The main takeaway?

Stay focused on the semiconductor CapEx receiver thesis. It’s way too early to pick winners in the application layer - especially illiquid startups burning cash and competing with their parent companies (Both OpenAI and Microsoft are selling to Enterprise).

And… Nvidia is not a bubble.

This is one of the most telegraphed CapEx spend stories. You have multiple big tech firms and sovereigns chasing the promise of AI.

The spend on Datacenters, Compute, Hardware, semiconductors is so predictable.

The fact that Cathie Wood is calling Nvidia a bubble tells you that it is not a bubble.

Now, Nvidia had its first week pullback in weeks. So, we may finally seeing an opportunity for better entries before May’s earnings season.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

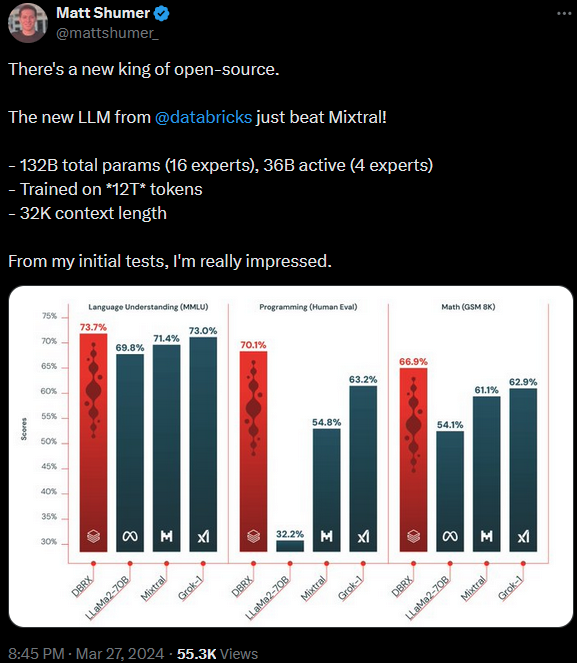

DataBricks Builds an LLM

DataBricks built an LLM that scores higher than leading open source AI models.

It’s inevitable that we’ll have GPT4 caliber open-source models running locally and in the enterprise.

A few observations:

1) Databricks is going to have a great IPO. Databricks is a leading cloud AI provider with a focus on data science. They compete with Snowflake.

Building an LLM today is like having a internet play in the DotCom era. You get a nice valuation bump.

Except LLMs cost more money - especially the build-from-scratch Foundation models like GPT or Meta’s Llama2.

Consider the power of doing data science on cloud with high-powered AI.

2) Will this inspire other vertical SAAS providers to follow suit and build their own LLM? (Yes.)

Other SAAS vertical startups to attempt to follow suit. Why? The market cap will benefit.

Now, the key is can they translate this to earnings. All we know for sure is capex spending is going up.

Adobe tried...but they are in a bind because it's cheaper to use Midjourney. Adobe is an innovator’s dilemma.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Is Your SAAS Investment AI Proof

One should not assume that building an LLM for a SAAS firm guarantees relevance.

There are many good reasons to expect that AI obviates the need for SAAS and will disrupt quite a few business models.

The internet disrupted newspapers, music, and book stores.

Do we need a travel booking site like Expedia, or Carta, or Salesforce with a high-powered LLM?

Here is a write-up on ‘The Bear Case for Adobe’ we wrote in September 2023. Adobe’s stock price is 10% lower since then despite a massive tech rally:

We also wrote about some of our favored names: Nvidia, TSM, ASML. Those are up 60 to 10%+ since then.

Note: Today, our optimal semiconductor allocation is somewhat different than what we have written before. Valuations have changed.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Scrub Your Portfolio

We encourage you to check your SAAS portfolio and test for two elements (i) AI disruption risk, and (ii) if your forward PE ratio is higher than Nvidia.

On the latter, there are quite a few companies that have valuations higher than Nvidia and are growing at a slower rate: Snowflake, Palantir, The TradeDesk and more. That doesn’t mean short them. It just means these should lag the performance of other ideas.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

What’s the Killer App for AI?

