Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we’ll cover this week:

Macro: Rate Cuts

Markets: Breadth Expansion Continues, Comcast Deep-dive

Company Earnings: Tech, Energy, & Finance remain strong

AI: OpenAI Caught in the Middle, Cohere Financing

Digital Assets: Google Focusing on Crypto

On this week’s ‘What’s on your mind? We sat down with Michael Parekh (Ex- Goldman Sachs Partner). He's a luminary tech analyst and has brilliant takes on the AI ecosystem.

We dove deep into the latest tech earnings & market reactions on Google, Tesla, and Meta Llama 3.1.

Click here for the full video, and don’t forget to subscribe.

00:01 Introduction and Michael Parekh

00:25 Tesla’s Stock and Future

03:29 Tesla’s Robots and Plans

06:14 AI and Robotics Challenges

10:18 Data for Robotics and AI

14:12 Tesla’s Financials

19:31 Tesla’s Investment Realities

22:42 Sovereign AI Models

29:08 Tesla’s Regulatory Context

33:53 Market Reactions to Tech Earnings

34:51 Google’s Earnings and Moves

44:02 Data Centers and Cloud Providers

51:08 LiDAR and Autonomous Vehicles

56:07 SaaS and Semiconductor Trends

01:02:04 Tech Investment Strategies

01:09:00 Meta’s Llama 3 and Open Source AI

01:16:12 Future of AI and AGI

01:06:36 Crypto and Politics

01:11:16 Semiconductor Insights

01:24:24 Political Influence on Markets

This Friday, we were at the NYSE as Bitwise rang the closing bell to honor the Ethereum community and commemorate the exciting journey to an ETF.

This week, we did an impromptu episode of What’s on Your Mind, as there was a lot of market activity related to some of our themes. We discussed small caps vs. semis, the consumer discretionary sector, and the momentum factors.

Plus, we've got a new team member on board who's bringing in fresh insights.

We'll uncover some major market shifts, talk about what the economy might do next, and share some potential stock picks and even crypto.

Click for the full video, and don’t forget to subscribe.

00:01 Introduction to Stein

02:16 Market Themes

06:09 Research Process

07:58 Small Caps Analysis

11:12 Consumer Discretionary Insight

18:31 Sector Flows

22:02 Economic Indicators

22:24 Consumer Strength

25:06 Impact of Trump

27:37 Reversal Factor

30:10 Momentum Factor

34:19 Tech vs. Energy

39:32 Semiconductor Trends

47:30 Sector ETFs & PE Ratios

50:07 Regional Banks

51:36 Market Insights

52:46 Stock Picks

55:18 Crypto Opportunities

Our ETF interest form is live!

Check it out here.

We’re thrilled by the amazing response so far! Thanks for all your questions and support. To help everyone, we’re adding your queries to our FAQs. Keep those questions coming!

A lot of you asked about the investing style & strategy for this ETF; here it is in brief:

Lumida employs a 'Quantamental Moneyball' strategy.

We combine qualitative judgments with statistical factors that we believe work over time based on our research.

Here’s our approach in brief:

Thematic (Top-down): We focus on long-term growth trends or "themes" that have secular solid growth potential

Fundamentals (Bottoms up): We perform security analysis at the stock level to identify the best expression for our themes

Industry Analysis: We seek to understand winners and losers based on their competitive advantage, moat, customer lock and quality of customer, market share, and profitability

Contrarian: When an industry is dislocated, we seek to find the highest quality assets that are mispriced

We seek to lead the markets and avoid names that are over-hyped and overvaluedPreference for Compounders: We prefer businesses that we can see ourselves holding over a long period of time that can also reinvest into profitable growth

Factor Aware: We incorporate statistical factor models that help us construct a portfolio that creates exposures to factors that we believe will outperform the markets, such as momentum, value, and quality

Macro Aware: We consider economic forces such as monetary policy and disruptive shifts in technology

Technical Analysis: We manage entry and exit points using technical analysis and key events such as company earnings, product launches, and macro events

Barbell Approach: We own both secular growth names that we expect will compound earnings for the long term, and quality value stocks that are ignored by the market but have attractive attributes (eg: free cash flow and buybacks, increased market share, etc)

Cross Asset Class: Although the ETF is primarily focussed on US equities, the ETF will also consider international equities or commodities exposure, fixed income, REITs etc, depending on market conditions

Tribute to The Olympics

My oldest son is now 5 years old.

He is starting to play sports.

This will be the first Olympics we get to watch together.

The Olympics represent a civilizational leap.

The games were created in ancient Greece (776 BC) to celebrate athleticism, art, and culture.

