Here’s a preview of what we’ll cover this week:

Macro: Initial Claims, Mag 7’s Dominance and S&P 500, Lumida Stocking Stuffers Stocks (Check-In), (Most) Investment Podcasts Are Bad For Your Investment Health

Markets: The Great Rotation; Factor Review, Multiple vs. Earnings Growth, Mean Reversion, “Best and The Rest” Giving Back, Nvidia's Culture Edge, Markets Are Efficient

AI: Google Gemini 2.0 vs. Open AI Grudge Match, Microsoft & AI data centers

This Thursday, Ram will be interviewing Michael Parekh - legendary and retired Goldman Sachs internet analyst about insights from the CES Show.

Stay one step ahead of the crowd and subscribe to the pod here: Youtube, Apple Podcast, Spotify.

Macro

Mag 7’s Dominance and S&P 500

Chamath on the All-In pod was complaining about Mag 7 dominant weight in the S&P 500.

It’s clear from various podcasts that he has missed the rally and has intimated that a recession is already here.

There is a simple way to “fix” Mag 7’s dominance in the S&P 500

Just ask Mag 7 companies to stop growing earnings.

Stop cloud computing.

Stop Waymo and Quantum research.

Stop OpenAI funding.

Stop Same Day delivery everything economy.

Stop Amazon Prime.

Separate Chrome from Google as the DOJ wants

Stop autonomous driving research.

Stop Nvidia from selling GPUs.

Result?

Your 401k will become a 201K.

Why not just buy the equal weight S&P and let people invest?

Here’s the key point…

Power laws are a part of capitalism.

A small edge compounds and strips the flesh bare from competitors (RIP Toys R Us, Tower Records, Borland, Visicalc, Buick, etc).

I thought VCs knew this?

A lot of VCs missed this market rally.

I know this because as a wealth manager my clients enter the confessional booth and they trust us to help them get back on track.

You start to see patterns and psychology of different buyer groups. (Example: VCs love growth stocks that lose money.)

Look up a newsletter from earlier this summer: Lumida Ledger post ‘Why There Are No Great Tech Investors’

One conclusion is stick to Mag 7 because they have enormous competitive advantages.

Bet on the Chicago Bulls in the late 90s.

