Here’s a preview of what we’ll cover this week:

Macro: Ed Hyman Flips from Hard Landing to Soft Landing

Markets: Fed Cuts Ahead, We expect 25 bps

Company Earnings: Tech continues strong earnings performance

AI: Larry Ellison lays out the bull case for GPU Demand

Curations: Brad Gerstner on Nuclear, Dario on AI, Musk on Humanoids

f you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.This week, we had a great conversation with Michael Weinberg.

Michael is a seasoned investor with significant experience working with George Soros and Stan Druckenmiller. We discuss hedge funds & their investment strategies.

We further dive into the impact of commercial real estate and private credit on regional banks, and the bear market situation in China.

Michael also provides an inside scoop from his time at Protege Partners, including the famous bet against Warren Buffett.

Subscribe to watch the full episode below on your favorite platform.

It airs at 2 PM ET.

Remember to like and subscribe. Apple and Spotify links get updated after the show airs. You can subscribe to our podcast page below to be notified.

It helps us grow and interview experts like Michael.

Buffett is a Market Timer

‘It’s time in the market, not timing the market’

‘Buy low, sell high’

‘The stock market is a market of stocks’

You can’t hold all of these statements as true at the same time.

Intuitively, you know you should buy low and sell high.

That means the timing on your decision matters.

Let’s take a look at what Buffett has done in recent years:

Bought homebuilders in 2023. They dumped for a month, then rallied hard.

Excellent timing.

Bought insurance themes (Chubb). Dunked for a month. Second best industry group.

Great timing.

Sold Apple near the highs

Great timing.

Sold BAC this week, top ticking the market

Chef’s kiss.

Buying energy stocks near the lows

He got in Japan years ago and did a carry trade - years before it was popular

Aren’t these all examples of timing?

(He has made mistakes like Snowflake and Delta - the point is that he cares about timing…)

If you are a value-oriented investor, by definition you need to re-position as valuations adjust.

What’s Buffett doing now?

He is building a massive cash war chest as valuations…

just as quality stocks like Costco and FICO soar past Nvidia’s valuation.

(Berkshire is levered with AAA debt so he doesn’t face that much cash drag)

When Buffett builds cash at these levels, my read is that he expects markets to dislocate.

Buffett is adjusting his ‘net long’ exposure.

That’s the definition of market timing.

The good news?

Buffett is usually one year early to building cash.

And indeed it looks like we will see IPOs in the 1H — which would be a classic last hurrah.

just as the flurry of landmark IPOs marked prior tops

Example:

Goldman IPO before dotcom implosion

KKR before 2008 implosion

Coinbase marked crypto top for miners

Last thought…

What causes the burst in animal sprits around IPOs is this:

1) Too much supply issuance relative to absorption

(appetite becomes indigestion)

2) Elevated expectations from IPOs from drinking the kool-aid

See Peloton, Rent the Runway, All Birds

3) The last straw?

IPO buyers get burned on names that drop instead of pop

DotCom era: Handspring IPO failed

2008 era: Debt IPOs (eg, securitizations) failed

2021 era: SPACs like SOFI failed and are exposed as awful business models wrapped in story tales

AI

We thought this was a great clip from Oracle CEO Larry Ellison

Here are select quotes:

".the entry price for a real frontier model from someone who wants to compete in that area is about $100 billion. Let me repeat, around $100 billion.

That's over the next 4, 5 years for anyone who wants to play in that game. That's a lot of money. And it doesn't get easier.

But in addition to that, there are going to be a lot of very, very specialized models. I can tell you things that I'm personally involved in, which are using computers to look at, biopsies of slides or CAT scans to discover cancer.

Also, there are also blood tests were for discovery and cancer. T

hose tend to be very specialized models. Those tend not necessarily use the foundational the rocks and the ChatGPTs, and the Gemini, they tend to be highly specialized models.

This is an ongoing battle for technical supremacy that will be fought by a handful of companies and maybe one nation state over the next 5 years at least, but probably more like 10. So this business is just growing larger and larger and larger.

