Welcome back to the Lumida Ledger.

If you find this valuable, we’d greatly appreciate you sharing it far & wide with your network. That’s how we grow and keep the content free to read.Here’s a preview of what we cover this week:

Macro: Uber and Illegal Immigration

Markets: NVDA, Semiconductors, Open AI, Startups

Company Earnings: Negative on China, Mixed Macro, Healthy Consumer Demand

AI: Sam Altman & Semiconductor CapEx Receiver Thesis

Digital Assets: Michael Terpin interview

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Ram was recently featured in The Exeter Bulletin's Winter 2024 issue.

Ram discusses the intersection of Crypto and financial wellness, and reminisces about his time at Exeter.

Here’s an excerpt - a walk down the memory lane.

“Ahluwalia credits his four years at Exeter with humbling and inspiring him, from the Cs he got in French his prep year (he won a French prize as a senior); to studying Buddhism and philosophy with Emeritus Religion Instructor Peter Vorkink”

“People’s long-term goals are incredibly meaningful to them. It’s deeply rewarding when you can help someone achieve their goals.”

This week we spoke to Chris Thomas, a Superbowl Athlete.

Chris’s stories provide a window into professional athletics - and the importance of psychology & mindset. We talk about greatness, trauma as teacher, and the Human Spirit.

Don’t forget to tune in to our latest episode of WOYM (What’s on Your Mind): where Justin & Ram discuss Nvidia, Sovereign AI, Biotech, Google Criticism

Subscribe to our Non-Consensus Podcast : Apple Podcasts, Spotify

Macro

China is now positive YTD and no one is talking about it

China is up sharply.

Have you checked in on China lately?

Take a look how it's done since our Capitulation call.

What exactly do these analysts at JP Morgan and Goldman Sachs do all day? As far as I can tell they 'explain' topics like the GLP1s or EV trends.

Then they slap on price targets. Then they change the price targets based on whatever the market did. There are a lot of fancy graphics involved.

I thought the purpose of investing is to make money. There is very little intellectual courage on Wall Street (although there are exceptions and they are A+).

You can see our timestamps in the image and thread. I have no idea what will happen to China from here on out. BIDU's earnings, reporting Monday, may shape that.

Can you bet on massive Illegal Immigration?

Yes. UBER stock.

UBER’s management noted ‘increased Driver availability’ on their earnings call.

More drivers means (i) more revenue and (ii) lower costs.

More drivers means more capacity and coverage.

That means a higher match rate for customers.

More drivers also means less need to pay out a competitive wage rate..

What are other businesses that might benefit?

InstaCart, DoorDash, and other home delivery or manual type work.

But CART and DASH benefit primarily on the cost side which is less interesting.

What are other specific businesses benefiting from illegal immigration? Construction is an obvious one.

Are there other tickers or sectors? Childcare?

For the record - I am not advocating for more illegal immigration. I am also not advocating to buy Uber.

That said, there are significant industry effects from massive illegal immigration and it's worthwhile to think through what those are.

3 MM immigrants is a big number.

Uber has had an incredible run up. Dara Khosrowshahi has done a fantastic job.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Markets

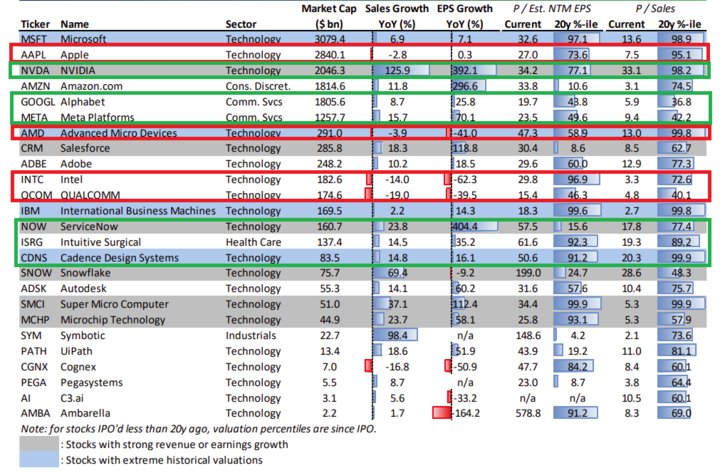

AI vs. Fake AI In Big Tech

The table below shows how the benefits of AI are accruing to a small group of companies.

