Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Macro: Housing, Higher for Longer, Tiktok & China

Markets: MHO, Meta, Google, Tesla, TSMC, INTEL Earnings, VC Power Laws

Company Earnings: Intel, Tesla Miss; META and Google dominate

AI: Boston Dynamics, AI Investment Returns

Digital Assets: Stripe Crypto Payments, Miners shift to AI

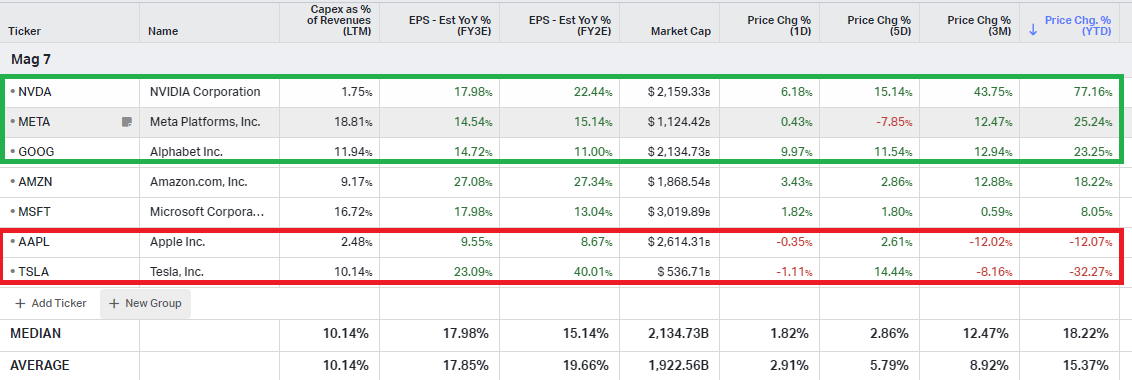

It was quite an action-packed week with Big Tech earnings reports from Google, Meta and Tesla.

Let’s take a look at the Mag 7 scoreboard.

We’ve been sharing our views that you want to own Google, Meta, and Nvidia - and sell or short Apple and Tesla. We view Amazon and Microsoft as Consensus - so you don’t get an ‘excess return’ (or alpha).

Here are the YTD return:

What we Own:

Nvidia: 77%

Meta: 25%

Google: 23%

Neutral:

Amazon: 18%

Microsoft: 8%

Sell or Short:

Apple: (12%)

Tesla: (32%)

We’ve nailed it.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

(Past results are no guarantee of future performance.)

More on these names later…

Tune in below for a quick watch, and don’t forget to subscribe.

Justin and I hosted a special edition of ‘What’s On Your Mind’ focused on near-term market outlook.

This one has slides.

The headlines are:

The economy is expanding despite a weaker GDP print. Real incomes and productivity are up.

This is a strong bull market

We are in a pull-back. Pull-backs happen 1 to 2x per year.

This pull-back is driven by Mr. Market recognizing ‘higher for longer’

The pricing in of ‘higher for longer’ is punishing long duration equities - including growth stocks indexed to themes we like

The correction should be relatively shallow all things considered and wrap up by Mid-May + or -

This will represent an excellent set of opportunities to get into quality stocks

If you’ve been on the sidelines and want to get in the market, we recommend building cash.

In terms of positioning, we favor tilts towards value currently: energy services, homebuilders, and select financials.

Listen to our analysis below, and if you are interested, reach out to become a client.

The Next Berkshire Hathaway?

Are you a family office looking to create a mini-Berkshire Hathaway?

As a guest on the FamilyOffice Podcast, Ram spoke with Angelo Robles about what makes a Buffett business and the trends shaping the investment landscape across markets, macro and digital assets.

Here’s our take on Mag7 & nuclear energy

Tune in to watch the video below, don’t forget to like and subscribe.

Are you sure you are sleeping well?

This week, we had an interesting conversation with Mollie Eastman, Founder, Sleep is a Skill.

Mollie is a renowned sleep expert consulted by founders, executives, and poker players looking to improve their daily performance on the road to building their legacy.

Tune in below to unlock secrets to deeper, better sleep.

Don’t forget to like and subscribe to Lumida Legacy.