There's no slowdown or shift coming.”

Larry has aptly summarized our Semiconductor Capex Receiver thesis. We started writing about this in the newsletter in the summer of last year - the basic conclusion is own the picks and shovels layer.

Last week, we did a portfolio review of Snowflake and highlighted the various differences we had.

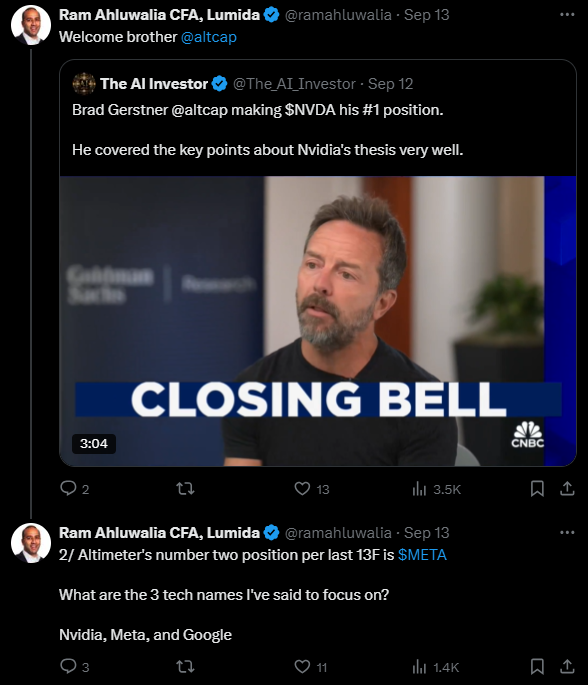

Funny to see this week that Altimeter has announced Nvidia is now it’s number one position! It’s number two position? Meta.

Funny - those are two of our top picks in technology as well as long-time readers will recognize.

Macro Update

Another bear has come to the light and turned bullish.

I have a lot of respect for Ed Hyman - he is in the same caliber as Byron Wein (famed market strategist).

