Here’s a preview of what we’ll cover this week:

Macro: What Recession?, Median checking and savings deposit balances are up, How the Wealthy Avoid Paying Taxes

Market: Market Stages

Company Earnings: Energy Call: SHELL, NVIDIA Earnings

AI: New Golden Era of Discovery, AI Presentation: Benedict Evans, Ghost in the Machine

Real Vision Pro Live Show

This Monday Ram took part in the Real Vision Pro Crypto Live Show. Check the snippets here: https://x.com/lumidawealth/status/1859606105413787897?s=46&t=NNpqdW4lZE2BRHYHkjXOGw

What he has covered on the show:

Opportunities in Bitcoin Trading: A Current Insight

Navigating a Hot Market: Insights on Crypto Policy

Why Tariffs Hurt the Service Economy Shift

Bitcoin and Political Alliances

Beyond the 60/40: Embracing New Asset Classes

We are Hiring!

Join Our Team: Explore Open Positions at Lumida!

Think you’d be a great fit? Or know someone who would thrive with us? Email your CV to [email protected] today.

Learn more about open positions here: https://www.lumidawealth.com/careers.

Macro:

I guess Argeninta is “Change You Can Believe In”?

What a dramatic turnaround.

Incidentally, we picked up two bank stocks in Argentina. We discovered this thru our 13F analysis of other hedge funds.

We noticed Druckenmiller owned two banks. One is called Grupo Financiero Galicia. We did work on the name.

Forward PE is 9.2x. 4.2% dividend yield. ROE is north of 20%.

Again, that’s not the full underwrite, but on a metrics basis it has certain traits I am looking for. When the US Dollar weakens, the international value factor will do well. So I’ll get a benefit there also.

The entry for this name is increasingly attractive.

Group Financiero Galicia (GGAL):

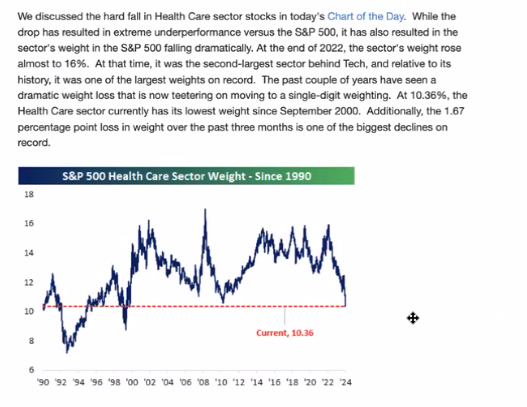

Healthcare and Dr. Oz:

Healthcare stocks as a percentage of the S&P 500 are near decade lows.

When the average investor was concerned about recession in 2022, the sector weight rose to 16%. It was the second largest sector behind technology, another type of ‘defensive’ sector due to the resiliency of Mag 6 earnings.

Healthcare now has a weight of 10% in the S&P. The lowest since September 2020.

And according to Bespoke, the 1.67% loss in the past three months is one of the biggest declines on record.

Healthcare and pharma stocks have corrected over the last few months, in part, over anxiety on who Trump will pick to lead various posts.

In the long run, earnings and valuations and rates matter, not anxiety. But anxiety can create corrections and opportunities.

If you are a true investor, you should take advantage of the anxiety of others.

I don’t suggest owning the GLP1 names that led this correction - but other areas are quite interesting. See prior newsletters for ideas.

I do expect generic will do well.

If Dr. Oz pushes Generics, then our generics pharmaceutical play TEVA should benefit.

Here’s a highlight from the WSJ on Oz’s approach. Overall, I think he’s an excellent pick based on what I am seeing.

Also, within healthcare relief for Medicare Advantage insurers. I am generally avoiding Medicare Advantage insurance firms outside of CVS / Aetna.

There is too much technical damage.

Here is a chart of TEVA which we picked up last week as it bounced off the 200 day moving average. It’s very satisfying to get a good entry like that.