Macro

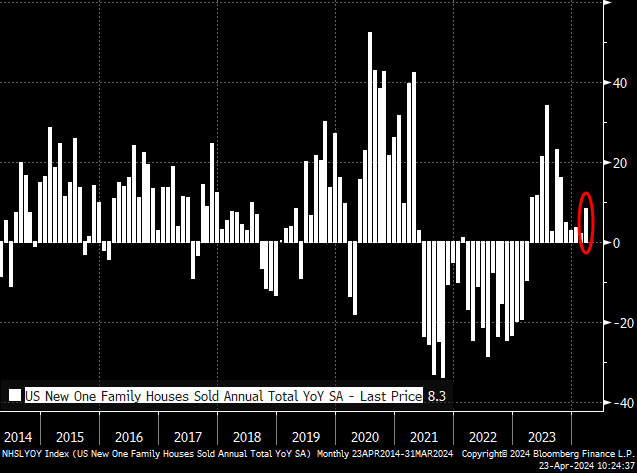

The housing market is strong. That’s great news as housing has a major multiplier effect.

The US economy is handling higher rates just fine.

New Home Sales just posted the best reading in 5 months.

This is not a sign of a weakening economy.

We continue to favor homebuilders. Rising mortgage rates mean homeowners are less willing to sell.

Homebuyers need to focus on new home building.

Note: You are going to see headlines about the US economy weakening in the upcoming weeks and months.

Economies inhale and exhale like a living organism. An exhale after a scorching hot 3 to 5 month sprint is perfectly natural.

Attractive growth conditions are still in place.

Policy volatility will challenge certain sectors however: like China and healthcare.

Higher for Longer CapEx and Rates

Mr Market is now pricing in ‘higher for longer’ AND ‘higher CapEx for longer’

Firms that increase CapEx expenditures, on average, have negative excess returns all things considered being equal.

The ROI on the CapEx is not clear in the next few years.

That means expenses are up, without matching earnings growth for certain AI firms.

In my view, this is a good time to tilt from Growth to Value and reduce exposure to tech and tier 2 semiconductor names like Intel and AMD.

(Did you see Intel drop 10% on earnings last week. We’ve done a good job avoiding laggards in this winner-take-most market.)

Industries we like right now are energy services and homebuilders.

Once the ‘CapEx and 10 year higher for longer’ is priced in the next few weeks, we believe you can embrace your favorite AI stock again.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

TikTok Ban: How might China retaliate?

We might see China do the following:

Ban Meta, Google, Twitter, Reddit, Zoom, Wikipedia (except Nvidia - need those chips)

Dramatic increase in espionage

Hiring of retired US military officers

Threaten Taiwan invasion

Capping amount citizens can leave the country to $50K

Supply arms & intel to Russia

Cyberattacks against US agencies and companies

Restrict rare earth mineral exports

Try to build an alternative to US dollar

Circumvent US export control restrictions on GPUs

Oh, wait, that already happened.

Geopolitical Shocks and Market Opportunities

We liked this research bit from or friends at BAML

The headline is geopolitical risk can create attractive entry points.

It takes about 1 month, on average, for the bad news surrounding a geopolitical event to price in.

Markets

Semiconductors

Taiwan Semiconductor Earnings highlights

Here are some notable quotes and our takes:

‘The Smartphone end-market demand is seeing gradual recovery and not a steep recovery.’

> Expect sluggish Apple revenue growth

‘The PC has been bottomed out, and the recovery is slower.’

‘AI-related data center demand is very, very strong.’

> Nvidia is benefitting from a multi-year trend

‘traditional server demand is slow, lukewarm’.

> Legacy CPUs not needed

‘IoT and consumer remain sluggish’.

‘Automotive inventory continues to correct’.

> Bad for EV stocks and On Semiconductor

‘We’re expecting [ EVs ] to decrease’.

FinTwit doesn’t read earnings transcripts, but people seem to have a lot of strong opinions, nevertheless.

We aren’t too far from having LLMs in extract exactly what I posted above.

More and more, I think it would be interesting for Lumida Wealth to launch a 130 / 30 long short ETF

We would have shorted Tesla, Apple, SoFi, Bakkt, and other nonsense ARKK is buying.

Each of those ideas we wrote about in real-time and they worked.

Then, use the proceeds from the shorts to go long, more great businesses and trends.

Shorts are a source of funding and can be used for risk management.

It’s just math.

Not embracing shorting is like saying we will only make right-hand turns.

Any mathematician or quant can show you the efficient frontier moves up and to the left if you enable shorting.