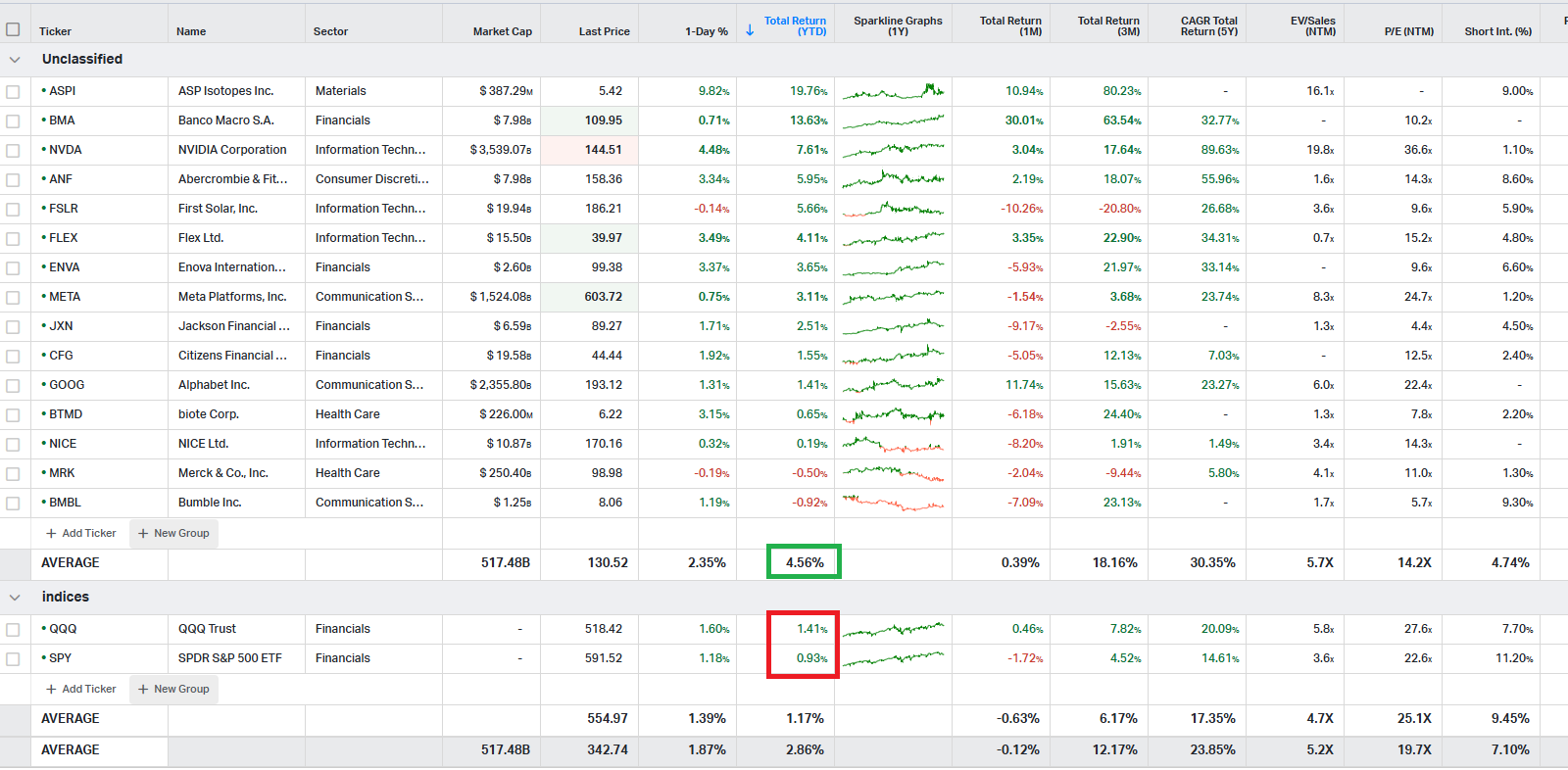

Lumida Stocking Stuffers Stocks (Check-In)

Well we are two days into the 2025 rally.

A lot of people are complaining about ‘bad breadth’ and a Mag 7 dominant rally.

Meanwhile, our stocking stuffer stocks have already earned the annual return on T-Bills.

The portfolio is up 4.5% vs. 1.4% for QQQ and 1% for T-Bills.

Notice:

1. Our median PE is 13x -- well below the S&P 500 median PE

2. We are well positioned for the 'Growth to Value Rotation'

3. Names selected across a range of industries (e.g., semis, pharma, banking, retail lending, etc.)

4. We have several international value plays with momentum such as BMA

5. We have several US plays with mean reversion such as FSLR

6. Rather than 10 names we went with 15 to open up the portfolio to 'right tail upside suprise'

I would have added GM and UBER and Tencnet, but the nature of Top 10 Lists is you aren’t permitted to do that.

What is the statistical likelihood that an equal weight basket of 15 names across industries beat the market two days in a row?

Is that luck or skill?

See the thread below to see a video of how our 2024 picks performed vs. Mr Market.

We are also hiring an independent third party auditor to assess Lumida’s live performance for client accounts in our active equity strategy.

I don’t know any wealth manager that does that.

Instead, they will proffer bad advice such as “dollar cost average down” to justify bad risk management or decision making.

That’s the opposite of what Paul Tudor Jones would say “Losers add to Losers”.

Is Paul Tudor Jones right or your Financial Advisor?

If you’d like to have an initial chat with Lumida, I’d suggest reaching out to [email protected]

Marc is ex-UBS ex-Fidelity and ex-Messari. We’re excited to have him join the team.

We also brought on Oien (pronounced “Owen”) a Columbia MBA and CFA to join the firm and have another CFA joining in a few weeks.

We’re excited about the year ahead.

(Most) Investment Podcasts Are Bad For Your Investment Health

Most podcasts are the junk food of investing—tasty but nutritionally void.

They offer dopamine hits that reinforce Recency bias.

They conflate news (what happened) with insight (this will happen).

