Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we’ll cover this week:

Macro: Fed’s Bostic Capitulated, Mortgage Rates Declining, Consumer Discretionary

Markets: LPL Financial, US Consumer is Alive and Well

Company Earnings: eCommerce growth

AI: China & Humanoids, Chatbot CFA

Digital Assets: How effective Candidate Harris and the DNC is at message control?

This week all the hedge funds filed their 13Fs.

We were ready with our quarterly whale watch tracker. We analysed the top moves from 46 Hedge funds to identify over crowding and themes to look out for.

Don’t forget to watch our episode dissecting these moves.

We’ll also have some high-level commentary in this weeks newsletter.

00:00: Overview of 13F filings and hedge fund strategies.

01:46: Positive economic indicators and S&P 500 sector analysis.

02:57: Highlights of hedge fund managers' holdings and company positions.

04:37: Key hedge fund holdings in Amazon and Nvidia.

07:19: Valuation insights and sector preferences in tech and biotech.

09:22: Global bets and sector-specific strategies by hedge funds.

11:19: Strategic rotation towards undervalued assets.

13:30: Debate on transportation and retail sector investments.

17:44: Corporate strategy challenges in cloud services and retail.

24:09: Hedge fund investment strategies and market speculations.

28:02: Value investing insights and stock analysis.

32:52: Examination of hedge fund holdings and equity approaches.

37:48: Broader market and industry analysis, including healthcare.

42:09: Investment sentiment on media and technology stocks.

48:17: Hedge fund strategies and shifts in top positions.

52:28: Home building and investment strategies.

55:14: Out-of-the-norm investments by Michael Burry.

56:14: Sophisticated energy investments and valuations.

57:52: Expanding content and community engagement efforts.

You have heard the expression of how Bulls are fighting Bears.

It’s as if there is a tug of rope and the two sides are fighting.

That’s not what happens.

The truth is cold and dark.

Bulls become bears, and bears become bulls.

Bulls also become exhausted, and so do bears. When they throw in the towel (e.g., ‘capitulate), they join the other side.

A bear becomes a buyer covering their short, and a bull becomes a seller when they can’t stand the pain.

That person in the foxhole next to you? The person who swears they are buying such and such a stock on social media?

They can flip to the other team at anytime.

And, the more crowded your team is… well that’s the period of peak vulnerability.

The solitary individual on the other side, by definition, is selling a top, or like Buffett in October 2008 is buying a bottom.

You can only lose ground when you are fully priced and Consensus.

Another way to say all of this: you can’t under-estimate the psychology that underpins ideas and markets.

A quote i love from commander Chesty Puller:

‘Men, the enemy are in front of us, behind us, and to the left and right. They aren’t getting away from us this time’.

Have I told you my March 2009 story?

I was at a social event in NYC with a bunch of investors.

We were exiting a brutal winter and the worst bear market in my living memory.

In March 2009, everyone by that point was a certified PHD macro economist and an expert in subprime securitizations.

Just like everyone became at the Yen carry trade this past week.

I was also bearish.

And I could tell you a crystal clear argument (balance sheet recessions and so forth).

The reasoning in my mind, and that of everyone else at the party, was obvious.

Then I realized everyone in the room was bearish.

That was the ‘a ha’ moment.

I switched teams.

Many memories like this stamped in my memory.

October 2011 is another one. That was shortly after the U.S. AAA debt was downgraded. We also had the Euro Greek debt crisis.

When I was at Merrill in the early part of my career, I noticed that markets tended to bottom when the back office team ordered in pizzas to clear and settle trades sold in a panic.

That was usually the best time to buy.

There is a term in warfare called the ‘culminating point’

This term refers to the stage in an operation where a force achieves its peak combat power and effectiveness, but from that point onward, it begins to lose momentum - the ability to sustain the offensive.

At the culminating point, the force becomes most vulnerable to over extension.

The culminating point manifests when you start to see parabolas take shape, when prices are dislocated from intrinsic value, or when the sentiment is lopsided and priced in.