The ones in Green we own or we intend to buy more of on pullbacks.

The stocks in Red we are skeptical of and may hedge with from time to time.

It’s not rocket science to identify winners and losers and do the work to map out the category.

We have said many times, the best names to own in Mag 7 are Nvidia, Google and Meta.

Microsoft is Consensus AI - and expensive. And it’s not growing fast enough.

Our conclusions look pretty obvious when you see a table presented this way.

We should note valuations are getting rich for several of these names - Microsoft and Apple.

And we expect they will lag.

Size is the Enemy of Returns

Here’s a snip From Berkshire Hathaway’s 10Q:

"Given Berkshire's present size, building positions through open-market purchases takes a lot of patience and an extended period of friendly prices.

The process is like turning a battleship."

They can't get great deals unless there is a prolonged bear market.

Open market purchases work against them.

That also means they are stuck holding Apple for a long time even as they try & sell.

The best days of Berkshire are behind it.

There is a way to build the next Berkshire Hathaway however. Some, like Apollo’s Marc Rowan are doing that. A family office or consortium of families can pull it off.

Berkshire’s at core is about tax-efficient internal compounded financed with cheap non-callable debt.

This thread explains high-level the key steps required to do so. If you’re a billionaire with some extra change, drop us a line and we’ll share the specifics

Investment Thesis: Elective Health

We live in a weird world where:

(i) Americans are not having enough kids, and

(ii) there are many, many couples struggling to conceive.

I drove by a fertility clinic today.

Parking lot is packed. I decided to drop in. The waiting room is packed.

I have more than a handful of friends that have shared their struggle.

I don’t have the data on whether this is a modern phenomenon or not…

But, these are generally young and health-conscious couples - both in diet and exercise.

They are spending tens of thousands of dollars on conception strategies.

It’s an unfortunate state of affairs and creates an emotional toll on the relationship.

I’m not sure how to make sense about the larger social issue or the causality.

(Will it turn out to be a story not unlike the hypothesis linking Diet Coke to autism?)

What are we doing?

Researching small caps that specialize in fertility services.

There are many of these wonderful small growing healthcare services businesses out there serving the unique demographic shifts underway.

And Elective healthcare spending across a broad variety of categories - from NAD to stem cells to fertility - shows no sign of abating.

Why we are Long Dell

The premise of the ‘capex receiver thesis’ you want to own the Silicon Layer.

Governments, Big Tech, and Startup (really, VCs) are going to spend tens of billions on GPUs.

The prize for winners is large - potentially winner take all within each customer segment.

At the same time, be skeptical of the Application Layer - the customers of Nvidia.

The Application Layer is still going through Discovery.

There are hard technical challenges… such as how does an LLM ‘remember’.

Or process and learn quickly on new data.

There is still no killer broad-based use-case for AI

Coding is the main use-case.

That’s a big use-case in terms of impact — but it appeals to a small fraction of the population.

The DotCom era had two killer apps:

1) Browser: Netscape Navigator

2) Email

We are a long way from generalized AI.

The use-cases that work - Mid Journey, Runway, Synthesia, Bloomberg GPT, and Legal GPT - are niche and verticalized.

And that’s what we continue to expect…

tl;dr LLMs are high risk, low reward startup investments

Winner and Losers in AI Mega Cap

Nvidia will win the race for Sovereign 'On Prem' AI. (We own it.)

Google will win the race for Personal Assistant AI. (We own it.)

Microsoft will win the race for Enterprise AI. (Too expensive, we don’t own it.)

CoreWeave will win the race for specialized AI compute. (We own it.)

Amazon and Microsoft duke it out for Startup AI services.

Oracle... not sure what race they will win. We are short Oracle. (We shorted it and made money.)

Apple is down 6 days in a row and broke thru its moving average.

Mr. Market is waking up to the idea that Apple is a shrinking business.

Guess what’s outperforming over the same timeframe.

Google.

Google is the only Mag 7 stock not priced for AI, and it’s the only Mag 7 name we continue to accumulate.

Market Compass

The market was shaky at the beginning of the week. Microsoft had breached its support.