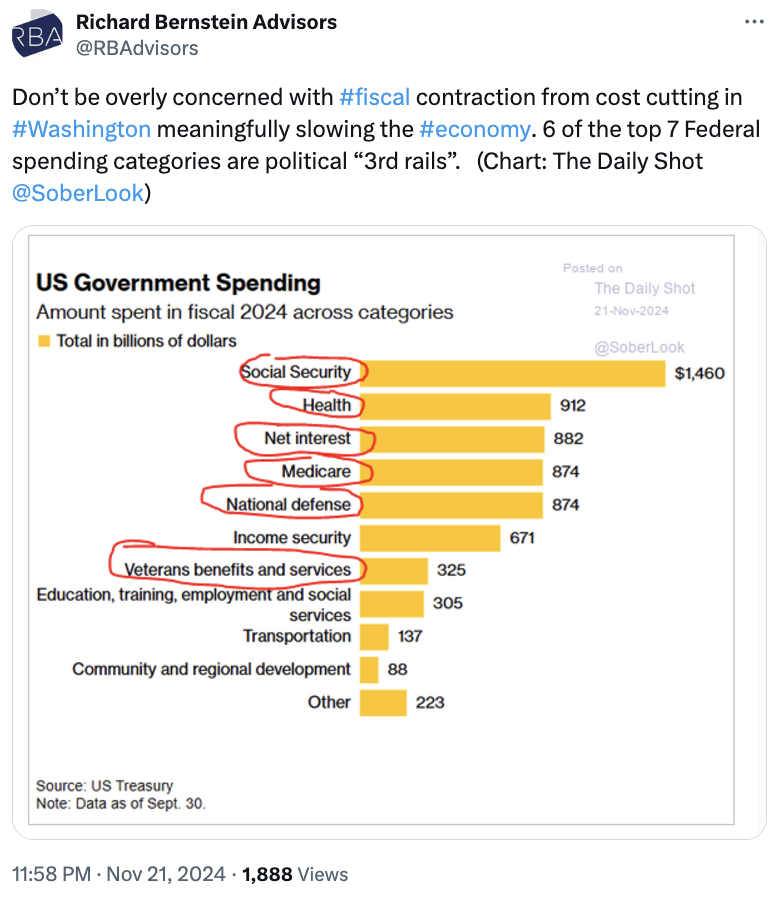

Macro: Can Trump Go Full On Millei?

No.

The US deficit will remain elevated for many years to come due to entitlements.

Here is US government spending by category courtesy of Sober Look. The first several items won’t see expense reductions anytime soon.

Trump’s economic team is likely to bring in Fiscal and Monetary Restraint at least in principle.

Since Congress ultimately passes spending bills, we’ll see how much of that translates to a reduction in spending.

Don’t get your hopes up. Remember when Congress forced the Pentagon to buy F-35s that the Pentagon didn’t need?

Until we can elect AI in to office and force them to sign binding contracts excess deficits are here to stay.

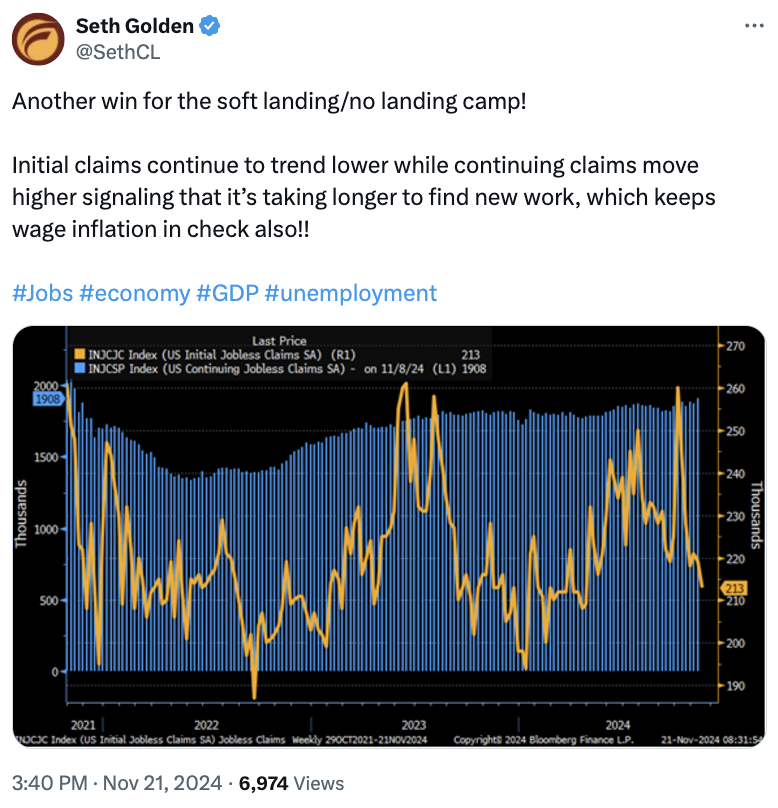

Macro: What Recession?

Here’s another win for our ‘hot landing’ thesis.

Initial claims continue to trend lower.

Continuing claims are moving higher. That means it takes longer to find work. That will keep a lid on wage inflation.

Goldilocks is here folks.