The games marked a shift from brute force to structured competition.

Nations, historically divided by conflict, found common ground in the shared language of sports.

The Olympics is about channeling aggression into something constructive - the noble pursuit of excellence.

Heroism is often misunderstood. It’s not merely about defying death; it’s about overcoming oneself.

It’s similar to the metaphor of transformation in how a caterpillar sheds its cocoon to become a butterfly.

(Greek mythology is full of transformation… See the metaphor of the Phoenix for example.)

Every athlete, regardless of medal count, is on a heroic journey in their own right.

They’ve each endured an excruciating, demanding, and often solitary journey to arrive at the world stage.

The Olympics are the stage where these heroic journeys come together.

Yet, the harsh reality is nearly everyone will experience defeat.

It’s in these moments of adversity that we discover the depth of our resilience.

Beneath the physicality is the battleground of the mind.

Psychology is the unsung hero of the Olympics.

The ability to withstand immense pressure, to channel doubt into determination…

…these are the qualities that separate true champions from also-rans.

The Olympics is a fascinating study in human potential.

I often say ‘you make your money on the buy.’

The same is true in athletics. Preparation is everything.

Champions are confined to the crucible of training for many years for a competition that may last 15 minutes.

Their only satisfaction is in defeating their own best time.

I hope to introduce my son to the ‘athletic mindset’.

It’s about summoning an inner spark each day despite the harsh reality of a sometimes confused and cold world.

Most importantly, it’s about a growth mindset—the belief that abilities can be developed through dedication and hard work.

(Folks like Carol Dweck and David Goggins have articulated this philosophy with unparalleled clarity.)

As I watch my son take his first steps in sports, I'm reminded that the true spirit of the Olympics is about striving for excellence and inspiring excellence in one another.

I hope to instill in him a love for the journey and a determination to push beyond his perceived limitations.

In the end, it's not the medals we win that truly matter, but the struggles we overcome and the person we become through striving.

Macro

Mr Market now has a 100% rate cut probability in September.

This is the first time we agreed with Mr Market and shared rate cut views a few weeks ago.

We have been consistent on ‘higher for longer’ fading pivot talk, while Wall Street liquidity junkies have been consistently wrong.

Rate cut hopes are why small caps are cranking…

This melt-up is driven by earnings expectations and Fed expectations.

I could see insurance cuts in September…

Small caps and midcaps should do well if that’s true.

The Thursday before the GDP print, our view was that the economy is normalizing from a heady 6% nominal GDP growth rate:

Friday’s GDP confirmed our view. The communications sector led the way with a bevy of breadth expansion.

The reasoning is simple. If GDP is growing, then corporate earnings and personal incomes are growing.

That’s good for small caps and midcaps.

We also wrote in late April the following:

Keep it simple. Corporate earnings are strong, and personal real incomes are still rising. We just finished a year of 6% nominal GDP growth.

Productivity rates are improving, and bank credit growth has yet to expand. And those banks are now healing as rate cuts come into view.

We will see another economic scare in September - it happens then I theorize because ‘back to school’ scrambles summer behaviors and spending data.

MARKETS

Back to communications.

Funny enough, we happened to buy Comcast Friday morning at the open. We’ve been mulling over this name for a few months.

We share our thesis below.

Non-Consensus Pick: We Are Long Comcast

We believe Comcast is a stock that will generate mid-teens returns over the next few years.

Let’s start with the bear case.

Declining Cable Membership: Comcast is seeing cable membership numbers in decline. This is a significant concern as cable has traditionally been a major revenue driver for the company.

Fiber Competition: Comcast has been losing ground to Fiber. Competitors offering fiber-optic internet services are attracting customers with faster speeds and more reliable connections.

Cord-Cutting Trend: Comcast has been on the losing side of ‘cord-cutting’. Customers are canceling cable subscriptions and moving to a range of streaming services for their content, reducing Comcast's cable revenue.

Adoption of Alternatives: There is a growing adoption of alternative TV services such as YouTube TV. Customers are finding these options more flexible and cost-effective. (I am a customer, love the product!)

Technical Weakness: Technically, the stock is also in a downtrend with the 200-day moving average in decline. The stock is down 9% YTD.

So, what’s the bull case?

We like to find stocks that have a Story, Good Fundamentals, a sound technical entry, and factors we like.

Let’s cycle through each component.

First, let’s start with the big picture.

Comcast and Charter Communications are in a duopoly.

We prefer monopolies, but we’ll settle for duopolies (Visa is another name we own.)

That’s notable as the moat is significant. It requires tremendous capital investment to create the assets Comcast has.

