Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Macro: Economy Slowdown, Trump Bump, Bulls in China, Uranium

Markets: Apple Buyback, Cloud Wars, Datacenters, Buffett’s Successors

Company Earnings: COIN, PYPL, AAPL, AMZN, ON, SMCI, QCOM

AI: Token Costs, Meta vs OpenAI

Digital Assets: Morgan Stanley, UBS & ETF Approvals

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Ram spoke on the Digital Assets Investor Adoption Panel at the AIMA - (The Alternative Investment Management Association's) Digital Assets Conference 2024 this week.

He was joined by:

- Steve Kurz, Global Head of Galaxy Asset Management,

- Christine Topf, Associate Director at Trinity Church

- Manoj Vasudevan, Director at KAUST Investment Management

- Travis Williamson and Head of Hedge Fund Research at Albourne

This is a photo of Ram contemplating the consequences of the double-split experiment.

Sofi released their earnings this week, and the Twitterati took notice, given our previous takes on the stock.

We remain of the view that SoFi is an awful stock. Hope some of our readers profited from shorting or, at the very least, sold the stock.

SoFi is the world’s cheapest hedge against economic weakness and credit risk deterioration.

Macro

We are seeing evidence of a slowdown in the economy. You’re going to hear recession and stagflation calls in the next 4 to 6 weeks.

First, will lay out the bear case. Then will explain the bull case.

Recall from last week, GDP clocked in at 1.6%.

1) Per our friends at Merrill, the “best leading indicator of ISM & profits = new orders/inventory ratio is down 3 consecutive months.

We also saw an increase in bearish chatter on several podcasts.

Danielle DiMartino Booth made a recession call on Forward Guidance. Michael Kantro (Piper Sandler) is citing deterioration in labor indicators.

