Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Macro: Manufacturing recession is over

Markets: Biotech and Energy

Company Earnings: Legacy Brand in Decline (LEVI)

AI: OpenAI vs Google, AI Bubble & Cohere

Digital Assets: We are midcycle in Crypto; Goldman Enters

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

I have been lucky to meet incredible folks:

- Arthur Levitt (ex-SEC Chair)

- John Mack (CEO, Morgan Stanley)

- David Rubenstein (CEO, Carlyle)

But all these moments were building up to meeting this legend.

We are investors not traders.

But, knowing when something is ‘on sale’ and when something is overbought helps to improve performance.

It’s been great to get the recognition on X for our work.

Here’s another. The iconic Ira Sohn conference featured one of our stock picks.

One of the 3 best stock ideas was $ASML

That’s a Lumida Stocking Stuffer pick and an October buy

(at a much better entry point than now I might add).

We wrote about ASML in our October 16th and noted it in our Holiday Top 10 Stocking Stuffer list. ASML is now 60% higher in 6 months.

The Lumida Stocking Stuffer stocks are also out-performing the major indices. See here.

Lumida's investment approach differs significantly from traditional wealth management products like ETFs, mutual funds, and hedge funds.

With ETFs, mutual funds, and hedge funds, you buy into a pre-existing portfolio with a specific net asset value (NAV). This NAV reflects the fund's performance over time, meaning you're buying past gains at current value.

This creates a performance lag - you will be buying assets that have already appreciated.

At Lumida, we use separately managed accounts (SMAs) for each client, customized based on market conditions and their investment goals and risk tolerance.

We focus on buying assets when they're out of favor and on sale — we like to say “you make your money on the buy” — and have the potential for future growth.

For example, we believed JPMorgan was a good investment in March last year, and we would allocate it to clients who joined us in March. A client joining later in October wouldn't have JPMorgan in their portfolio unless it remained a good buy; they would have semiconductors.

This is different from an ETF that might already hold JPMorgan, regardless of its current price attractiveness.

Here’s a short clip explaining the investing process and how it differs from traditional wealth management products like ETFs, mutual funds, and hedge funds.

Check out the links to the full episode of What’s On Your Mind below to dive deeper:

In case you missed our last episode on on Crypto, Macro and trading psychology with Alex Kruger, here are the links below:

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

We Had a Lot of Fun on April Fools

Here’s the full write-up:

I was wrong.

Cathie Wood is right.

Nvidia is a bubble, like Cisco.

The Apple Vision Pro will be a smashing success.

A recession is coming. It will start with a ‘credit event’

Inflation and interest rates will be lower for shorter.

60/40 is the future. Always was…

Trust whatever Goldman Sachs, Morgan Stanley, and JP Morgan call research.

Especially their conviction buys, like Apple or Tesla.

Tesla will be the most valuable company globally and dominate the EV market.

Cybersecurity investment is a fad.

Crypto is a scam.

The SEC has provided crystal clear regulations, firms should just go in and register.

SoFi will transform banking. Credit losses will be ‘contained’ because management said so.

X offers massive alpha. Just buy Snowflake and Palantir.

SoFi007girl is a real person and has genuine feelings for abstract corporate entities.

Stay single. You can get an AI girlfriend or boyfriend and build a family in the metaverse.

Centralized power works. We just need enlightened leaders who are incorruptible and know better.

Tech firms should not be permitted to compete with JP Morgan and other big banks.

They can’t build banking apps or serve tens of millions of people without a branch network.

The future is in 3D printing and seed oil based meats.

The United States isn’t growing anymore. Invest in Europe.

China will eclipse the United States. Robots will replace China’s shrinking population.

The SEC under Chair Gensler is neither capricious nor arbitrary.

There is nothing to learn from Buffett except his dietary choices: diet coke & burgers.

Investing in pre-revenue AI startups with $1 Bn+ valuations is a good idea.

The BRICs will create a currency that replaces the USD.

The peak for humanity was when Prince released ‘We’re going to party like its 1999’

We don’t need more nuclear energy. We need to reduce our energy demands.

Modern Monetary Theory (MMT) represents our best science.

We do not live in a simulation.