Comcast has an answer to cord-cutting.

Comcast has introduced a new bundled streaming package called Xfinity Flex.

This is a streaming service for Xfinity Internet customers that integrates various streaming services on one platform at no extra cost.

The offering packages popular streaming services (Netflix, Netflix, and Apple TV) free content from Peacock, and other free channels and live sports options.

The product is called Now TV and it will be available for $30 with upgrade options.

That’s a strong customer value proposition - a key element to assess when investing in a business.

Now, it’s crucial to ask yourself is Comcast is a value trap.

A value trap is a business that is in structural decline. You can sometimes see this with revenue and earnings growth decline.

That’s not the case.

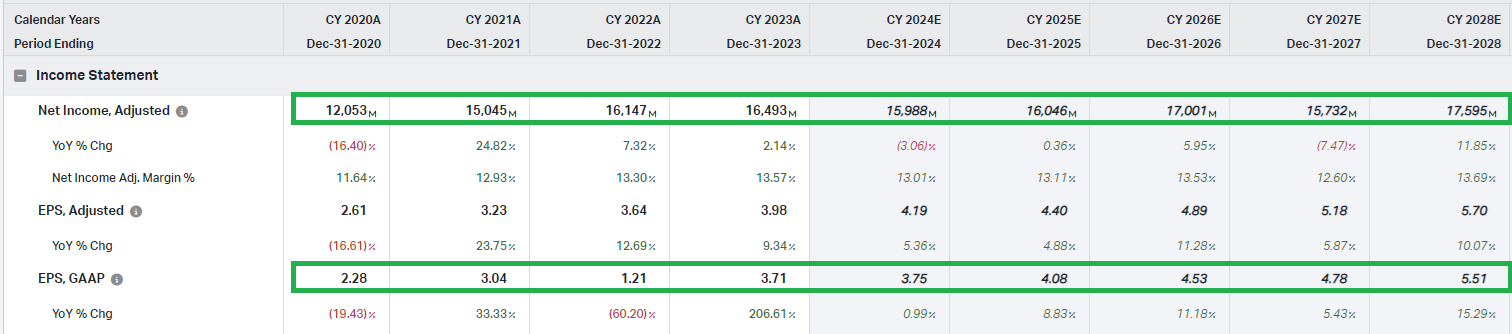

Comcast is growing revenue and earnings - take a look.

On revenue, Comcast has continued to grow revenue and is projected to do so at a tepid pace going forward.

We like that pattern - namely, low growth expectations relative to recent growth.

Analyst expectations are low, this is a low bar for Comcast to cross.

Take a look at earnings.

Notice earnings per share is growing at a faster rate than earnings.

If consensus analyst expectations are right, then Comcast earnings per share will increase 50% in 5 years.

How are earnings per share increasing faster than net income?

Buybacks!

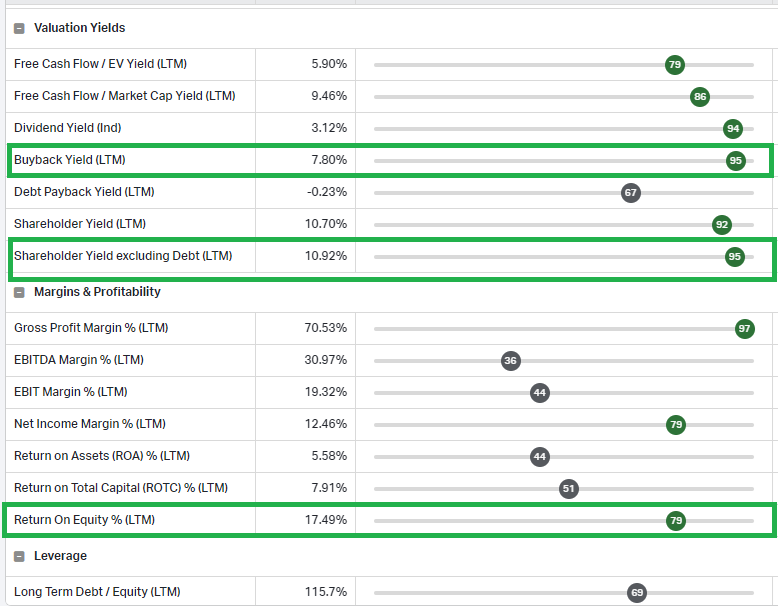

The buybacks is a core part of our thesis.

This chart shows Comcast’s buybacks compared to free cashflow per share.

Management did not buy shares during the 2020 and 2021 eras, when stock valuations were high.