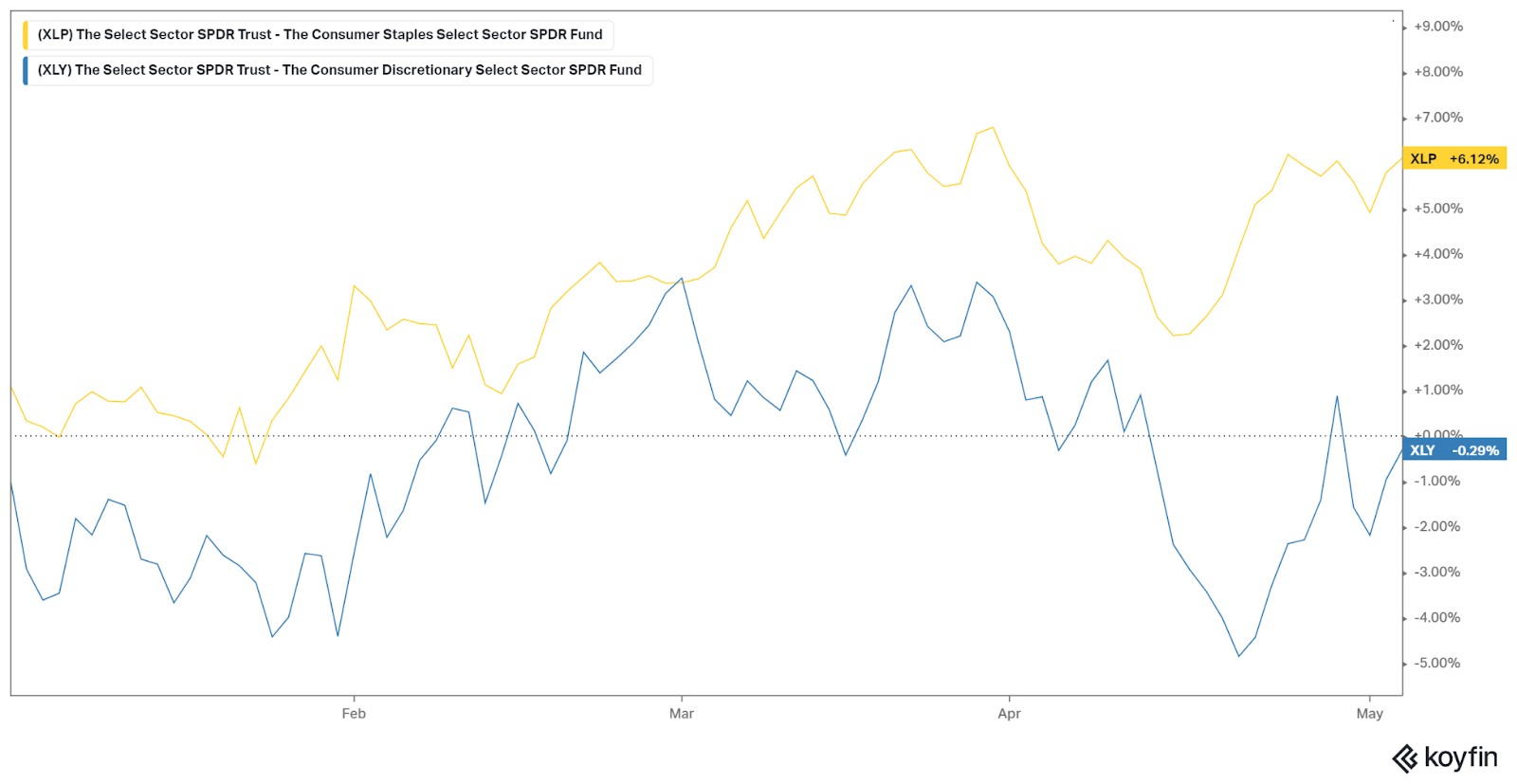

2) Take a look at how Consumer Discretionary is outperforming Consumer Staples YTD.

This happens when Mr. Market is concerned about a slowdown or growth fears.

Several consumer discretionary stocks have taken a hit - Lululemon, Starbucks, etc.

One interpreation of that is that consumers are “trading down” and pulling back (although valuations, exposure to China, and continued growth in e-commerce is another key variable). Dick’s Sporting Goods is doing fine for example.

F3) Take a look at the Citi Economic Surprise Index. This indicator dipped into negative territory, which means economic data is coming in weaker than expected.

4) Friday’s payroll report generated 175 K jobs - below economist expectations.

5) Leading economic indicators are deteriorating faster than Coincident indicators.

It’s fair to say Mr. Market is moving past inflation concerns and now focused on growth concerns.

We believe we’ve seen the peak in the 10-year rate. And we are seeing oil crack to the downside.

Here’s why you shouldn’t get too bearish despite a slowdown.

1) First off is the framing - Economies live and breathe like organisms. This is the ' exhale ' phase after a torrid 5% GDP growth in recent quarters.

Households have record net worth. Boomers are spending. Higher rates gives them the income to spend. Boomer categories like cruise lines and restaurants are growing nicely (see Royal Caribbean or Shake Shack for example).

2) The second derviative of Leading indicators are turning positive. Markets are forward looking.

Markets are forward looking.

Our synthesis is as follows:

1) We believe defensive positioning around quality value stocks is a great idea, and megacap tech firms that we continue to like: Google, Meta, Nvidia.

If there is a drawdown, the shear earnings power of these firms will carry them. The best part of high quality earnings growth is that if you’re wrong on your entry, earnings growth can bail you out.

2) Have a bias towards value. There’s a reason we like Google and Meta - they are the cheapest in Mag 7. We believe Amazon, Microsoft, and Tesla carry higher risk.

Look at Chipotle Mexican Grill (CMG). This stock is overvalued, and we recommend you sell it if you’re in that situation. It has a forward PE of 54.6 compared to Nvidia's 35.4.

There are still a couple dozen stocks that are far more expensive than Nvidia. Avoid those.