Stay Consensus.

Here’s a funny rap video we made if you want a chuckle 🙂

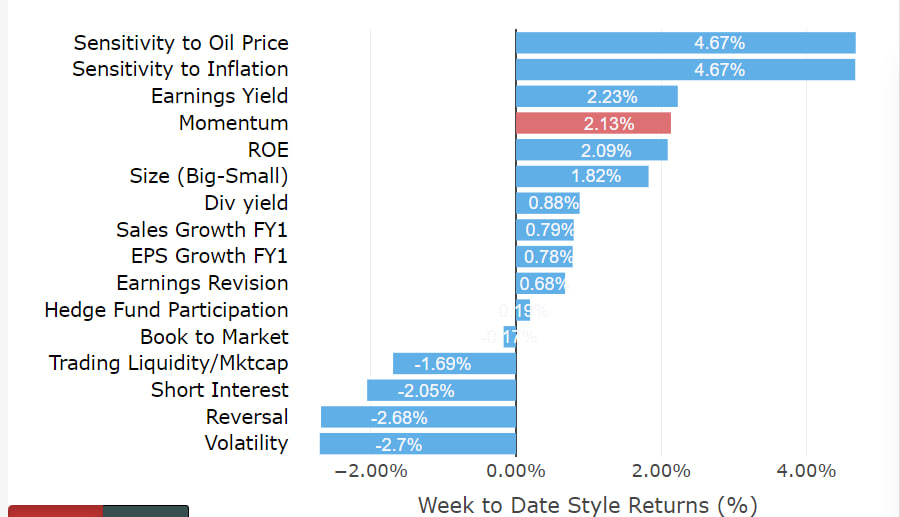

Factor Returns Analysis

For the first time since October, the S&P 500 closed more than 2% below its previous closing high set at the end of last week.

We have a new regime now. It started after the last FOMC meeting.

There is plenty of evidence now to suggest Mr Market is dancing to a new tune now.

It’s still bullish.

In short, Mr. Market favors stock that benefit from inflation (e.g., energy) and dislikes stocks that are punished by higher rates (e.g., biotech).

(We have reduced our biotech holdings quite a bit. We’ll rotate in when they are on sale after this factor subsides.)

And technology stocks are lagging. Not all of them - but the major indices. That’s something we’ve been anticipating since January when we noted that tech stocks are at the 99%-ile valuation.

You can still own tech - but you need to be precise.

Let’s take a look at what factors are working.

Momentum and Earnings Yield is a healthy combination. The losers are heavily shorted and volatile stocks (like SoFi).

We are starting to see some sloppy market action – namely, a couple dozen tech firms have tech valuations using the Forward PE metric that are higher than Nvidia.

But, that’s not reason enough to de-risk. Markets over-shoot and we are in a historically bullish period for equities.

Earnings growth can carry the market forward.

Note a change in color. Hedge funds are getting tired. Retail investors (folks that chase sales growth) are picking up some of the slack.

I will get nervous when I see a breakdown in Momentum and Earnings Yield factor. That’s not happening.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Macro: Manufacturing Recession is Over

Inflation re-accelerating across the board and challenging to the ‘rate cuts’ narratives.

As you know, we’ve been on the right side of this call for quite a while.

The CPI is coming in hot. The jobs report was strong.

The market expects rate cuts in June. I don’t see how we get a rate cut in June.

The public is hallucinating again.

We’ll continue to observe April and May data to see if there is any change in view.

Betting against rate increases has been a highly successful ‘non-consensus & correct’ move.

Note the ISM manufacturing PMI also improved.

The rolling recession we saw for most of the past 15 months appears to have ended.

This is the first expansionary reading since September 2022.

The improvement was driven by production and new orders – that’s bullish for the economy.

There will inevitably be some disappointing economic news. Economics breathe in and out like an organism.

When you see that bad data come in inevitably be sure to maintain perspective.