We wrote up about M/I Homes two weeks ago. Here’s their earnings result.

M/I Homes (MHO) stock gained 3.7% in Wednesday morning trading after the company delivered 2,158 homes, its highest Q1 level ever.

Backlog sales value rose 4% Y/Y to $1.79B.Q1 GAAP EPS of $4.78, vs. the $3.96 consensus, jumped from $3.64 in the year-ago quarter.

Total revenue of $1.05B, beating the average analyst estimate of $1.01B, rose from $1.00B in the year-ago quarter.

Adjusted EBITDA of $186.8M climbed from $146.8M a year ago.

Q1 new contracts increased 17% from a year ago to 2,547 from 2,172 in Q1 2023.

At the end of the quarter, the backlog stood at 3,391 units, with a sales value of $1.79B, compared with 3,301 units, with a sales value of $1.72B, at the end of Q1 2023.

Average sales price of $528K increased from $522K in the year-ago quarter.

A cancellation rate of 8% dropped from 13% a year earlier.

General and administrative expenses increased to $56.1M from $51.0M, and selling expenses rose to $53.9M from $49.1M.

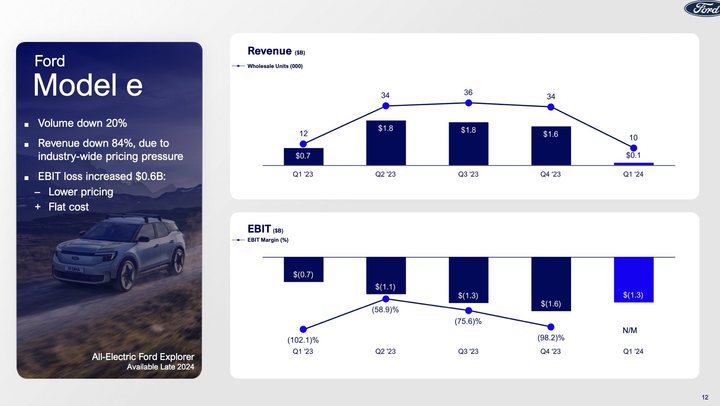

Tesla: EVs Remain in a Bear Market

Tesla lost $2.5 Bn in free cash flow and has $25 Bn in cash left. That’s ten quarters of runway.

We wrote in January in this newsletter that the ‘EV Bubble is Disinflating’.

That call has worked out beautifully. We expect that thesis to keep working.

The demand for EVs is waning.

You can save on fuel with an EV…

But, the (i) the decline in re-sale value and (ii) higher insurance costs can wipe out your savings.

That is the crux of the issue.

Take a look at this excerpt from Ford.

(By the way, Ford and GM are handily outpacing Tesla stock. It’s not even a comparison.)

Ford is up 5.18% YTD. Tesla is down 32.3% YTD.

Congrats to all those that observe Google earnings.

As you know, our favored names in Mag 7 are: Google, Meta, and Nvidia.

Google is back to All Time High and soared 10% after earnings.

Our steak dinner bet with Brad Gerstner (Founder - Altimeter Capital X: @Altcap) is looking good…

We also bought Meta after the stock gapped down 15%.

I have a 10 minute analysis of Meta in this video here. We go deep.

Our conviction on Meta remains high.

The risk is Meta accelerates CapEx spend further.

If you know the name and have conviction, you can use algo over-reactions to your advantage.

After we bought Meta the open on Thursday, the stock rallied 5%.

It’s important to be counter-cyclical. You want to invest at lows and de-risk at highs when markets are crowded.

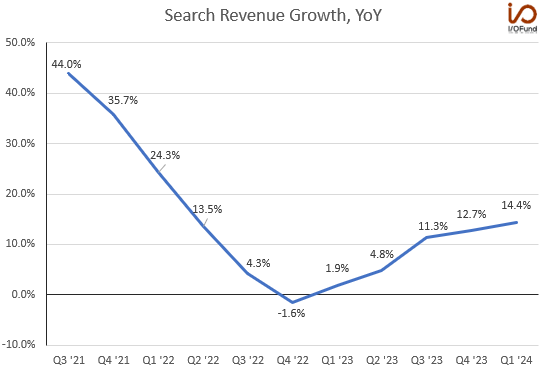

Google Search revenue notched a fifth consecutive quarter of accelerating revenue growth, reporting 14.4% growth in Q1, versus 12.7% in Q4 and 1.9% in the year-ago quarter.