Just when a trend is recognized and put into words, Mr Market is moving on

Remember June 16th?

That was the Nvidia ‘Cathie Wood’ top - the date ARKK bought Nvidia they top ticked the market.

This top took place 3 weeks after Nvidia’s May blockbuster earnings. After the top, it took 4 to 5 months for the stock to recover.

At the time, my inbox was flooded with weathervane VCs disclosing that came out of the closet gushing about how they were actually long bitcoin this whole time. (*shakes head*)

Podcasts focus attention on what is immediately behind them.

Podcasts focus on what just got priced in.

Most podcasts are like reading The Economist.

They are barometers of Consensus.

Example: Today, podcasts are talking about Argentinian banks.

The time to talk about that was last month like our Nov 16th episode of Lumida Non-Consensus Investing here. (Worth a re-listen, lot of good ideas in there from various 13F filings.)

The Argentinian banks are up 30% now.

Here’s the issue.

People are wired to ‘make meaning’ of recent events.

Analysts that are invited to these shows - not wanting to appear unpopular and off trend - reinforce said trend by stating what already happened.

Then the trend sucks up more marginal buyers.

That creates a temporary phenomenon called the ‘Hot Ball of Liquidity’.

It’s an expression of herd mentality.

Then the smart (early) money sells into that Trend like Druckenmiller exiting NVDA to Cathie Wood.

Remember the “Eye of Sauron” in Lord of the Rings?

Sauron’s eye is the crowd.

The “eye” adds energy and momentum to whatever it focused on.

But then, some other event happens, and the focus breaks.

(The crowd has ADD).

What was previously in focus drops like a rock.

The herd fixates on yesterday’s news, leaving you chasing trends that have already peaked.

Here’s the paradox:

The real opportunities—the ones with asymmetric upside—

are precisely the ideas podcasts ignore because they aren’t hot yet.

tl;dr stop rubbernecking like the crowd and gawking at what already happened.

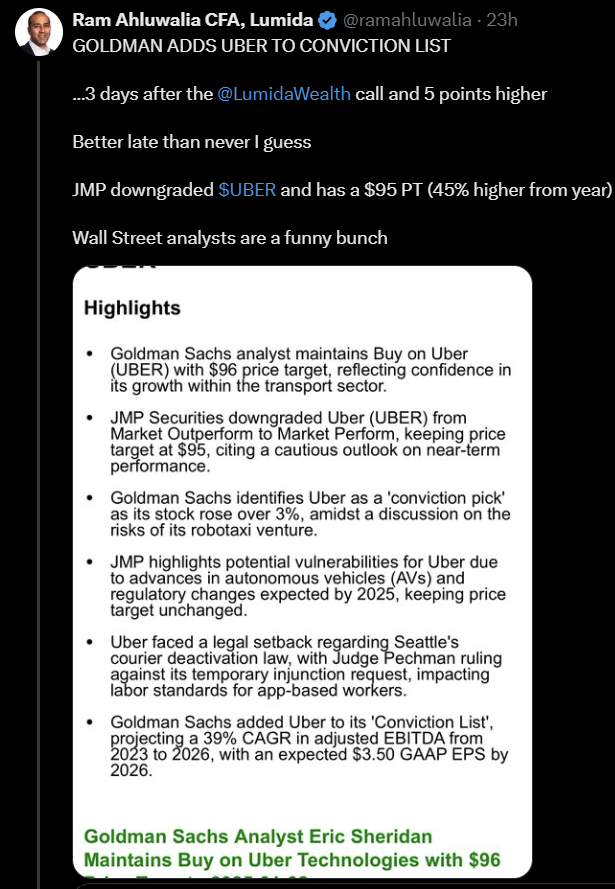

UBER

On Sunday, we announced on Twitter that we were long UBER.

We were bears on the name due to autonomy (write up here “Is UBER the Next Circuit City”).

Uber is a a level in valuation (19.8x forwardP PE) where any half way decently articulated plan around autonomy will restore confidence.

They have a capable CEO and they will have a credible plan announced.

Relatedly, my self development plan for next year is to find ways to get buy ideas that we disliked after bad news is priced in.

I believe this is the main area of improvement for us.