Markets

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

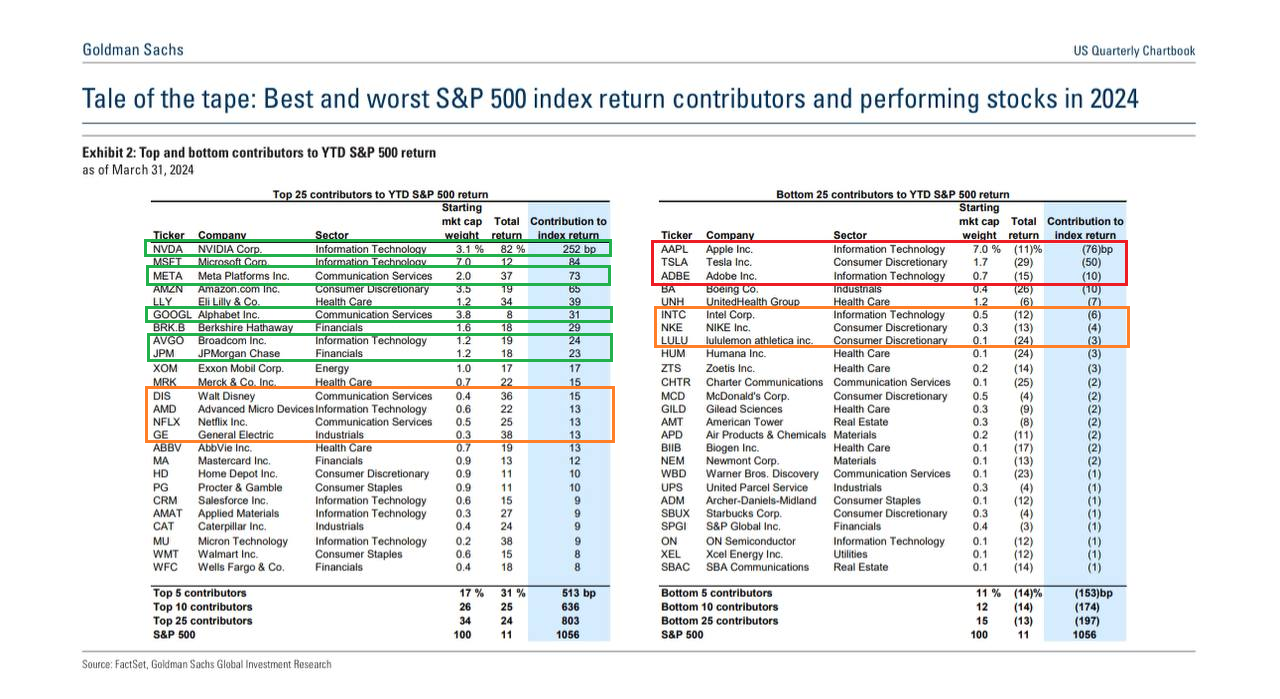

There’s a lot of questions around the sustainability of Mag 7 dominating the S&P 500 return.

Two thoughts:

1) Mag 7 is delivering earnings growth. But, fundamental earnings growth is there and in other names.

2) There is fear that Mag 7 names may need to correct.

But, the inverse can also happen. We can have other stocks ‘catch up’. That would also bring the Mag 7 weight to historical levels.

We are seeing leadership rotation to cyclicals such as energy and other areas with high earnings yield.

That’s what to expect from a broadening recovery.

Winners & Losers in S&P 500

Take a look at this chart.

It's overlayed with a few colors.

Green = we own it

Red = successful shorts

Orange = avoid

On Microsoft and Amazon, as noted, I believe these are fully valued. That means you get a Consensus Return.

We're looking for excess returns.

I would also add we wrote about all the green and red positions last summer and bought in October.

Mr. Market now views those positions as 'Consensus'.

That makes our job harder.

So towards the end of last year, we started to focus on Energy after the extraordinary tech rally

Now Mr. Market is feasting on Energy...

Note: Today is the first day in at 120 days that Nvidia broke thru its moving average on the downside

There is continued sign of Leadership Rotation from tech to energy

Chasing yesterday's winners is not a path to success

'You make your money on the buy'

That’s strong evidence, in our opinion, that Lumida has strong security selection and factor selection skills.

Ozempic Check-In

The Economist says: Demand for weight-loss drugs is surging.

Blockbuster medicines like Ozempic have spurred the development of almost 100 wannabe drugs that aim to be easier to take, cause fewer side-effects or deliver more effective weight loss.