Nvidia breathed new life into markets.

However, on Friday, we saw SMCI and Apple continue to head lower. We do see signs of ‘buyer fatigue’ so we caution against chasing semiconductors at these all-time highs.

Better to focus on small caps and biotechs now.

We believe Nvidia’s earnings were the ‘sugar high’ and create a local top for semiconductors.

A good strategy is to buy collars or hedge semiconductors positions. Hang on to the winners - including Nvidia.

Avoid owning weaker semiconductors stocks including Intel and AMD.

Also, as you know, we don’t like Apple and Oracle.

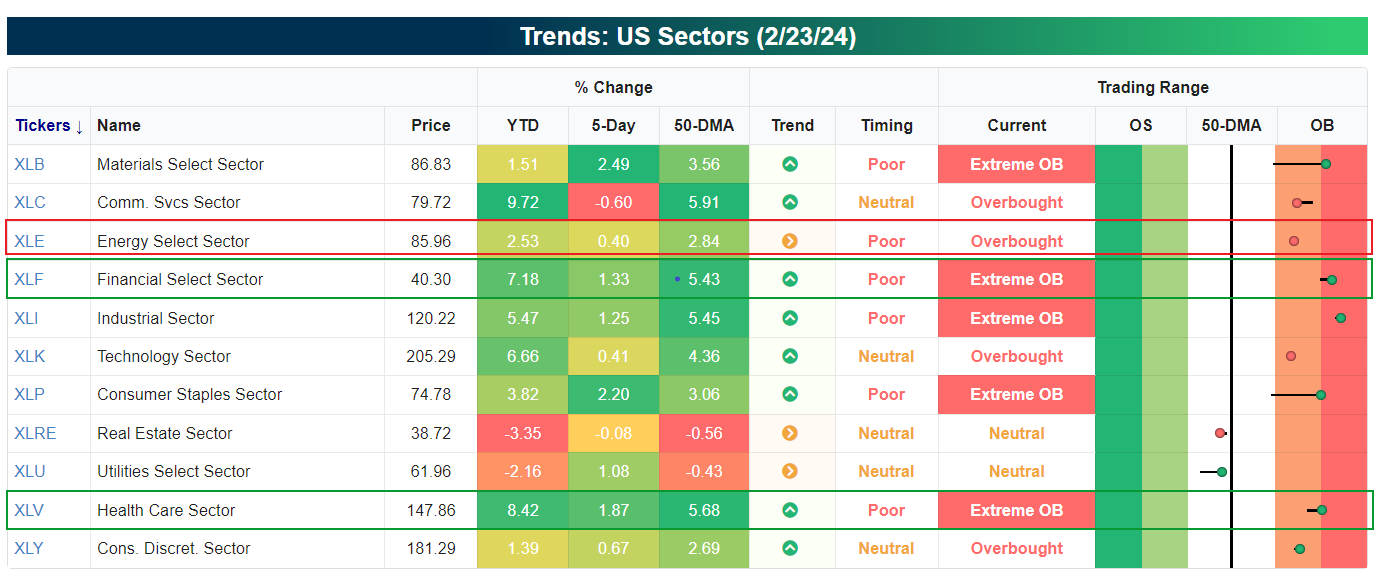

Cyclical sectors such as Energy and Financial are up 1.87% and 1.33% respectively, since last week.

The 10-year is near YTD highs.

Mr. Market is focusing on value rather than technology. Technology leadership is quite narrow.

We bought a gold miner (Eldorado Gold) on Friday. We haven’t bought a gold miner in… over 10 years.

But we buy what’s on sale and play the best hand we can given what Mr. Market offers.

Here’s a chart showing our nice entry point on a high volume down day.

We are more excited about a Utility. We acquired a Utility that has a link to both Nuclear Renaissance and AI Data Center play.

There is an embedded real option in this utility play should they win this contract.

AI energy demand is already causing brownouts in certain parts. The need for old energy and nuclear power is real.

We will share this ticker in a few weeks as we are still building our position.

We also own WorkDay (WDAY), which reports earnings this Monday. WorkDay, a human resource SAAS firm, is demonstrating continued margin improvement and can grow revenue through its partnership with ADP. Workday also has an international expansion opportunity.