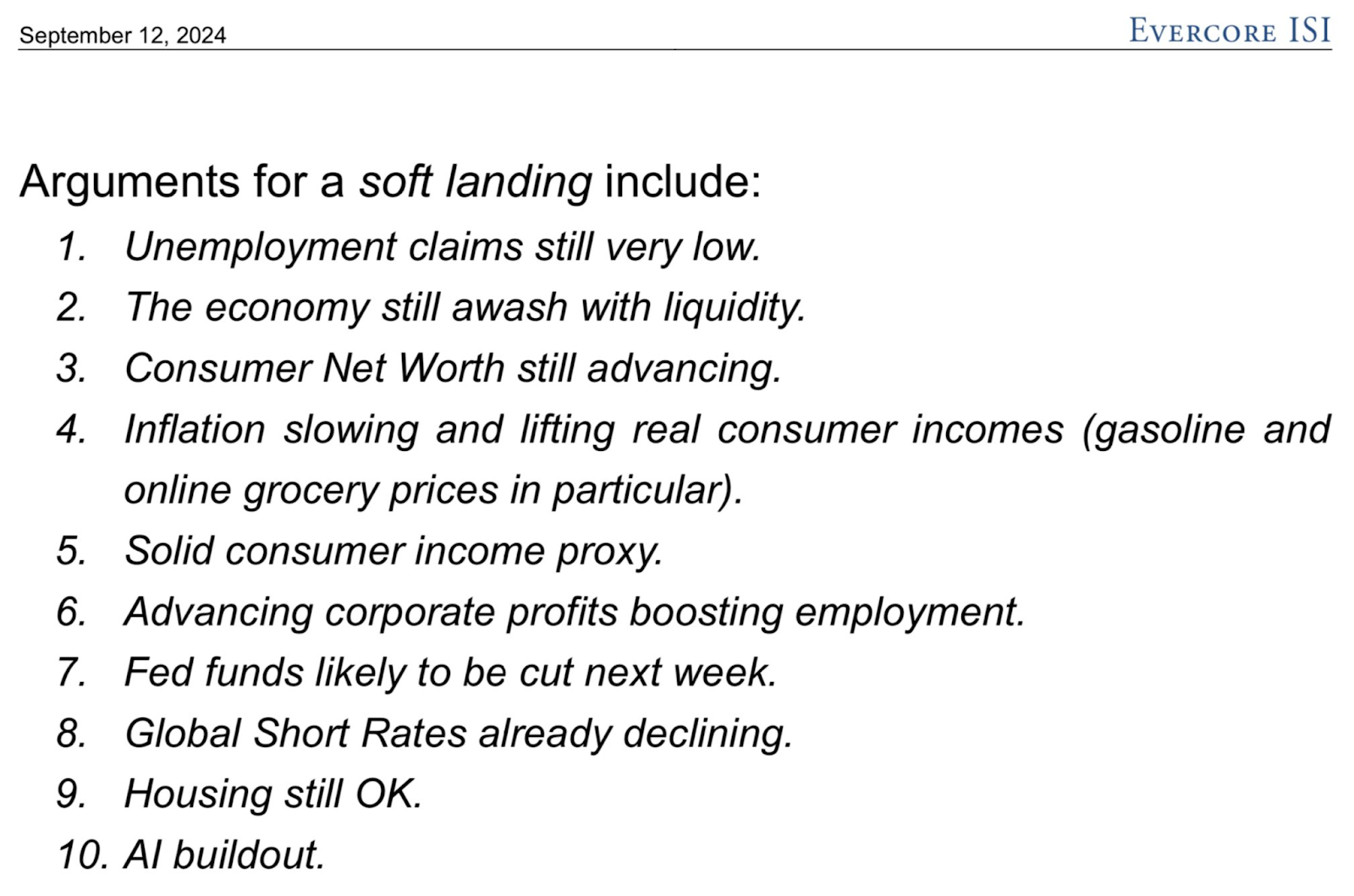

Ed Hyman revised his view from -1% GDP growth so a soft landing:

“History and experience say to stick with a hard landing outlook. However, the hard math that our team has reviewed says flip to a soft landing outlook. And that’s what we’re doing.”

These are all arguments we agree with. The big one not on the list is corporate earnings growth.

Companies are reluctant to cut workers when earnings growth is strong.

When do you see mass layoffs when earnings growth is strong? It’s the other way around… when earnings growth is weak, you see widespread layoffs - as we saw in the 2002 cycle.

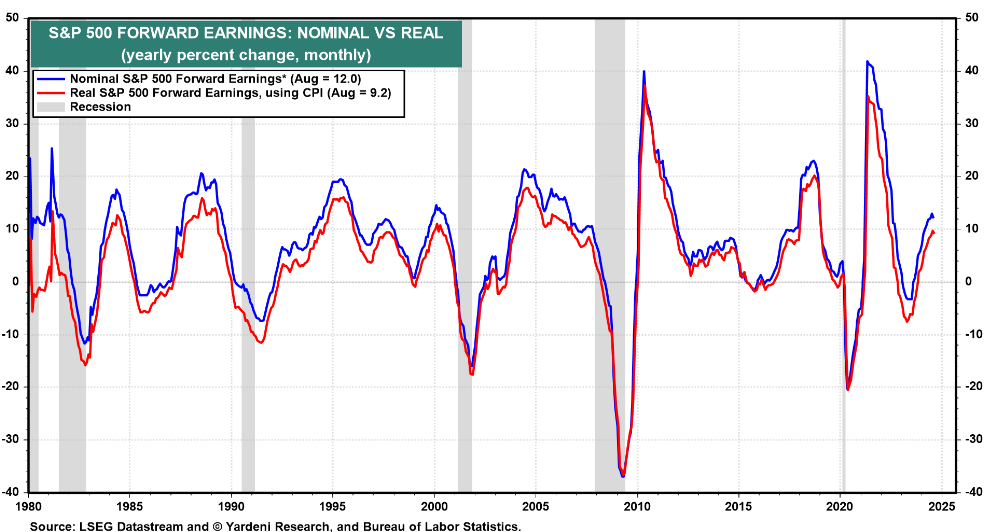

Here’s a chart showing corporate earnings. Do you see a recession anywhere?