3) Avoid pricey software stocks - and anything that is more expensive than Nvidia. CapEx spend on datacenters is going up. Businesses are rational. They are going to cut capex elsewhere.

Where? Our bet is Software. (Perhaps other categories too). Take a look at Atlassian (TEAM) for example. They had a beat/beat/raise, but the stock was hammered anyway.

Flashback… In the Summer of 2011 the US fiscal debt was downgraded due to fiscal spending concerns. There was a European debt crisis around the ‘PIGS’.

The leading indicators were bad. In mid-October, the Economic Cycle Research Institute put out a recession call.

Markets flushed on that day. That was the best time to buy.

We envision a scenario where over the next couple of weeks the ‘bear case’ continues to ascend amidst negative headlines - illegal immigration, concerns on taxes, weakness in the labor market.

If that’s the case, we’ll continue to monitor. On the other side of that, markets will price in these risks.

It took Mr. Market only 60 days to price in Fed Powell’s ‘There will be pain’ speech.

A defensive posture with tilts as we suggest above is a good idea. Panicking is not a good idea. Focusing on wonderful companies with earnings growth and good valuations is the best strategy.

As Peter Lynch used to say, more money has been lost anticipating corrections than the corrections themselves.

Our various mix of indicators suggests that if there is a correction, it won’t exceed 10%. And we’re already at the 5% level.

We believe the FOMC press conference may have marked the peak of the 10-year. Take a look:

Possibly the 10-year bumps higher…but if Mr. Market is concerned about ‘growth’ then that is less likely.

A lower ten year is good news for equity markets as the discount rate applied to equities is lower (e.g., equities fair value is higher).

To be sure, we’ll have to see how markets react when the CPI is released on May 15th.

The FOMC indicated they see no stagflation and will not raise rates.

Rate-sensitive names like small caps and biotechs took off as a result.

Oil has also come down - take a look:

Part of this is driven by new supply coming online, but also prospects for slower growth.

Oil prices are a good proxy for global growth.