Since 2022, management has accelerated the pace of buybacks.

The buyback yield is unusually high, as is the shareholder yield of ~11%.

The shareholder yield is one way to approximate your average annual return assuming no multiple expansions.

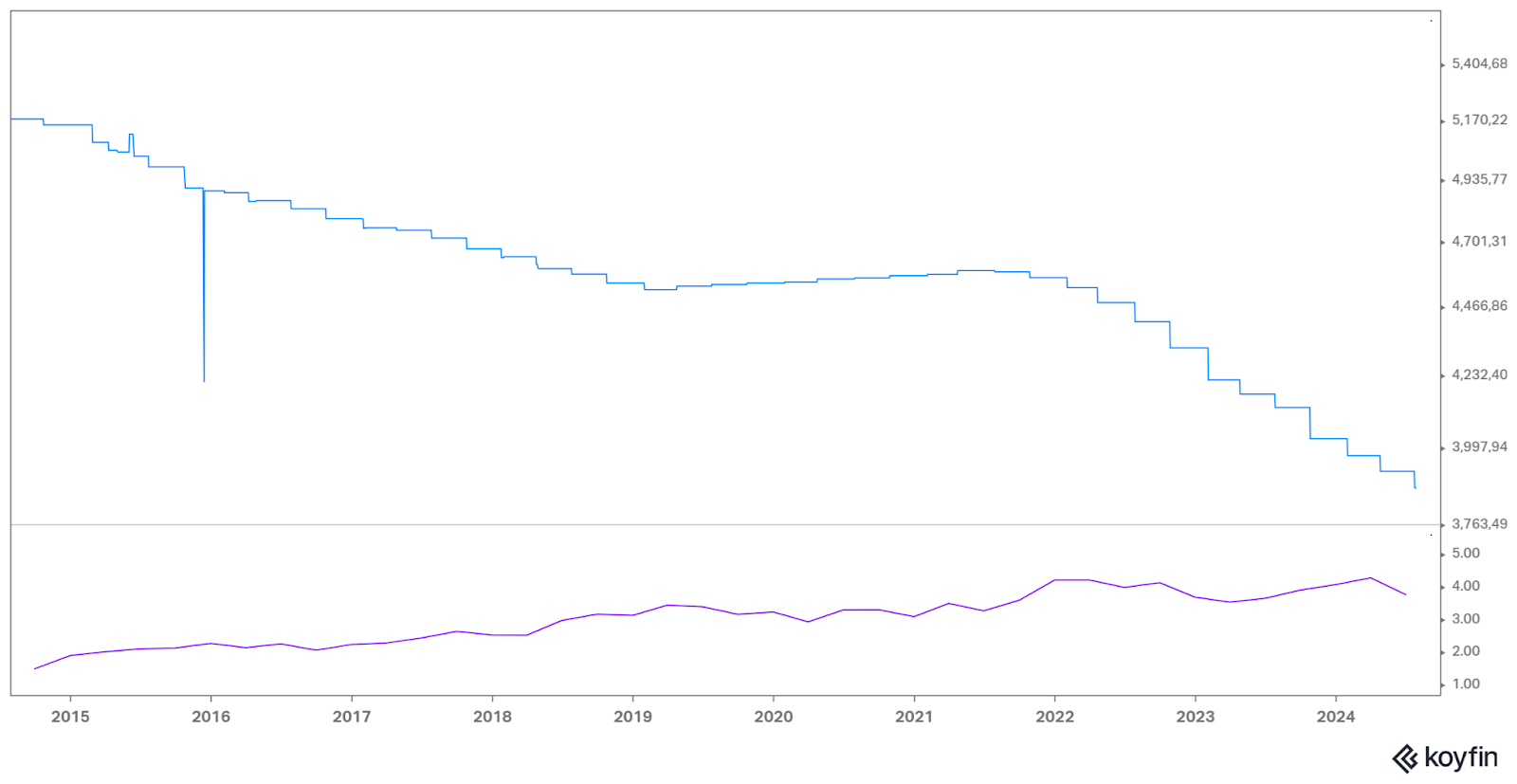

Comcast’s trailing PE ratio is unusually low. Here’s a 10 year chart showing PE ratio since 2008.

We believe the green line represents a historical valuation (~15x) that this asset will mean revert to over time. (And hopefully overshoot).

That represents a potential return of 60% from multiple expansion over 3 years or so.

Competitor Charter communications has a PE ratio that is 16% higher. Also, Charter reported earnings this Friday - the stock jumped 16%.

We like to see the ‘theme’ as a whole rallying.