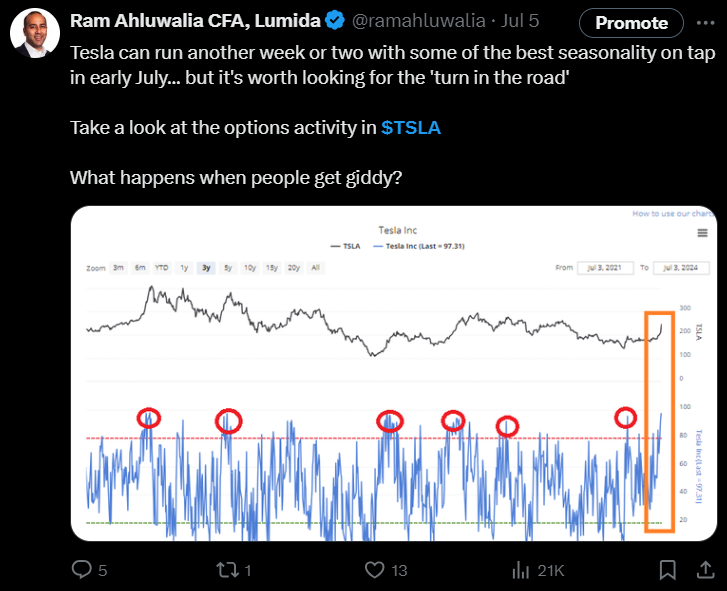

The culminating point in Tesla was noted in this post here on July 5th. Indeed, Tesla - a great proxy for animal spirits and speculation - topped along with the broader markets one or two weeks later on July 16th:

There’s an implication to the idea that contrarians are out-numbered but have unusual advantage.

They are not running over each other when they head for the exit or FOMOing and paying high prices.

This means that all contrarian investors are by definition value oriented.

Value names have less crowding… that’s why they have value!

When I see self-described contrarians on Twitter pushing stocks like Tesla, SoFi, or Palantir “because they are hated” - despite stratospheric valuations - I have to chuckle as these are not contrarian ideas.

A contrarian idea is buying JP Morgan, and at the same time, buying Bitcoin during the banking crisis. That was a lonely at the time but highly profitable contrarian idea.

Contrarian ideas involve a dent & scratch somewhere. Or, the idea is not the shiniest new new thing which is crowded & pricey (like OpenAI last round).

Now OpenAI needs to raise money - and dilute shareholders - as they are blowing billions on GPUs. Better move would be to buy CoreWeave.

A contrarian also manifests certain personality traits.

Look at Buffett.

He lives in Omaha. He is physically away from the crowd.

The jets fly to Omaha, not the other way around.

Buffett’s lifestyle is fairly drab and ordinary.

He enjoys cherry coke and burgers.

His leisure activity is playing bridge. It’s not kite-surfing or Formula 1 car racing. He plowed his wealth back into Berkshire.

Buffett’s social circle fairly dry and boring (in the best of ways).

The other quality of Contrarians?

They are highly obsessive, competitive, and analytical.

Look at Michael Burry in The Big Short. Remember the scene where he is crawling on the floor looking for FICO scores?

You need to be highly analytical to have a variant perception from the crowd.

The Consensus is generally on the right idea - indices do go up after all. But, alpha requires a non-consensus views.

Non-consensus views come with heavy social costs.

Remember when Michael Burry’s LPs wanted to redeem on one of the greatest trades of all time?

Contrarian investing requires deep analysis…otherwise it’s just a weird kind of mental illness.

Example: We’ve owned Nvidia for a while. Sometimes the obvious thing to do is the right move.

Contrarians need analysis.

Buffett studied insurance actuarial tables early in his career

Munger was always compiling mental models.

Contrarians are highly analytical. They are less prone susceptible to ‘stories’ which characterize so many growth stocks today - like Tesla or Palanatir.

Another key quality: Contrarians also have Delayed Time Gratification.

The contrarian believes that ‘you make your money on the buy’.

That means the value creation was at time of purchase. The contrarian seeks to purchase assets below intrinsic value.

Then they wait.

That’s what we did with ETHE last year when it had a 40% discount, or JP Morgan or UBS.

This year that would include CVS (aka Aetna), LPL Financial, and Comcast.

The opposite of a contrarian is an easily excitable trigger based momentum trader.

The crucial quality for a Contrarian investor is Temperament.

As Buffett notes: ‘You need a stable personality that neither derives pleasure from being with the crowd nor against the crowd’

There are tens of thousands of Wharton Grads and CFA charterholders with great analytical skills.

Most are ‘me too’ herd followers. Only a small fraction go on to be strong investors.

The dividing line is temperament.

Counter Signal

I have learned to test contrarian ideas by running them smart investor friends. When they hate it, it usually means I am on to something.

More AUM doesn’t mean more performance.

This week, we learned the Saudi Sovereign Wealth fund is one of the largest shareholders in Twitter.

That means they have lost something like 60 to 80% on their initial top of the market investment.

The Saudi SWF doesn't have a great track record.

Remember, Saudi's SWF was a ~10% shareholder in Credit Suisse...

