Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Macro: Impact of Rate Cuts, Biden Drop-out

Markets: Our Small Cap picks, LULU, Value vs Growth

AI: TSM, China & Taiwan

Digital Assets: Grayscale Trade is Back?

Lumida Curations: Coatue EWM ‘24 Deck, Powell on Rates, Bill Gurley on AI

Market Call: Vibe Change Ahead?

On Tuesday, July 16th, I did an impromptu ‘What’s On Your Mind’ video about Thoughts on the Market.

Since then, the market tanked, and we believe is entering a corrective phase that will last through August and September.

Watch the video here and jump to the 14:00 or last 5 minutes for outlook.

TIMESTAMPS:

00:02 Overview of Lululemon, Abercrombie & Fitch stocks, and opportunity costs.

02:18 Financial analysis and market performance of Lululemon.

05:37 Small caps’ response to CPI prints and recent market trends.

08:07 Market rallies explained, including 'Melt Up' and 'Mag 7' stocks.

17:01 Rally in low-quality stocks and its speculative nature.

20:35 US Dollar’s effect on global markets and investment in Brazil.

22:39 Technical and thematic analysis of Brazilian company PAGS.

27:01 Value traps in Walgreens vs. CVS’s turnaround potential.

30:40 Investment strategies for small caps and trend analysis.

37:10 Strategic trades in the energy sector and impact of political changes.

39:05 Correlation between crypto, commodities, and potential policy shifts.

41:07 Upcoming market events and their speculative impacts.

45:28 Key indicators in Tesla and Palantir, and significant market dates.

47:11 Market themes and the role of small caps in current trends.

48:32 Sentiment analysis and speculation in 'Mag7' and AI stocks.

49:33 Year-end equity market forecast and caution for late summer.

The timing was uncanny on release.

Notably, the top was on the exact same day in July as last year.

Here are some snippets from a thread I did this week summarizing our reasoning:

1) Consider that Goldman’s Most Liquid Short Basket (e.g., really awful companies) is up 17% YTD, rivaling the S&P

And 11% of that gain was in the last week

2) Call options activity ramped in Mag 7. Options expiration on Friday could be an inflection point

3) Seeing the tepid response to robust earnings (see Wells Fargo, ASML etc)

4) Early July seasonality is behind us

5) The RNC Convention marks peak ‘Trump Bump’ sentiment

6) I see sloppy speculative behavior, which is a marker of ‘last call at the bar’

7) Mag 7 names are approaching 2021 levels, but not quite there yet (mileage may vary)

Later in the week, I provided another update, given the heightened volatility.

Check it out here on Youtube. Don’t forget to subscribe.

I covered various investment topics, including the shift from AI to China-focused sectors, tactical investment strategies, and the energy sector's role in diversifying tech-heavy portfolios.

TIMESTAMPS

01:11: Rotation from high-performing themes like AI to sectors like China.

07:26: Tactical approaches for favorable investment entry points.

09:17: Energy sector's rise as diversification for tech-heavy portfolios.

11:24: Concerns about overvaluation in the restaurant sector.

15:43: ASML stock as a market performance indicator.

24:07: ASML’s long-term valuation trends and potential overvaluation.

26:01: Taiwan Semiconductor's financial performance and margin expansions.

30:30: TSMC forecasts a 10% increase in the semiconductor market, excluding memory.

41:52: LPLA’s resilience as an independent RIA aggregator.

54:54: Active management revealing tactical opportunities and risk mitigation.

55:23: The impact of taxes and time horizon on investment strategies.

56:33: Market predictions for China’s bottom based on political factors.

57:21: Tencent’s expected rise resembles semiconductor stock behavior.

We believe Mexico and Brazil will outperform the United States for a few months.

The risk to that view is inflation returns, and the Fed goes ‘higher for longer’ again. We don’t believe that’s the case, but we would like to share both sides so you can make your own determination.

It’s as essential to share the thought process as the conclusion itself.

Macro:

Impact of Rate Cuts

Barron’s has an article titled “Home Buyers, Get Ready. A Window of Opportunity May Open Soon.”

We believe the benefits of ‘insurance cuts’ are dramatic on psychology. Insurance cuts are when the Fed does a series of targeted rate cuts, but not a full easing cycle.

Even though rates are high, it’s not the level, it’s the direction of travel.