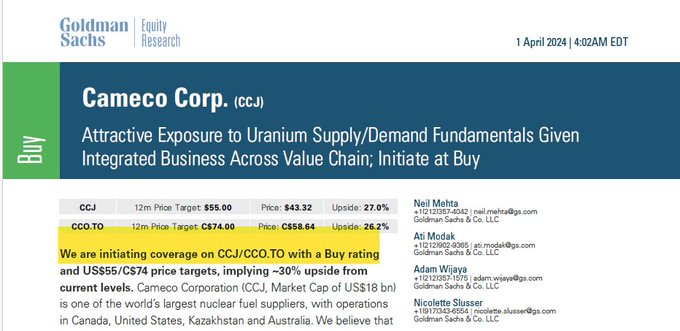

Goldman issued a BUY On Cameco

Cameco is the world’s leading Uranium miner.

Have a listen to this clip where we shared our thesis. That was last year.

The advantage of investing in uncovered securities is that you can get a real bargain before the sell-side banks notice.

We were buying Cameco last summer. And Energy.

Now this name is becoming Consensus.

Note: We believe there are higher risk-adjusted returns in Uranium than Cameco. We’ve learned more.

Cameco has sold forward Uranium contracts. This could force them to buy uranium in the spot market to fulfill demand. It’s not as clean a position as unhedged uranium miners.

We still own Cameco but aren’t adding more to it, and we have shifted towards other uranium positions.

Give us a few more weeks and we’ll publish another uranium name that we believe could do a 30 to 50%. No one has heard of it. We’re deep in diligence. It takes time…

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Lululemon Check-In

Lululemon was down 4.5% this Friday. That’s after a double-digit drop after earnings.

You don’t buy all the dips

Here’s what we said after Lulu 💩 the bed

Glad we dodged that bullet

Defense is dodging bullets

Writing about why you don’t do something is as important as writing about why you do something

We dodged bullets like this, Apple, Tesla SoFi and anything with a higher forward PE than Nvidia.

Capital is precious.

Semiconductors: Intel is down 7% on sales miss

We’ve been consistent on Intel and calling it out as a laggard

Intel needs a new AI PC product cycle to get its mojo going

That’s not happening this year

I do believe your expression in tech needs to be very precise

We’ve done a good of separating winners from losers right in semis and Mag 7

Tune into our semiconductor interviews on Lumida Non-Consensus Investing

Those interviews, along with research, shape our thesis formation

Much of our research is all out in the open.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

The Death of Google Was Greatly Exaggerated

Financial Times reports: ‘Google considers charging for AI powered search in big change to business model’

We wrote this on X:

2/10: ‘Google’s opportunity is to transform Gmail, Chrome, Search with AI app integration + SAAS revenue’

12/18: ‘Google can charge $20 / month for Personal Assistant AI’

We shared this idea on @howardlindzon Trends With Friends a few months ago and will find

Google was and remains one of the most mispriced assets in Mag 7.

And Google isn’t blowing loads of money on capex like Microsoft and Amazon

So far, odds of winning steak dinner bet with @altcap are looking pretty pretty good…

Bloomberg: ‘Apple Explores Robotics as Potential Next Big Thing’

Apple is throwing a lot of ideas at the wall.

Here’s one.

Excerpt:

Engineers at Apple have been exploring a mobile robot that can follow users around their homes, said the people, who asked not to be identified because the skunk-works project is private.

The iPhone maker also has developed an advanced table-top home device that uses robotics to move a display around, they said.

Before the EV project was canceled, Apple told its top executives that the company’s future revolved around three areas: automotive, the home and mixed reality. But now the car isn’t happening and Apple has already released its first mixed-reality product, the Vision Pro headset. So the focus has shifted to other future opportunities, including how Apple can better compete in the smart home market.

But the company has been concerned about whether consumers would be willing to pay top dollar for such a device…

Our take is simple. Apple is so big, new products don’t move the needle. They are reaching.

1) Apple car fizzled.

2) Apple Vision Pro Returns are increasing.

3) Now Apple wants to get into Robotics. Just like Tesla whose valuation is also ahead of itself.