...before they accidentally destroyed the business by announcing they would not inject new capital.

Credit Suisse was then sold to UBS. (I promptly bought UBS after that sweetheart gift / sale. Investing in the acquirers of failed banks is a great strategy.)

I believe the lesson from all of this is....

The more access you have to gifted story tellers like Elon Musk, the worse your performance.

This explains why the crew on the All-In Podcast seems to have awful ideas - like owning Tesla, or pitching Bitcoin to the day at the top of the market.

Consider Cathie Wood.

She interviewed SoFi's CEO on her podcast at $9. And then she started sold SoFi in the $6 just a few months later.

Warren Buffett did the opposite.

Buffett would avoid management. Management is charming.

Buffett would interview competitors in a target industry. He would ask them who they thought the best-in-class run firm was amongst the competitive set.

That's how he found Geico.

I believe this also explains why certain locations - like Hollywood - are full of notoriously bad investors.

They are surrounded by glam and celebrities.

There’s too much noise that masquerades as signal disguised by social proof.

There is no they are investing into an idea like Chenerie or CoreWeave latest deal.

Instead, they will pass the hat around and invest in a hype deal like OpenAI.

The buzz around them will always be in hype names like OpenAI.

You can't stand out from the crowd if you are a part of the crowd.

Or, look at Harvard's endowment. The performance is atrocious.

The Committees at these big institutions lead to sub-optimal after the fact decision-making.

The best alpha is thinking for yourself.

Brad Jacobs and QXO

I was teasing for a month or so that we found our next Coreweave.

Very selectively, Lumida finds a private deal where we expect a nice risk adjusted return in hopefully quick order.

CoreWeave was an example of such a deal. We did that deal while saying no to OpenAI, xAI, Antrophic, and a whole host of other hype deals.

Proud to report that we just entered and exited our second deal: investing in Brad Jacobs next roll-up.

We bought in via a private placement at $9.14 cents in July near the top of the market (it was a nice rotation from overbought equities). Then we sold over the last two weeks.

We are still calculating the returns - it looks like a 20% before incentive fee.

What we found attractive about this deal was the asymmetry.

We didn’t see a real risk of principal loss. The downside was maybe we make only 10% in a short period of time with no material lock-up.

The upside is we make 200%.

Some confusion in the market around the filing of QXO’s registration statement (had an undisclosed number of shares) combined with market dislocation meant we walked away with a high-teens return.

I expected more… but if I could pull that off every months, we’d do it every time.

We separately bought QXO as a long-term position. We’ll share that thesis in another newsletter.