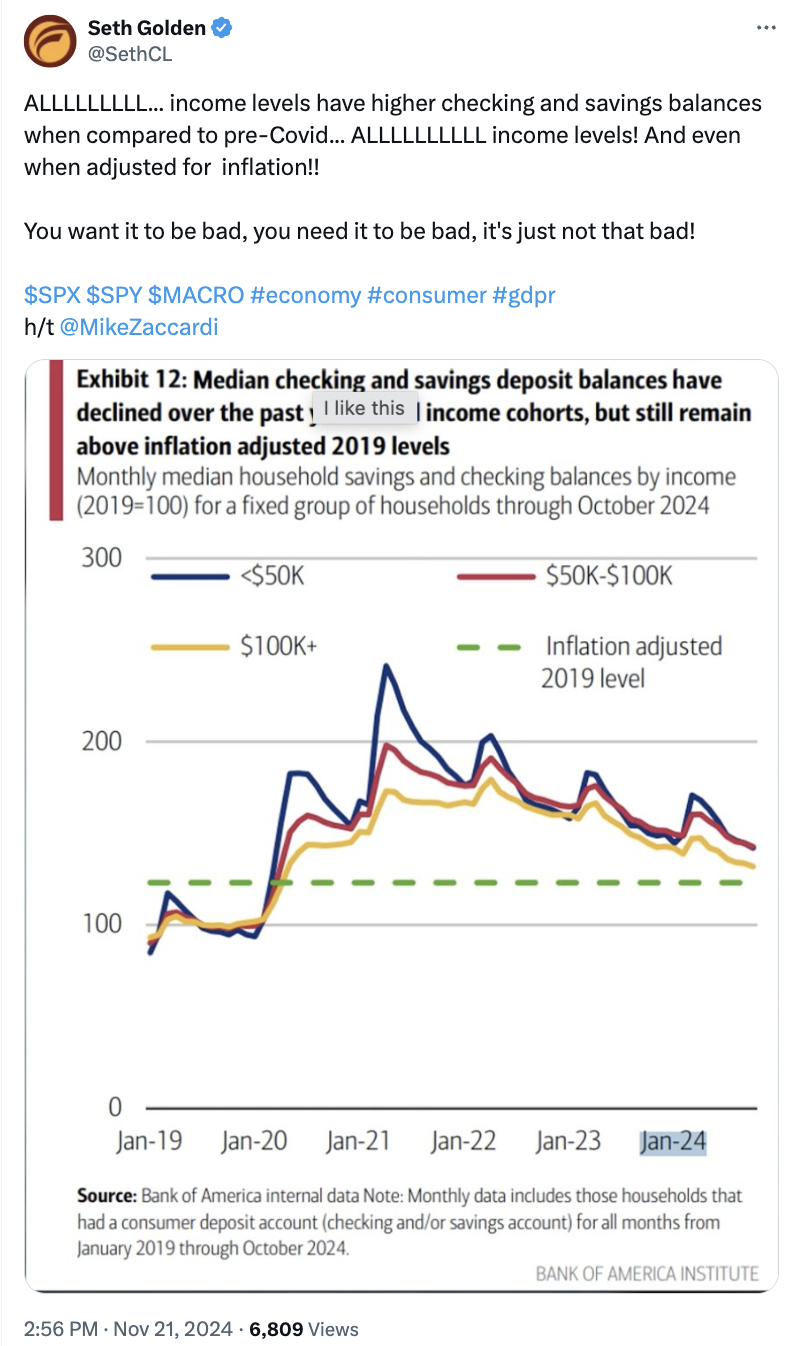

Median checking and savings deposit balances are up

Here’s another little indicator I love. Every quarter I listen to what Brian Moynihan, CEO of Bank of America has to say about the health of the consumer.

And they share data on US consumer deposit balances and income. Notice the levels are above 2019 inflation adjusted levels - across all income strata.