Whose chips will power both? 🤔

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Goldman Sachs:‘The best sector YTD is energy’

The best is when your non-consensus view becomes consensus.

That’s how you generate excess returns.

Click and you will see our non-consensus call

The thing about GS research is that it is backward looking

Thank you Goldman for telling us that Energy has been going up.

We will share an energy stock next week or two… we are still assessing it. We are also very excited about this one and it could be a 50% return in 12 to 15 months purely from multiple expansion.

We are focused on Energy Services. Why? Their input and output costs are not sensitive to volatile energy prices. They provide services to the oil drillers… It’s a picks and shovels bet in the energy sector.

Looks promising.

Lessons Learned: One Year After the Banking Crisis

Checking on UBS 1-year after the Bank Mini Crisis

We bought UBS during the bank crisis. You can see our rationale in the thread below.

It's up about 60% since then.

We are trying to sort out whether to hold it or take advantage of long-term capital gains treatment and rotate.

I do believe we can do better by rotating. That's often the case once you get past long-term capital gains and you buy a quality dislocated asset.

But, it's also a nice quality compounder with share buybacks.

Click the thread to understand our rationale around UBS at the time.

I remember telling many people to buy this and I don't believe many people acted.

Here’s the main lesson.

When there is a dislocation, buy the highest quality asset on sale.

From the FT:

"UBS shares hit a 16-year high last week and have risen more than 60 per cent since it agreed to take over Credit Suisse last March, but the bank is under pressure from investors to improve its valuation versus US peers.

The shares were up 1 per cent on Tuesday morning. The two-year repurchase plan is significantly smaller than the previous two programmes — $4.5bn in 2021 and $6bn in 2022 — but UBS said it hoped to exceed its pre-acquisition level of buybacks by 2026.

The lender intends to repurchase $1bn of shares in 2024, but that would only begin after it completes the merger of the Credit Suisse and UBS parent companies, which is expected to take place in the second quarter."

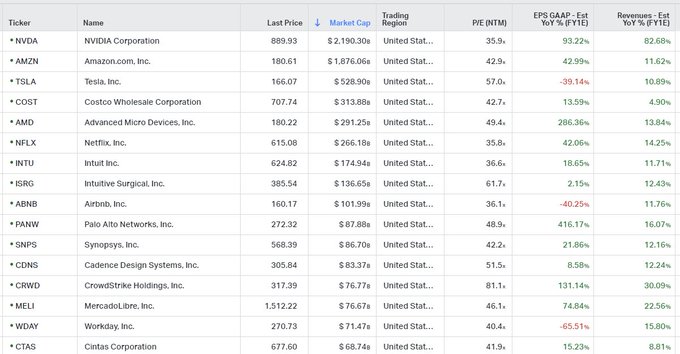

Stocks that are Pricier than Nvidia

Nvidia is the 'pace setter' in the market.

Does it make sense to over-pay up for an asset that is growing less than the pace setter?

That means you should scrutinize investments that are (i) more expensive than $NVDA, and (ii) have lower growth

There are many tech stocks that do not meet this simple criteria, including:

$AMZN

$TTD

$TSLA

$AMD

$INTU

$DDOG

$MDB

$TEAM

$LLY

$COST

$NFLX

$NOW

$GE

$ABNB

$CMG

$WELL

$PODD

$EQIX

$MSCI

$AXON

$TER

$TDG

Several of these are fantastic businesses with real moats.

In fact, we owned three of the names on the above list including Axon, Team, MongoDB, and DataDog... then we performed this analysis and concluded that was a mistake.

I would note on the bull case that the recent correction in software stocks looks like it is over from our perspective.

Here’s a table showing various stocks (not exhaustive) and their forward PE vs. Nvidia.

Still think Nvidia is an overpriced bubble?

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Company Earnings

Overall, the consumer sector appears to be in a cautious mode.

Companies focused on optimizing their product mix, channels, and cost structures to protect profitability in the face of inflation, higher rates and demand uncertainty

Consumer:

Conagra (CAG):

Outperformed analyst expectations, but revenues were down YoY.

The Grocery & Snacks segment grew; however, the Refrigerated & Frozen segment declined, potentially reflecting a shift in consumer preferences. We will look to follow up on this trend.