We did a good job avoiding Tesla and Apple for 1H ‘25. But we should have said ‘It’s time to own these as the bad news is priced in.”

The thought had occurred to us but it is psychologically difficult to overcome that initial bias.

Buying UBER here is an example of acting upon that. We were bears before, and now we are bulls.

Mental flexibility is essential. You need change your mind on a position where you’ve done the work.

At a certain price, ‘avoids’ become ‘accumulates’

If UBER were to break down further (say below $55ish), I would cut my losses and rotate.

That’s not going to happen though.

Three days later Goldman Sachs added UBER to their Conviction list pumping up the stock well above our buy point.

Wolfe Research also upgraded UBER.

What’s really happening here?

Many analysts were looking at UBER and privately thinking “Gee… this looks cheap. But it’s a falling knife. I don’t want to catch that. But, it has support here…”

Then someone takes a leadership position and makes the bull case. If the price goes up, others follow.

Then analysts pile-on because they don’t want to miss the rally.

That’s what happened.

It’s a “bandwagoning effect” and safety in the herd phenomenon.

The true alpha is having an original idea and leading the crowd when it is Non-Consensus.

If you’re wrong, just cut your losses and move on.

That basic approach has led us to outperform the venerable S&P 500 and we’re confident we’ll do it again this year.

Markets: Multiple vs. Earnings Growth

The last two years we have seen ~25% back to back years.

Last years rally was 50% multiple expansion and 50% earnings growth led.

Multiples are high. However, earnings growth can continue.

If we assume no multiple expansion, then you can still get a mid-teens return.

The left-tail risk is a rebound in inflation in the 2H.

We don’t see the inflation risk currently - but must remain watchful there.

If inflation comes back, we would re-orient the portfolio towards inflation pass thru names like energy and consumer staples.