We also successfully shorted JetBlue (JBLU). Carl Icahn announced he has an activist position. That caused a bump in the stock price. That was a fairly easy ‘sell the news’ event. We bet 2% of the portfolio on that tactic. We have since fully covered the position.

Here’s JetBlue:

Hedge Funds Are Over-Rated

Why pay 2 and 20 for a hedge fund?

Brutal article critiquing Bill Ackman’s Pershing Square. The vast majority of hedge funds are over-rated and not worth the fees.

This person calls hedge funds a scam.

What’s better to Own: Nvidia or OpenAI?

Nvidia will outperform OpenAI the same way liquid QQQ beat venture capital over the last decade.

OpenAI is already losing ground to another AI startup called Perplexity…

LLMs are facing the Search Engine wars all over again.

The 18th search engine (Google) won.

What will outperform both Nvidia and OpenAI?

Hypothesis: CoreWeave (2 to 4x in 18 months)

Lumida Wealth sourced CoreWeave, the Cloud AI data center provider that powers Open AI, in the fall.

We are skeptical about most IPOs, but we are excited about this one!

Gene Munster: Tech ETF Portfolio Manager says ‘X’ will be a Top 3 Foundation model

We believe Gene is wrong.

Is X a $100 Bn LLM in the making?

No.

Open Source LLMs such as Meta Llama make the value of Foundation LLMs close to zero.

I can run an LLM on my laptop for close to nothing.

Like water, LLMs are high value and essential to life…

but low marketable value w/o proprietary data.

X data has value. But you can buy X data today

Hedge funds do that. (And others screen scrape).

And they don’t pay tens of billions of dollars for the data.

In the Dot Com era, people thought Amazon would make a fortune selling consumer data insights.

That did not go anywhere.

This is a peak sentiment AI type post.

X will make money on Ads for many years to come.

If Elon could re-trade X he would.

And he tried!

Remember the courts would not let him out of the deal.

Does X have the capex to spend $10 Bn on GPUs like Meta and others?

No.

I’ll take the other side of this easy.

It’s getting more clear. @elonmusk is 80% genius, 20% master of good luck.

In a decade, his purchase of Twitter will power #XAI to rival $TSLA and #SpaceX as his greatest source of wealth creation.

The reason is Twitter’s data is powerful (best source of real time intention), and he’ll use the data to train xAI to be a top three Foundation Model.

Those models should be valued in the hundreds of billions of dollars. Bloomberg estimates his current net worth at around $210B.

And Gene who is a highly regarded tech analyst is also wrong on Apple.

On Startups:

Venture markets have re-priced. Entry valuations start at $10 MM.

Not bad.

But, there’s still way too many venture firms out there. Why give up liquidity when there is no major capital imbalance?

The best venture vintage was 2011 +/- a year. That produced Uber, Twitter, and a host of other incredible outcomes.

‘You make your money on the buy’