People expect they can refinance out of higher mortgage rates. Indeed, we’re seeing some improvement in housing-related statistics after months of horrid data.

What to expect?

More breadth expansion

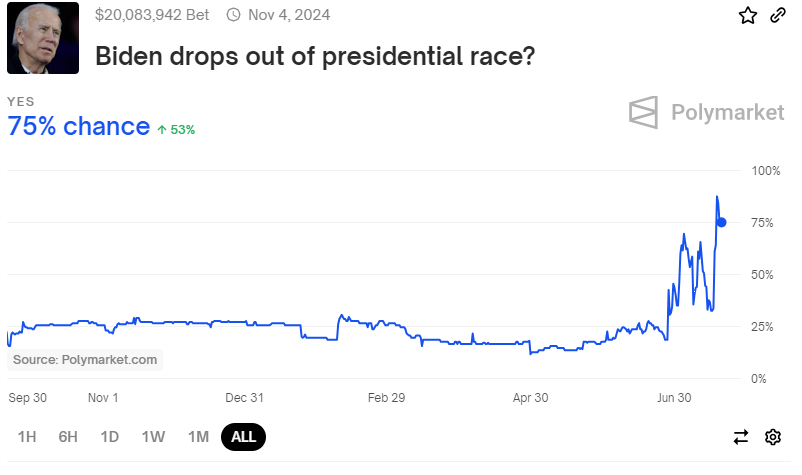

One of our non-consensus calls this week was predicting that President Biden would drop out of the race.

Polymarket's dropout probability went from 37% last Sunday evening to 70 to 90% in five days.

That’s a 2x return in one week, not bad. (Unfortunately, regulations prohibit us from actually executing this trade.)

We made this call the same day Bill Ackman and Consensus expectations said it would not happen.

Non-consensus is powerful because the Consensus is priced in.

Non-consensus is cheap and, therefore, asymmetric.

MARKETS

Small Caps

We have been talking about small caps for a few weeks now.

We wrote that small caps will rally strongly if the market perceives Fed cuts.

And that’s what is happening. We own quite a few small caps - quality businesses that are cheap and generally buy back shares, with earnings growth and room for multiple expansions.

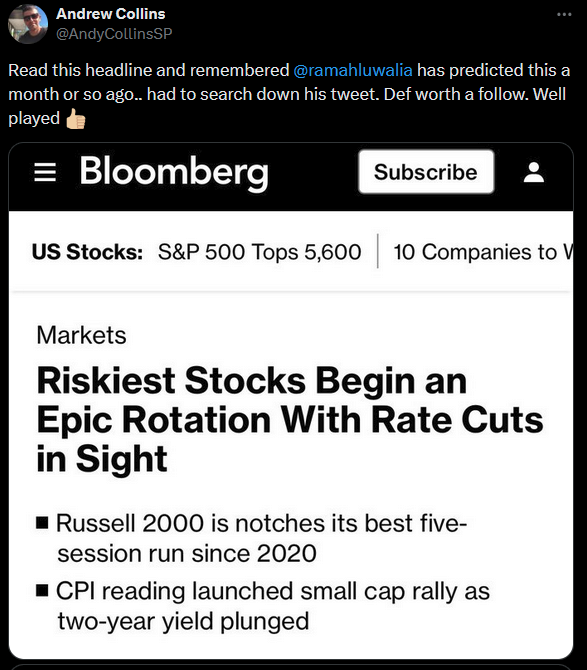

We appreciate the love from Andrew Collins here.

We grow through word of mouth, so we appreciate it when folks give us a shoutout. Thank you, Andrew.

Speaking of - check out www.lumidaetf.com - something may be coming soon.

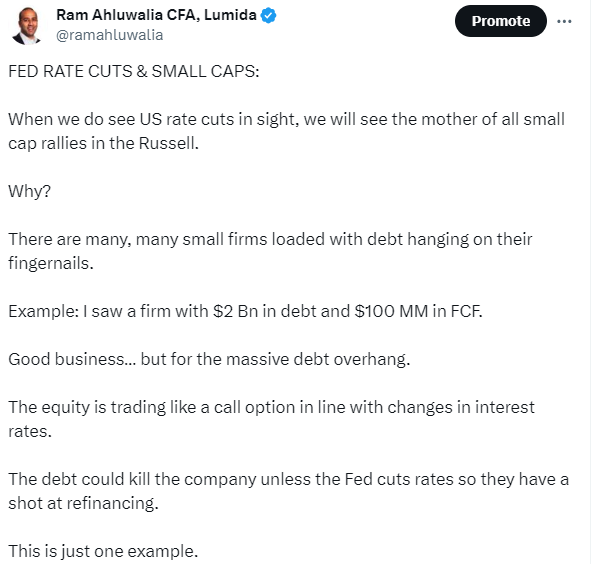

Take a look at this 6/20 post:

‘When we do see US rate cuts in sight, we will see the mother of all small-cap rallies in the Russell. ’

That just happened.