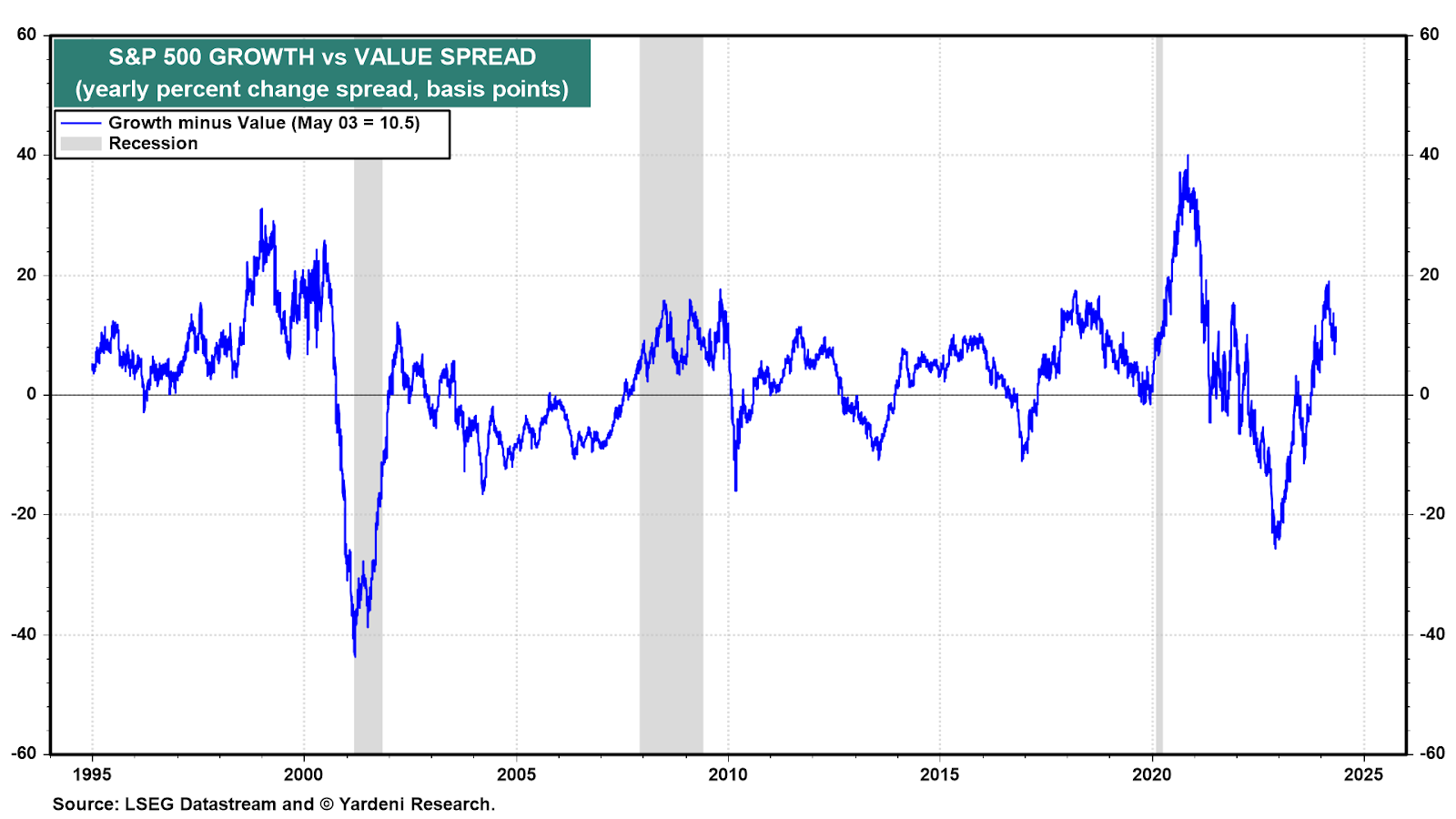

We are also seeing value stocks outperform growth stocks.

We expect that trend to continue. Mean reversion is at work.

All of the above suggests Mr. Market is concerned more with growth slowdown concerns rather than inflation.

Energy stocks and other commodity names are an excellent hedge if inflation is a concern. The point of concern is changing.

In a growth slowdown, Mr. Market favors value names with durable and quality earnings growth.

That’s why we are seeing Consumer Staples perform for the time being.

We believe that defensive positioning is a good idea. Focus on stocks with earnings growth and reasonable valuations.

Speaking of - here’s a check-in on Inspire Medical (INSP).

Inspire is a medical device company that treats sleep apnea. Our research on our ‘Aging Demographics’ theme discovered the stock.

We want to get long cataracts (via Harrow: HROW) and sleep apnea!

The stock has been up 30%+ since our Twitter call. Here’s a chart and link to the call.

Separately managed accounts that were opened at our buy point participated. We are not allocating that name to recent accounts or now - it’s just not on sale in the same way as it was back then.

We prefer energy services today. We’ll do a write-up soon and get more specific.

Harrow, another aging demographics play, is reporting next week.

We expect the stock to miss earnings due to a cyberattack on Change Healthcare - the largest reimbursement provider of medical claims in the United States.

Analysts haven’t updated their models to reflect that one-time disruption.

Management expects $1 Bn in revenue in three years from the cross-sell of new ophthalmic products launching later this year. The company has a bevy of other positive developments.

Either way, this name will be volatile, but we’re here for a three-year journey. At the end of 2027, we’d expect this stock to be up nicely.

If the stock disappoints due to the Change Healthcare issue next week, that would represent a buying opportunity.

Trump Bump

In February, we floated a hypothesis that a ‘Trump Bump’ is lifting equity prices.

Here’s a few more data points:

Biden’s State of the Union Address marked the top for US momentum ETF- to the day!

2) China is rallying.