If Corporate Incomes are up, consumer real incomes are up, and government spending is up… It’s hard to get a recession.

The unusual dynamic this time is the rise in productivity rate. We’re seeing more slack in labor market as firms are getting more efficient.

AI is slowly making itself felt. Give it a few more years and we could see GDP growing without much growth in jobs.

Owners of capital will out-perform providers of “white collar” labor which will create some real social issues.

Mr. Market is Worried About a Recession

This sets up a dynamic where the market may 'test' the Fed when the FOMC convenes next week.

That means markets could prove to be disappointed. Currently markets expect a 25 bps cut – but there is a ~40% bet that the cut could be 50 bps.

We are in the 25 bps camp:

A 50 bps cut could exacerbate the Yen Carry Trade (USDYEN is in the dumps)

The market might say ‘What does the Fed know?’

The Fed wants to telegraph every move it makes… 50 bps is a surprise

Mr. Market believes we are in a recession.

Consider:

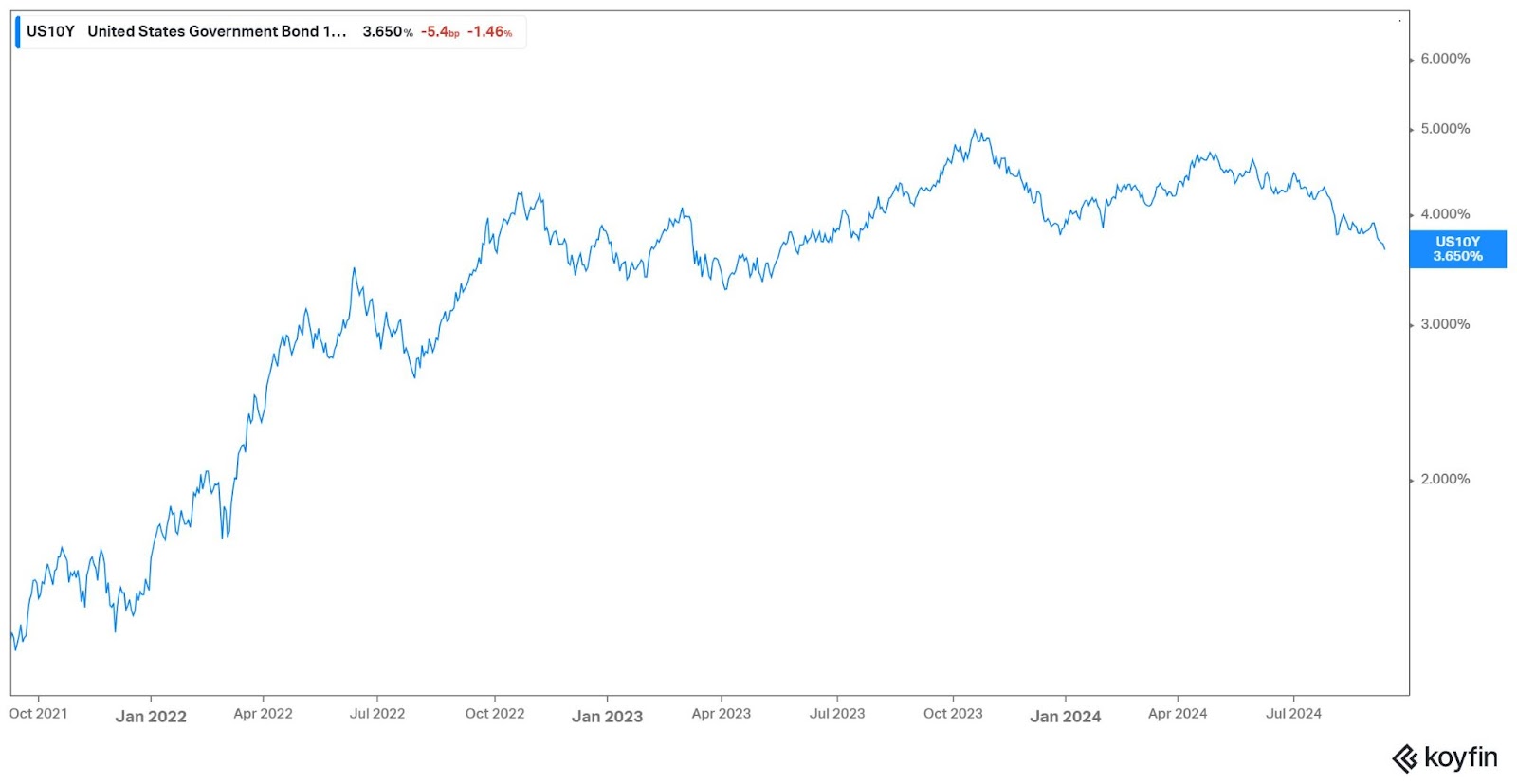

(1) The price of oil is $66 -- at multi-year lows. See chart.

(2) The 10-year is at lows not seen since the banking crisis in March 2023

(3) Defenses like Staples & Utilities are leading and cyclicals like Energy are lagging.

Initial claims came in-line with expectations.

Back in April, we noted Mr. Market was worried about inflation.

These are mostly mood swings.

Take a look at the charts below of the 10-year and oil to get a sense of the ‘deflationary impulse’ in markets.

Tech Continues to Lag

The Nasdaq 100 ETF’s QQQ total return over the last 3 years is less than 20%.

We have had a lot of volatility in tech. And we started the year at the top decile of tech valuations.

WIthin tech, as we’ve noted before, we believe you need to stick to strong earnings growers at reasaonble valuations.

Those names have done well. Our tech picks are: Nvidia, Meta, and Google in Mega Cap. We also own App Lovin (Ticker: APP) which is re-rating to new all-time highs.