We saw a 4-standard deviation move in IWM.

If you weren’t pre-positioned, it was hard to participate as Mr. Market went up strongly four days in a row.

History was made this week.

The Russell 2000 closed 4.4 standard deviations above its 50-day moving average.

No other major US index (Dow since 1900, S&P 500 since 1928, and Nasdaq since 1971) has ever closed at that much of an extreme.

"Where were you when..."

We believe we’ll see a retracement for a few days, then a resumption of the rally.

We call a significant, pervasive move in small caps a “breadth thrust.”

This week, we wanted to focus on several small-cap ideas.

We have written about some of these before. Note: Some of these have excellent entries, but most do not. Small caps should retrace a bit. Choose your entries wisely.

Or sign up to be a client at Lumida. We have a 2-hour morning CIO call to review positions, themes, and ideas, including when to enter.

Click here to explore becoming a Lumida Wealth client

M/I Homes (Ticker MHO)

Our favorite home builder is M/I Homes (Ticker: MHO).

The homebuilder focuses on building affordable housing for prime borrowers with an average down payment of 18%.

We like that profile and target customer.

The valuation is now 8.3x (it was 7.2x when we first wrote it in the newsletter). The stock generated ~$550 of cash flow on a $3.2 Bn market cap. The stock has a mix of traits like a good valuation, momentum, and a business linked to a secular trend.

The stock is much cheaper than better-known home builders such as DH Horton or Lennar, which are ~30% more expensive.

The stock is under-covered - only one analyst covers it. So, it will have more volatility than other homebuilders.

At the same time, the stock should benefit from multiple expansions as more analysts cover the name.

MI homes has exposure to Florida, Texas, and North Carolina. Those are markets experiencing population growth and have favorable demographic trends. (The firm also has exposure to other markets, such as Ohio.)

Here’s an excerpt from their most recent earnings call:

“Strength of our communities and product offerings, along with our selective and very targeted use of below-market financing incentives contributed to our strong fourth quarter and full year sales performance.

In the fourth quarter, we sold 1,588 homes, a 61% increase over last year with significantly better per community absorptions.

Clearly, as rates begin to fall in the fourth quarter, we saw a pickup in both traffic and demand. Notably, our December sales were the best month of the fourth quarter. For the full year, we sold 7,977 homes, an increase of 20% over 2022.

Our monthly sales pace during the year averaged 3.3 homes per community compared to a sales pace of 3.1 homes per community during 2022.”

We like the target demographic and the ability to offer financing during higher mortgage rates.

Management also notes that costs have stabilized (we speculate that’s likely due to a greater labor pool from immigration).

The firm ended the year with $733 million of cash and zero borrowings under its $650 million unsecured revolving credit facility.

They have a considerable amount of undeveloped land. Land is a high beta exposure. They have a 3-year supply of land to develop.

The bear case for MHO is that their pipeline—the backlog of homes they have under contract to sell—is shrinking. Some of that is seasonal, but fundamentally, these are transient factors.

So, we expect this stock to do well when it reports earnings. As the stock gains a following and analyst coverage (which can take 1 to 2 years), we expect the valuation discount versus its peer group to close.

Advanced Isotopes (Ticker: ASPI)

ASPI, an advanced materials company, has distinguished itself through its pioneering Aerodynamic Separation Process (ASP) and Quantum Enrichment (QE) technologies, enriching challenging isotopes.

With a history spanning 18 years of innovative development, ASPI is well-positioned at the forefront of the nuclear and semiconductor industries. The recent legislative shifts and increasing market demands in these sectors make ASPI an exceptionally compelling investment opportunity.