I want an LLM that can "see" and interact across my apps on desktop or mobile.

The LLM should be omni-present, accept voice commands, and perform actions across applications.

Everyone gets their own super-analyst that works lightning fast and error free.

They have my context (and yes, personal data) and can execute on complex workflows.

This type of app can be built at the Operating System (Microsoft / Apple) level, the Browser level (Google), or the App level (Meta).

It’s going to take several years and iteration to get there. The software is way behind the hardware.

Arguably there is no real need for specialized apps like spreadsheets and word processors the stronger AI gets.

The visual interface itself is simply a mode of experience that AIs will eventually generate based on the task at hand.

Today, Microsoft and Google are trying to win the battle for search.

So don’t get too excited about these powerful consumer and enterprise apps yet.

They have a long way to go.

But, consider that - it’s not just Search that is under attack. The operating system itself is open to attack.

What is the relevance of Windows in an AI-infused world?

The UX of how operating systems are designed, and the form factor (Raybans? Vision Pro?) needs a complete overhaul.

The competition in the next 5 years will be wild.

Bloomberg reports Amazon plans to spend $148 Bn on data centers over the next 15 years.

One of the ways to bet on AI is to break it down into subsectors.

The Application layer, in our view is over-rated.

Betting on Data Centers, like our bet on CoreWeave, makes a lot of sense.

Hardware Based Memory and Micron

Micron has been on a tear.

We believe there are better moves than Micron, although Micron has room to run. (We don’t own Micron, but we like the HBM theme).

HBM enables GPU to access memory registers at nearly the speed of light.

A new generation of AI PCs will start shipping in the coming years. (We need better software though).

The best HBM player in our view is SK Hynix - a South Korean firm. They have a better position than both Micron and Samsung.

It’s not easy to buy though - no ADRs.

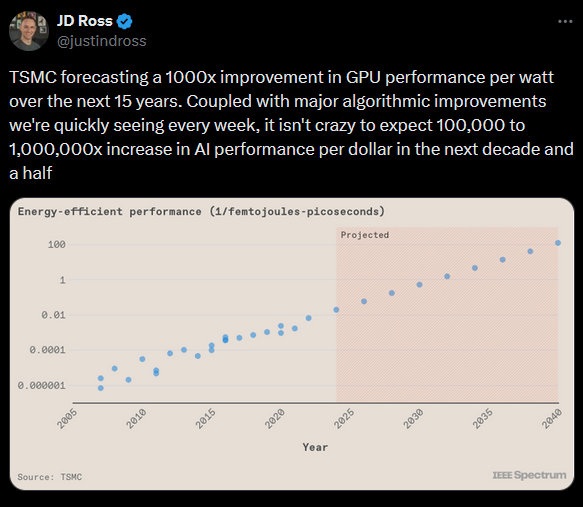

GPUs are Scaling Faster than Moore’s Law

TSMC is forecasting a 1000x improvement in GPU performance per watt over the next 15 years.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Macro

The economy is accelerating. GDP is strong. What’s not to like?

New orders are up. Manufacturing is ending its local recession.

This is more evidence for our hot landing thesis. Here’s a re-cap of our twitter post from October 2023:

The ‘Hot Landing’ Thesis:

The easy wins in inflation - repaired supply chains & declining shelter costs - are behind us.

Now these structural pressures remain:

- Re-shoring from China to Mexico/Vietnam/E. Europe/India increases industry cost structure

- Labor: UAW strikes and 20% wage hike demands are a symbol for wage pressure elsewhere

- Energy & Food: YTD records (almost $100 oil)

- Persistent Budget deficits

- Stimulus from Chips ACT & IRA

I’m not saying we are going to relive the 1970s.

However, the path to 2% gets harder the closer you get.

And 2% is the Fed target - they are not settling for 2.5%.

That means ‘higher for longer’ rates and inflation.

On China

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

What do you see in this chart of the FXI?

I see higher highs and higher lows. (The green line is where we called a capitulation.)

And, not all, but several economic data in China are improving.

People are biased negatively on China and ignoring good news.

Property prices continue to drop. And by several measures - they are still way over-valued.