Google cloud was always an also-ran after Amazon AWS and Microsoft Azure.

Our investment in Google doesn’t turn on Cloud.

This growth in Google’s Cloud business is encouraging.

Google continues to offer the highest risk-adjusted return, in our view, over the next several years.

West Coast VCs are in a Bubble

Remember when the West Coast VCs thought Google CEO should be fired?

And that SNOW and ADBE and TSLA were the names to bet on?

Members of the All-In Pod and Altimeter have expressed views like this much to our puzzlement.

We believe it stems from the fact that VCs believe they have relationships with CEOs of these firms: Frank Slootman, Elon Musk and so on.

Crossover VCs incorrectly conclude that this gives them an ‘edge’ in public markets.

It doesn’t work that way.

They are getting a sales story.

This is why Warren Buffett is in Omaha - he’s not distracted by the siren songs of the Bay Area or New York City.

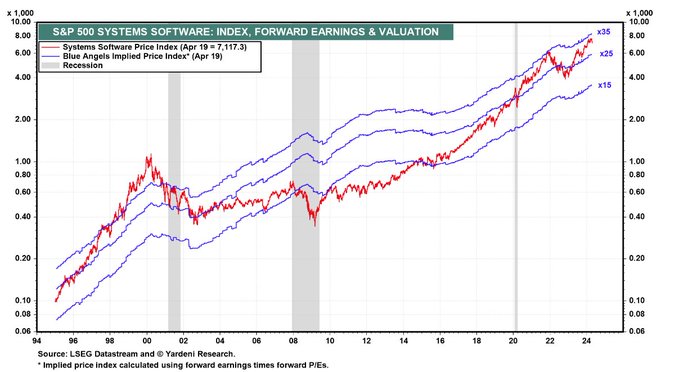

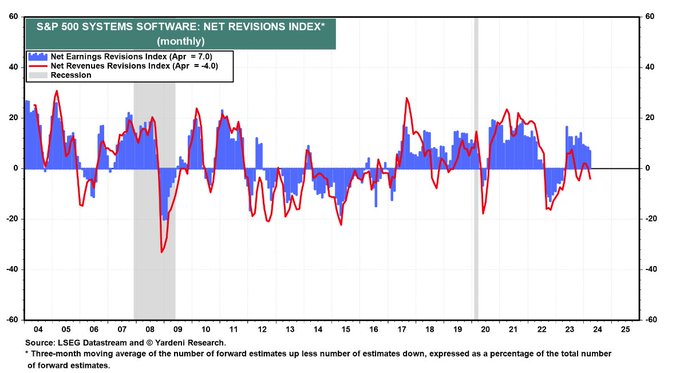

Software Valuations Are Over-Valued (Again):

Take a look at this chart showing software valuations and analyst revisions turning down.

We're approaching the upper bound of tolerable valuations.

Maybe this is why there are no great tech investors?

Cross-over tech investors - those that have public funds and private VC arms are the worst.

They fall in love with their own stories when they should be de-risking into public markets.

ARKK blew it (down 20% YTD).

Tiger blew it.

Coatue blew it.

Altimeter lost big on $SNOW.

How many hedge funds are loaded up on fancy software names?

One of the rules we have...

Don't own a stock with a higher forward P/E than Nvidia (~30x now).

Here are tech stocks more expensive than Nvidia.

Not exhaustive.

Some of these are fantastic businesses... but price is what you pay, value is what you get.

That 'rule discipline' has kept us out of a lot of trouble.

We believe many names on this list may under-perform.

Some of these are wonderful businesses and we’ve owned them as recently as this year.

But, we no longer have them in our portfolio.

We would buy after a significant market correction where valuation is in line with earnings growth.

Congress, for a change, may get TikTok right.

Who benefits from a TikTok ban?

1) Meta

Who buys TikTok if there is a sale?

2) Meta or Google

Will FTC seek to prevent Meta from Buying?

Yes. That favors Google.

Lumida Wealth owns both as top positions, so win win.

We call these ‘embedded real options.’

3) What about SNAP?

They have insufficient marketcap to make a real bid.

Note: If you don’t think foreign espionage is a real issue or don’t think social media is the new ‘soft power,’ you really need to re-calibrate your worldview.

This is an embedded real option.

fyi my tiktok account is here. You can call out TikTok risks and still be on TikTok.