We believe ASPI has a shot at being a $1 Bn business (5x from year). It’s also the riskiest of our calls as it is unprofitable, although it has commercial agreements and intends to generate free cashflow.

It’s also the most volatile name we own.

Company Overview: ASPI specializes in enrichment isotopes that traditional technologies find challenging. This capability is critical for materials required in small modular reactors (SMRs) and advanced semiconductors, positioning ASPI as a key supplier in these rapidly evolving markets.

Technological Leadership and Operational Excellence: ASPI’s proprietary ASP and QE technologies offer substantial improvements over traditional enrichment methods, achieving efficiencies approximately 600 times greater than current centrifuge techniques. In 2023, ASPI completed its first enrichment facility, with revenue generation projected to begin in 2024, signaling robust operational capabilities and market readiness.

Strategic Market Opportunities:

Nuclear Sector: The U.S. has recently banned the import of High-Assay Low-Enriched Uranium (HALEU) from Russia, highlighting a significant opportunity for ASPI to supply critical materials for SMRs, essential for achieving zero-carbon energy production.

Semiconductor Industry: ASPI is set to impact the semiconductor industry significantly by producing Silicon-28, vital for high-performance semiconductors used in quantum computing. With significant backing from industry partners financing new production facilities, ASPI is strategically positioned to meet growing market demands.

Financial Projections and Valuation: ASPI's subsidiary, Quantum Leap Energy (QLE), is planning an IPO with projected proceeds of $50-100 million. This suggests a post-IPO valuation between $200-500 million, potentially exceeding ASPI’s current market cap. This indicates strong financial health and growth potential, making ASPI an attractive investment proposition.

Competitive Landscape and Market Comparison: Despite Silex’s $1 billion valuation with minimal revenue generation, ASPI stands out with its proven technological superiority and operational effectiveness, led by a management team with deep experience from Highbridge and Soros. This competitive edge, combined with imminent revenue streams, underscores ASPI’s potential for a higher valuation relative to its peers.

Investment Rationale:

Technological Superiority: ASPI’s enrichment technologies provide a competitive edge in efficiency and application versatility.

Strategic Market Positioning: ASPI is positioned as a key supplier in critical and expanding markets. Its capabilities align closely with the global shift towards advanced nuclear technologies and next-generation semiconductors.

Legislative and Market Dynamics: Recent legislative bans on HALEU imports and the urgent need for domestic uranium enrichment position ASPI to capitalize on national security and energy independence needs.

Proven Leadership and Swift Execution: With leadership experienced in managing and scaling complex financial and technological operations, ASPI demonstrates a clear capacity for rapid and effective strategic execution.

Risks

The customer demand is not a risk. As noted, customers, including large publicly traded companies, are financing the capex needs of ASPI.

The two major risks are: (i) technical readiness. Each isotype requires its own plant and adaptions to the process. Management believes their technical readiness for the core business is ‘9 out of 10’, and the newer technology (‘one step laser enrichment’) is ‘7 out of 10’. Delays in delivery are a risk.

Financing Risks: ASPI has issued shares to raise capital in the past. Management considers its balance sheet strong and does not have imminent financing needs. A secondary offering might be issued should ASPI need more capital or time.

Licensing Risks: ASPI operates in the highly regulated isotope market. Entering new markets or delivering certain isotypes requires skillful navigation of federal and state licensing - globally. ASPI is aware of this and thoughtful in their market and isotype selection.

Market Liquidity Risk: Should US equity markets experience a sharp downturn, ASPI and other small cap securities could be disproportionately punished due to thinner liquidity.

Jackson Financial (ticker: JXN)

Jackson was a spin-out of Prudential.

They sell annuities and other products to retirees. We like that because we believe this is a Boomer economy. (Look at Cruise lines, restaurants, travel, and healthcare spending…)

Their business model is simple to understand, and they have a strong customer value proposition. Boomers want income and become risk-averse as they age.

Jackson has a free cash flow/enterprise value yield of 50%.

They are buying back 6% of their stock. We like buybacks for the same reason Warren Buffett does. You own more of the company for doing nothing.

The stock is up 50% YTD and 140% in 1 year. It has momentum and a strong trend.

That means institutions are buying this, likely via a VWAP order.

And the Forward PE ratio is 4.4X.

So, this can compound for many years.

American Public Education (Ticker:APEI)

American Public Education (APEI) was one of the Lumida Stocking Stuffer stocks.