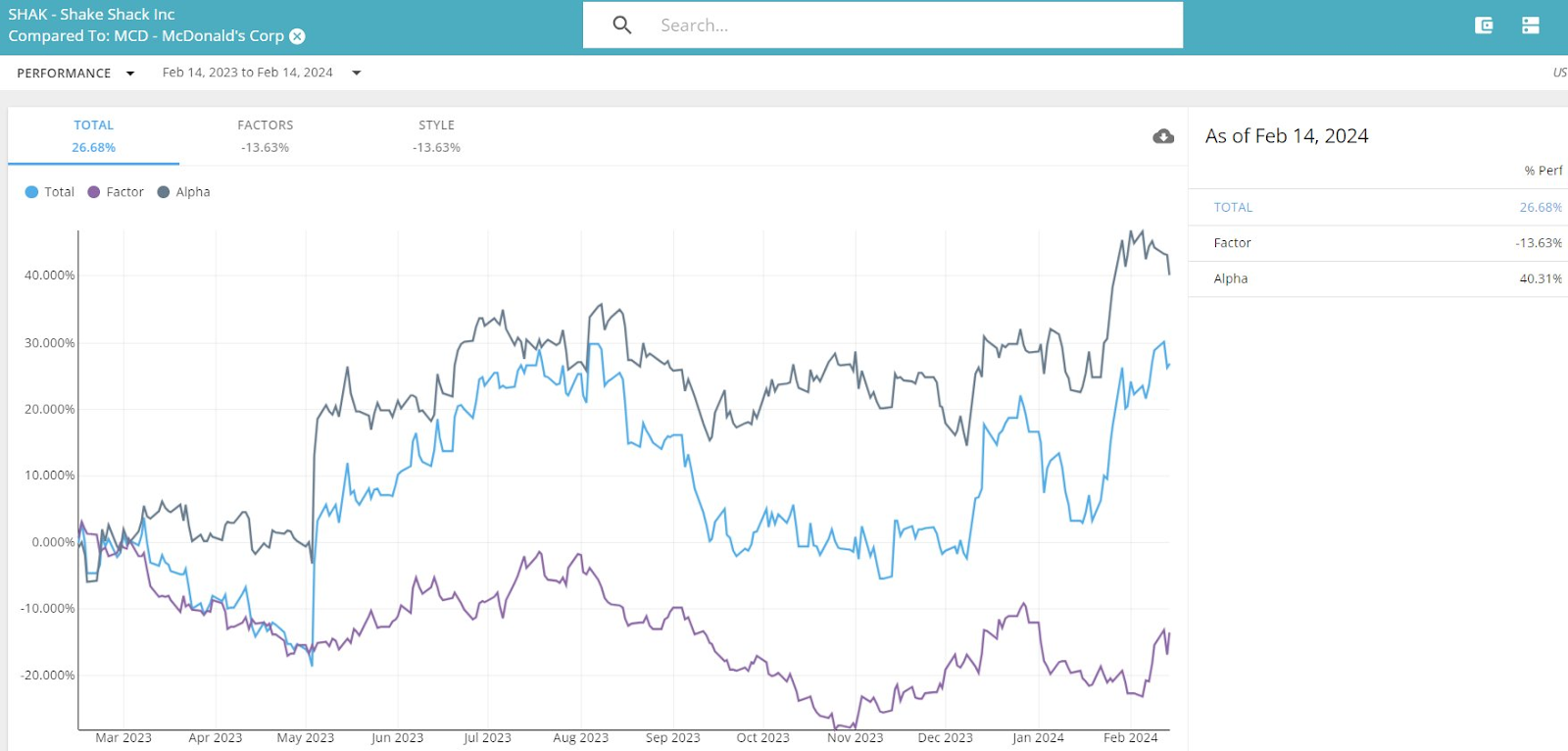

Lumida Call: Shake Shack

Shake Shack had a 30% bump on the day it announced earnings..

We pointed on February 15th on X out that a market-neutral pair trade that was long Shake Shack and short McDonald’s has generated 40 points of alpha in one year.

This thesis we file under our ‘Legacy Brands are in Decline’.

Quick callout - Reddit is going public under the symbol $RDDT

Quick stats:

$804 million in annual sales for 2023

100,000 communities

3M daily active users

$10B valuation

On Nvidia

We wrote on 4/30: ‘When does Nvidia replace Netflix in FAANG?’

I believe we can say that’s official now.

When the market bottomed in Oct of 2022, NVDA had a market cap of $280bn and a 12-month forward P/E of 32x.

Nvidia added $276bn of market cap this past Thursday. The P/E is now 33x.

Nvidia is growing earnings roughly in lock-step with its stock price.

The wild part about Nvidia is not the revenue growth.

It's that Nvidia is likely once again cheaper than Apple on a forward PE basis.

Earnings grew much faster than the stock price bump.

I remain of the view that the best names to own in Mag 7 are: Nvidia, Meta, and Google.

Definitely no Apple and Tesla.

Amazon is lukewarm, but why own it if you have higher conviction names.

On Semiconductor Policy:

“The US will need a ‘CHIPs Act 2’ to continue investing in semiconductor manufacturing to regain global leadership and meet demand for AI, said Commerce Secretary Raimondo, referring to the 2022 CHIPs Act, which set aside $39 billion to support the sector. She said the US fell “pretty far” behind. “We took our eye off the ball.”