We pointed out previously that Trump’s Iowa Straw Poll win coincided with China’s FXI index dropping to new lows.

Take a look at China’s FXI index:

China is in a bull market, and no one is talking about it.

We own 3 names here that we picked up after our “China capitulated” call on February 6th.

We were bearish on China for all of last year. When all the risks are priced in, no one is left to sell, and bad news is impounded into stocks.

That was an excellent call.

The names we picked up on that day, including Tencent and Alibaba, are up about 25% for separately managed accounts that were with us on that day.

We do not have a ‘thematic weight’ on China. This was a tactic.

3) Here’s the last data point under Trump Bump thesis:

Clean Energy stocks such as First Solar (FSLR) are no longer in a bear market.

You can look at our earlier Lumida Ledger for other data points, such as the sentiment of Anheuser Busch small business distributors, for more evidence…

It’s incredible how much these factors drive psychology and sentiment.

And if you aren’t aware it’s happening, you may lose sight of what’s driving Mr. Market’s behavior.

Note: We believe China and these Clean Energy stocks are overbought tactically. These names will move up and down alongside the election cycle.

The best entry or exit points are at extremes.

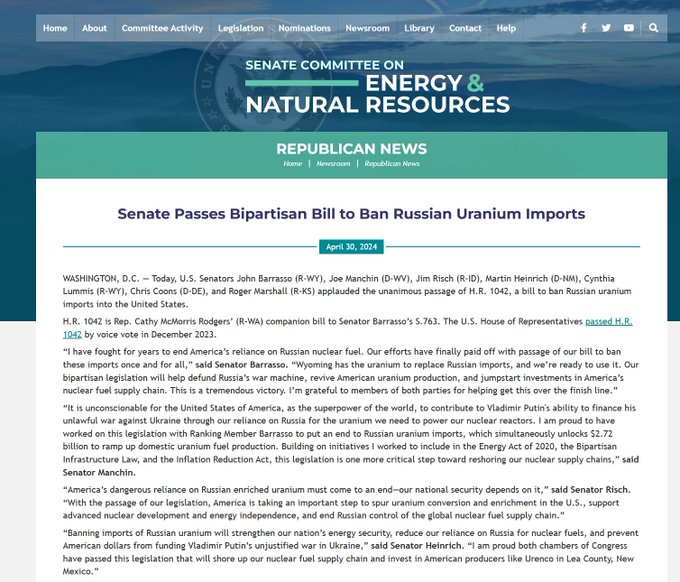

Uranium

The Senate Committee on Energy & Natural Resources passed a bill to ban Russian Uranium imports.

Russia is the world’s largest exporter of uranium. A state-owned agency produces it.

There are few alternatives.

The reality is that this bill is unlikely to pass—the world, including the United States, needs uranium.

In recent weeks, Lumida has been accumulating a new uranium name for our clients. Our goal is to interview the CEO in the next month or so, and we’ll tell you more about it.

If the stock is added to the Russell, it could run up purely for re-balancing reasons.

This stock would reduce the world’s reliance on Russia as a provider of high assay low-enriched uranium. We’re excited to own it.

Lumida Curation

There’s a lot of insight and alpha trapped in podcasts and substacks.

We’re investing time to comb through the best to harvest insights that we can weave into our investment process.

Don’t miss out on this take from Harris Kupperman by Lumida Curation on Uranium.

We have several uranium positions, and they’ve worked out well.

Check out this clip from Kupperman explaining the market dynamics and opportunities ahead.

On Inflation

Shelter Costs remain sticky. The median home price is up 7% YoY. That’s unlikely to change anytime soon.

Here are the charts:

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

MARKETS:

Apple Earnings

First, the facts:

Apple’s revenue was $90.75 Bn, down 4% YoY and down 24% QoQ

Net earnings: $23.63 Bn, were down 2% YoY, down 30% QoQ.

We started sharing our bearish takes on Apple when it had a modicum of earnings growth.