The stock is up 100% since January 1st, one of our best picks, along with Google, Nvidia, and Meta.

APEI is a good example of how a theme, factor, and security selection come together:

- Theme: Aging Demographics: Major shortage of nurses

- Factor: We want to own small caps at good valuations

- Security selection: ARR business model with strong fundamental growth trends in revenue and earnings, and a moat in the form of 'licensing' and brand

Start from the Macro finish at the Micro.

I first mentioned APEI in early December when it was in the $5 to $ 6-ish range.

Now it's $19 ish and change.

This is another example of how diversification doesn't mean giving up returns.

Concentrate on the themes.

Then find the best expressions in the themes at good prices at that point in time.

For example, there are about a dozen fantastic semiconductor businesses.

There are a dozen businesses we love in our aging demographics.

These range from in vitro fertilization, clinical software SAAS plays, hormone replacement therapy, and certain biotech plays.

There are ~5 businesses in our Nuclear Renaissance theme.

Not all of these are 'on sale' at any given time.

We have enough quality ideas that when we see a quality idea go on sale and want to increase thematic exposure, we can pounce on it.

On average, if we are skilled at identifying enduring secular trends and can identify winners in those themes before Mr. Market, we'll do just fine.

We can't control Mr. Market.

We can focus on doing our best to make a good decision and get a good entry.

Take a look at APEI here. We first mentioned it on Twitter in early December… Next time someone says ‘You must own Mag 7’ just show them this chart.

This is what happens beneath the surface of the indices.

The big money managers are rotating to small caps by macro-focused index products. Those lift the largest market caps in the space. There is plenty of opportunity in small caps remaining.

Markets : S&P Longer Term Outlook is Bullish

The S&P is up double digits, and people are still concerned about a recession.

Consider this…

Bank credit growth is near 0%

When bank credit growth recovers, as long-term rates fall and HTM holes fill, that’s another driver of growth that’s not online yet.

And then you have strong productivity.

And labor force expansion.

And strong profits growth.

And record household wealth and stock prices.

If small caps generate profit growth after rate cuts and debt refinancing, then you have yet another driver.

If rate cuts drive positive psychology, then combined with net new household formation, you have another driver.

What are the tail risk factors?

- China invasion of Taiwan / War

- Excessive tariffs (I’m reluctantly OK with ‘PR tariffs’ and strategic tariffs)

- Meddling in free enterprise

The economy’s natural instinct is to grow

You need a severe misallocation of capital (e.g., overinvestment), profits collapse, labor participation collapse, or the Fed raising rates…

None of that is happening folks.

So, for these reasons, we see this as a Correction in the context of a bull market.

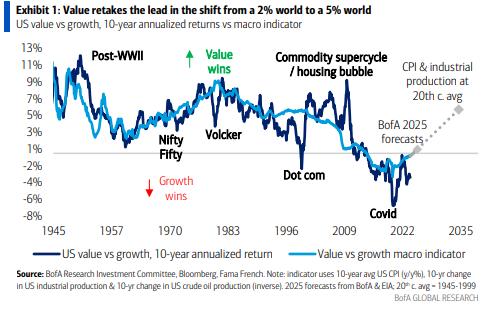

Value Versus Growth

We wrote in April and May about the rotation from Growth to Value.

If you believe the economy is on the mend, then earnings growth broadens.

And growth is expensive. So, capital will flow to quality value.

BAML is picking up on this now also:

It’s simple.

The Best vs The Rest Theme which we discussed earlier this year is over-priced. There are names within that theme that can certainly continue (like Nvidia), but other names like Chipotle and Costco should lag simply due to relative valuation.

Reports of the Death Of Lululemon May Be Greatly Exaggerated

This may surprise some of you…

We bought Lululemon. This is after our critique of Lulu after their March’s earnings miss after which we cautioned not to buy the dip.

Lulu continued to drop like a rock after that call (noted with red line).

Now, we believe Lululemon will be higher within one year double-digits.

What risks aren’t priced in?

Deterioration in consumer spending seems priced in

And rate cuts are coming… along with animal spirits

Lulu is at the same price as it was in 2020, and this is a strong support zone

ANF is cheaper and has more momentum…

But that valuation spread has closed.

And Lulu has a strong brand with an international growth story.

At low valuations, you can give company’s credit for its business plan.