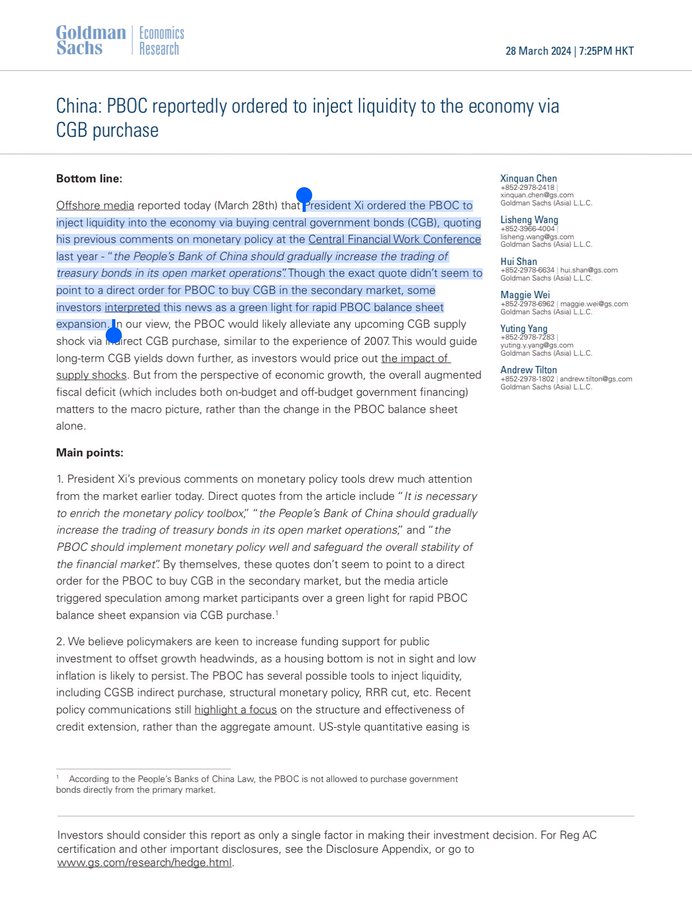

What’s new? Goldman Sachs is reporting on a rumor that China’s President wants to start QE.

What might be their objective?

China starting Quantitative Easing would lower mortgage rates.

This would allow the population to refinance and also improve affordability, and stabilize property prices.

The capitulation we saw in early Feb is holding firm.

It’s difficult to say whether China can break thru into a new bull market. The American Presidential election is going to create a lot of volatility.

However, if you bought at the capitulation lows you’re up 20% and can wait out the volatility.

Over a three year time frame, China should do well. We don’t recommend buying right here, but keep an eye on this market.

Things are never as good as they appear, and never as bad as they seem.

Markets:

Coreweave

CoreWeave is at a $16 Bn valuation!

Reminder: CoreWeave is the private Cloud AI that powers Microsoft and OpenAI.

I believe CoreWeave generates more in revenue than OpenAI does. It’s yet another instance of betting on the ‘capex receiver layer’ not the application layer.

Lumida Wealth bought in at the $7 Bn valuation alongside Lumida Wealth clients.

That’s a 2x+ gain in 6 months

My base case was a 2x with upside surprise by the time the IPO hits

I expect this will be a 4x now with long-term capital gains treatment

It took a lot of hustle to originate, underwrite, and participate in this deal.

Note we turned down deals to invest in OpenAI at an $86 Bn nosebleed valuation last year.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