Last quarter, Apple had 0.5% YOY earnings growth.

Apple as a business is shrinking.

Shares were up ~7% after the results.

Just like Tesla’s shares bounced, in our view, this is just mean reversion from having a lot of bad news priced in.

And Apple announced a $110 Bn buyback – the largest ever. That boosted the stock by 7%.

We dug in deeper.

Apple’s Buyback is Exit Liquidity for Buffett.

1) Apple’s buyback program is $110 Bn

2) Apple’s free cash flow estimate for all of ‘24 is 109.9 Bn

That’s not a coincidence!

3) Buffett’s stake in Apple is $135 Billion. He announced this weekend that Apple would no longer be his largest position by year-end.

Apple’s buyback program is designed to provide liquidity to Buffet’s sales.

Why didn’t management just come out and explain it that way?

Always be skeptical of management on earnings calls.

We noted that management shared no sales figures on Apple Vision Pro either.

What we heard was a commercial.

Our thesis remains intact: Apple is a growth stock transitioning to a value stock.

We recommend folks sell at these levels if you haven’t had a chance to get out. Here’s a chart.

This is a sell-the-news event. Notice Tesla did not participate in the post-FOMC rally this week either…

Apple had no breakout of Vision Pro sales.

Simply put, Apple is so large it cannot find earnings growth anymore.

Apple needs another planet to sell into. China is tapped out, and other local providers have a faster-growing market share.

GS on Energy Demands from Datacenters:

Goldman expects an incremental 650 TWh of energy demand.

Let’s put that in perspective.

An average data center can consume about 30 to 50 MW of energy.

650 TerraWatt Hours implies 2,000 to 2,500 datacenters

Sanity Check: One country, Saudi Arabia, is setting up 60 data centers.

The math checks.

You can front-run sovereigns and corporations on this investment theme.

There is more to AI than NVDA.

These are the names to scoop after the ‘higher for longer’ correction.

if you want to get long after the correction.

We are getting closer to the bottom.

Highlights:

- Rising Demand: Data center power demand is projected to increase by 160% by 2030 compared to 2023 levels, adding about 650 terawatt-hours (TWh). This rise corresponds to a 0.3% compound annual growth rate (CAGR) in global power demand attributed specifically to data centers.

- Focus on Data Centers: The growing emphasis on data centers is due to their expanding role in supporting increased digital activities like cloud computing, data storage, and internet services. As global digital infrastructure expands, so does the demand for data centers.

- Technological Impact: From 2015 to 2019, the workload demand on data centers nearly tripled, but their electricity consumption remained stable due to efficiency gains from shifts to cloud computing and hyperscale data centers. These technologies optimize power usage and server utilization, initially allowing more computing power with the same or less electricity.

- Narrowing Efficiency Gains: The initial large gains from transitioning to cloud and hyperscale platforms are tapering off. As most of the easy gains from technology and infrastructure upgrades have been realized, further improvements in efficiency are becoming harder to achieve.

- Increasing Power Consumption: With diminishing returns on efficiency and continued growth in digital demand, the power consumption of data centers has started to increase. This trend is expected to continue as the capacity and number of data centers grow globally.

- Comparison with IEA Forecasts: The forecasts from Goldman Sachs Investment Research (GIR) are more aggressive than those of the International Energy Agency (IEA), suggesting a more rapid increase in power demand for data centers. This discrepancy highlights differing assumptions about technological advancements and market growth rates.