Macro

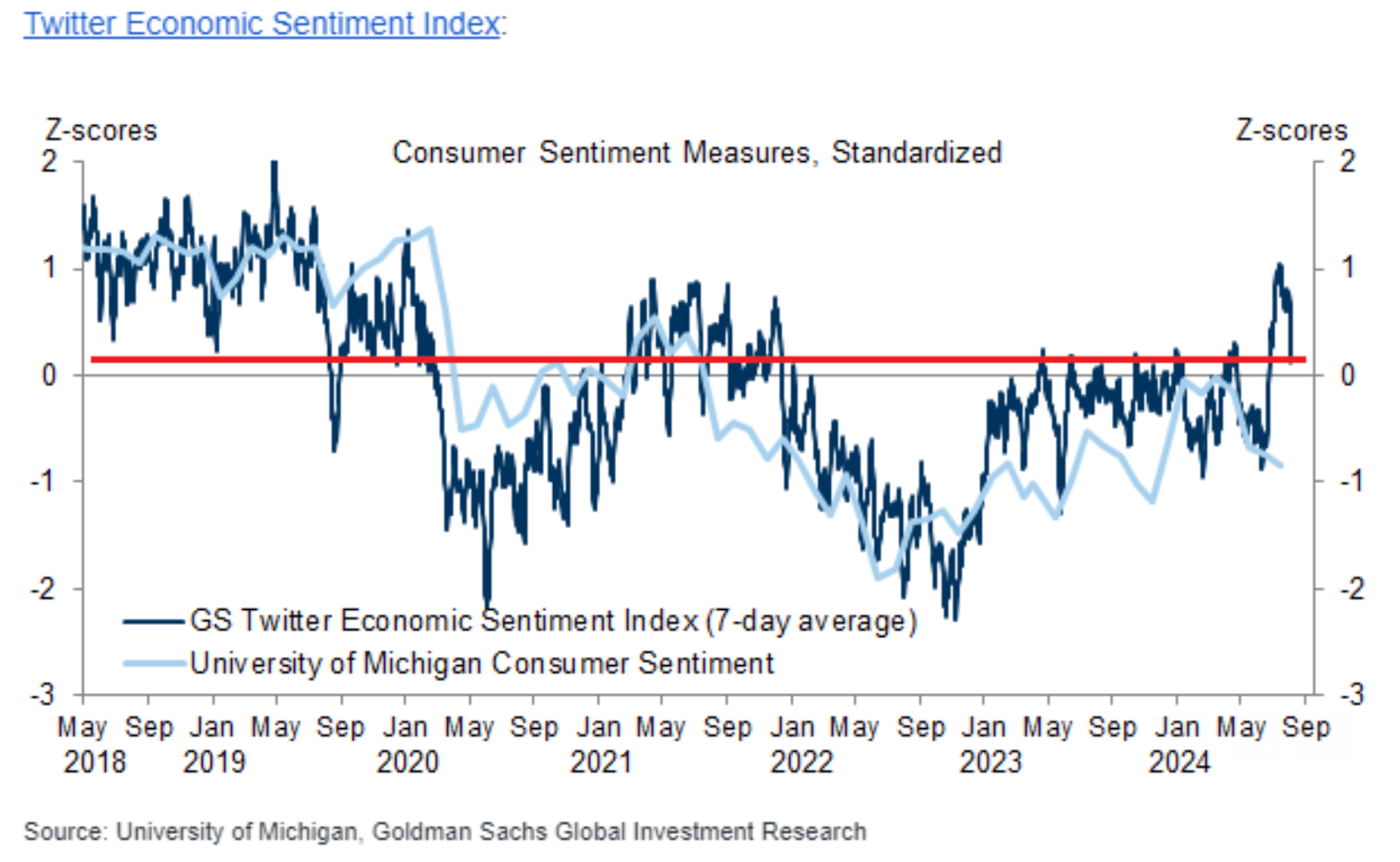

Goldman's Twitter Sentiment Index dropped sharply in the last week.

That’s good news. As we noted last week or two ‘Narrative Follows Price’.

It’s good to see sentiment work itself out. That means more cash on the sideline which will want to get back into the market – at higher prices.

What’s the probability of recession? Here’s neat graph highlighting various indicators.

The one indicator that is flashing red is the 12 month implied market expectation for Fed Cuts.

We believe that’s a headfake. As you may know, we’ve been of the view that the crowd has been hallucinating rate cut expectations for the last two years.

This is a sign of excessive bearishness in markets.

That said, we do see rate cuts coming in September. We’ve had 3 months of good inflation prints.

Real interest rates are 2%+. It’s not clear that’s ‘bad’ but a lot of PHD type economists (who did a brazen experiment with QE) seem to think so,so they will cut rates.

Mortgage Rates Declining

I noted two weeks ago that the ‘one fly in the ointment for our bull thesis is elevated mortgage rates. Also noted that Agency MBS was a mispriced asset.

Guess what?

Mortgage rates are dropping! That’s excellent news.

Housing is a core pillar for the economy. As housing goes, so goes the economy.

Mortgage applications are up U.S MBA MORTGAGE APPLICATIONS 16.8% VS 6.9% previous week.

The US 30-Year mortgage rate is now 6.54% down from 7.5% a few months ago.

My guess is some big institutions started buying Agency MBS and that’s bringing rates down.

Glad to have played a small role in contributing to the repair of the housing market ;)

The Macro Is Good. And Good News is Good News.

Sometimes good news is bad news - because the Fed has to slow down the party.

Not today. Good news is Good news.

What we learned this week:

1. Unemployment claims dropped

2. Retail sales beat expectations

3. Inflation continuing to improve (producer price index and CPI were benign)

This confirms our thesis two weeks ago where we noted that there is no recession - and the Non-Farm Payrolls and ISM Orders were just a headfake.

Take a look at that post here for the reasoning.

We leaned into the August 5th Monday morning crash and picked up terrific bargains for the long-haul.

We also had a tactical bet against the Vix and a bet on the 10-year going up via SVIX and TBT.

Unfortunately, we will pay short-term capital gains on those two ideas…which is why I am exploring an ETF.

The IRS does not tax in-kind transactions. This is totally different from tax-loss harvesting.

An ETF can swap appreciated Nvidia for, say, a 10-year bond and not pay taxes.

This is why you don’t get a tax bill if you own the S&P 500 thru an ETF each time they rebalance.

Fill out the form on www.lumidaetf.com if you have interest in this. We are taking a Dollar Shave Club approach to ensure there is sufficient AUM upon launch to make this work.