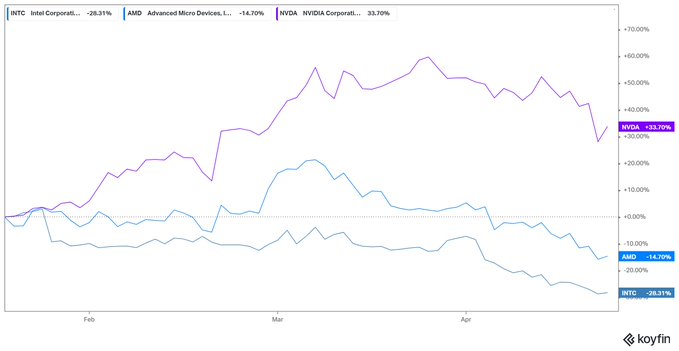

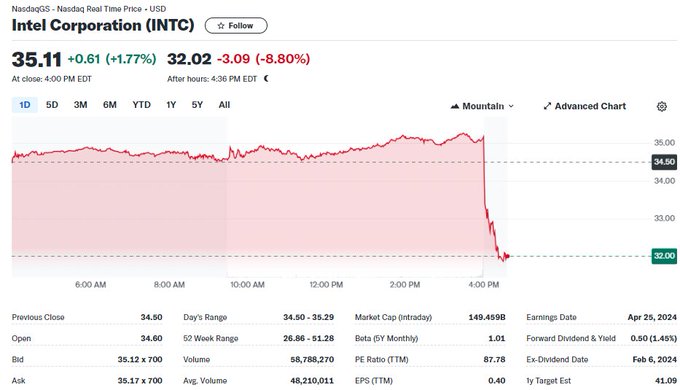

INTEL: SOMEBODY CALL A DOCTOR

Take a look at Intel after this post.

Good defense is avoiding losers.

I'm really happy with our defense, as much as the offense.

The chart makes sense to me...

Intel is waging a two-front war: Foundry business & GPU business and losing in both.

Here's a chart comparing Intel vs. Peers

Picking the right winners within a segment is the definition of alpha.

Intel was down 9% as CEO Pat Gelsinger underwhelmed again on revenue outlook.

Meta Horizon

Meta just announced Horizon OS - which supports their mixed-reality headset Quest.

Zuck knows that the Operating System and legacy apps are at risk for AI.

Microsoft has much more to lose than most.

Why do we need Windows apps if an AI can spin up a dashboard?

Zuck is going for the jugular.

Prediction: Meta will launch a mobile phone tailored to AI & Ray Ban / Quest.

Zuck is going to build an ecosystem.

The New Power Law

This viral tweet from Jason Shuman, GP at Primary VC gives an exclusive breakdown of top VC firm returns.

Key Takeaways:

Good Funds in the dataset returned 3.53X MOIC.

Great ones?

A whopping 17.95X MOIC.

Great Funds (all with > 10X+ MOIC) hit home runs >2X more than Good Funds.

10X+ funds get 10X+ returns on 14.1% of their companies.

And Great Fund “Winners” are nearly 2.5X larger outcomes for them than good funds.

Great Funds see an average MOIC of 68.42X on their 10X+ investments vs. Good Funds at 27.44X.

This shows that not only are they winning, but they’re winning big.

The returns driven by 10X+ investments show the power law within Great Funds…

91% of Great Fund Returns come from 14% of the Companies for Great Funds.

Great Funds invested 38.7% of their capital in 23% of their investments that generated over 5X+.

23.9% of which went into their 10X+ investments.

Good funds on the other hand invested 18.4% of their capital in 14.4% of their investments that generated 5X+.