Levi (LEVI):

Despite beating expectations, LEVI's overall revenue dipped YoY. It ties up with our thesis on Legacy brands in decline.

LEVI, CFO Harmit Singh stated: “The structural economics of our business improved in Q1, driven by significant gross margin expansion, disciplined expense controls, and efficient working capital management.

As this earnings season draws to a close here are the major trends we witnessed.

Positive Trends:

● Financials: Most banks beat on both earnings and revenue, with loan growth and strong performances in wealth management and capital markets driving results. There were some exceptions, such as Discover Financial Services and UBS Group.

● Technology: Tech companies mostly beat on earnings and revenue, with cloud computing, cybersecurity, and chipmakers showing particular strength. There were some misses, such as Netflix, Spotify, and Snap.

● Consumer Staples: Companies like Walmart and Costco continue to see strong sales growth, driven by demand for groceries and household goods.

● Healthcare: Most healthcare companies beat on earnings, with strong growth in pharmaceuticals and medical devices. There were some misses, such as Pfizer and AstraZeneca.

● Industrials: Several industrial companies beat on earnings, but some missed on revenue due to economic softness in China.

Negative Trends:

● Retail: Many retailers missed on earnings and revenue, as higher costs and cautious consumer spending weighed on profits. There were some exceptions, such as Dollar General and Chipotle Mexican Grill.

● Real Estate: While some companies like Simon Property Group and Hilton Worldwide Holdings beat on earnings, others missed due to a slowdown in the housing market.

● Media & Entertainment: Warner Bros. missed on earnings and revenue, with weakness in its film division. There were some bright spots, such as Disney, which beat on earnings but missed on revenue.

Other Notable Trends:

● Several companies benefited from increased demand for electric vehicles (EVs), such as General Motors and Ford.

● Geopolitical tensions & Trade tariffs between US & China saw American companies feeling the pinch across sectors - first Apple, then Starbucks and Nike

● Many companies highlighted cost-cutting initiatives to improve profitability in the face of inflation and other economic headwinds.

AI

Bloomberg: YouTube Says OpenAI Training Sora With Its Videos Would Break rules

It looks like OpenAI is training their LLMs on Google’s data.

And we learned two weeks ago that 1 trillion parameter models are coming. They need massive amounts of data.

Who has the most data to train a trillion parameter model? Google.

The value of Youtube and Gmail and Workspace and Android in an AI ecosystem is under-stated. Google is one of our largest positions.

We bought about 1 month ago in size when it was on sale and wrote about it here.

Google is now near all time highs. We aren’t buying here, but we are still constructive - it’s cheap and out of favor for narrative reasons.

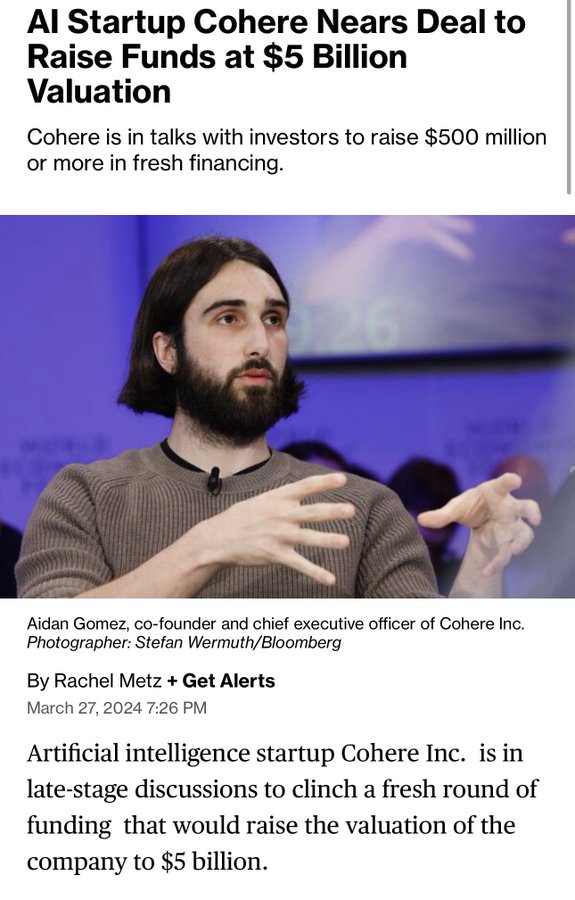

AI Bubble

Cohere is raising at a $5 Bn valuation on $22 MM in ARR

That’s a face melting 227x ARR multiple!