The stock was in the low teens despite delivering strong earnings growth. We had picked it up around the August 7th lows.

Overall, we believe elevated share based compensation and disruptive innovations poses significant risk to tech stocks.

See fallen angel Snowflake or Asana or your favorite cloud ETF.

Combined with the growth to value rotation we have discussed previously, you really need to position correctly within technology.

And there are plenty of opportunities away from technology - don’t feel like you are missing out.

Peter Lynch made the Magellan Fund an extraordinary success by avoiding chasing the latest memes.

That said, we did pick up Nvidia on September 5th in the $105 to $107 range as “growth factor” was oversold.

The stock is at $118 now.

We think you may get another shot at buying growth names in October so don’t fret if you missed this one.

We tax loss harvested various names that are under-performing, and we rolled that capital into Nvidia. Tax loss harvesting is good risk management and good practice.

And we might be able to buy those names back in late October at around the same prices.

Those names include Pag Seguero and Micron.

Our market outlook is that October will pose additional downside volatility. We remain of the view that the S&P is capped at 5,600 until earnings season gets underway.

We remain a tactical underweight and are raising some cash here.

However, we expect markets finish the year at all-time highs.

Palantir SPV: A True Story

A buddy of mine was in Palantir at $1 / share.

He invested in an SPV that had sourced secondary shares.

After Palantir IPO lock-up expires, the stock is ~$20.

Everyone (meaning the LPs) want out.

The GP running the SPV refuses to distribute shares.

The stock drops to $10 / share.

My buddy still made 10x, but could have been more.

The main lesson: If you participate in an SPV, check for Manager Discretion.

My view on late-stage venture capital deals is simple: look to get liquidity as fast as possible in public markets. Wait for long-term capital gains - that’s it.