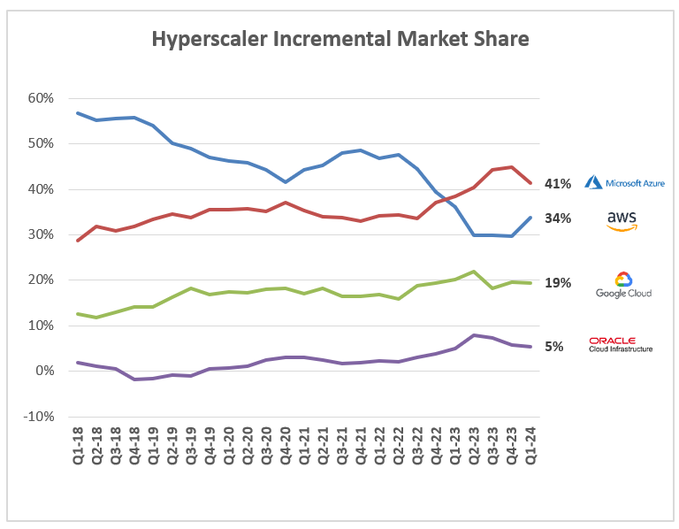

Cloud AI Earnings Reports

Check out the full post on hyperscalers growth here from Jamin Ball.

Amazon: $100B run rate growing 17% YoY (last quarter rose 13%)

Microsoft: ~$76B run rate (estimate) growing 31% YoY (last quarter rose 28%)

Google: $38B run rate growing 28% YoY (last quarter rose 26%)

Amazon is seeing some reversal in incremental share gained from Azure to AWS and Google Cloud.

We believe Amazon and Microsoft are fully valued and favor Google.

Encouraging to see Google gain market share in Cloud. Google was always a distant third. Our thesis in Google doesn’t turn on Cloud, but we’ll take it.

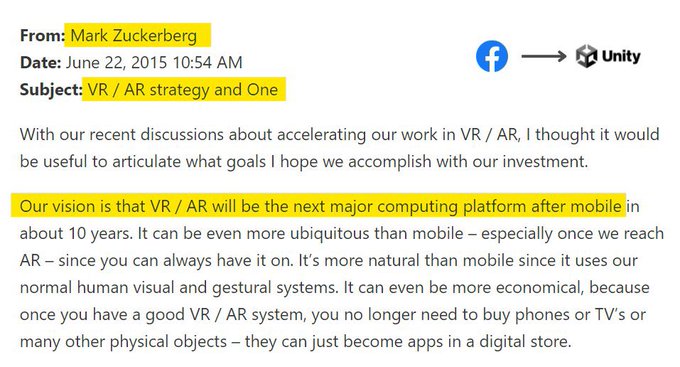

Meta vs. OpenAI:

(1) Open AI has 100 to 300 MM monthly users and charges $20 per use.

(2) Meta has 3 Bn per month and charges $0.

Who wins on consumer adoption?

A friend sent me this after hearing my take on META.

My view on META evolved after listening to Zuck on the latest call.

He is not spelling out the vision… but I see it.

He is taking on Microsoft, Amazon, and Apple.

Not surprisingly, the analysts aren’t getting the big picture

Buffett’s Successors Are Lagging Buffett

The Roman Empire nearly fell apart after Marcus Aurelius.

What good if you are goat 🐐 level but can’t transmit the way to the next generation?

Excerpt from FT:

They also may have been behind the disastrous investment in Paramount Global, the entertainment company that owns MTV and CBS. Buffett has not specified who made the $2.6bn wager in 2022, and when asked about the trade at last year’s annual meeting, he did not take ownership of the bad bet, something he often does.

The stock has dropped more than 60 per cent since it invested and Berkshire recently started dumping its position at a loss.

Combs was rumored to be behind an investment in Viacom, Paramount’s predecessor, back in 2012, and even though the size of the investment would be quite large for one of the two managers, it is not out of the question given they also hold multibillion-dollar stakes in other businesses.

In a world without Buffett, Combs and Weschler will still benefit from the company’s long-honed advantages, including something that hedge funds and private equity groups have been chasing in recent years: permanent capital.

But the pair also face a structural disadvantage that Buffett did not have in his early years. Combs and Weschler will become some of the largest money managers on the planet when Buffett departs, with a vast stock portfolio bigger than any of Berkshire’s individual operating divisions.