Combine that with the 11% shareholder yield and we believe there’s a good opportunity for mid-teens performance.

Why would you own a bond when you can own a business like Comcast? It’s literally buying back stock and paying you dividends, and as a real asset has its own inflation hedge.

We also like the 17% return on equity.

However, we wish it were closer to 20% - a Buffet type threshold.

The trailing PE is at 9.3x.

In sum, we believe there is a double-digit equity return from: buybacks, earnings growth, dividends and multiple expansion.

The risks are increased competition from “fixed wireless” solutions. Players like AT&T, Verizon, and T-Mobile.

These firms are tapping newly accessible “C-Band” spectrum to offer broadband wirelessly.

It’s going to take time, and a lot of capital, to bring these competing services to urban and rural areas. The C-band services are targeting major cities first.

This is certainly a risk to continue to monitor.

Even if you can get WiFi from a C-Band provider, you still need to subscribe to a bundle of streaming services.

Therefore, Comcast’s strong customer value proposition will help.

We are continuing to research the speed at which C-Band can roll-out and customer adoption rates.

In the meanntime, however, with the Olympics and also this technical entry we thought it was a good idea to establish an entry.

See those long wicks highlighted by the green circle? That indicates strong buyer demand. It looks to us that seller exhaustion is mostly behind us.

The stock may move like CVS:

CVS has had a strong performance since our May call - but the volatility will find a way to frustrate investors with fake breakdowns along the way.

Lastly, here’s a table of comps comparing Comcast (CMCSA) to peers.

How does Comcast compare to other opportunities?

Several of the small caps we shared last week we believe have better upside potential this year - especially those with massive buybacks and low multiples (like Jackson Financial and Enova)

However, a 2% to 3% allocation to this name seems reasonable as the ‘catch up trade’ and value rotation start to broaden to Communications.

If you are looking for a wealth management partner, Lumida is now welcoming a limited number of new clients.We offer a range of services, alternative investments (such as our CoreWeave deal), white-glove crypto management, to public equity management, and high-touch family office services, including trust, tax, and estate planning.

Ready to explore? Click here to fill out our form to start the discovery process.

Interested but not ready to commit? Build a relationship with Lumida and stay informed. Click on the poll below if you want our advisors to reach out.IS CROWDSTRIKE THE NEW EQUIFAX?

Context:

Crowdstrike’s valuation is down to a nosebleed inducing 72.8 forward earnings after last Friday's outage

It's current price to sales is 22x after another large down day (13%+) after CathieDWood gave the stock the kiss of death.

Thoughts:

(1) If you stick to the rule of don't buy stocks that try to move faster than the speed of light (e.g., NVDA) you will avoid a lot of brain damage from incidents like

Crowdstrike was priced for perfection.

Aren't there better ideas out there?

Wouldn't a name like ASML or MU or QCOM or NVDA outperform a name like CRWD due to multiple expansion opportunities?

(2) Gene Munster's point is that cybersecurity platforms like Crowdstrike are sticky - switching costs are high.

So that July earnings will be fine.

That's true for existing customers...

BUT...

The primary driver of valution for a go-go growth stock is future earnings growth.

The vast majority of a growth stocks valuation can be explained by long-term stream of future earnings

Is there a CIO that's going to stick their neck out on the line here?

Or, do new customers choose Palo Alto Networks PANW which has a platform solution instead?

(3) Equifax brings to mind a similar face planting type historical reference.

The Equifax self-own was publicly disclosed on Sept 7, 2017

The stock took 6 days to bottom. The 4th day was the worst down day.

The stock then had a V-shape recovery lasting 2 to 3 weeks recovering almost 50% of the losses before chopping around for a month or so...

The stock came close to recovering its all time high one year and change later, but never quite got there.

Then Equifax re-tested its 2017 lows in December 2019 due to new on-going regulatory scrutiny, congressional inquiries, and significant fines and settlements.

A key question: Does Crowdstrike face any similar liability? (Certainly not the same magnitude)

For the record - I don't believe Equifax faced serious consequences for breaching customer data and privacy.

The Equifax data breach is another reason why consumers should own their data and then can license their data to credit bureaus -- all managed on-chain...

See attached charts of EFX and CRWD

Non-Consensus: General Motors

Our boomer stock GM beat expectations on earnings

Year-to-date GM is up 23% - beating most Mag 7 names.

GM is beating nearly all the tech and SaaS names and even our tech picks META and GOOGL picks (except NVDA).

GM is another stock no one is talking about. GM stock sold off after Ford’s lousy earnings.