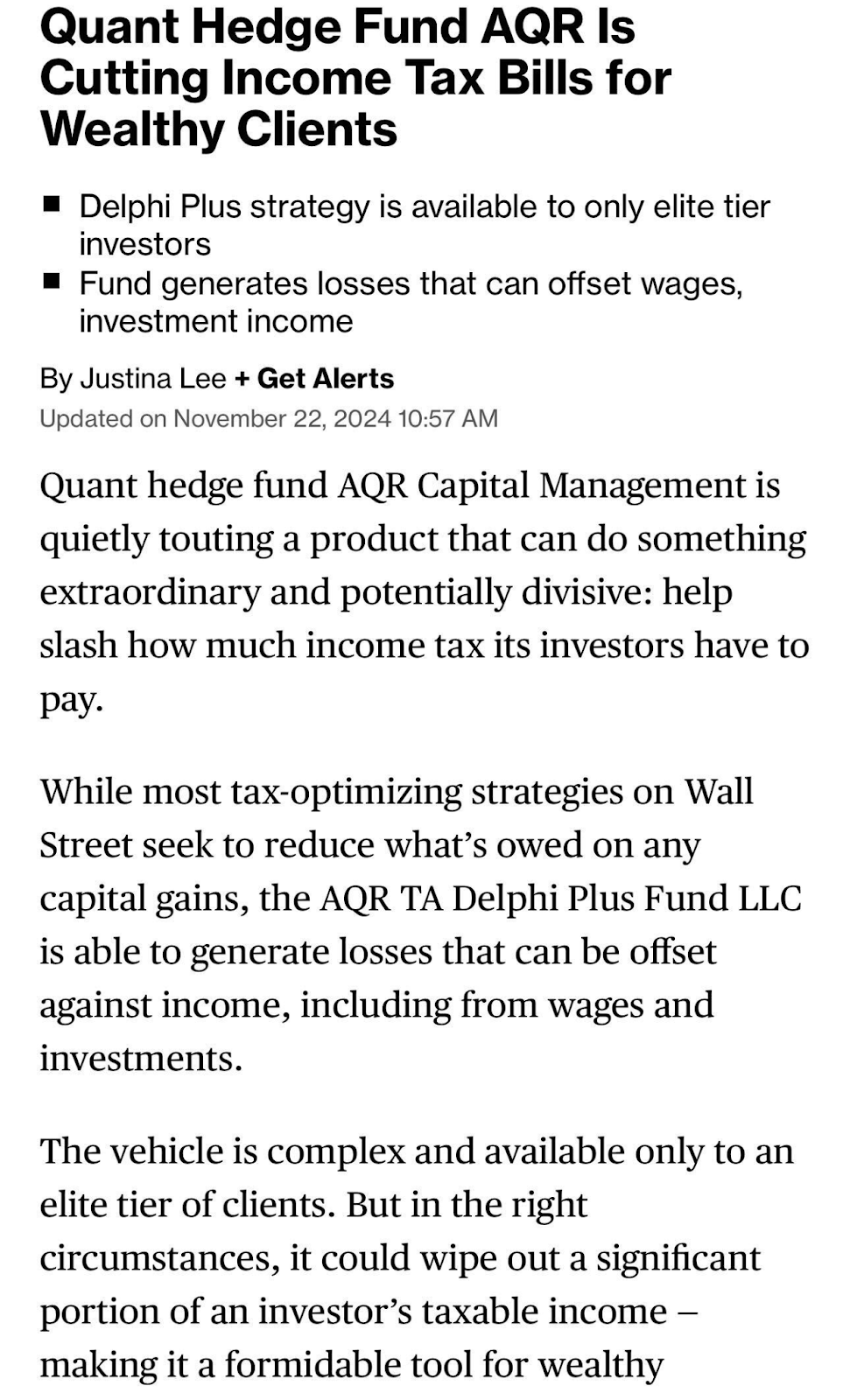

How the Wealthy Avoid Paying Taxes

There’s an article circulating on Bloomberg titled ‘Quant Hedge Fund AQR is Cutting Income Tax Bills for Wealthy Clients’.

You may have noticed in the last several months we have been publishing memes to reach out to us to help us address your tax situation.

There are several strategies to mitigate or eliminate capital gains taxes, income taxes, and passive income.

I’m not going to write about them here, because they will go away, and it’s a source of differentiation for our firm.

But, if Bloomberg is writing this then I’m happy to shine a light on it with the goal of opening your mind up to these possibilities.

Do drop by our Tax Shield Page. That specific strategy is focused on how to mitigate Capital Gains, but we can certainly help on the other buckets as well.

These strategies must be applied in the same tax year. Meaning, your actions in 2024 determine your 2025 tax bill. So email [email protected] now to learn more.

These strategies are ideal for someone with $3 MM+ in assets although they also start to work at $1 MM in assets.

If you have over, say, $50 MM in assets there are different classes of tax strategies that start to come into view such as Private Placement Life Insurance.

I’m going to hire a full-time dedicated CFP specializing in implementing these tax strategies. One can build an entire business around tax.

If you can combine tax, estate planning, and investment excellence together - and combine that with digitally-native technology - you have one hell of wealth management value proposition.

Check more about taxes here: Seamless Trusts and Tax Techniques at Lumida

Market:

Market Stages

I’ve said before we are in Phase 3 of the Market.

It’s a momentum market.

The public consciousness had the ‘recognition moment’ that there is no recession.

They want to get out of bonds and buy stocks.

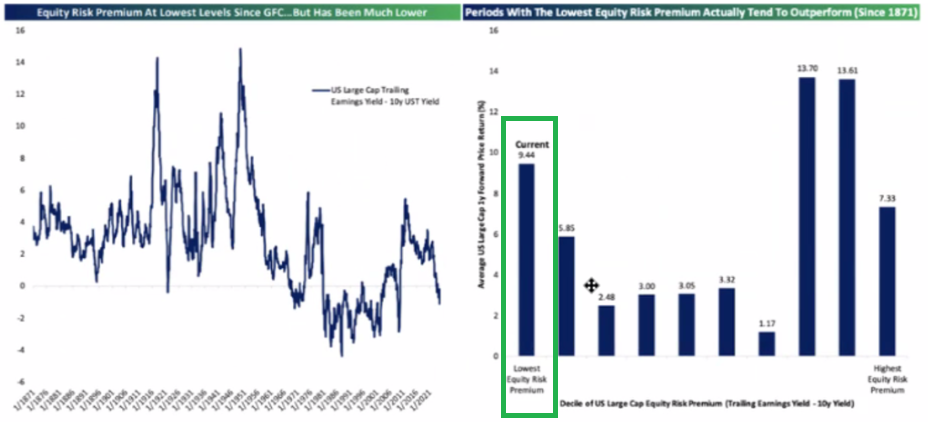

How do stocks do when valuations are at this level.