In 2021, SAAS firms at peak insanity were getting 100x ARR multiples

My mental model is to view these LLMs like engines during the dotcom era.

Many are sprouting up, many will fail to deliver outstanding returns.

One or two will dominate.

And my bet is Google is one of them - they have both the training data and the compute.

I’m fairly sure our investment in the ‘capex receiver layer’ - including CoreWeave will outperform all of this on a risk-adjusted return basis

Note: The CEO of Cohere, Aidan Gomez, was co-author of the seminal AI paper published at Google called ‘Attention is All You Need’

That paper will go down in the history books as one of the most transformative for civilization.

I don’t think that’s hyperbole.

Remember: QQQ beat venture capital over the last decade.

The pattern of liquid public equities indexes out-performing private expensive deals is a reasonable expectation.

‘You make your money on the buy’

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Digital Assets

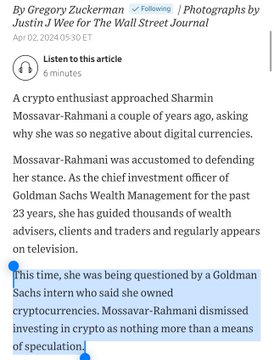

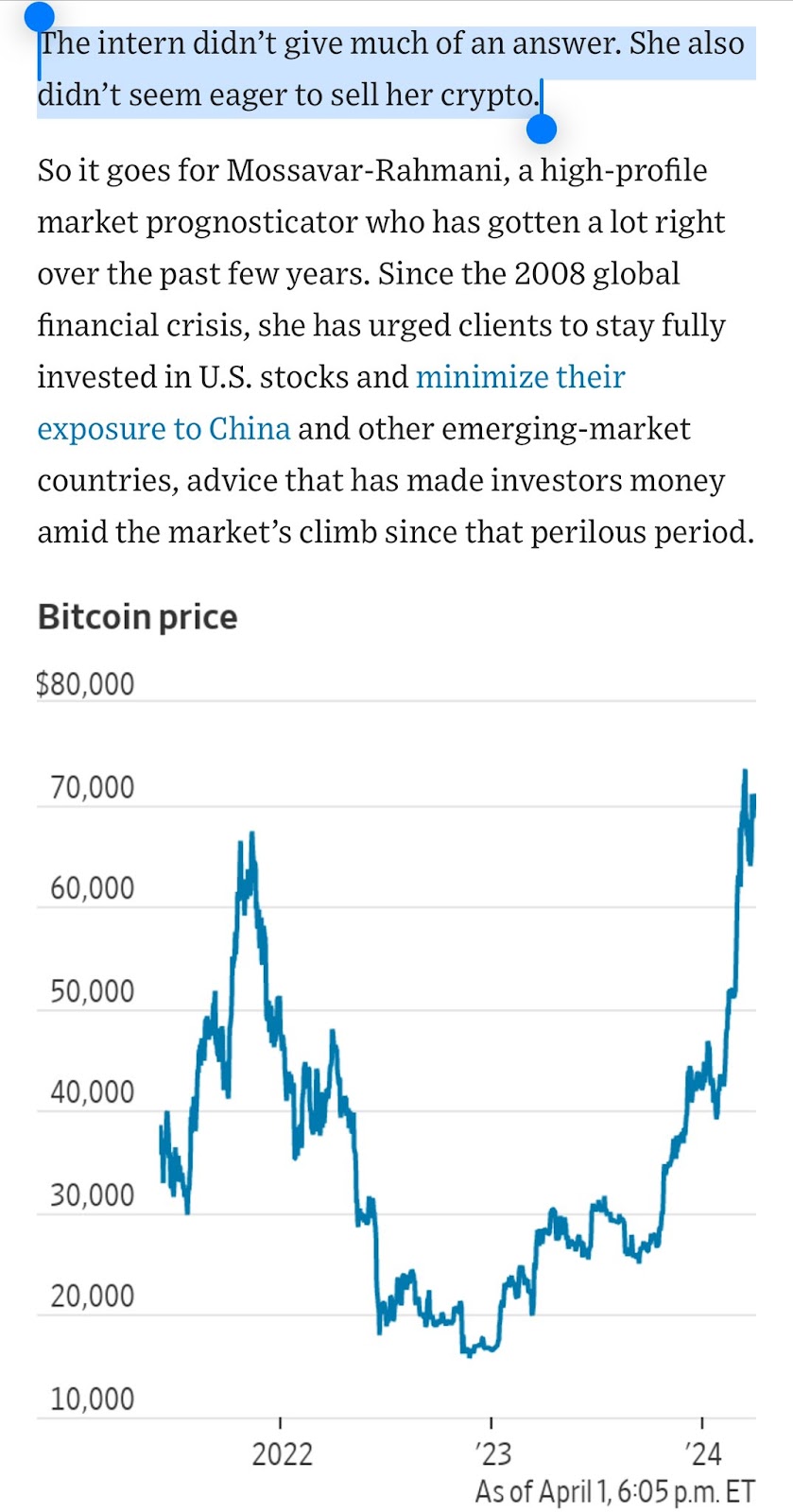

The WSJ has an article about an intern at Goldman Sachs (‘GS Intern’)

GS Intern is outperforming the CIO of Goldman Sachs due to their crypto exposure

GS Intern asked CIO why not own crypto. GS Intern was not persuaded by CIO

Message to GS Intern: I see you. We have a role opening for you.