At high valuations, you should be skeptical.

Lululemon may also benefit from the ‘negative momentum’ rally.

Could there be more downside ahead?

Sure. Maybe.

But, Lulu has more upside potential than downside as risks are increasingly priced in.

Look at this 5-year price chart of Luluelemon:

5 years ago, Lululemon had a comparable revenue growth rate. Except now its Free Cashflow and Revenue base is ~3X higher.

And it’s the same price.

That looks like a bargain to us.

ASML is back below prices seen at the Ira Sohn conference - the seminal annual stock picking conference.

We have an interesting history with ASML

Mr Market … isn’t he devious?

Mr Market is manic depressive,

highly moody,

will party with you in Vegas one day, stick you with the bill the next day,

and only after raiding your mini fridge,

and he will take your iPhone charger when he packs his bags.

Do you see the value of an Active ETF?

Not paying ST cap gains taxes and not having to tie up capital in dead positions (but great companies) can add a lot of value.

Imagine bugging out of ASML at the Ira Sohn conference or Nvidia at the Cathy Wood top and re-entering when conditions are favorable.

ASML is no longer more expensive than NVDA.

We issued a buy call on ASML last octoer. Then at the Ira Sohn conference we said this is Consensus and a hold (to avoid paying taxes).

Now, we believe ASML is attractive.

We expect semis to have a relief bounce this week.

Also, the other caveat is that the Summer correction is not done in our view.

But it is worth establishing starter positions.

We are proud of how we navigated this complex name thru the Non-Consensus to Consensus and back to Non-Consensus…

Restaurants: Chipotle Check-In

Take a look at CMG

The stock is down ~18% since our 'Sell Restaurants call' and down 23% from its All-Time High.

I never understood why Chipotle should be worth more than Nvidia

Great fundamentals but...

"Price is what you pay, and value is what you get."

LPLA Financial:

Another name we bought this week… LPL Financial.

We will double-click on this next week.

The headline is that regulators are pressuring wirehouses and independent RIAs to reduce or stop fee-sharing on client deposit balances.

Schwab’s stock was whacked on the news and they are going to use 3rd party cash sweep providers.

These brokerage firms would take clients cash, deposit them, earn a yield and then split the revenue with the client. That practice is rightly coming under scrutinty (these are fiduciaries after all).

Side Note: This kind of non-senses and shennanigans is one of many reasons why I started Lumida Wealth. Wall Street is loaded with conflicts…

In any case, the bad news is priced into LPLA. We did a deep-dive on this and feel pretty good about the analysis. Now, it may take a week for the stock to settle.

But we do believe one year from now, the stock will be a double-digit percentage higher.

Technically, the stock is also at multi-year support. And we see a volume climax indicating bulls coming to defend the stock - including us.

LPL Financial has a forward PE of 12.8x and a current PE of 16x.

That’s a bargain for a high quality business model, and on a relative value basis verus the Forward PE of 20x+ for the S&P 500.

The secret is that asset managers have high margin businesses and long-duration client relationships.

We love the business model.

Company Earnings

Consumer:

Netflix (NFLX): Strong performance with beats on both EPS and revenue. Significant growth in paid memberships and ad-tier subscriptions. Expanding into ad tech and planning Canada launch in 2024.

Industrials:

United Airlines (UAL): Mixed results with EPS and revenue beats, but domestic PRASM (Passenger Revenue per Available Seat Mile) decline.This suggests that the company is increasing capacity to meet travel demand, but at the expense of profitability per passenger. Premium revenues show growth.

AB Volvo (VLVLY): Positive results with beats on both EPS and revenue. However, truck deliveries softened while service sales grew.

Financials:

Discover Financial Services (DFS): Exceptional performance with significant beats on both EPS and revenue. Strategic move to sell private student loan portfolio.