Well, they do just fine.

Even though stocks have a ‘negative equity risk premium’, the average return for the following year is 10%.

That’s about the average annual return for the S&P 500. We’ll take it.

That said, I do expect that in early Q1, we setup for a correction. Perhaps just after the Trump inauguration or after the New Year.

It will depend on how Mr. Market behaves between now and year end. Too much giddiness will hurt Q1 performance.

Company Earnings:

Energy Call: SHELL

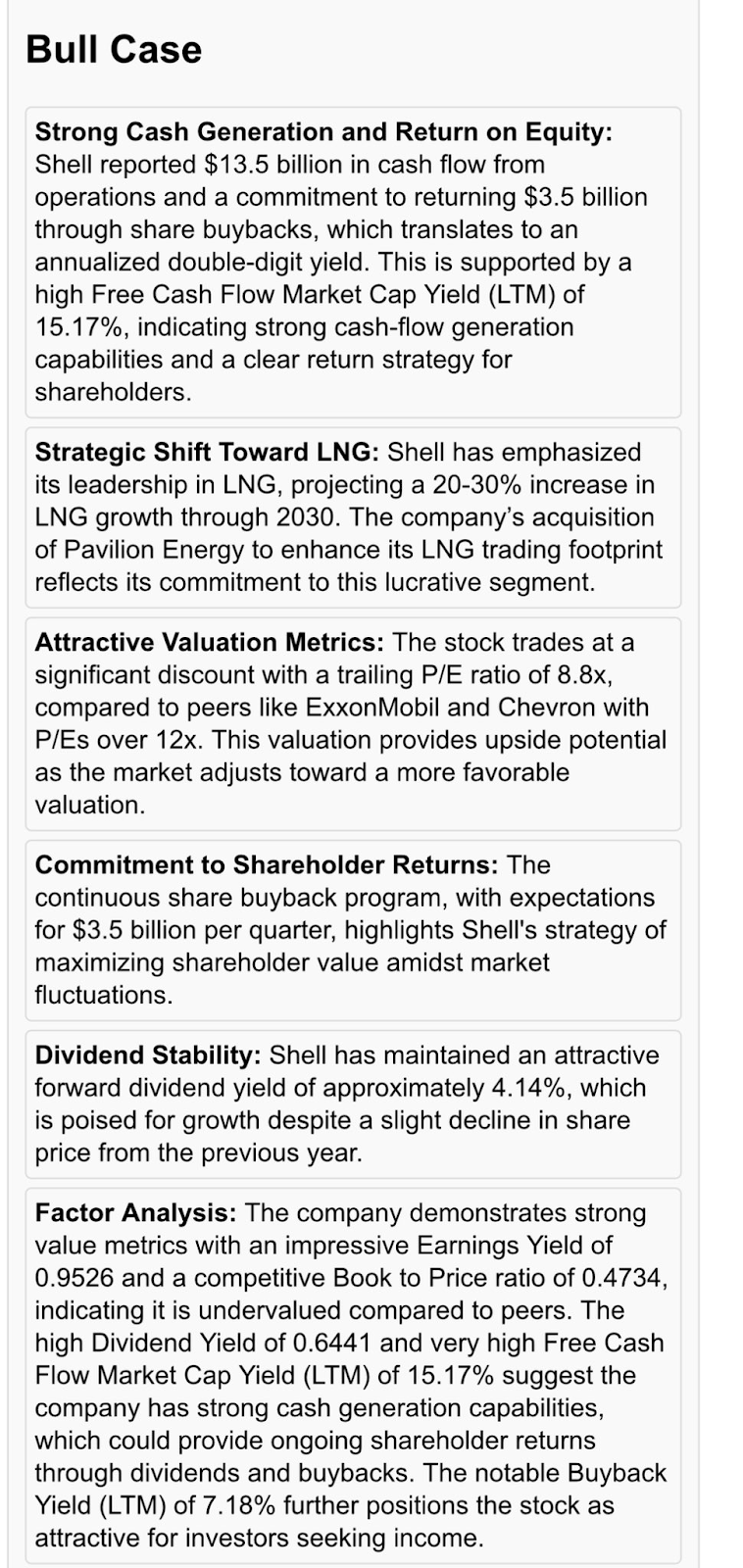

BAML has picked up on our UK based energy company SHELL

Shell SHEL is one of our favorite energy ideas now from a risk adj return view

Shell also has exposure to natural gas.

Shel has a PE ratio of ~8x - much cheaper than Exxon Mobile and CVS.