GM has far better metrics. Ford is losing $5 Bn a year due to its F-150 EV truck experiment which lacks product market fit. (Tesla is winning the EV truck market, and its sales are lousy overall.)

We believe now is an attractive time to buy GM.

If you think you can only grow wealth only through tech you are missing a universe of opportunities

Someone forgot to tell GM only Mag 7 stocks go up in this market.

Why GM?

Non-Consensus & overlooked

1) buybacks and $9 Bn in free cash flows on a $55 Bn market cap

2) low 5x PE (multiple expansion)

3) market share growth / capture from rivals (leadership)

4) Hated during the UAW negotiations…and yet, GM still makes plenty of money (non-consensus)

Not the best entry here, but keep on your radar

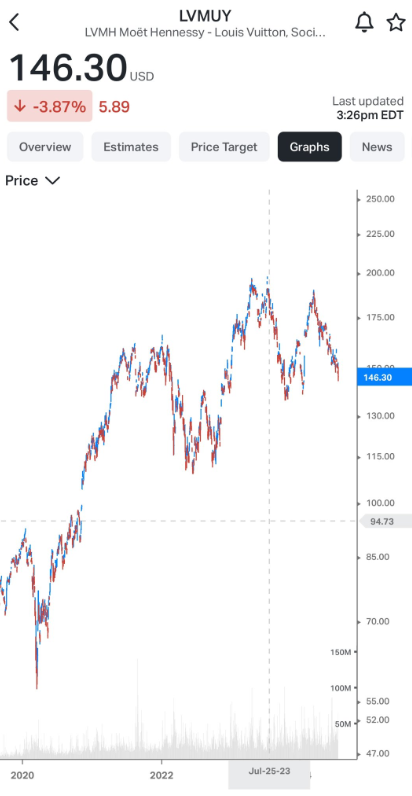

LUXURY RETAIL BEAR MARKET

I can’t get my head around why handbags, and the manufacturers that make them, are so expensive.

Luxury YOY sales growth flattened in July of 2023 .

That was near the top for these luxury brands.

Since then LVMH and others have been in a bear market.

Imagine if one paid attention to these growth trends and rotated out of harm's way when fundamentals deteriorated.

Most ETFs are mechanical or silos - they don’t have a cross-asset class approach.

If https://www.LumidaETF.com gets to $100 MM in commitments, I intend to launch that.

(Plus, it will poke an eye into all of the mediocre hedge funds charging insane fees)

My conviction in a tax-efficient ETF vehicle is growing and is highly relevant in today’s markets.

Other thoughts…

Hermes is in a quiet bear market. It’s PE is higher than NVDA

And revenue and NI growth is less than 20%

That 20% growth number is the price of admission to the growth stock multiple club.

If a stock can’t hit those numbers, I don’t believe it deserves a growth multiple.

Hermes downtrend is less vicious than its competitors despite its price due to earnings growth.

LVMH appears so well-bid that it behaves like a bond.

Not as much downside, but not as much upside either due to 44x forward PE.

Retail has been in a bear market in virtually any corner…

Themes tend to bottom together.

Look at the correlation across LULU ULTA NKE HESY LVMH DLTR

Luxury or mass affluent or Dollar Store - doesn’t matter they ride the same tide.

And some of those waves appear to be troughing.

TESLA AND EVs REMAIN IN A BEAR MARKET

Take a look at Tesla after our warning call.

The red line on the chart is when we noted call option buying was approaching excessive levels.

The stock is down 11% on weak earnings.

Look out for an earnings inflection point in the EV category.

Until then the EV market remains in a bear market.

The dramatic Tesla bounce we saw since last quarter was mostly technical: bad news was priced in, sellers were exhausted, and there was hype around robo taxis and FSD approvals in China

I also have attached a 3-year chart of Tesla. You can see the stock is gradually compressing.

Kind of amazing how Cathie Wood timed those Tesla buys near the peak of the market.