We are also talking to a handful of world-class VCs and family offices that share Lumida’s vision.

More to come!

Fed’s Bostic Capitulated

Bostic was one of the few Fed Governors whom I thought had the right read.

Now he’s saying: “.. we can’t really afford to be late. We have to act as soon as possible.”

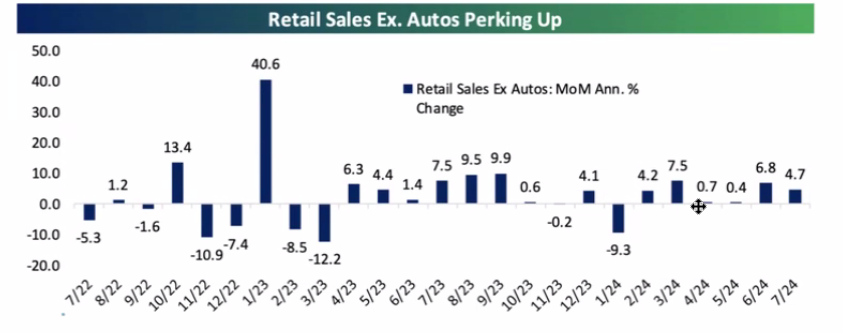

Consumer Discretionary is Back

We have now had two back to back retail sales reports beating expectations.

If you strip out the volatile auto category, you see the numbers aren’t that bad at all.

Now, stocks like Luluelmon, Nike, and Ulta are moving higher.

Markets: Technical Studies

From Fundstrat’s Tom Lee:

Other than Volcker era, market has NEVER been lower in 2H when delivering 10%+ returns in 1H.

Median gain in 2H = 10% with positivity rate 83% overall.