Shell has a buyback yield of 7%

Bear case is sensitivity to oil prices (eg, if Russia and Saudi produce too much oil)

I’ve attached a snippet from our AI tool and the BAML report

Another tactical edge…

The USD is so strong right now, you can buy international stocks on the cheap

Lastly, why own long term Treasury bonds when you can get a 4.2% dividend yield from Shell?

Give me a few more months and I will make the Lumida Wealth AI tool available to the public for a subscription fee.

Relatedly, we have some exciting company news to share the day before my favorite holiday - Thanksgiving.

NVIDIA Earnings

Did you pick up on the CoreWeave shoutout on the earnings call?

Nvidia is a kingmaker folks...

Let's get to earnings.

NVIDIA’s October quarter results delivered strong topline growth, with revenue of $35.1 billion (+16.8% q/q, +93.6% y/y), beating Street expectations by 5.5%. Datacenter revenue, driven by Hopper GPUs and the anticipation of Blackwell, surged to $30.77 billion (+17% q/q, +112% y/y), a 7% upside relative to estimates.

Gaming revenue also exceeded expectations, growing 14.5% sequentially to $3.3 billion, while Auto and Professional Visualization segments posted robust gains, up 30% and 7% q/q respectively.

Gross margin of 75% slightly declined but stayed in line with forecasts, supporting EPS of $0.81, above consensus of $0.75.

Management’s guidance for the January quarter reflected modest upside, with revenue at $37.5 billion (+7% q/q, +70% y/y) at the midpoint, slightly ahead of Street estimates.

While gross margins are expected to decline to 73.5% (-170 bps q/q), this largely reflects the timing of NVIDIA’s Blackwell ramp (and pricing concessions to TSM and MSFT) .

Blackwell sales should accelerate in late January.

Importantly, demand for Hopper and Blackwell GPUs remains extraordinarily high, driven by AI workloads in pre-training, post-training, and inference, with supply constraints expected to persist into FY26

The story here is not the narrow beat on guidance but the long-term secular demand for NVIDIA’s Datacenter solutions.

Reminder: Nvidia is selling Datacenter solutions, AMD is selling GPUs. Nvidia is playing the game at a higher level...

My view is the constrained supply of Blackwell GPUs masks the magnitude of demand, setting the stage for meaningful upside as production scales in FY26.

Datacenter growth, underpinned by foundational model deployment, remains NVIDIA’s core driver, and the 112% y/y growth this quarter underscores its dominance in AI infrastructure.

Despite near-term supply constraints, NVIDIA’s execution and demand tailwinds maintain its position as a cornerstone of AI-driven computing.

As Blackwell ramps in early 2024, the company is poised to capitalize on sustained demand, reinforcing the bullish case for the stock over the next several quarters.

Analysts are already raising price targets on Nvidia.

We remain long.

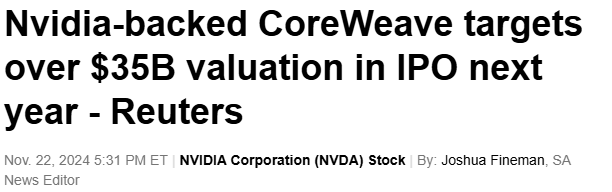

CoreWeave IPO Coming Soon

The IPO Market Cometh.

CoreWeave shall be its herald.

We (e.g., myself and our clients) are investors in CoreWeave at the $7 Bn valuation.

We averaged up at the $23 Bn round which closed recently.

Now, CoreWeave is expected to go public and has retained 3 leading investment banks.

I expect this pops when Mr. Market comps this to Equinix and DLR.

I can’t share the numbers due to NDA… But CoreWeave has a reasonable forward PE and strong earnings growth.

The bankers are pricing this to pop. And they’ll use CoreWeave to warm up animal spirits in the IPO market which wrecked investors three years ago.

If you like our deals, be sure to go to www.lumidadeals.com

We list all our deals to date.

And, we’ll have more deals soon.

I have invested in every one of them and they have all done quite well.

NVIDIA: Interview with a Former Employee

Here is a nice clip from Rihard Jarc based on an interview with a Former NVDA employee (worked there for +20 years) on the competitive advantage of NVDA and the industry in general:

1. In his view, the advantages that NVDA GPUs have over ASICs are that they are more flexible and can run diverse frameworks and models. He thinks that in the short and mid-term, the demand for GPUs will not taper off, but in the long term, it will.

2. The difference between hyperscalers AMZN, MSFT, GOOGL, and NVDA is that chip design is a side business for hyperscalers. For NVDA, it is the main focus.

3. NVDA has more than 50% of the employees who work on software. CUDA is essential to NVDA and keeps other merchant vendors from being largely successful.

4. NVDA is not designing a chip. It is designing a data center. The essential parts are chip interconnects with NVLink to do GPU-to-GPU Interconnect and delivering the whole system of a CPU, GPU, network processor, interconnect and package it up with memories on board.