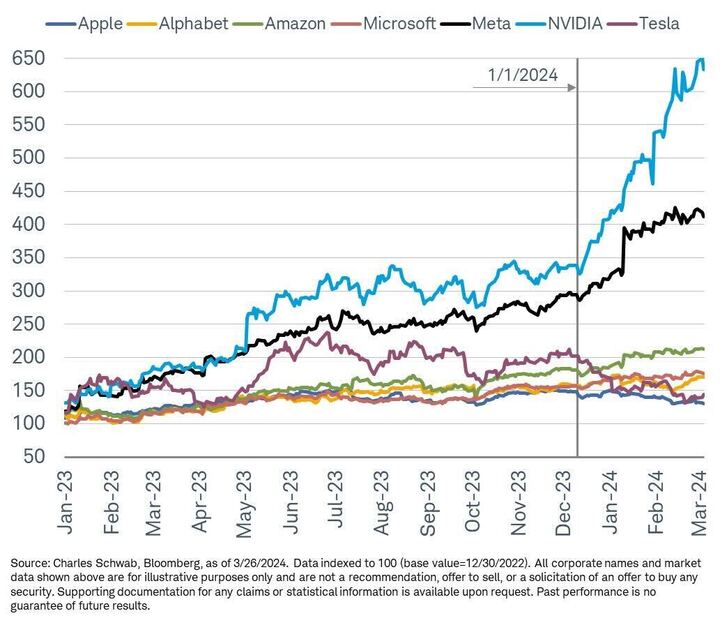

Mag 7 Check In

Let’s put in perspective how the year is shaping up.

As you know, we like Nvidia, Meta, and Google.

We nailed the top two. And I shorted Tesla and Apple.

Amazon and Microsoft we view as Consensus - that means you get no excess return. Consider that Microsoft trades at 95%th-percentile of its historical valuation.

Amazon has a great cloud business. But I don’t want to pay an excess valuation for Whole Foods and e-commerce.

Google under-performed due to fears of Open AI extinguishing search. Those fears are overblown. And we bought Google in size for our clients and it is near ATH now.

We are doing pretty, pretty good this year and we’ve been writing about this trio for months.

Note: Nvidia is quite a bit overbought now and traded down for the week. We recommend an overweight. But, hopefully the market gods will give us a better entry for new client money we recently onboarded.

On Energy

Morgan Stanley upgraded energy to a sector overweight… after energy made its move

We were scooping up energy back in December when it was on sale.

Here’s an excerpt from an X post.

Energy has positive seasonality now thru mid-summer.

We already made our buys some months ago. We like to buy sectors with positive fundamentals when they are on sale.

That said, we did buy a nuclear utility we wrote about in this newsletter about a month or so ago.

GPUs place a tremendous demand on energy.

On EVs and Auto:

For all the talk of Tesla destroying the domestic car industry, we see Ford and GM cranking higher

The non-stop media coverage around the UAW strike created a bottom in autos

Auto stock have been leading the S&P 500 winners table a few days this week now

And now no one is talking about them

I don’t own these and don’t plan to, but study the narrative, price behavior and how those stocks went from bear market to bull market in a few months

Was Microsoft’s ($MSFT) acquisition of Inflection a panic deal?

Yes.

It takes about 3 months to put a fast M&A deal together:

An M&A transaction requires: initial outreach, term sheet negotiation, board consent, shareholder consent, mgmt and team comp, IP agreements and so forth.

Reid Hoffman was an investor in Inflection and Microsoft de-risked by internalizing talent and capability.

AI is driving the Microsoft multiple which is at a 95th-percentile valuation.

And AI is offering the promise of earnings growth via Co-Pilot (still not proven product market fit).

A $1 Bn is nothing for a $Tn company.

It makes sense to de-risk the left tail.

Microsoft’s stock price dropped $50 Bn ish around the OpenAI drama.

Satyanadella made the right decision.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Bloomberg: ‘China’s Super Cheap EVs Offer Hope for the Average American’

We are already seeing glimpses of a promised age of super abundance.

And it has nothing to do with AI.

Take a look at this excerpt:

BYD’s most extraordinary feature is its $9,698 price tag.

That undercuts the average price of an American EV by more than $50,000 (and is only a little more than a high-end Vespa scooter).

Such aggressive pricing by BYD, which surpassed Tesla Inc. in late 2023 to become the world’s largest producer of electric vehicles, is indicative of how Chinese auto manufacturers will likely force US makers to pivot away from mainly producing expensive second cars for the affluent and toward more reasonably priced EVs for the Everyman.

WSJ: Tesla’s Terrible Quarter Catches Analysts Asleep at the Wheel

The WSJ has an article calling out wall street analysts for being asleep at the wheel.

Certainly Goldman Sachs was asleep. So was Morgan Stanley who had a $400 price target on Tesla.