At some point, we’ll have to share our framework for crypto investing.

In short, buy when no one wants to own it. Sell when everyone wants in and you see laser eyes on twitter.

It’s a sentiment cycle like anything else.

Unplug from the matrix.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

We bought ETHE

The Discount to NAV is 25%.

The funding rates have reset.

Ethereum has narrative pressure.

We view an Ethereum ETF as inevitable. It’s a question of when.

If it’s delayed, that gives us time to accumulate

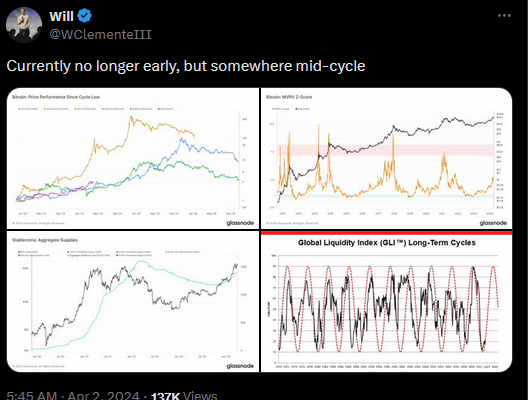

However, we do agree with Will that crypto is mid-cycle.

We have somewhere between the November election to next year at this time from where we stand today.

The last leg of the crypto cycle is where most of the gains are. The last 2 months can deliver strong returns.

We need to work thru some of the euphoria around meme coins and markets are doing that now.

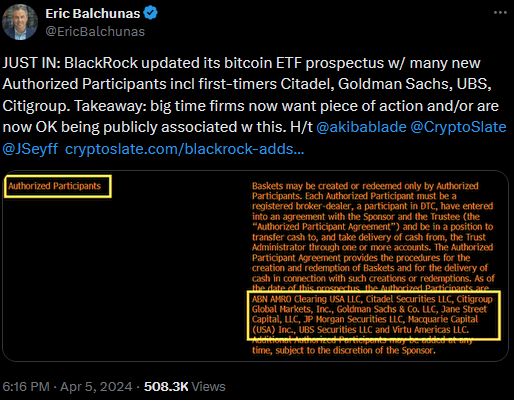

Goldman Sachs is market making for Bitcoin ETFs. The asset class is rising in legitimacy.

Meme of the week

Quote of the Week

“An investment said to have an 80% chance of success sounds far more attractive than one with a 20% chance of failure. The mind can't easily recognize that they are the same.” - Daniel Kahneman

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.