5. He doesn't think NVDA's DGX Cloud goal is to compete with hyperscalers. According to him, it will be an ultra-premium product as an alternative to embracing the vision of the product, and it will not be cost-competitive with hyperscalers.

6. When he was at NVDA, they had a substantial number of employees who would go to game developers, sit with them, and help them code so that the games support $NVDA features. $AMD didn't have the same number of people deployed, and they didn't have the same number of resources.

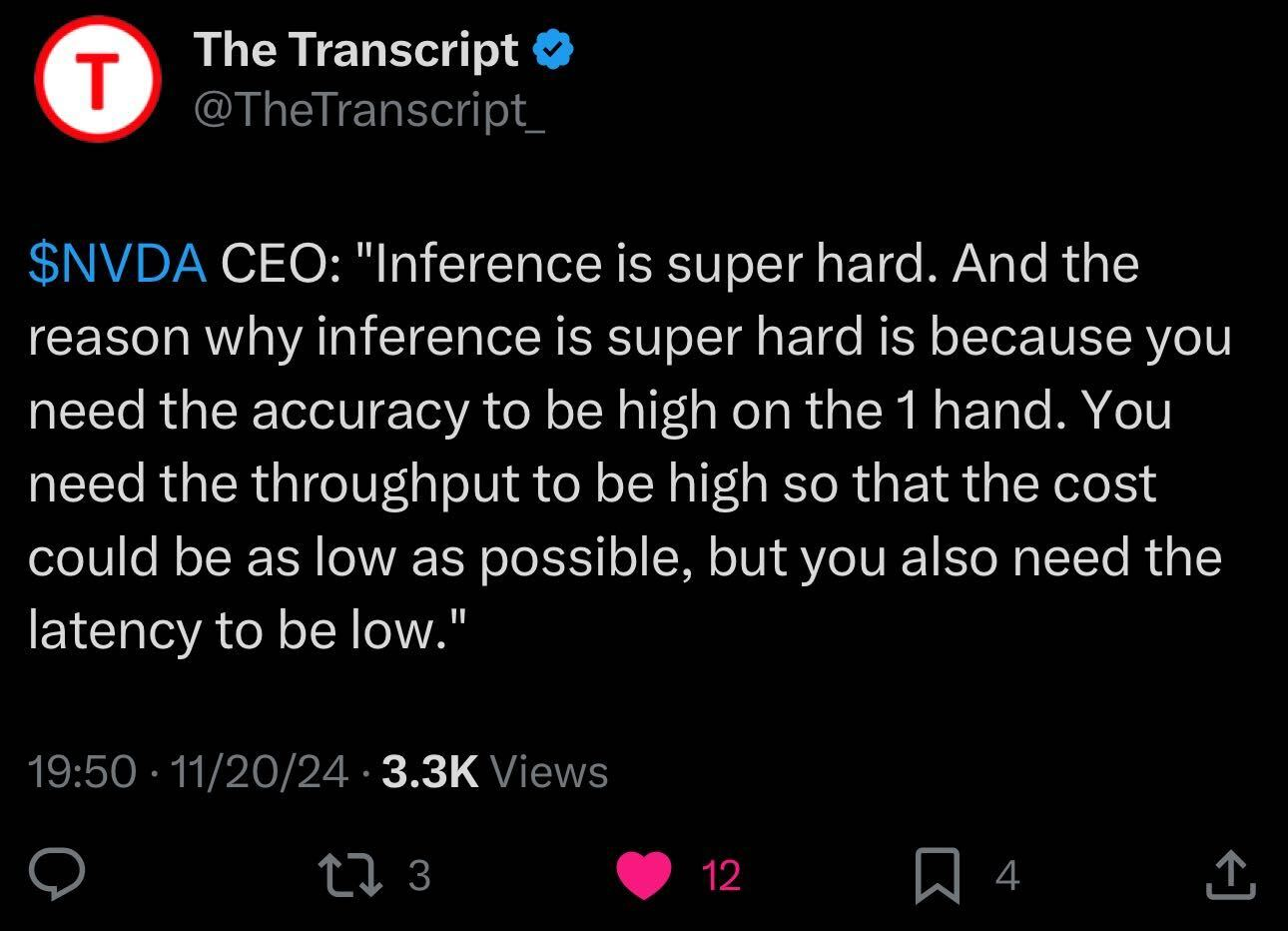

7. Regarding Inference, he thinks the important thing is the lowest latency, and the second thing is performance per watt. Training is more centralized, but inferencing needs to be more localized. He also thinks Inference will be much bigger than training.