Not Lumida Wealth.

Complacency is the enemy.

Hold your growth stocks accountable and expect the best from them. Earnings growth, margins, and market share growth.

Triple doubles only

Don’t worry, we’re human and we will make mistakes too. Hopefully they involve missing winners rather than sitting on losers.

Mr. Market loves a good story

Here are the themes at work:

AI / semiconductors *

Cloud *

Biotech *

Housing shortage *

GLP-1

On-shoring

Defense

power

Japan

India

I put a * next to themes we own.

There are half a dozen themes we own not shown here (e.g., aging demographics, elective health, housing shortage, etc).

It’s rare to see so many themes in the market working.

It’s evidence of a strong bull market.

The TradFi Complex thinks in terms of a 2x2 matrix ranging from Mega Cap Growth to Small Cap Value.

The reality is Mr Market is Thematic.

Mr Market is a narrative junky.

He loves stories and he gets fixated as if binge watching a Netflix TV show.

And Analysts aren’t as sober and clear-eyed as you may think.

Consider that GS, after the Nvidia GTC conference, raised their price target on Nvidia to a $1,000 year-end target.

That’s 5% up from here.

Would you buy a stock where the analyst has a 6% return target?

GS had a 5% return target for the S&P at the beginning of the year.

Mr. Market is already well ahead of that target.