American Express (AXP): Solid performance with beats on both EPS and revenue. Strong core business and international growth

Energy:

Halliburton (HAL): Met revenue expectations with flat growth QoQ. International revenue growth and continued e-fleet adoption

Healthcare:

Novartis (NVS): Strong performance with beats on both EPS and revenue. Solid sales growth and improved core operating margin

Intuitive Surgical (ISRG): Impressive results with significant beats on both EPS and revenue. Strong procedure growth and system placements

Technology:

Taiwan Semiconductor Manufacturing Company Limited (TSM): Strong performance with beats on both EPS and revenue.Arizona and Kumamoto fabs to begin production in 2025

Infosys (INFY): Strong performance with significant EPS beat and slight revenue beat. Growth across multiple dimensions, particularly in financial services

Real Estate:

Prologis (PLD): Mixed results with slight EPS beat but revenue miss. High global occupancy and increased leasing activity positive signs

AI : TSM and Taiwan

TSMC reported stellar earnings this quarter, with a double beat. Total Revenue was up 32.8% year over year, and Net Income was up 13% year over year.

TSM advanced nodes (7nm and below) contributed 67% of revenue in Q2, up from 65% in Q1, as the 3nm node accelerated in the quarter to 15% of revenue.

Non-Consensus: Taiwan & CHIPS Act

1) To develop on-shore foundry capability, the U.S. would have been better served by the Defense Production Act rather than the Chips Act.

We have little to show for the CHIPS Act besides cost overruns and delays.

2) The Chips Act won’t deliver anything tangible in a relevant timeline

It’s a sunk-cost gift to semiconductor firms I have investments in (thanks, Uncle Sam).

3) Semiconductor chips are the new oil.

To paraphrase Frank Herbert’s Dune,

The spice must flow.

The spice flows through the Taiwan Straits.

He who controls the spice controls the universe.

(Spice = Silicon in case you missed your coffee)

4) AI is not at the same level of destruction as, say, a nuclear weapon.

But AI is just as strategic - and far more useful in day-to-day affairs.

5) The Sovereign winner of the AI race gets all the marbles.

The U.S. has a head start. China is investing more in semiconductor VC and IP theft than anyone else, and complacency isn’t wise.

The U.S. has enjoyed technological pre-eminence.

5) If you believe (2) and (3), then it follows that a policy of ‘strategic ambiguity’ is the kind of policy that leads to miscalculation.

If I want my kids not to do something, I let them know the consequences in advance.

The last thing you need is China gaming American domestic politics.

Sadly, if there were a key moment of vulnerability for Taiwan, it would be between now and Election Day.

6) The appropriate American policy is an unambiguous defense of Taiwan.

It is in the American interest that China not invade Taiwan, for the same reason that technology and AI dominance is in the American interest.

Imagine a world where China controls Taiwan and places export controls on the US via the control of TSMC.

The right policy towards Taiwan is unambiguous support.

Taiwan should also contribute to funding its defense further. Imagine if CHIPS Act spending was focused on Taiwan's defense instead of giving billions to immensely profitable semiconductor firms.

Digital Assets

A Presidential Candidate (Trump) is discussing Bitcoin at a major conference next week.

An Ethereum ETF is launching.

And Solana is moving.

How to bet on all 3 and enjoy a discount to NAV?

It was a few days early thanks to Germany ‘hit max sell button’, but all is well that ends well.

Explore becoming a Lumida Wealth client: learn more about our Crypto White Glove Service or Click here to explore our Wealth & Family Office Services.

LUMIDA CURATIONS

In case you missed it, here are some of the best curations from Lumida Wealth on Twitter.

Be sure to follow Lumida Wealth on Twitter, and on Youtube, where you can get more such curations.

Instead of watching hour-long market podcasts - we distill the key insights in 1 min shorts and serve them in threads.

The goal is to maximize insight per unit of time.