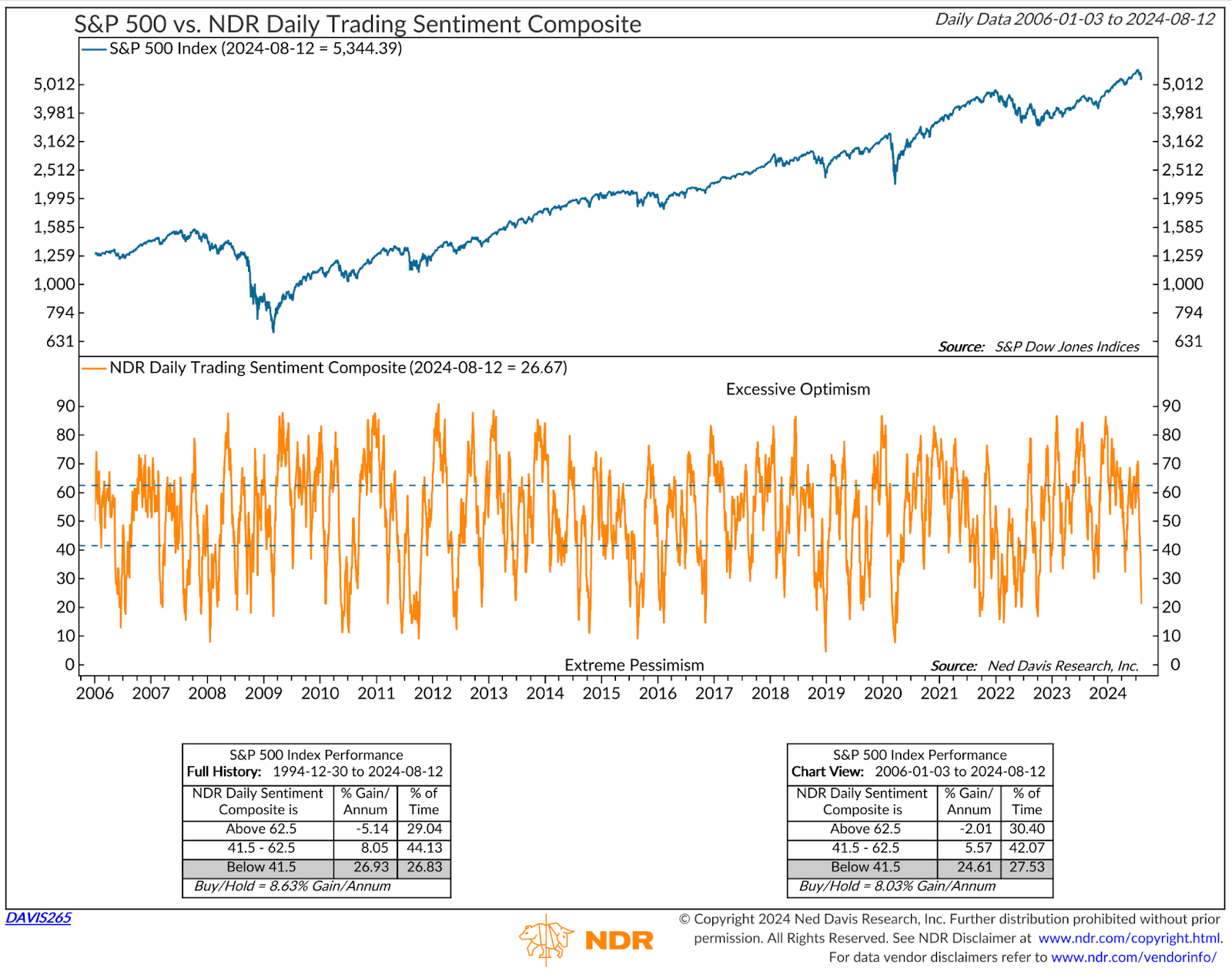

Here’s another from Ned Davis Research.

Their sentiment composite is at the lowest level since late-2022 – that was a great time to buy.

When short-term sentiment is this washed out, stocks usually rip.

We Quoteth Nietzsche: SaaS is Dead

Databricks acquired Tabular for $2 Bn (!!).

Remember when SaaS was CapEx light?

That was a different era.

The business models are dilutive to shareholders now.

We own zero SaaS; I believe names in WCLD will remain under pressure.

Look at the weak results from TEAM - an otherwise strong and ubiquitous SaaS firm (creators of Atlassian)

Also… note the Big Tech firms are encroaching on their offerings (Microsoft /Fabric getting into analytics; Google angling into cybersecurity)

If you can integrate a value-added offering into your cloud you have a competitive advantage that’s hard to beat

It’s not that different from Microsoft baking Internet Explorer into the OS which hurt Netscape

LPL Financial

This is a wealth management business benefiting from the trend of advisors leaving the big wirehouse firms to go independent.

LPL sports an ROE of 40% and has a forward PE of 12.5x (lowest decile of historical valuation).

Normally this business has a high-teens multiple.

The stock was whacked, along with Schwab SCHW, due to concerns around a decline in interest income from client cash sweeps due to regulatory pressure and a declining interest rate cycle.

We did not own the stock when that happened.

But, we do track about 200 stocks we view as ‘quality businesses’.

We simply wait for them to drop, and if they do - we take a closer look to assess whether the risk is priced in or not. Markets after all do over-react.

In this case, we concluded that the worst case was priced in AND that there was likely upside to the worst-case scenario.

This business is a classic compounder. And you can see that from the 10-year chart.

Aside fron the fundamental story, look at the subsequent performance (green dot) when the business goes on sale. The technicals line up.

I expect in a year or two this will be up 30% or so provided there is no bear market and the usual caveats.

If you are looking for a wealth management partner, Lumida is now welcoming a limited number of new clients.We offer a range of services, alternative investments (such as our CoreWeave deal), white-glove crypto management, to public equity management, and high-touch family office services, including trust, tax, and estate planning.

Ready to explore? Click here to fill out our form to start the discovery process.

Interested but not ready to commit? Build a relationship with Lumida and stay informed. Click on the poll below if you want our advisors to reach out.The US Consumer is Alive and Well

Walmart beat estimates posted strong 4.2% YOY revenue gains.

So... there is no recession.

Poor retail performance elsewhere means consumers are down-shifting their spend to save at WMT

That's partially why good inflation is coming into check.

Americans are trading down.

Amazon and Walmart are teaming up to hurt retailers. That’s why the retail sales figures were weak earlier this year.

Also, the Millennial generation is minimalist. They prefer experiences over goods. That may explain a role.

Company Earnings

Technology, Media, Telecom

monday.com (MNDY): Beat on EPS and revenue. Revenue up 34.4% YoY. Strong demand and operating margin improvements driving growth.

Cipher Mining (CIFR): Miss on EPS and revenue. Revenue up 17.9% YoY. Revenue shortfall despite year-over-year growth.

Applied Materials (AMAT): Beat on EPS and revenue. Revenue up 5.4% YoY. Strong cash generation from operations.

Consumer Discretionary

Home Depot (HD): Beat on EPS and revenue. Revenue flat YoY, up 18.52% QoQ. Fiscal 2024 guidance boosted by an additional sales week.