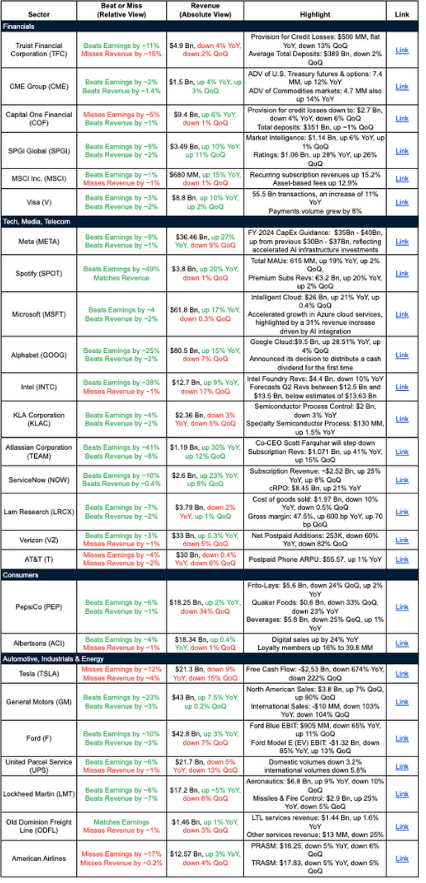

Company Earnings

Financials:

Mixed bag on earnings with some exceeding estimates (TFC, CME, SPGI, MSFT, V) and others falling short (COF, MSCI).

Revenue growth is generally muted, with some companies experiencing declines (TFC, PEP). Truist (TFC) is a standout with a significant decrease in revenue year-over-year and quarter-over-quarter.

Credit loss provisions seem to be flat or declining (TFC, COF) which is a positive sign.

Strong performance from payment processing companies (V) and business intelligence firms (SPGI).

Tech/Media/Telecom:

Mostly positive earnings reports with companies exceeding estimates (META, SPOT, MSFT, GOOG, INTC, KLAC, TEAM, NOW, LRCX)

Big tech companies like Meta, Microsoft, Alphabet are accelerating investments in AI infrastructure and cloud services integration

Streaming platforms like Spotify adding users steadily

Semiconductor players seeing mixed performance - Intel missing on datacenter/foundry revenues, while KLA and Lam benefiting from semiconductor process control demand & margin improvement

Productivity software vendors like Atlassian, ServiceNow posting robust ARR/subscription revenue expansion.

Traditional Telecom companies (VZ, T) are lagging behind with declining revenue and subscriber growth

Consumer:

Consumer staples leader PepsiCo navigating well across snacks, beverages and foods amid pricing actions and category shifts

Grocers like Albertsons benefiting from digital sales growth and loyalty program momentum

Automotive/Industrials/Energy:

Mixed results on earnings with some companies exceeding estimates (GM, F, LMT, HAL, XOM) and others falling short (TSLA). Tesla (TSLA) is a standout with a significant miss on both earnings and revenue

General Motors (GM) and Ford (F) show some recovery in North American sales

Lockheed Martin (LMT) continues to grow strongly in its Missiles & Fire Control segment

Declining volumes for package delivery companies (UPS)

ExxonMobil (XOM) beats on revenue despite missing on earnings, indicating higher oil prices but potentially lower production volumes

Healthcare/Hospitality:

Hospital operator HCA seeing robust inpatient admission trends driving revenue outperformance

Hilton adding supply at a record pace and seeing a recovery in RevPAR performance

Overall, a mixed bag with secular tech growth drivers around AI/cloud offsetting cyclical consumer/industrial headwinds. Financials navigating rate cycle reasonably well so far. Pockets of strength in hospitality/healthcare volumes.

AI

Boston dynamics has been leading the way on robotics for awhile but beginning to see other companies coming to market.

Robotics naturally require a multi-model form of AI that can read information about its environment and output that data in another format that's executable e.g. movement/speech.

The world will look very different in 10 years.

Quick take on AI VC returns from Meghan Reynolds, Partner Altimeter.

The LP takeaway:

AI waves are huge, but most $$ invested today won’t deliver VC returns because a) valuation or b) no durability of revenues.

Big AI deals shown widely via co-invest SPVs, which are easier for LPs to access than GPs.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Digital Assets

Stripe has a crypto payments rail use case.

Crypto is the last chapter in the evolution of Fintech.

Lending, Payments, Settlement… all of that should be done on transparent, decentralized, cryptographically secure public ledgers.

Here’s John Collison, Founder at Stripe, explaining.

Bitcoin Miners May Shift Focus to AI After Halving

Miners will be faced with substantial cost increases as a result of the halving, with electricity and bitcoin production costs almost doubling, the report said.

Bitcoin miners may shift towards AI due to the potential for higher revenue, CoinShares said.

The average bitcoin production cost post-halving is about $53,000.

Some miners are actively managing financial liabilities and are using excess cash to pay down debt, the report said.

Quote of the Week

"Successful investing is about managing risk, not avoiding it." — Benjamin Graham

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.