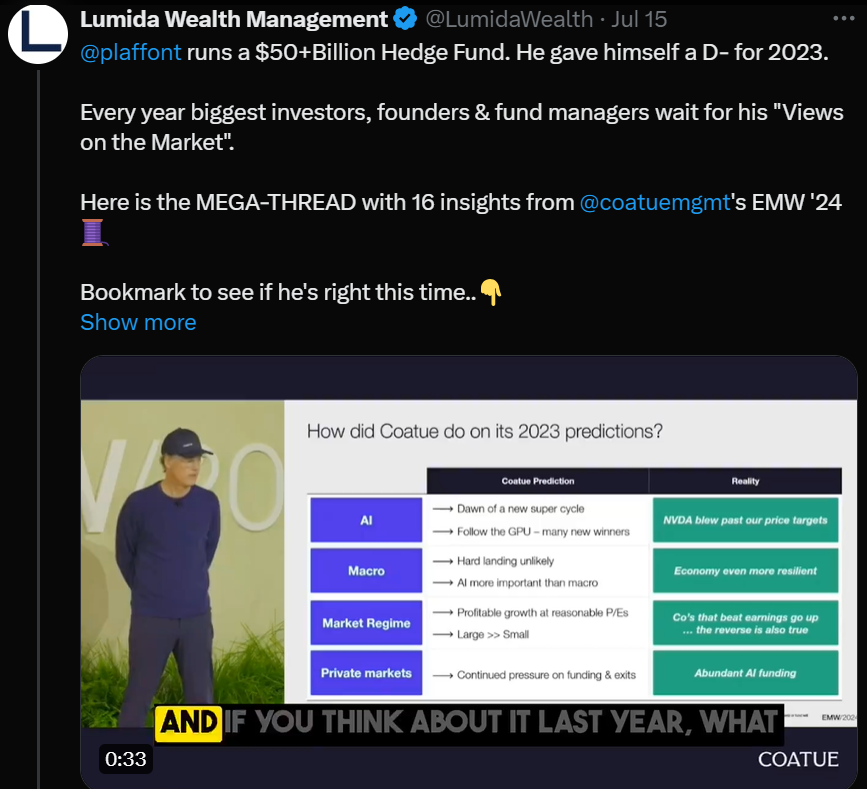

Here’s a MEGA thread of the best clips from Philippe Laffont, CIO of Coatue Management, at his much-anticipated East-West Conference 2024.

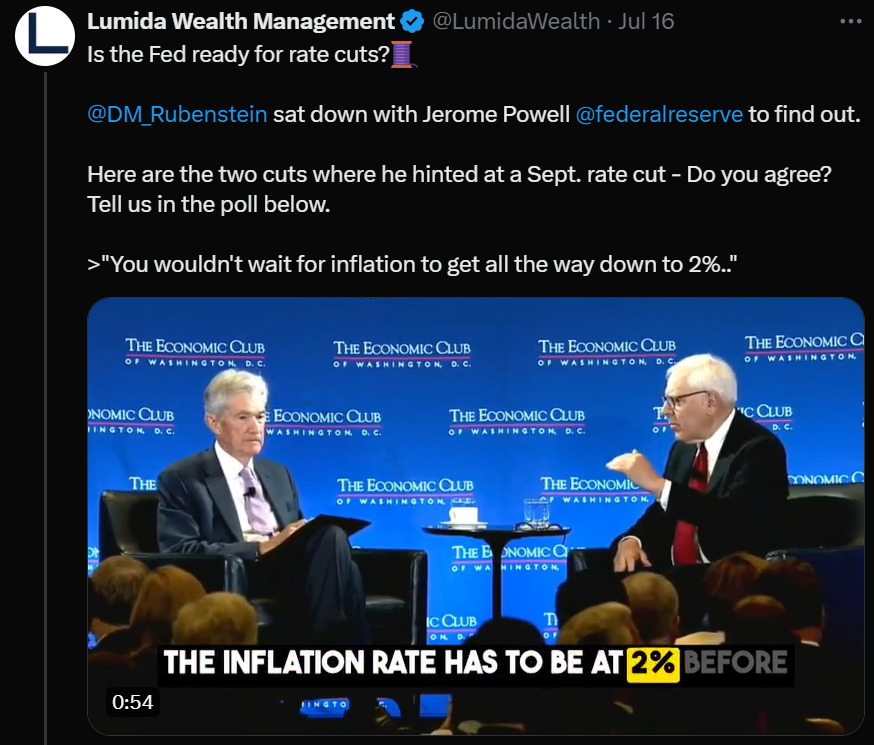

Is the Fed Ready for rate cuts? Find out what Jerome Powell's thinks.

Former US Treasury Secretary Larry Summers shares insights on global economics and AI.

If you are looking for a wealth management partner, Lumida is now welcoming a limited number of new clients.We offer a range of services, alternative investments (such as our CoreWeave deal), white-glove crypto management, to public equity management, and high-touch family office services, including trust, tax, and estate planning.

Ready to explore? Click here to fill out our form to start the discovery process.

Interested but not ready to commit? Build a relationship with Lumida and stay informed. Click on the poll below if you want our advisors to reach out.Quote of the Week

"The biggest mistake an investor can make is to be too scared to make a mistake." Ray Dalio

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.