Once a security is freely trading, the SPV creator is not adding value.

Check out http://www.lumidadeals.com where we show all the late-stage private deals we have executed. (All 2 of them - we aim to be selective).

These private deals have outperformed the S&P 500 significantly, and relative to equities we believe select private deals offer more reward than equities priced at the top-end of historical valuations.

Palantir

Major accomplishment!

What happens to firms that join the venerable S&P?

They tend to lag.

The run-up happens before inclusion.

Study Tesla inclusion in 2020.

It had weeks of follow-thru rally, then it gave back the inclusion gains.

The problem is - GPs and VCs fall in love with their darlings.

They are too close to management CEOs.

Talking to management is negative alpha in the age of Reg FD where most of the insights are dropped in earnings calls.

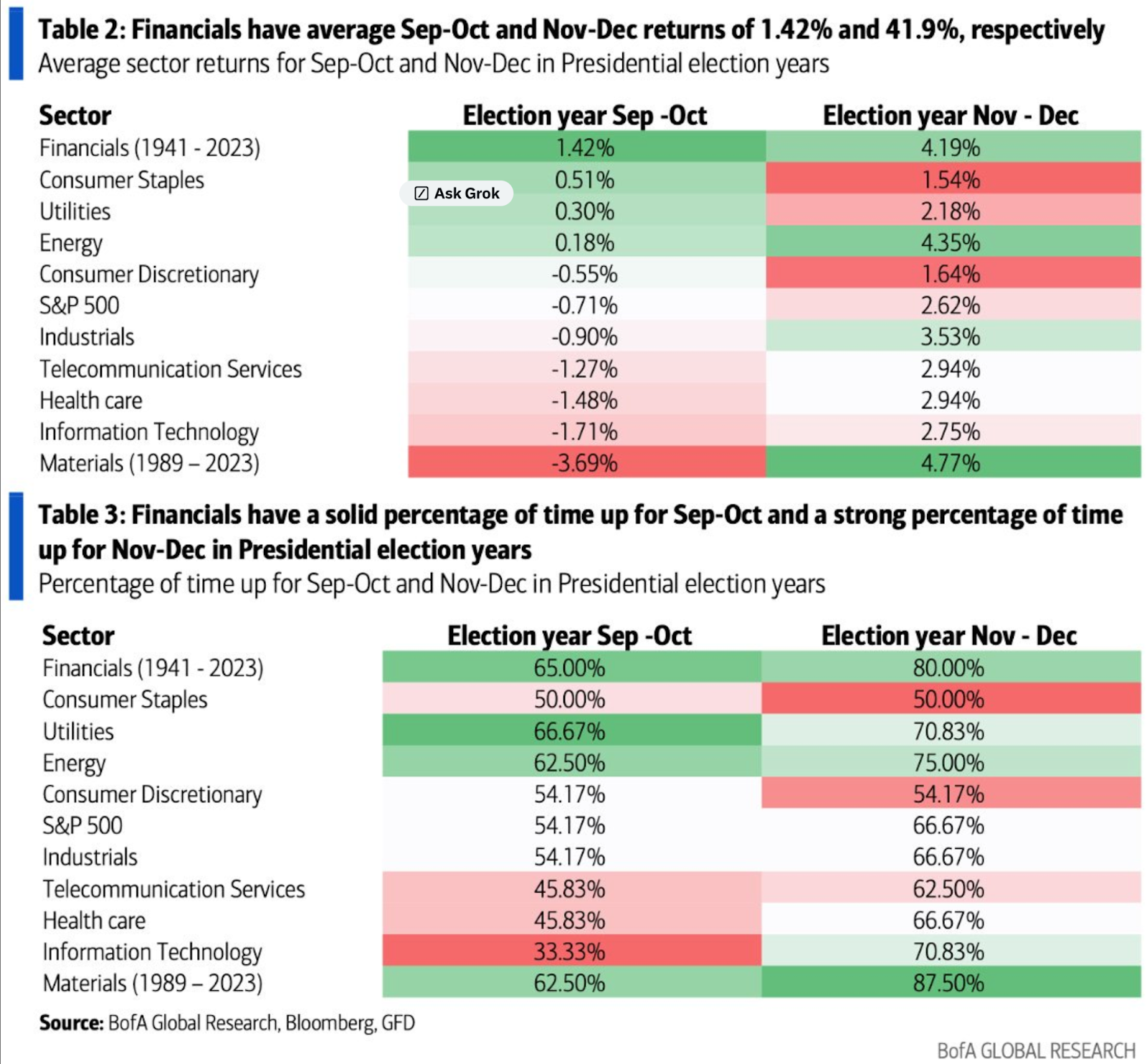

Market Outlook

Here’s how various sectors perform the months leading up to and following presidential elections.

Apollo ETF: Private Credit in Liquid ETF? How?

Apollo is launching an ETF that will contain illiquid private credit assets.

That's highly unusual since the create/redeem process of an ETF requires a liquid underlying.

Apollo resolves this issue by providing liquidity for the undelying credits.

Apollo is the market maker.

Doesn't that create a large set of contingent liabilities (equal to the size of illiquid assets)?

A contingent liability is similar to a bank offering deposits.

Generally, not everyone redeems deposits at once, and banks have a lender of last resort.

How will Apollo ensure it has sufficient capital on hand to create liquidity?

And, if Apollo fully reserves, doesn't that defeat the purpose of the ETF as a liquidity channel?

I wrote last year sometime that Apollo's goal was to disintermediate banking with capital markets.

This model of creating liquidity on illiquid assets is consistent with that.

How they risk manage this - would love to learn more...