On Holdings (ONON): Miss on EPS, revenue beat. Revenue up 27.8% YoY. Strong sales growth across all channels and categories.

Alibaba (BABA): Beat on EPS, revenue miss. Revenue up 4% YoY. Cloud and AI-related products showing strong growth.

JD.com (JD): Beat on earnings, revenue miss. Revenue up 1.2% YoY. Record-high profits on a non-GAAP basis.

Financials

StoneCo (STNE): Beat on EPS and revenue. Revenue up 8.8% YoY. Improved EBITDA margins reflecting operational efficiency.

Nu Holdings (NU): Beat on EPS and revenue. Revenue up 52.4% YoY. Significant customer base expansion fueling revenue growth.

UBS Group (UBS): Revenue beat. Revenue up 24.7% YoY. Strong asset inflows in Global Wealth Management.

Consumer Staples

Walmart (WMT): Beat on EPS and revenue. Revenue up 4.7% YoY. eCommerce growth driven by pickup, delivery, and marketplace.

Industrials

TORM (TRMD): Strong earnings. Revenue up 13.5% YoY. Robust year-over-year revenue growth.

Sector | Company (Ticker) | Beat or Miss | Revenue (Absolute View) | Highlight |

Technology, Media, Telecom | monday.com (MNDY) | Earnings beat by 67.9%, Revenue beat by 3.1% | $236.1M, up 34.4% YoY | Strong revenue growth of 34.4% year-over-year, indicating robust demand. Operating margin improvements. |

Consumer Discretionary | Home Depot (HD) | Earnings beat by 2.6%, Revenue beat by 1.1% | $43.2B, flat YoY, up 18.52% QoQ | Fiscal 2024 guidance includes a 53rd week, expected to add $2.3 billion to total sales. |

Financials | StoneCo (STNE) | Earnings beat by 8%, Revenue beat by 4% | R$3.21B, up 8.8% YoY | Adjusted EBITDA Margin increased from 49.0% to 49.5% sequentially. |

Financials | Nu Holdings (NU) | EPS beat by 10.9%, Revenue beat by 1.4% | $2.85B, up 52.4% YoY, 4% QoQ | Customer base grew to 104.5M, adding 5.2M new customers in Q2. |

Consumer Discretionary | On Holdings (ONON) | EPS missed by 15.8%, Revenue beat (exact % not provided) | CHF 567.7M, up 27.8% YoY | Sales increased across all channels and categories by double digits. |

Technology, Media, Telecom | Cipher Mining (CIFR) | EPS missed by 700%, Revenue missed by 3.89% | $36.81M, up 17.9% YoY | Revenue missed analyst expectations by $1.49M. |

Financials | UBS Group (UBS) | Revenue beat by $350M | $11.9B, up 24.7% YoY, down 6.3% QoQ | Global Wealth Management saw net new assets of $27B. |

Consumer Staples | Walmart (WMT) | EPS beat by 3.08%, Revenue beat by 1.15% | $169.3B, up 4.7% YoY | Global eCommerce sales grew 21%, driven by store fulfilled pickup & delivery and marketplace. |

Consumer Discretionary | Alibaba (BABA) | EPS beat by 7.5%, Revenue missed by 3.3% | $33.47B, up 4% YoY | Cloud Intelligence revenue grew 6% YoY to $3.65B, with AI-related product revenue growing triple-digits YoY. |

Technology, Media, Telecom | Applied Materials (AMAT) | EPS beat by 4.9%, Revenue beat by 1.6% | $6.78B, up 5.4% YoY | Generated $2.39 billion in cash from operations. |

Consumer Discretionary | JD.com (JD) | Earnings beat by 48.3%, Revenue miss by 1.7% | $40.1B, up 1.2% YoY | Record-high operating and net profit on a non-GAAP basis. |

Industrials | TORM (TRMD) | Earnings: $2.14 per share (GAAP) | $384.3M, up 13.5% YoY | Strong year-over-year revenue growth of 13.5%. |

China & Humanoids:

There’s a good chance we will see China as a major world exporter of Humanoids

Tesla and Figure may be in the lead now…

But, China has demonstrated time and again its ability to ‘fast follow’ swiftly

China’s dominance in EV and Solar are simple examples

And China has national focus on humanoids to offset population decline

The less discussed use cases for humanoids - outside of childcare and elderly care - will be manufacturing and infrastructure… two areas where China excels

The idea of having humanoids manufactured by a foreign state with a surveillance focus obviously will lead to new tensions and debates

AI

Here’s an excerpt from Bloomberg that caught my attention.

They discuss how investment managers are using AI to transform the investment process.