When the government is spending on these companies, it’s hard not to be anything but bullish.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Company Earnings

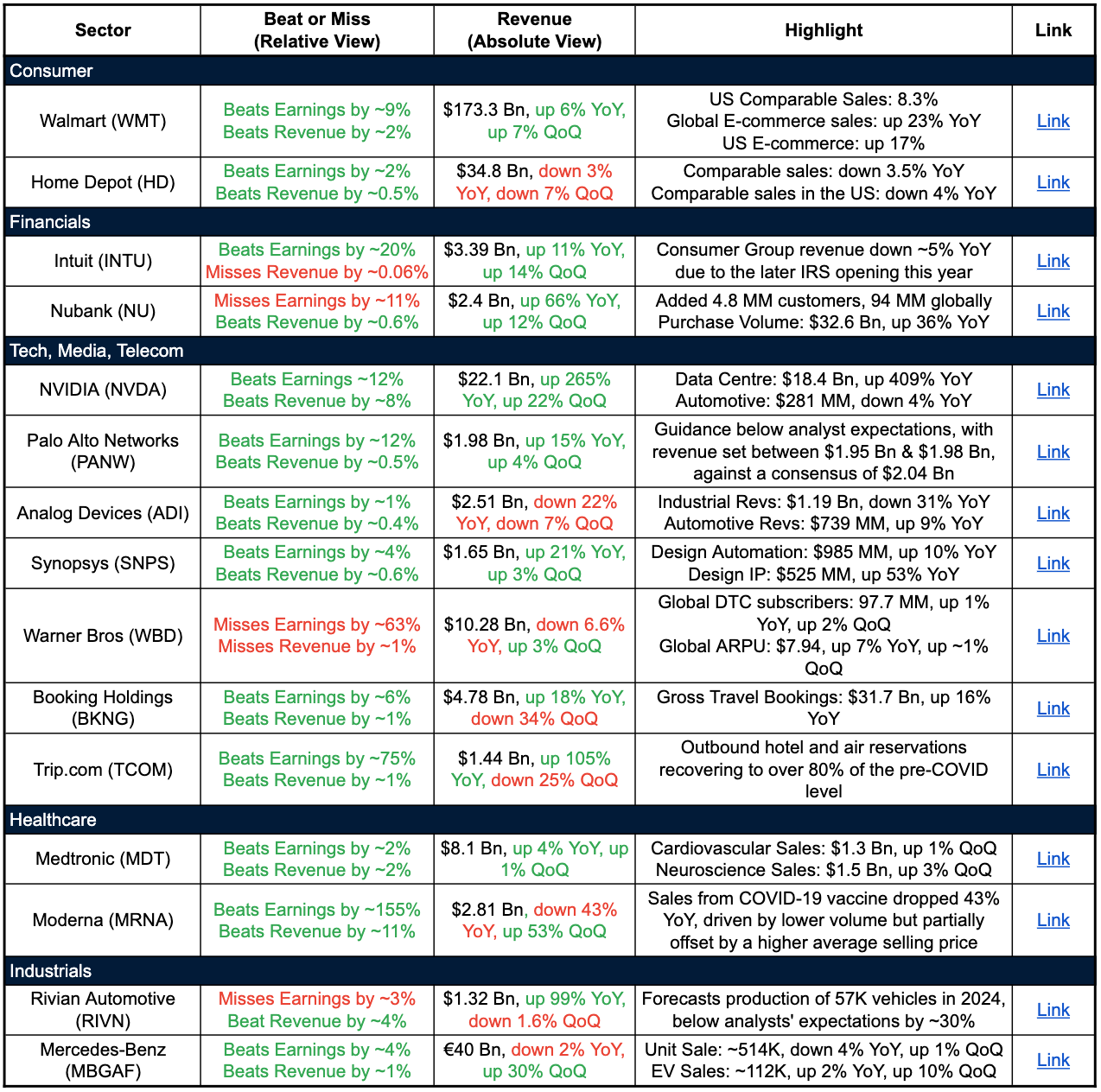

Broader Trends observations this earnings season:

Sellers to China are feeling the pinch

We saw this with Apple and Starbucks

Earnings present a mixed picture on the macroeconomy. Tech seeing continued growth while others like consumer discretionary face headwinds from inflation and economic uncertainty.

Consumer fundamentals remain relatively healthy. Demand looks strong in e-commerce and technology.