Company Earnings

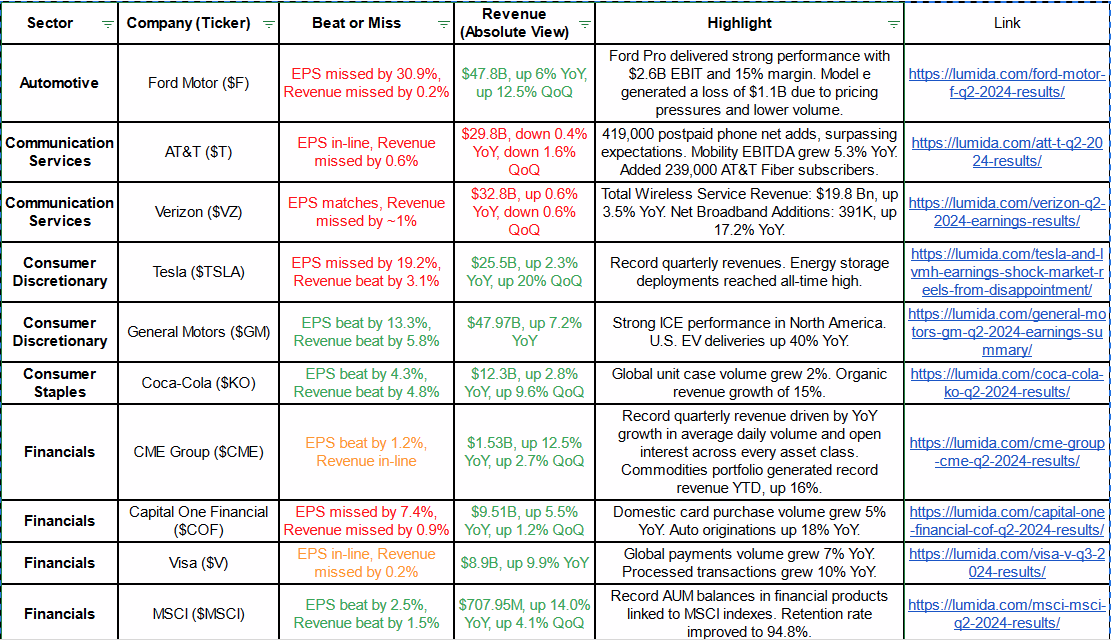

Automotive:

Ford Motor (F): Missed both EPS and revenue targets. Revenue grew 6% YoY. Ford Pro performed well, but Model E struggled with losses due to pricing pressures. Highlights that the consumers may be sensitive to price increases in electric vehicles.

Communication Services:

AT&T (T): In-line EPS, slight revenue miss. Added 419,000 postpaid phone subscribers, strong Mobility EBITDA growth. Highlights the growing demand for high-quality mobile services and fiber internet.

Verizon (VZ): EPS in line, revenue slightly below expectations. Wireless service revenue up; strong broadband additions. Highlights the stable demand for connectivity services, with a focus on broadband growth.

Consumer Discretionary:

Tesla (TSLA): Missed EPS, beat on revenue with record highs. Energy storage deployments surged. Highlights the growing interest in renewable energy solutions alongside electric vehicles.

General Motors (GM): Beat on EPS and revenue. Strong North American performance and EV growth. Highlights the increasing consumer adoption of electric vehicles and robust ICE vehicle demand.

Consumer Staples:

Coca-Cola (KO): Beat on both EPS and revenue. Global unit case volume and organic revenue grew. Highlights the steady demand for beverages, with potential growth in premium or health-focused products.

Financials:

CME Group (CME): EPS beat, revenue in line. Record revenue driven by growth in trading volume. Highlights the heightened interest in diverse investment products.

Capital One Financial (COF): Missed both EPS and revenue. Growth in card purchase volume and auto loans. Highlights that the Consumer credit activity is increasing, potentially signaling economic confidence.

Visa (V): In-line EPS, slight revenue miss. Payments volume and transactions grew. Highlights the Continued rise in digital and cashless transactions.

MSCI (MSCI): Beat on both EPS and revenue. Record AUM and high retention. Highlights the growing interest in indexed financial products.

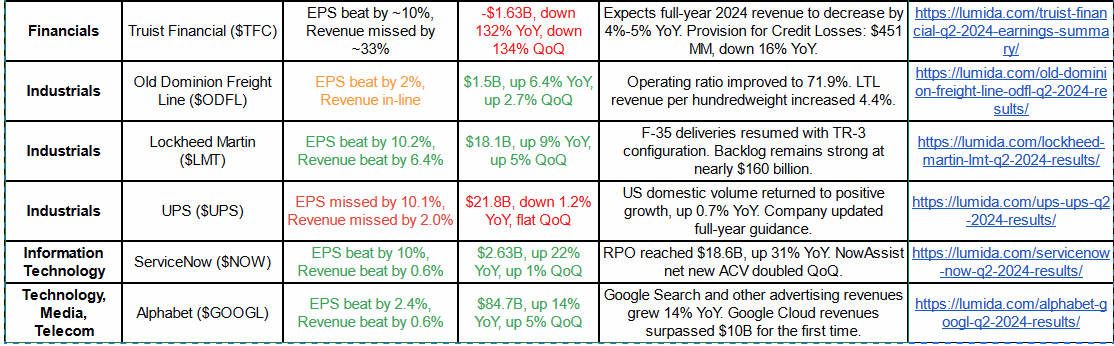

Truist Financial (TFC): Beat on EPS, significant revenue miss. Guidance suggests revenue decline. Highlights the challenges in the financial sector, possibly due to economic conditions.