This violates a couple laws of financial physics.

Disclosure: We are long APO

Digital Assets

Bitcoin is at a key technical level.

I was on the On the Margin podcast with friend Quinn Thompson. It airs this weekend.

Have a listen for our thoughts on Digital Assets and markets. We deep-dive into the ‘hot ball of liquidity’ thesis.

Overall, we believe it’s best to sell rallies in digital assets. We may re-assess our view sometime in October.

Company Earnings

Technology, Media, Telecom

Oracle (ORCL): Earnings and revenue beat. Revenue up 6.8% YoY. Strong cloud growth with IaaS and SaaS revenue up 21%, driving overall performance.

Adobe Inc. (ADBE): Earnings and revenue beat. Revenue up 10.6% YoY. Impressive growth in Digital Media ARR, highlighting robust demand for creative solutions.

Sector | Company ticker | Beat or Miss (Relative View) | Revenue (Absolute View) | Highlight |

Technology, Media, Telecom | Oracle (ORCL) | Earnings beat by 4.5%, Revenue beat by 0.45% | $13.3B, up 6.8% YoY | Cloud revenue (IaaS plus SaaS) reached $5.6 billion, up 21% in USD. |

Technology, Media, Telecom | Adobe Inc. (ADBE) | Earnings beat by 2.4%, Revenue beat by 0.74% | $5.41B, up 10.6% YoY | Digital Media ARR reached $16.76 billion, with net new ARR of $504 million. |

Lumida Curations

In case you missed it, here are some of the best curations from Lumida Wealth on Twitter.

Instead of watching hour-long market podcasts - we distill the key insights in 1 min shorts and serve them in threads.

The goal is to maximize insight per unit of time.

Clips from BG2 podcast about why USA needs to step up its nuclear strategy.

A great discussion on nuclear economics of USA, China, South Korea.

Snippets from We Study Billionaire’s Podcast with Jeremy Grantham, CIO GMO.

He discussed Amazon, AI & Macro events.

Insights from the recent Logan Bartlett podcast with Anthropic CEO, Dario Amodei.

Dario talked about Google, Government AI & Frontier models.

Highlights from the recent All in summit with Elon Musk.

Elon talked about Humanoids, AI, & SpaceX.