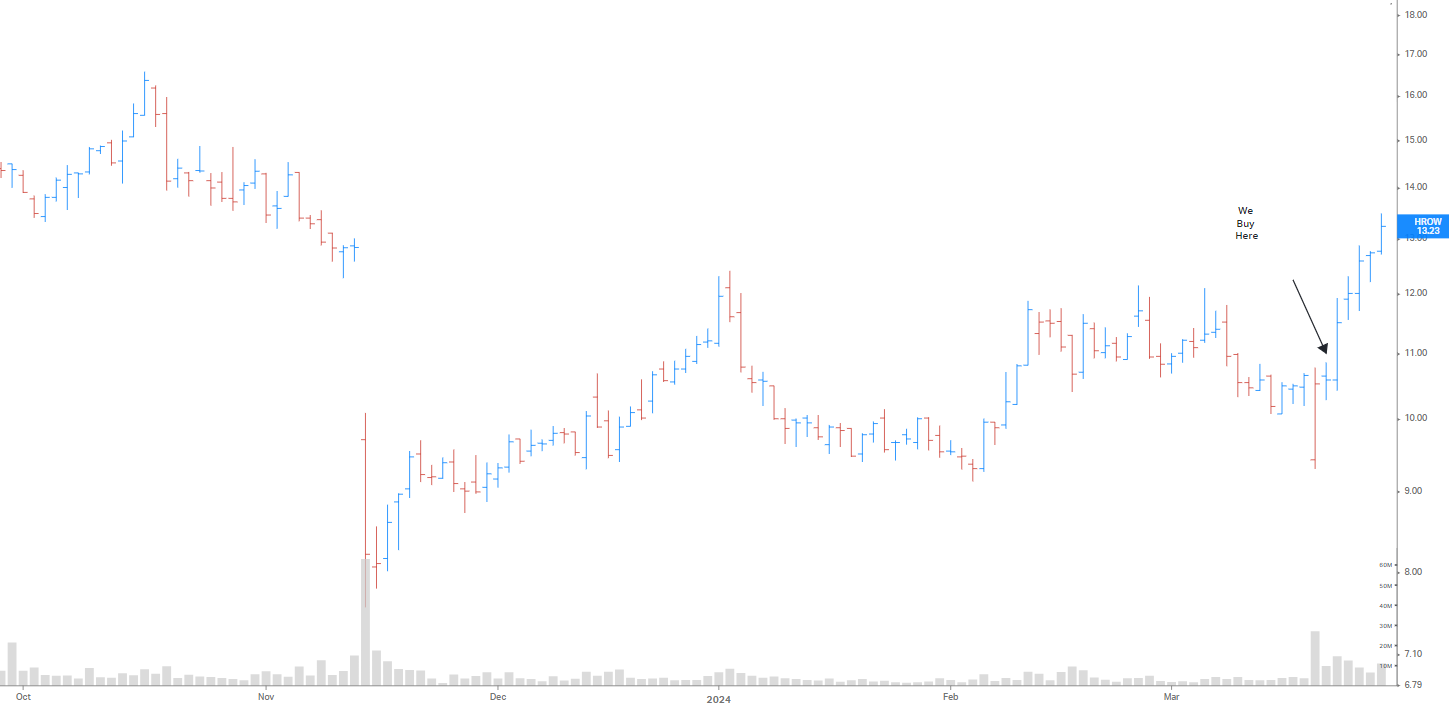

Aging Demographics: Harrow

We bought Harrow (HROW) across client accounts after earnings last week

No one on X is talking about Harrow…that means we are leading Mr. Market

Harrow provides eye care pain treatment for patients dealing with cataracts.

Their target demographic: the ‘oldest of the oldest’. And they are living longer than ever.

The ‘oldest of the oldest’ cohort is growing faster than any other demographic bucket.

And we are continuing to research investments that services this category.

We are long the (treatment of) cataracts. These procedures will only increase.

Harrow has a 5-year sales CAGR of 25% and recently turned profitable at a $400 MM ish market cap.

We can sit back now and let that CAGR compound

Take a look at their shareholder letter here.

The risk to monitor is any signs of long-term debt refinancing issues. They also have strong sales expectations to live up to.

Usage of their lead analgesic product which was fast-tracked by the FDA is up 300% in the recent quarter.

We wrote about HROW last Thursday. It’s up 20 to 25% since then:

We wrote about this call on Twitter the day after so folks that participated also are up 15%+.

Here is our investment thesis.

Markets: Leadership Rotation

We are seeing strong evidence of leadership rotation.

Energy and midcaps are doing well, as are small caps with earnings growth. Biotech is doing well.

Tech remains expensive. We own tech - but you really have to be precise about your expression or you will lag.

We recommend this post to dig into our Leadership Rotation hypothesis, and the segments we expect will benefit the most.

Homebuilders

The best AI proof investment? Land.

Land is also high beta. There is also a major housing shortage.

We bought MHO last week - our homebuilder with a 7.8x Forward PE ratio

I mentioned this on Trends with Friends. In this clip I explain quality, value and momentum and how we seek to bring these factors together with a strong theme and good security selection.

MHO is up about 4% since then.

Company Earnings

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Consumer

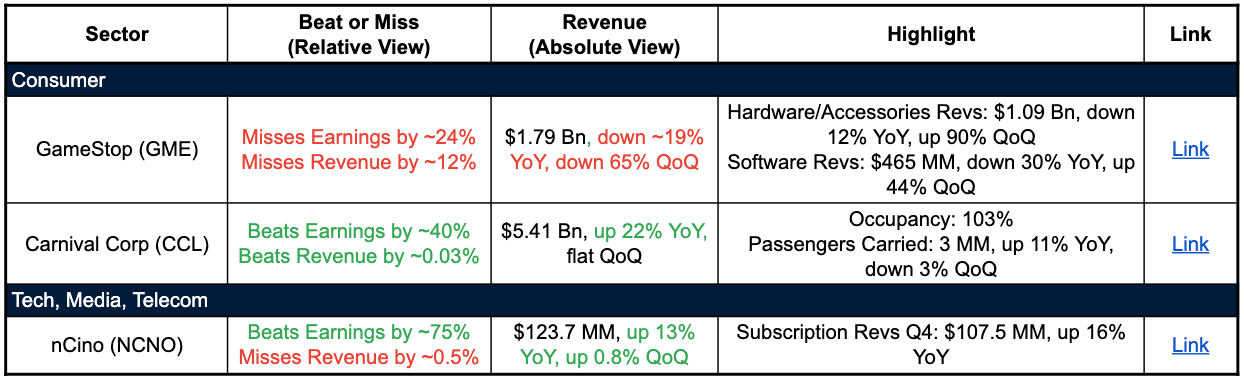

GameStop (GME): The video game retailer missed earnings and revenue expectations. The hardware/accessories increase suggests a potential focus on higher-margin products.