Consumer:

Companies reported: WMT, HD

Walmart benefited from value positioning while Home Depot saw declining sales as consumers pull back discretionary spend

Financials:

Companies reported: INTU, NU

Intuit saw growth in small business segment but decline in consumer revenue due to delayed IRS opening

Nubank continues rapid customer acquisition but competition is increasing

Rising interest rates benefit net interest income for financial institutions

Tech:

Companies reported: NVDA, PANW, SNPS, WBD

NVIDIA saw huge growth in data center/AI segment, robust enterprise cloud demand.

Warner Bros witnessed plateauing streaming subscriptions.

Healthcare:

Companies reported: MDT, MRNA

Steady growth driven by device sales

Vaccine (COVID) related sales drop, driven by lower volumes

Auto:

Companies reported: RIVN, MBGAF

EV demand up but, Rivian missed production forecasts as supply chain issues persist

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Digital Assets

We will be interviewing Michael Terpin, a Bitcoin OG, in early March to commemorate his book.

Don’t forget to subscribe to our Youtube Channel

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

On AI

Sam Altman asking for trillions to design semiconductors lands differently after Nvidia’s results

Nvidia is growing revenues far, far faster than OpenAI — and at much larger scale

OpenAI, and the application layer more generally is 1 of N (where N is large), whereas the capex receiver layer is full of monopolies

Sam is FOMO’ing into the Silicon Layer.

It’s hard to see how Sam can close the gap. The moat Nvidia has with the CUDA library is significant.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Quote of the Week

"Don't look for the needle in the haystack. Just buy the haystack!" — John Bogl

If you enjoy the Lumida Ledger, please forward share with a friend or subscribe.

If you’re interested in learning more about Lumida’s wealth management services, click to explore becoming a client

Disclaimer: Lumida Wealth Management LLC (‘Lumida”) is located in New York, NY, and is an SEC registered investment adviser. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability. Lumida only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Any direct communication by Lumida with a prospective client will be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides.

The information in this material has been obtained from sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated in this material are accurate and that the forecasts, opinions and expectations contained herein are fair and reasonable, Lumida, Inc. and Lumida Wealth Management LLC (collectively Lumida) make no representations or warranties whatsoever the completeness or accuracy of the material provided, except with respect to any disclosures relative to Lumida. Accordingly, no reliance should be placed on the accuracy, fairness or completeness of the information contained in this material. Any data discrepancies in this material could be the result of different calculations and/or adjustments. Lumida accepts no liability whatsoever for any loss arising from any use of this material or its contents, and neither Lumida nor any of its respective directors, officers or employees, shall be in any way responsible for the contents hereof, apart from the liabilities and responsibilities that may be imposed on them by the relevant regulatory authority in the jurisdiction in question, or the regulatory regime thereunder. Opinions,forecasts or projections contained in this material represent Lumida’s current opinions or judgment as of the day of the material only and are therefore subject to change without notice. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions or any other publicly available information. There can be no assurance that future results or events will be consistent with any such opinions, forecasts or projections, which represent only one possible outcome. Furthermore, such opinions, forecasts or projections are subject to certain risks, uncertainties and assumptions that have not been verified, and future actual results or events could differ materially. The value of, or income from, any investments referred to in this material may fluctuate and/or be affected by changes in exchange rates. All pricing is indicative as of the close of market for the securities discussed, unless otherwise stated. Past performance is not indicative of future results. Accordingly, investors may receive back less than originally invested. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. The recipients of this material must make their own independent decisions regarding any securities or financial instruments mentioned herein and should seek advice from such independent financial, legal, tax or other adviser as they deem necessary. Lumida may trade as a principal on the basis of its views and research, and it may also engage in transactions for its own account or for its clients’ accounts in a manner inconsistent with the views taken in this material, and Lumida is under no obligation to ensure that such other communication is brought to the attention of any recipient of this material. Others within Lumida may take views that are inconsistent with those taken in this material. Employees of Lumida not involved in the preparation of this material may have investments in the financial instruments or securities (or derivatives of such financial instruments or securities) mentioned in this material and may trade them in ways different from those discussed in this material. This material is not an advertisement for or marketing of any issuer, its products or services, or its securities in any jurisdiction.Qui