Alongside Buffett’s chosen successor as chief executive, Greg Abel, they will also decide how a record $168bn cash pile is allocated, a sum so vast that the sprawling investment conglomerate could buy up all but a handful of companies.

It is a level of firepower that is unheard of on Wall Street and Buffett has lamented the dearth of long-term investment opportunities suitable for such large sums of money.

On Venture Capital

This is a very scary graph, but it didn't surprise me. Darwin returned from vacation two years ago, and many startups haven't made enough progress to make him happy. Many of these companies are being propped up by wishful insiders and won't make it when all is said and done.

Company Earnings

Financials:

Crypto exchange Coinbase seeing explosive growth in transaction and subscription revenues as digital asset trading activity surges

Fintechs like SoFi benefit from diversified business models with lending segment offsetting revenue fluctuations

Payment giants PayPal and Mastercard are navigating higher transaction volumes through credit losses remain an overhang

Exchanges like ICE are gaining from robust mortgage tech demand while Moody's shows strength across ratings and analytics

Tech/Media/Telecom:

Big tech players like Apple weathering demand softness in hardware like iPhones with growth in higher-margin services

Cloud hyperscalers like Amazon Web Services maintaining solid growth despite cyclical consumer pressures

Semiconductor firms AMD and Qualcomm driven by data center/AI acceleration and automotive growth opportunities

Component supplier ON Semiconductor impacted by weakness in sensors

Enterprise hardware vendors like Super Micro are benefiting from infrastructure refresh cycles.

E-commerce marketplaces like eBay posting modest GMV gains but advertising a relatively bright spot

Delivery platforms like DoorDash are facing profitability challenges despite healthy order/GOV growth

Automotive/Industrials/Energy:

EV makers like BYD are seeing demand volatility across passenger and commercial vehicle segments

Electrical equipment provider Eaton aided by healthy America's growth though global electrical remains sluggish

Utility Dominion Energy impacted by weather and pricing pressures weighing on top-line performance

Healthcare:

Pharma giants Eli Lilly and Novo Nordisk outperforming, driven by volumetric growth tailwinds and pricing power in key therapeutic areas like obesity

Consumer:

Coffee chain Starbucks grappling with traffic declines, though loyalty remains an offset.

Beverage leaders like Coca-Cola and PepsiCo benefiting from resilient demand and effective revenue management strategies

Quick service restaurant McDonald's delivering modest comparable sales growth amidst consumer spending shifts

Overall. Financials and payments are exhibiting momentum, and healthcare is benefiting from innovation. While discretionary consumer segments face volatility, staples and beverages are holding up. Industrial and automotive trends remain mixed.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

AI

Here’s an excellent post from Awni Hannun - ML researcher at Apple.

Excerpt:

This is an essential chart for LLMs. The $/token for high-quality LLMs will probably need to fall rapidly.

Here's a back-of-the-envelope forecast for Llama 3 4-bit 70B on an M2 Ultra with MLX: $0.2 / million tokens.

- 4-bit 70B model generates at 15 toks/sec on an M2 Ultra

- Consumes 60W power

- $0.18 per Kilowatt-hour average for US

1,000,000 tokens (1 second / 15 tokens) (1 hour / 3600 seconds) = 18.5 hours

18.5 hours 60 W (1 Kilowatt / 1000 Watts) (0.18 dollars / Kilowatt hour) = $0.2

To understand more about the LLM wars - check out this Lumida Curation of BG2 Podcast - it gives an excellent outlook on the future trends shaping the playing field.

Digital Assets

We have a credible source that indicates Morgan Stanley and UBS will be approving Bitcoin ETFs on their platform in the coming months.

UBS is the largest asset manager in the world. Morgan Stanley has a lot of cred.

Intriguing developments.

Quote of the Week

“In the business world, the rearview mirror is always clearer than the windshield." - Warren Buffett

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, please join our waitlist.

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.