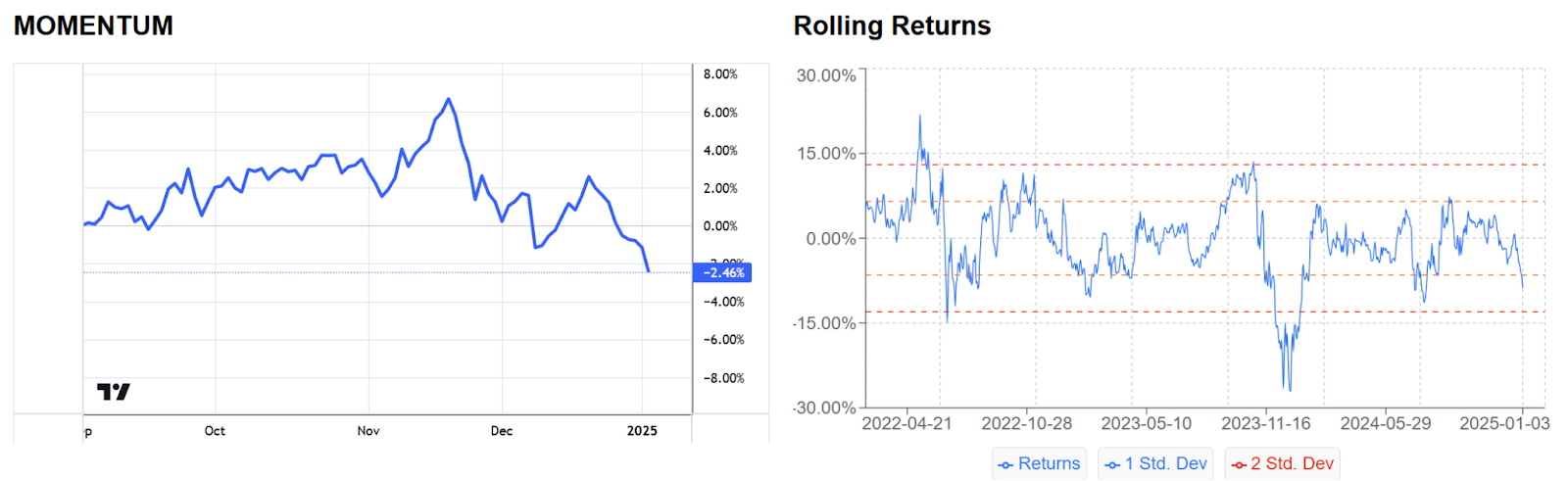

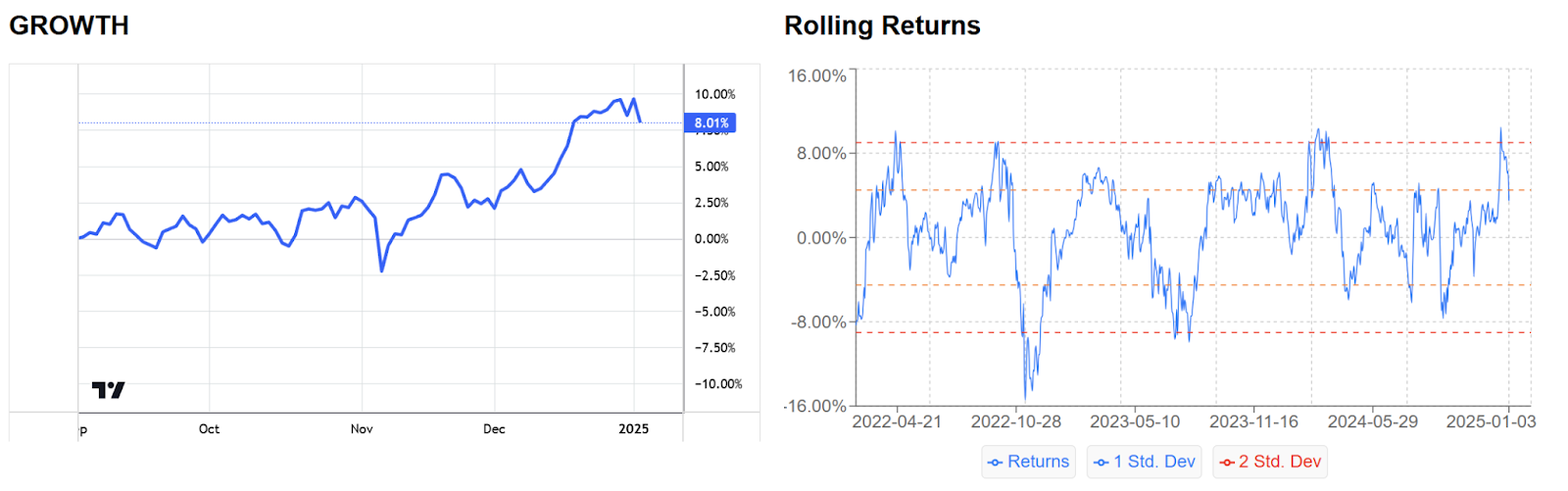

IS THE MOMENTUM FACTOR RALLY OVER?

Take a look at these charts:

FICO

AXON

CVNA

VRT

HROW

These were all high momentum names. They are all fading in unison.

You can see that in the Momentum Factor. Take a look at this snap from our AI platform:

Stocks that went up bigly in the last 12 months are giving back gains, on average.

The same is true for stocks indexed to rapid sales or earnings growth.

What we saw in the back half of December was a correction in “Momentum & Growth” factor.

Although momentum is approaching oversold, Growth factor continues to give way to Value which is a compelling buy in our view.

Value stocks are oversold:

And the mega-cap banks are reporting this Friday followed by regionals the following week.

Those stocks are indexed to the value factor (along with energy and insurance names).

In addition to the CES show (which should create renewed focus on Nvidia), we expect the banks will report record results in aggregate.

It’s a great category to own - and excess after the “Trump Bump” is now worked off.

Mean Reversion

If momentum is fading, how to exploit that?

Bet on mean reversion.

That’s in part what led us to buy UBER. We also like Bumble. The dating app has a 6x Forward PE earnings and a 25% buyback yield.

It’s battling it out with the 200 day moving average. It’s hard to know when it breaks thru (maybe next earnings), but to quote Agent Smith we expect “It is inevitable” in 2025.

The stock is up 18% in 3 months and out-performed the S&P 500 over the last week.