This is something we’ve thought a lot about - and more importantly, are investing in technology for this future.

In the future, Lumida is as much as media company as it is an investment management company.

I don’t see why we wouldn’t have AI Influencers debating markets. They will be smart, funny, attractive, and always informed.

The hard part is the information substrate. And the workflows and decision making frameworks.

Lumida has that. I don’t see why a 10-person firm can’t disrupt a 10,000 person legacy wealth manager like my old shop Merrill Lynch with AI.

Excerpt on Chatbot CFA:

‘For these early adopters, who are long in the business of deploying new technologies for an investing edge, chatbots can conduct the thankless tasks like any eager-to-please intern, including filtering through regulatory filings, summarizing research and writing basic code.

But a fully fledged analyst in chatbot form that can spit out savvy investment ideas, granular research and reliable predictions? That remains ways off, just as Wall Street frets that the new tech will struggle to justify this year’s frenetic stock rally.

In one instance, a Balyasny portfolio manager wanted to see if its chatbot could figure out the stock winners or losers from higher tariffs — a reasonable question that it couldn’t answer at the get-go. Engineers had to first train the model by breaking such scenarios down to a series of sub-questions. It took 99 minutes scanning 20,000 documents and going step-by-step before formulating a satisfactory answer.

“We’re relying on the capabilities of a junior intern: you ask AI to do some simple analysis with internal data sources, it will do it, but either you have to give lots of very specific prompting or the analysis itself is quite rudimentary,” said Charlie Flanagan, head of applied AI at Balyasny, which runs about $22 billion. “So how do we move it from a junior intern to a senior intern to a junior analyst so that at the end of 2024, folks are able to ask quite robust questions?”

None of this comes cheap. Goldman Sachs estimated that building out AI infrastructure across the economy will cost more than $1 trillion over the next few years. Balyasny has a 12-person team for AI while Man is about to have six people devoted to gen AI specifically. Fully trained systems like ChatGPT or Anthropic’s Claude charge for every incremental use, while building one up from open-source models like Meta’s Llama requires a big splurge on talent and computing power.

And even when the AI currently lags humans on cognitive prowess, it has the advantage of speed and scale, says Ben Wellington, deputy head of feature forecasting at Two Sigma. He points to the example of tracking corporate executive departures. While quants like him used to write a formula to identify the latter via particular keywords or expressions, he can now do that much faster by querying an LLM.

Digital Assets

Coming off of a market bottom, investors rush to buy the highest quality assets.

This is why Nvidia is up 19% over the past week.

Note: We suggested Nvidia was a good buy this past Sunday.

Bitcoin is at a key technical level.

The question is now - Can Nvidia have a graceful hand-off to Digital Assets?

We have the DNC convention this week. Historically, this elevates the polling for the candidate in question.

Candidate Harris is polling favorably and is in the ‘honeymoon’ period. I’d expect the polling elevates further and we see “Peak Harris” - much like we had “Peak Trump” shortly after the assassination attempt.

The risk to this view is if images of protestors taking over the convention narrative just like the DNC convention in the 60s. This is Steve Eisman’s view and it’s a clever and original idea.

I’m not sure that happens. The DNC is aware of this risk and wants to project a manicured image.

Fox News will undoubtedly highlight this aspect of the debate.

The question turns on how effective Candidate Harris and the DNC is at message control.

Harris’s comments at the AZ border last week where she took a ‘law and order’ message suggests they are pivoting to the mainstream center rather than the progressive crowd.

We remain skeptical that Candidate Harris favors a constructive digital asset policy.

That’s unfortunate as the big banks and tech gatekeepers need more competition.

And sound Digital Asset policy that advances US dollar hegemony globally is in US interests.

Good policy would also help the long-tail of creatives capture the value they create - rather than capture whatever thin scraps the Apple Store or TikTok or Youtube chooses to offer to creators.

Digital assets do require a regulatory overhaul to unlock the full potential of tokenization, creator economy, and decentralized capital markets.

The question to wrestle with is this…

What’s the fastest horse between now and year-end? Nvidia or digital assets?

Digital assets require attention and momentum to thrive.

Those following us may know we exited our ETHE positions around the May top and continue to do that for remaining positions as they hit long-term capital gains.

Our view on Digital Assets is now highly tactical. We believe we are past mid-cycle.

I will be interviewing Michael Terapin, an OG investor in Bitcoin, soon. Can’t wait to get his thoughts.

Quote of the Week

In the short run, the market is a voting machine, but in the long run, it is a weighing machine.” - Benjamin Graham

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.