Travel & Leisure

Carnival Corp (CCL): The cruise line company exceeded both earnings and revenue forecasts. Strong occupancy rates, but a slight decrease in passengers carried might indicate some lingering travel hesitancy.

TMT

nCino (NCNO): The cloud banking platform exceeded earnings expectations but missed on revenue. However, subscription revenue growth suggests a healthy customer base.

As this earnings season draws to a close here are the major trends we witnessed.

Positive Trends:

● Financials: Most banks beat on both earnings and revenue, with loan growth and strong performances in wealth management and capital markets driving results. There were some exceptions, such as Discover Financial Services and UBS Group.

● Technology: Tech companies mostly beat on earnings and revenue, with cloud computing, cybersecurity, and chipmakers showing particular strength. There were some misses, such as Netflix, Spotify, and Snap.

● Consumer Staples: Companies like Walmart and Costco continue to see strong sales growth, driven by demand for groceries and household goods.

● Healthcare: Most healthcare companies beat on earnings, with strong growth in pharmaceuticals and medical devices. There were some misses, such as Pfizer and AstraZeneca.

● Industrials: Several industrial companies beat on earnings, but some missed on revenue due to economic softness in China.

Negative Trends:

● Retail: Many retailers missed on earnings and revenue, as higher costs and cautious consumer spending weighed on profits. There were some exceptions, such as Dollar General and Chipotle Mexican Grill.

● Real Estate: While some companies like Simon Property Group and Hilton Worldwide Holdings beat on earnings, others missed due to a slowdown in the housing market.

● Media & Entertainment: Warner Bros. missed on earnings and revenue, with weakness in its film division. There were some bright spots, such as Disney, which beat on earnings but missed on revenue.

Other Notable Trends:

● Several companies benefited from increased demand for electric vehicles (EVs), such as General Motors and Ford.

● Geopolitical tensions & Trade tariffs between US & China saw American companies feeling the pinch across sectors - first Apple, then Starbucks and Nike

● Many companies highlighted cost-cutting initiatives to improve profitability in the face of inflation and other economic headwinds.

Digital Assets

SBF was sentenced to 25 years in federal prison on Thursday.

Let’s get the history straight. There are misconceptions around FTX & Alameda and the nature of the fraud.

Here’s the story of the demise of FTX & Alameda. Oldie but a goodie.

The Spice Must Flow

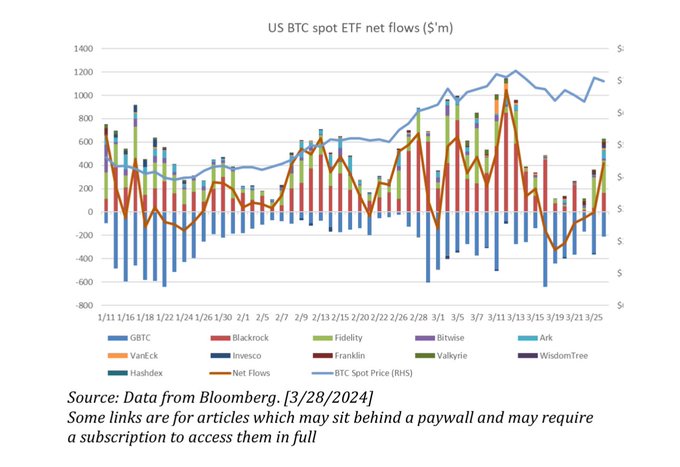

Here’s a chart of Bitcoin ETF Flows

The GBTC hangover is subsiding.

Sam Bankman-Fried (SBF) received a 25-year prison sentence this week for his role in the FTX collapse.

For those interested in learning more about the sentencing, check out this brilliant thread by John Wang on his courtroom experience

For those interested in learning more about the case, we recommend our podcast featuring Tracy Wang (formerly of Coindesk) and Zach Guzman (Coinage media).

They break down the key details and offer insightful commentary.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Quote of the Week

"Beware the investment activity that produces applause; the great moves are usually greeted by yawns." - Warren Buffett

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.