Other mean reversion ideas with a longer-time frame include Merck, Legal Zoom, and Nice.

“Best and The Rest” Giving Back

In January last year, I wrote a post about how the Best Quality stocks in the world were getting bid up.

Names like Costco, Walmart, S&P Global, FICO, Berkshire Hathaway and about a dozen others.

There are undoubtedly world-class businesses. (That’s why we track them - we want to know when they go on sale!)

They are giving back and have technical deterioration. See FICO below. It hasa 66x Forward PE.

FICO is way pricier than Nvidia.

The Best and The Rest theme is a source of risk.

If you consider all of the above observations, it’s clear that 2025 is setting up for the Great Rotation.

Nvidia's Culture Edge

We saw this X post and thought we’d share it here. There’s lesson here for Founders too.

We do believe Nvidia is poised for strong returns in 2025 so why not highlight the name.

"Every former Nvidia employee that goes to a large tech company like Google and MSFT says it's extremely difficult to adjust to the culture, Nvidia is faster but the work ethic is on a different level"

3dfx was the No 1 graphics company in the mid-to-late 90s, their main competitor Nvidia beat them and essentially destroyed them - acquired their assets and hired 100 of their engineers.

The 3dfx engineers kept looking for Nvidia's secret or magic trick, but it turned out the only secret was relentless execution & working crazy hard.

This culture obviously stems from the CEO, Jensen - who loves to work on Sunday nights & finds it relaxing.

Every time they need to make decisions, he brings together top 10-15 people, including lower-level employees, to hash out the main problems in an intellectually honest way and execute quickly - what they call "speed of light" at Nvidia. Link to the interview.

Markets Are Efficient

MY SAFE WORD IS

‘Markets are efficient’

If I say that, you will know something terrible has happened.

‘Random walk’

This means send in the marines asap.

‘Dollar cost average down’

This means I have a brain hemorrhage, call doctor

‘Buy and Hold’

Means aliens have abducted me.

AI

OpenAI vs. Google

OpenAI just spilled blood.

Did you see this?

OpenAI did this because Google dropped the Quantum news and Google Gemini 2.0 during the '12 Days of OpenAI'

It's high drama.

I hope I can buy Google on the cheap again.

Sell to optimists, buy from pessimists.

Google’s Gemini 2.0 Flash is a powerful competitor.

The new LLM has (i) much larger context window than rivals, (ii) multi-modal (Open AI o1 model is not), (iii) fast and cheap.

Google invented the Transformer (the seminal AI whitepaper). They have cracked the code on Custom Silicon.

There’s a major battle raging between all of these hyperscalars.

Betting on the picks and shovels idea (Nvidia) and the players with data and distribution (Meta and Google) at good valuations remains our thesis in 2025.

Microsoft & AI data centers

MSFT expects to spend $80 billion on AI data centers in 2025.

This should mean a lot more revenue for CoreWeave - our most recent deal.

By the way, you should register at www.lumidadeals.com if you want access to our next deal.

All of our deals are in the money and you can see them on the webpage.

SEC rules prohibit us from telling you we have a new deal until the deal is closed.

You need to register in advance. You can choose what deals you want to participate in and meet other leaders on our rapidly growing team.

AI is under Hyped

Investor Tip

FOCUS on information at the edge of public awareness that is gradually coming into view.

IGNORE information at the center of public discussion. It will inevitably fade from view.

Example 1:

Biden admin indicated in a relatively uncovered news item that energy sanctions may be coming.

Focus. Energy higher 1 week later.

Example 2:

One week after Yenmageddon carried trade, every podcast is explaining embedded leverage

Example 3:

Death at the hands of OpenAI at Max volume.

Ignore, buy Google

Example 4:

Death of UBER via TSLA at max volume

Ignore, buy UBER

Example 5:

Microsoft deemed AI the crown winner after investment in Open AI.

Ignore, buy CoreWeave

Example 6:

Recession is here yada yada.

Ignore, buy stocks.

Example 7:

Stocks have achieved a permanently higher plateau (Irving Fisher)

Run for the hills.

Example 8: Drudge Indicator

‘Banking crisis’

Priced in. Buy banks.