Industrials:

Old Dominion Freight Line (ODFL): EPS beat, revenue in line. Improved operating ratio. Highlights that Efficient operations are crucial in a competitive logistics market.

Lockheed Martin (LMT): Beat on both EPS and revenue. Strong backlog and resumed F-35 deliveries. Highlights the Continued government and defense sector demand.

UPS (UPS): Missed on both EPS and revenue. Domestic volume growth, updated guidance. Highlights the Fluctuating demand in logistics, potentially linked to consumer spending patterns.

Information Technology:

ServiceNow (NOW): Beat on both EPS and revenue. Strong growth in RPO and NowAssist. Highlights the Increasing enterprise demand for digital transformation and automation tools.

Technology, Media, Telecom:

Alphabet (GOOGL): Beat on both EPS and revenue. Growth in ad revenue and Google Cloud. Highlights the Rising digital ad spending and cloud service adoption.

AI

Bloomberg: Enterprise AI Focused Cohere Raises a $5.5 Bn Round

Highlights:

- Revenue of $35 MM ARR, up from $13 MM ARR end of 2023

- $5.5 Bn valuation implies a 150x (ish) price to sales multiple. 2x valuation from last year

Investors:

The company has raised $500 million in a Series D funding, it plans to announce on Monday.

The round was led by Canadian pension investment manager PSP Investments, alongside a syndicate of additional new backers including investors at Cisco Systems Inc., Japan’s Fujitsu, chipmaker Advanced Micro Devices Inc.’s AMD Ventures and Canada’s export credit agency EDC.

Customers: Cohere has customers across a wide range of industries.

They include banks, tech companies and retailers.

One luxury consumer brand is using a virtual shopping tool Cohere built to help workers suggest products to customers. Toronto-Dominion Bank, a new customer, will use Cohere’s AI for tasks such as answering questions based on financial documents

Sourcing:

Cohere’s models can be used across 10 languages, including English, Spanish, Chinese, Arabic and Japanese, and its models can cite sources in answers.

OpenAI is ‘caught in the middle’

That means they are flanked by competitors who have greater customer focus

On one side: Meta is free and will soon be state of the art with Llama 3.1

And when you consider Meta’s training dataset and distribution channel and zero fee (and loads of capex) — it’s hard to see how OpenAI can catch up

So OpenAI must focus on Enterprise

On the other side: Cohere is single-mindedly focused on Enterprise

And so is OpenAI’s parent Microsoft

And so is Palantir

OpenAI was the ‘hot deal’ last Fall.

It won’t be the ‘best deal’.

The best deal in the fall was the infra play: CoreWeave or just owning capex receivers like NVDA ASML TSM KLAC LRCX AMAT

Digital Assets

Interesting tweet from our friend Yano

THE OVERTON WINDOW HAS MOVED

There was speculation that Candidate Harris is speaking at the Bitcoin Conference?

Will the admin terminate Chair Gensler?

Isn’t that the only action that counts?

Two Presidential Candidates are competing to win the affections of crypto natives at the Bitcoin conference.

Both flip-flopped in the pursuit of political expediency

However, Trump did appoint Brian Brooks as head of the OCC, which opened the door to Anchorage, an OCC chartered bank, getting a banking license to custody digital assets, and Coinbase went public before Chair Gensler was sworn in…

…who subsequently denied the ETFs that are now currently trading due to litigation via the court systems

The courts sided with issuers and ruled the SEC was not ruling by law, and admonished the SEC for making up facts

If Biden & Harris are serious, they should terminate Chair Gensler

Explore becoming a Lumida Wealth client: learn more about our Crypto White Glove Service or Click here to explore our Wealth & Family Office Services.

Lumida Curations:

In case you missed it, here are some of the best curations from Lumida Wealth on Twitter.

Be sure to follow Lumida Wealth on Twitter, and on Youtube, where you can get more such curations.

Instead of watching hour-long market podcasts - we distill the key insights in 1 min shorts and serve them in threads.

The goal is to maximize insight per unit of time.

Dive into expert insights and market trends from Wall Street Week.

Snippets from our WOYM episode

Click here to explore becoming a Lumida Wealth client

Quote of the Week

“The best time to invest is when you're afraid.” – John Templeton.

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.