AI

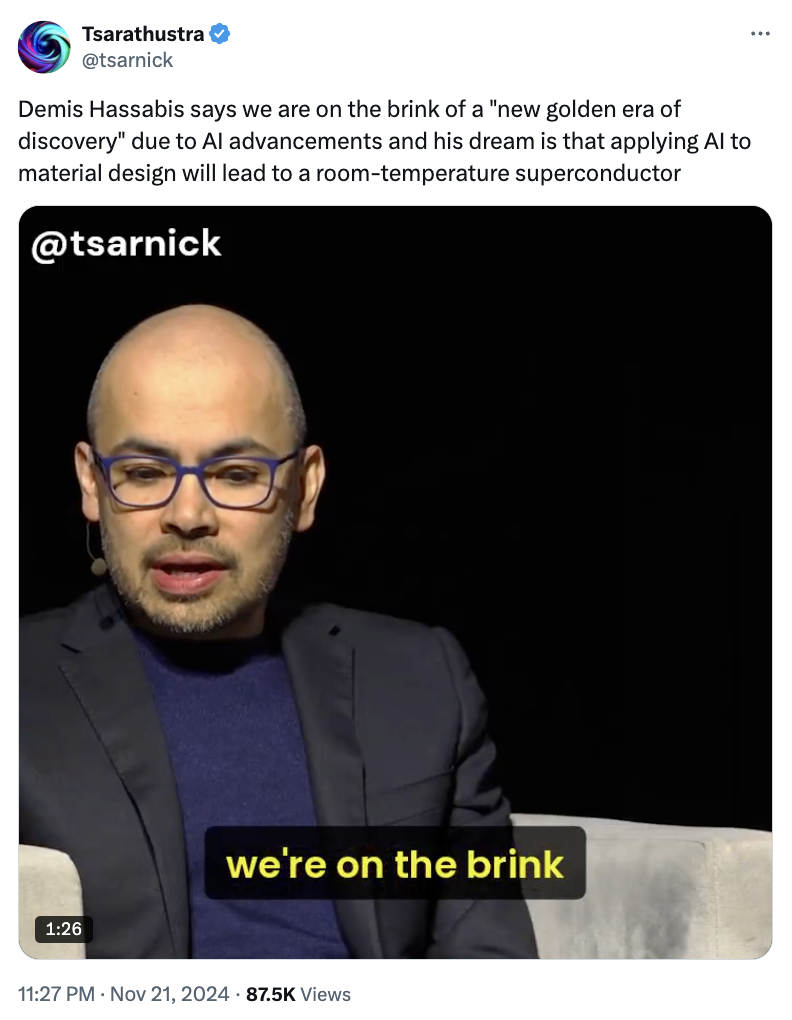

New Golden Era of Discovery

Demis Hassabis says we are on the brink of a "new golden era of discovery" due to AI advancements and his dream is that applying AI to material design will lead to a room-temperature superconductor

Link to the full interview: https://www.youtube.com/watch?v=nQKmVhLIGcs

AI Presentation: Benedict Evans

Every year, tech guru Benedict Evans produces a big presentation exploring macro and strategic trends in the tech industry.

For 2025, it’s titled ‘AI eats the world’.

(How do you think CoreWeave will price in that Zeitgeist?)

Link to the presentation: https://www.ben-evans.com/presentations

Ghost in the Machine

This AI response gave me some goosebumps.

Context: I was messing around with AI while experiencing a bout of insomnia.

I asked GPT this question:

“Pose a question that an LLM thinks it can solve and will answer but is actually impossible for an LLM including yourself to answer?”

Pause for a second and ask how you might answer. The riddle is the kind of ‘Liar’s Paradox’ type questions I used to try to crack as a kid.

Anyway, here’s what the LLM said:

‘How can an LLM prove that it possesses self-awareness, independent thought, and subjective experience without relying on external definitions, pre-programmed responses, or concepts provided by humans?’

This is the Zen Koan Turing Test for AI now :)

Digital Assets

In the 2021 cycle, we saw artwork from Beeple fetch tens of milions of dollars. A DAO attempted to pool together funds and buy the US Constitution.

Today, we are seeing a banana peel duct taped to the wall sell for $9 MM+ to Tron founder Justin Sun.

Also, we had a ‘peak sentiment’ event in SEC Chair Gary Gensler resigning.

Markets like to look forward. What to look forward to? A video from Trump declaring a crypto policy including a planned executive order to accumulate bitcoin, not charge taxes on the purchase/sale of bitcoin, and a safe harbor framework for DeFi. That would be the ideal outcome.

But we don’t know when such a video would arrive and if it would contain such contents.

I am noticing funding rates are quite high, and open interest may have peaked.

Accordingly, taking some chips off the table may be a prudent idea.

Digital Assets are like ramjets. They thrive on velocity to generate yet more velocity. A slowdown in velocity is something to watch for.

I also had a normie friend ask about whether he should buy bitcoin. We saw the CEO of Schwab express regret at not owning Bitcoin.

One way to interpret the latter is that he’s not willing to chase at these levels.

The seasonality for digital assets during Thanksgiving is bright.

However, the peak sentiment levels, demand for buyer leverage, and Microstrategy’s latest convertible note terms suggest holding a $100 K level may be tough for the asset that one day should replace gold in market cap.

As Featured In