Example 9:

Snowflake CEO has Midas Touch and a 200x PE ratio.

Sell SNOW, no buyers left

Example 10:

Uranium on every VC Pod

Sell uranium

we like uranium again and China

No one talking about either

Human psychology is a manic depressive pendulum draped over some fundamentals

example 11:

Ira Sohn conference declares one of our 2024 picks ASML as best stock

example 12:

‘Crypto is dead. Warren Anti-Crypto Army is coming’

Buy bitcoin

Example 13:

‘Hedge into the election, drawn out process’

Go unhedged, quick victory

Example 14:

‘The Fed loves to cut’

Higher for longer

Example 15:

‘Apple Vision Pro is coming. Will be great’

Sell Apple

Example 16:

‘US is the best stock market in the world’

True!

Don’t bet against rule of law, capitalism, and a culture of entrepreneurship

Investor Tip: Skewness

Suppose you have two assets with identical Expected Return of 50% but different skews.

Asset A has a negative skew.

Meaning the lumpiness of the distribution of returns is slewed left.

Asset A will have frequent up days that are small and positive.

Now and then Asset A will have sharp corrections.

The slope is steady up, but there are elevator drops.

Examples:

Momentum Growth stocks, cybersecurity, growth stocks, the S&P 500. Meta and Nvidia.

Asset B has a positive skew.

It has a ‘lottery ticket’ effect.

Some days, or a window of time, produce outsized returns.

A quarter goes by and you beat the market,

rest of the time your returns are boring or even negative.

Bitcoin, uranium, biotech and venture capital are like this. (And Tesla.). And value stocks.

The trap doors are to the upside.

The big returns are lumpy rather than steady.

The big returns occur in shorter punctuated bursts.

Positive skewness means big upside volatility.

Which is better: Asset A or Asset B?

Neither.

Both have the same expected return!

(Leaving aside your utility function.)

We are just talking about the return distribution.

What’s the point?

Skewness should change your approach to entry, exit, risk management and position sizing.

If you apply the same risk management framework to both assets you are making a mistake.

Pull up a chart of, say, Meta and compare it Microstrategy YTD (see attached).

Both had an incredible year.

Notice the difference in the chart pattern from skewness.

$MSTR has a short period of time where the asset cranks.

Meta is the tortoise. It doesn’t sprint like the hare that is MSTR.

Negative skewness means plentiful Small steady gains, and then now and then you get a big left tails surprise (such as when $META was down 20% after Q2 ‘24 earnings).

Then, like a good tortoise, it starts grinding up again….

A negative skew asset is like Le Bron James.

You expect a triple double night after night and month after month.

If Le Bron or Meta doesn’t perform, you get out.

Momentum growth assets are great…

except when you are in a correction regime.

A negative skew asset requires tight risk management to guard against the fatter left tails.

I believe it’s OK to sell tops in negative skew asset…

esp if they have more mean reversion tendencies and less auto-correlation.

A positive skew asset is different.

You want to expose yourself to that right tail.

You need to be in the market for the ‘lottery ticket’ scenario.

So, selling (or shorting) tops is highly risky.

You could be truncating the right tailed outcome you were waiting for.

Also, nailing the timing on your entry helps (of course)

but it doesn’t matter as much as in a negative skew asset.

The mistake in a right tailed asset is not having upside exposure; the mistake in a left tailed asset is not having downside protection

The main idea if you are correct about the expected return in a right tailed asset is ‘maintain exposure’.

Your risk management (say, stops) should be looser.

You offset that greater risk from looser risk management with a smaller position size.

Unlike a momentum growth stock, Positive skewness is all about patience.

You stomach long, slow bleeding periods until high upside volatility occurs — provided your read on expected return is correct.

You cannot apply the same entry / exit or risk management to both positive and negative skew assets.

I have included an image of a negative (red) and positive (green) skew distribution on the attached.

Remember, both have the identical positive expected return.

Side Note: I am fairly sure personality types correspond to skewness preference in asset returns.

VCs are positive skew. ‘Never sell’ and HODLing is a positive skew mindset.

Poker players and traders are negative skew. (It’s easier to flip sides.)

Which personality are you?

As Featured In